Author: Eric, Foresight News

Original Title: The Same Judge, Different Outcomes for Uniswap and Tornado

At 3 a.m. Beijing time on March 3, the class action lawsuit demanding that Uniswap and its founder Hayden Adams be held responsible for scam tokens on Uniswap was dismissed by the U.S. District Court for the Southern District of New York. Brian Nistler, General Counsel of the Uniswap Foundation, called it a "landmark ruling for DeFi."

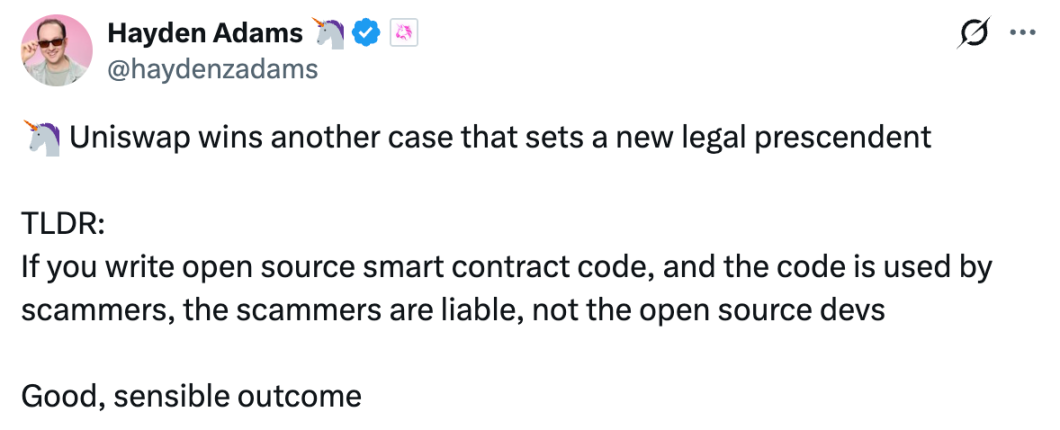

Hayden Adams also tweeted, "If you write open-source smart contract code and that code is used by scammers, the scammers are responsible, not the open-source developers. This is a reasonable and just outcome."

For Web3 developers, this is undoubtedly good news. But little known is that the judge who made this "just ruling" is the same person who, during the tenure of the former SEC chairman, found the developers of the mixer Tornado Cash guilty.

The Final Verdict

Nearly four years have passed since the class action lawsuit against Uniswap was filed and today's final resolution.

In April 2022, Uniswap users, represented by Nessa Risley, filed a class action lawsuit in court, accusing defendants Paradigm, a16z, Uniswap, and its founder Hayden Adams of violating federal securities laws by issuing and selling unregistered securities, including UNI, in the form of tokens on Uniswap. Additionally, the defendants failed to register Uniswap as an exchange or broker-dealer under applicable securities laws and did not provide investors with registration statements for the securities they issued and sold.

This lawsuit was initiated by the law firms Kim&Serritella and Barton, representing users who traded EtherumMax, Bezoge, MatrixSamurai, Alphawolf Finance, RocketBunny, and BoomBaby.io tokens on Uniswap between April 5, 2021, and April 4, 2022.

The phrase "unregistered securities" had extraordinary destructive power in the crypto industry at the time, but this lawsuit unexpectedly and quickly tilted in Uniswap's favor.

Presiding Judge Katherine Polk Failla, while agreeing that the so-called "scam tokens" were indeed securities, ruled that Uniswap did not need to be held responsible. Failla argued that Uniswap's decentralized nature meant the protocol had no control over which tokens were listed on the platform or who could interact with it. "The case is more like holding the developer of an autonomous vehicle responsible for traffic violations or bank robberies committed by third parties using the car."

Based on this, Failla dismissed the federal securities law charges in August 2023. The plaintiffs then appealed, and the Second Circuit Court of Appeals affirmed the dismissal of the federal part in 2025 but remanded the state law part for retrial.

Subsequently, the plaintiffs amended the complaint and sued again. This time, the losing investors accused Uniswap and other defendants of aiding and abetting fraud, making false statements, profiting from transactions involving scam tokens, and violating fraud laws in multiple states.

After another review by the same judge, Failla, the amended claims were dismissed again, with no further amendments allowed, bringing the case to a complete end.

The judge's reasoning this time was largely the same as before: Uniswap was unaware of the scam tokens, and even if it were aware, it did not provide substantial assistance. It also did not meet the definition of fraudulent behavior under any state law. Regarding unjust enrichment, Uniswap did not gain direct benefits, and the speculative indirect benefits from such scam activities expanding the user base were too tenuous.

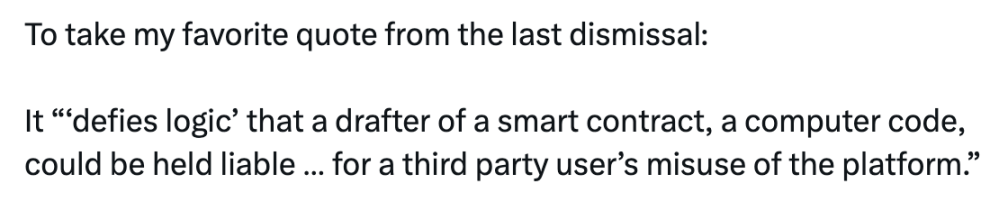

Brian Nistler stated in a tweet, quoting a line from the previous ruling, that it "defies logic" to hold the drafter of a smart contract responsible for the abusive actions of third-party users on the platform.

Tornado Cash's Different Outcome

Facing the same judge, Roman Storm of Tornado Cash met a different fate.

Tornado Cash was first added to the sanctions list by the U.S. Treasury Department's Office of Foreign Assets Control (OFAC) on August 8, 2022, accused of helping criminals, including North Korean hackers, launder over $7 billion. Two days after being added to the sanctions list, Dutch police arrested Alexey Pertsev, one of Tornado Cash's core developers.

On May 14, 2024, a Dutch court found Alexey Pertsev guilty of money laundering and sentenced him to 64 months in prison. The court ruled that Pertsev was aware that the platform he developed and operated was used for crime but did nothing to stop it, subjectively acquiescing to Tornado Cash being used as a money laundering tool. Alexey Pertsev is still appealing, but there have been no recent updates.

Seven months before Alexey Pertsev was found guilty, the U.S. Department of Justice sued two other developers, Roman Storm and Roman Semenov, in the Southern District of New York. Roman Storm was previously arrested in Washington State, while Roman Semenov remains at large.

Roman Storm in court

Although an appeal later determined that OFAC's sanctions against Tornado Cash were an overreach and invalid, Roman Storm still found himself in the defendant's seat last July. After a trial presided over by Judge Katherine Polk Failla, the jury found Roman Storm guilty of "conspiracy to operate an unlicensed money transmitting business," though sentencing has not yet been formally announced.

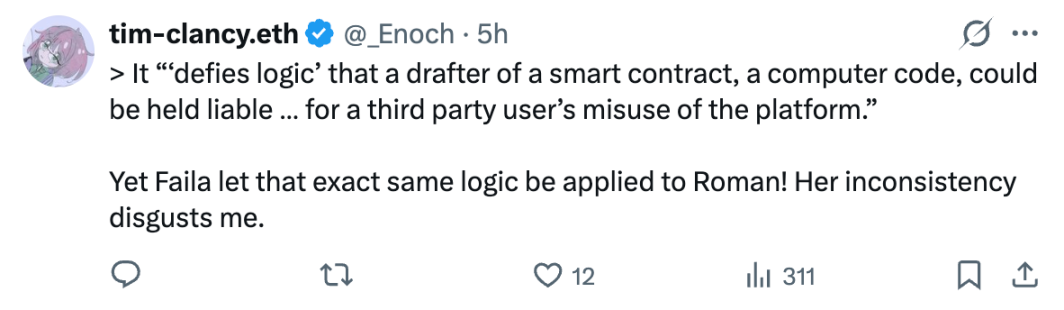

Under Brian Nistler's tweet celebrating Uniswap's victory, a comment by Sigil developer tim-clancy.eth criticizing Failla's contradictory rulings (the verdict against Roman Storm was actually made by a jury) received the most likes among all comments.

Decentralization Is Fine, but Privacy Is Not

I am not a professional lawyer, but setting aside political factors and from a simple emotional perspective, I can roughly understand why Uniswap and Tornado Cash had different outcomes.

The core reason is that Tornado Cash's developers should have been well aware that mixers would inevitably be used for money laundering. This clearly reveals regulators' stance: decentralization is acceptable, but it must be traceable. Tether faced similar challenges, which is why it later began cooperating with money laundering investigations and added freezing capabilities.

Perhaps Roman Storm, behind bars, would feel unjust upon learning of today's ruling. But he should realize that even in a crypto-friendly U.S. under Trump's administration, platforms aiding North Korean state-level hackers in money laundering cannot be tolerated. The power of crypto today is still insufficient to challenge national authority.

Web3 practitioners decry the injustice faced by Tornado Cash's developers while cheering Uniswap's victory. In our eyes, the two protocols are not fundamentally different; in fact, Tornado Cash even excels in privacy protection. Uniswap's addition of front-end blocking for sanctioned addresses in 2022 sparked some debate. Now, it seems that permissionless operation within the existing legal framework may be the only way for decentralized protocols to survive.

But that said, did Uniswap really have no responsibility at all in these scam incidents?

Strictly logically speaking, as the judge's analogy suggests, you cannot hold Mercedes responsible for a bank's losses just because a robber used their car to rob a bank. However, from a business perspective, we tend to believe that giants should provide protection within their capabilities. Current security tools can already identify a large number of potential scam projects in advance. For these established projects that have reaped the benefits of Web3's development, simple screening is not troublesome.

Doing their part to protect investors is not a mandatory obligation, but it is a responsibility that ordinary investors hope Uniswap and others will actively shoulder.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush