Author: Rhythm BlockBeats

Original Title: If the US and Iran Don't Reach an Agreement in 5 Days, What Other Cards Does Trump Have?

On March 23, Trump announced a 5-day suspension of strikes on Iran's energy infrastructure, claiming that there had been "very good, productive dialogue" and "major points of consensus" between the US and Iran. Upon the news, Brent crude fell from $112 to $99.94, a single-day plunge of 10.92%, the largest single-day drop since the start of Epic Fury.

However, Iranian Parliament Speaker Mohammad Bagher Ghalibaf denied the same day that any direct negotiations had taken place. Turkey, Egypt, and Pakistan are acting as intermediaries to relay messages, with Kushner and Witkof coordinating, but there is disagreement even on the basic fact of "whether talks are happening."

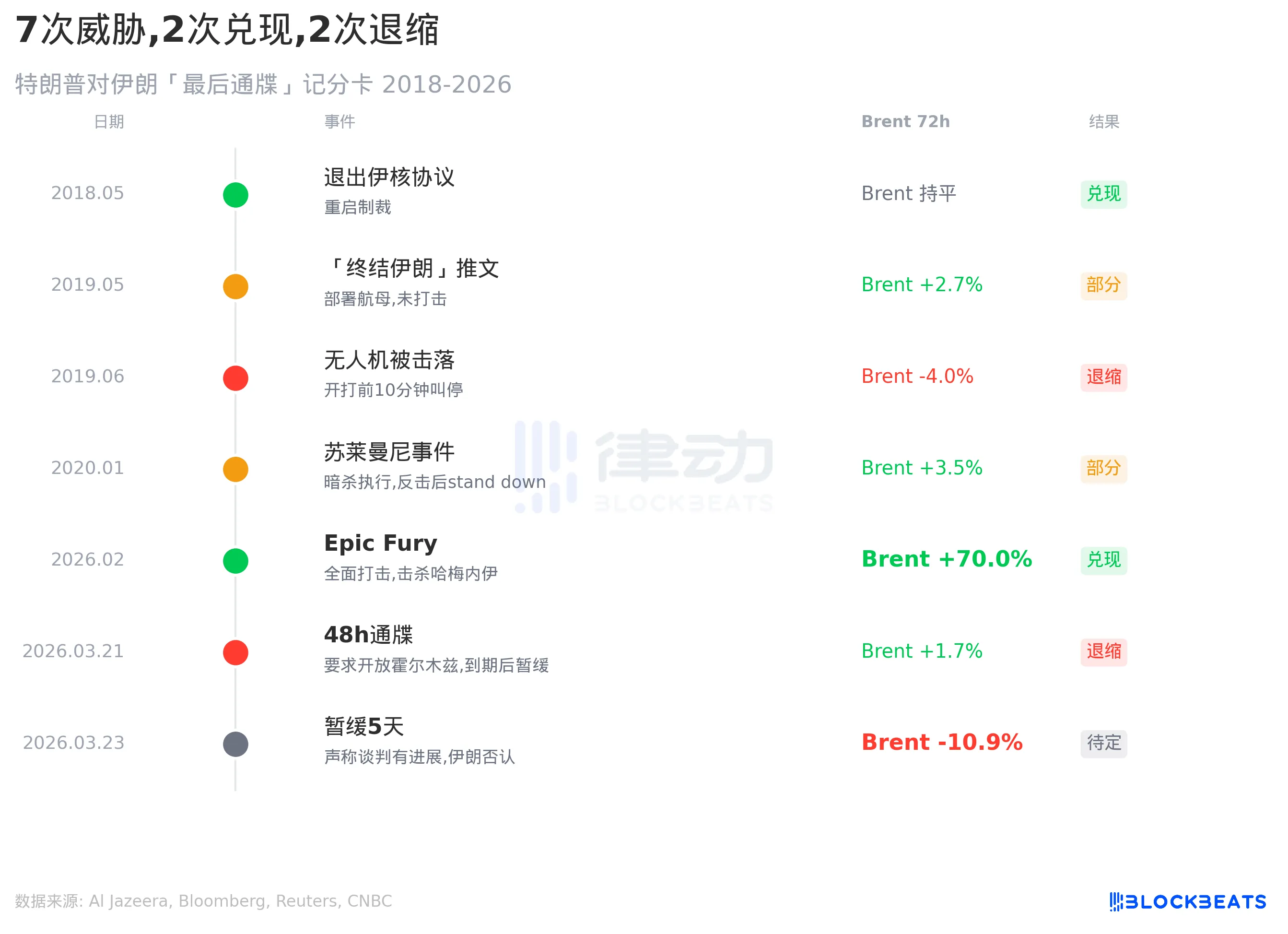

On the Iran issue, this is not the first time Trump has issued an "ultimatum" and then stepped back. From 2018 to now, a similar pattern has occurred 7 times.

7 Threats, 2 Delivered

Laying out all of Trump's major threats against Iran from 2018 to the present reveals a clear pattern.

In 2018, he withdrew from the JCPOA, followed through, and sanctions were reinstated as scheduled. In February 2026, he launched Epic Fury, also followed through, killing Khamenei within 24 hours and destroying over 70% of Iran's missile launchers (according to Israeli intelligence assessments). These two were fully delivered, with oil prices reacting violently; Epic Fury drove Brent from $71 to $119.50, a 70% increase.

But the other side is equally prominent. In June 2019, after Iran shot down a US drone, Trump ordered strikes on Iranian radar and missile sites; the military was "cocked and loaded," but he called it off 10 minutes before launch. On March 21, 2026, he issued a 48-hour ultimatum to Iran to reopen the Strait of Hormuz; when it expired, he didn't strike, instead switching to a "5-day suspension."

Out of 7 instances, 2 were fully delivered, 2 were partially executed, 2 were退缩 (stepped back), and 1 is pending. The market's response is also changing. After the 2019 strike call-off, oil prices fell back only 3-5%. This time, with the 5-day suspension, oil prices directly fell 10.92%. The market's reaction amplitude to "suspension" type signals is放大 (amplifying), because investors are increasingly quickly pricing in the "threat devaluation."

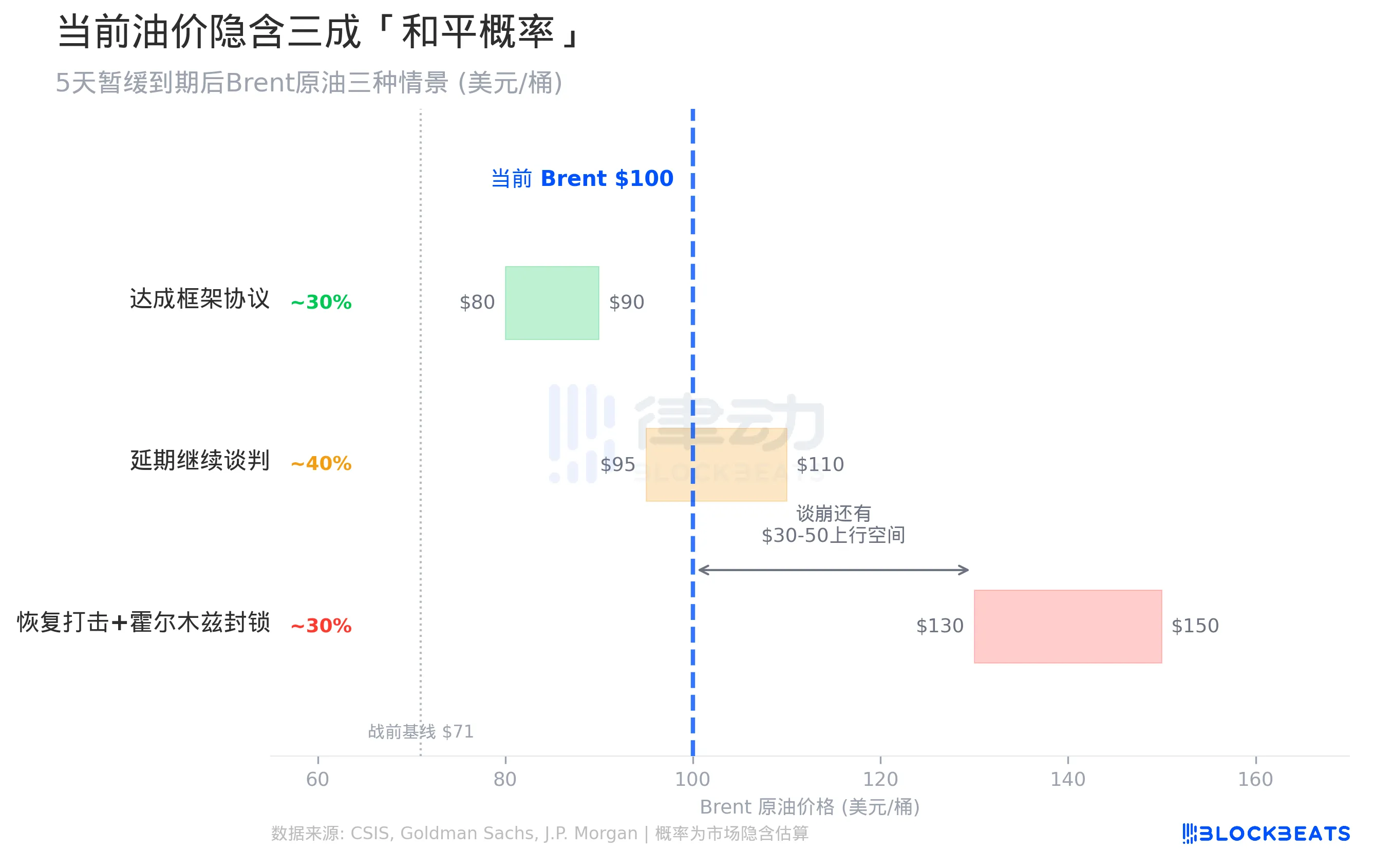

What $100 Oil is Saying

After the 5-day window expires, there are three paths.

First, reaching some kind of framework agreement. Not a comprehensive deal, more likely a 30-60 day temporary freeze to buy time for后续 (follow-up) negotiations. In this scenario, Brent could fall back to the $80-90 range, close to Goldman Sachs' 2026 average price forecast of $85.

Second,延期 (extending) and continuing talks. After the 5 days expire, neither striking nor signing, but换 (exchanging for) a new suspension window. Oil prices remain震荡 (oscillating) in the $95-110 range, with war risk premium neither eliminated nor increased.

Third, resuming strikes加上 (plus) continued blockade of the Strait of Hormuz. According to CSIS's scenario modeling, if Iran expands attacks on Gulf oil facilities after being struck, Brent could surge to $130-150. Goldman Sachs' extreme scenario is more aggressive: if the Hormuz blockade lasts 60 days and Middle East production is长期 (long-term) reduced by 2 million barrels/day, oil prices could break the 2008 historical high of $147.

The current $100 Brent pricing roughly implies about a 30-40% probability of "reaching an agreement." Put another way, the market believes there is a 60-70% chance that the situation will not fundamentally improve after 5 days. If talks collapse, oil prices have another $30-50 of upside potential.

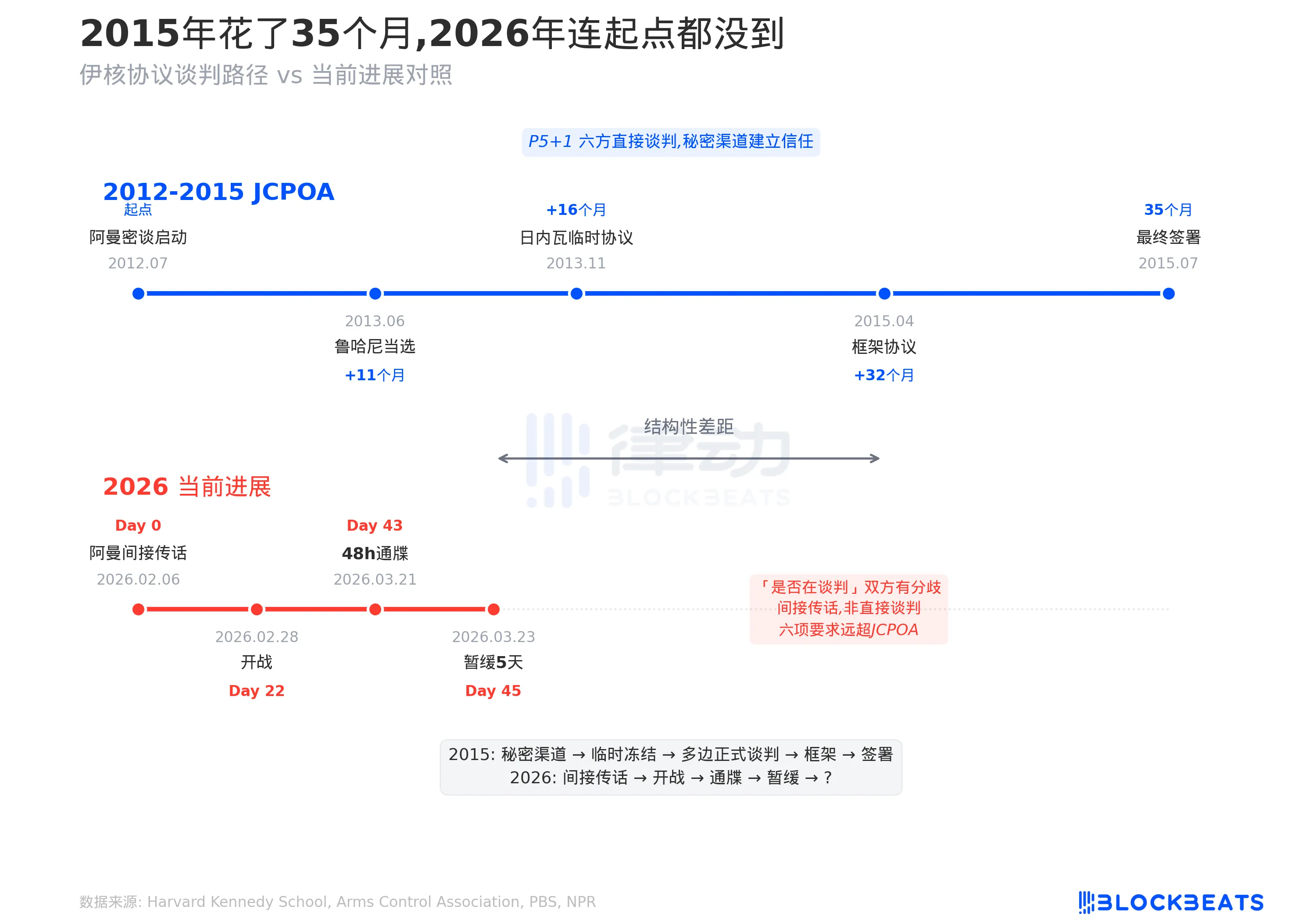

The 2015 Negotiations Took 35 Months

Trump's six core demands include zero uranium enrichment, dismantling nuclear facilities, a 5-year freeze on missile development, stopping funding proxy militias, recognizing Israel's right to exist, and US physical custody of Iran's stockpile of highly enriched uranium. This set of demands far exceeds the framework of the 2015 JCPOA. The当年的 (that year's agreement only limited enrichment levels to 3.65%, kept facilities operational, and did not address missiles or proxy militias.

The 2015 JCPOA started with secret contacts in Oman in July 2012 and took 35 months until the final signing in Vienna. In between, there was Rouhani's election bringing pragmatists to power, the interim Geneva agreement building trust, and 20 rounds of direct P5+1 six-party negotiations.

Where is the progress in 2026? There was one indirect message relay through Oman on February 6th, then the war started on February 28th. As of the March 23rd suspension, only 45 days have passed, and the two sides don't even agree on "whether negotiations are happening." The intermediary structure involves Turkey, Egypt, and Pakistan separately relaying messages, not the multilateral direct谈判 (negotiations) of P5+1. The precondition for谈判 (negotiations) (both sides acknowledging their existence) isn't even met yet, whereas the 2015 path used secret channels to build trust for over a year before entering public谈判 (negotiations).

If No Deal, What Other Cards Does Trump Have?

The military card is the most direct. Power plant strikes are the direct object of the 5-day suspension; resuming strikes has the lowest operational threshold. More升级 (escalated) options include blockading or occupying Kharg Island; Al Jazeera reported on March 20th that plans were already being discussed. Kharg handles 90% of Iran's crude exports, about 1.3-1.6 million barrels/day (according to EIA data). Regarding nuclear facilities, Natanz was damaged in the first week of the war, Fordow's highly enriched uranium has not been moved since being struck in June 2025 (according to FDD analysis), but Iran's new Pickaxe Mountain facility, built 100 meters underground in granite near Natanz, is beyond the reach of airstrikes. Currently, the US military has deployed 2 carrier strike groups, over 16 surface vessels, and more than 100 aircraft in the Middle East (according to Military Times), the largest scale since the 2003 Iraq war.

On the economic card, Trump announced in January a 25% tariff on countries doing business with Iran. The main targets are China (over 90% of Iran's oil trade), as well as India, the UAE, and Turkey. Iran's current oil exports are still 1.5-1.6 million barrels/day, with daily revenue of about $140 million (according to Defense News data).

Cyber warfare is already underway. According to Foreign Policy报道 (reporting), before the Epic Fury kinetic strikes, US Cyber Command had already launched "non-kinetic effects," paralyzing parts of Iran's communication and early warning systems.

But Iran is not without counter-cards. According to US Defense Intelligence Agency (DIA) assessments, Iran can maintain a blockade of the Strait of Hormuz for 1-6 months. The Strait of Hormuz sees 20 million barrels of crude and refined products pass through daily, accounting for 20% of global oil consumption (according to EIA data), while Saudi Arabia and the UAE's pipeline bypass capacity is only 3.5-5.5 million barrels/day, leaving a huge gap of 14.5 million barrels/day. Iran still has about 1,500 ballistic missiles and 200 launchers (according to Israeli military estimates), and Hezbollah holds about 25,000 missiles (according to Israeli assessments).

This is the underlying博弈 (game theory) logic of the 5-day window. Trump faces a credibility trap: if he strikes, oil prices could spiral out of control, putting pressure on the domestic economy. If he doesn't strike, the cycle of ultimatums and suspensions will further weaken the pricing power of military threats. Iran's dilemma is对称 (symmetrical): if they talk, domestic hardliners won't agree. If they don't talk, the next round of strikes could target power plants and Kharg Island. The March 28th expiration date is not the end point; it's the next flip of this trap.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush