This report is authored by Tiger Research. The discourse power within the decentralized finance (DeFi) lending sector is gradually shifting from project protocols to professional operating entities holding risk control decision-making authority. In essence, the industry entry now presents a single choice: to leverage others' research and judgment capabilities, to export one's own research and judgment capabilities, or to build and control these capabilities in-house.

Key Highlights

- A new asset management role is emerging within DeFi, marking the end of an era where the industry was solely dominated by protocols and community governance.

- While still in its early stages, capital flow and channel resources are rapidly converging towards top-tier risk operator teams. Their past practical performance is becoming a core reference standard for institutional entry.

- Three primary entry paths currently exist in the industry: channel distribution (with operator teams providing backend support), asset supply (onboarding real-world assets), and independent operation (building an in-house team to become a risk operator).

- The chosen entry path directly determines the entity's discourse power, required core competencies, and potential risks assumed.

- The industry's core decision is not whether to enter DeFi, but how to delineate authority and responsibility: which risk control decision rights to delegate externally, and which core authorities to retain control over.

I. Risk Operators: Professional On-Chain Asset Management Service Providers

Traditional finance has long achieved the separation of decision-making/research and trade execution responsibilities. As the crypto market matures, specialized professional entities have also formed for various segmented functions.

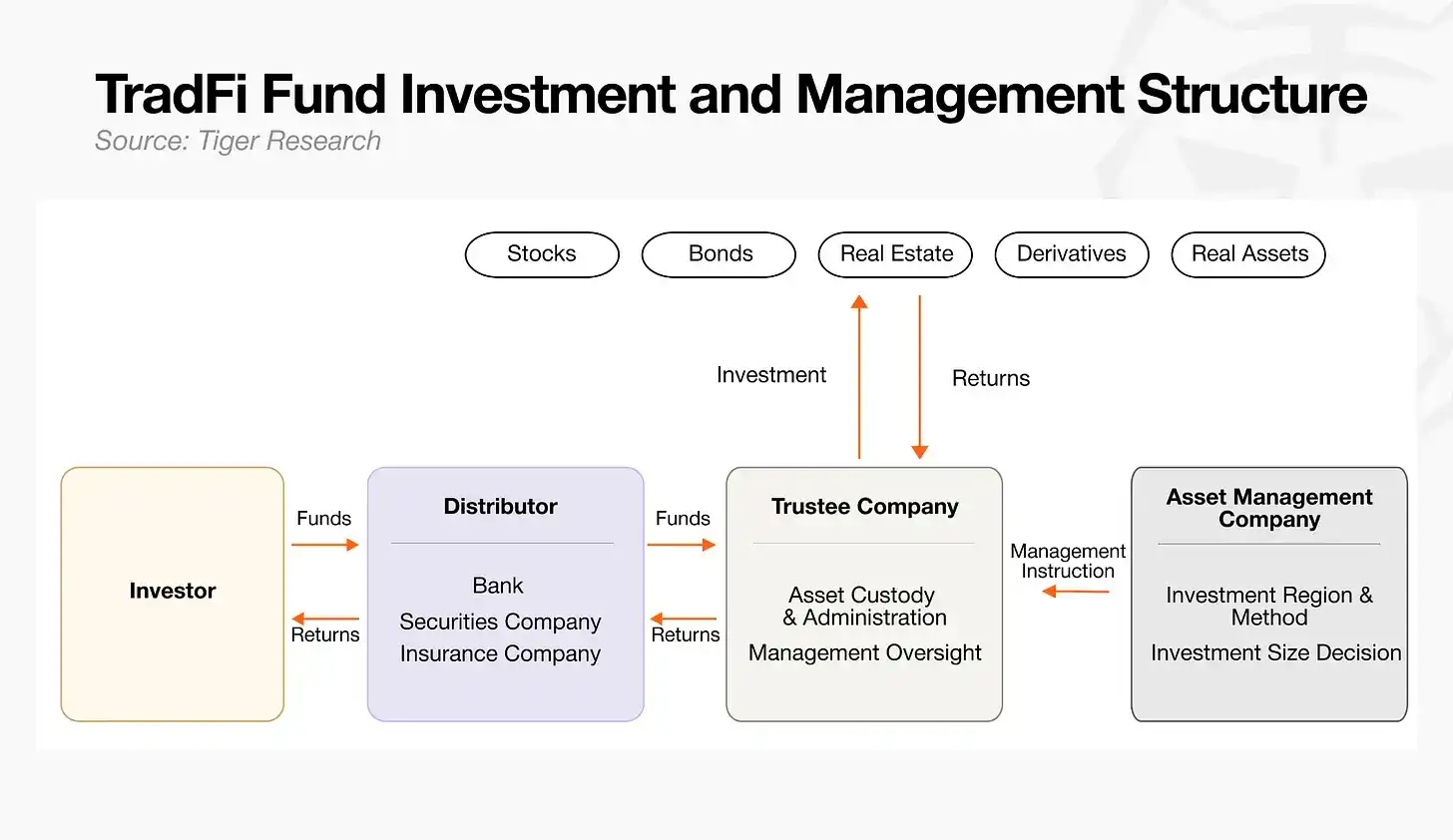

Traditional Finance Functional Division

- Asset Manager: The core decision-making hub for fund operation, formulating overall investment strategies and issuing specific execution instructions to custodians.

- Custodian: Responsible for asset safekeeping, strictly executing investment operations per the manager's instructions, and overseeing asset safety throughout the process.

- Distributor: Markets and sells fund products to investors, completing fundraising and capital aggregation.

The crypto industry has evolved a corresponding functional system. Early DeFi operated entirely on smart contracts, but market practice has proven that code alone cannot comprehensively mitigate all potential on-chain risks. To ensure the stable operation of on-chain lending businesses, a group of professionals specializing in complex risk assessment and coordinated allocation emerged—the risk operators—formally assuming the asset manager function within the on-chain ecosystem.

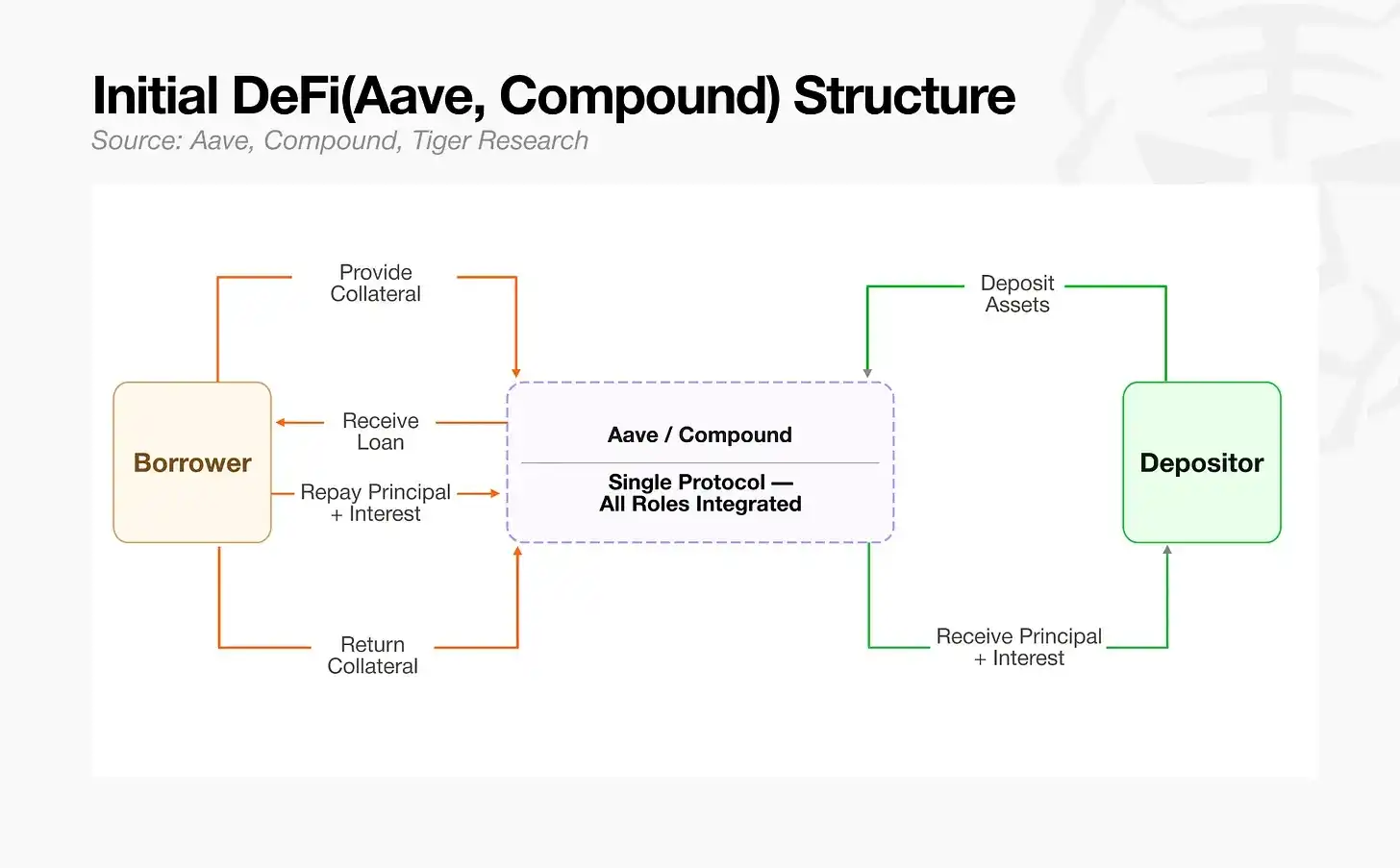

II. Early DeFi Lacked Professional Segmented Risk Control Roles

First-generation decentralized lending protocols like Aave and Compound deeply integrated the underlying lending infrastructure with risk control standards into a monolithic architecture. While there were practitioners related to risk operation at the time, all network assets were aggregated into a single pool. Practitioners could only act as global risk administrators for the protocol, making minor adjustments to overall risk parameters. Once highly volatile assets entered the pool, the single-pool structure was prone to risk contagion, where losses from a single inferior asset could rapidly spread throughout the entire ecosystem. The industry urgently needed specialized personnel to manage such chain-reaction risks.

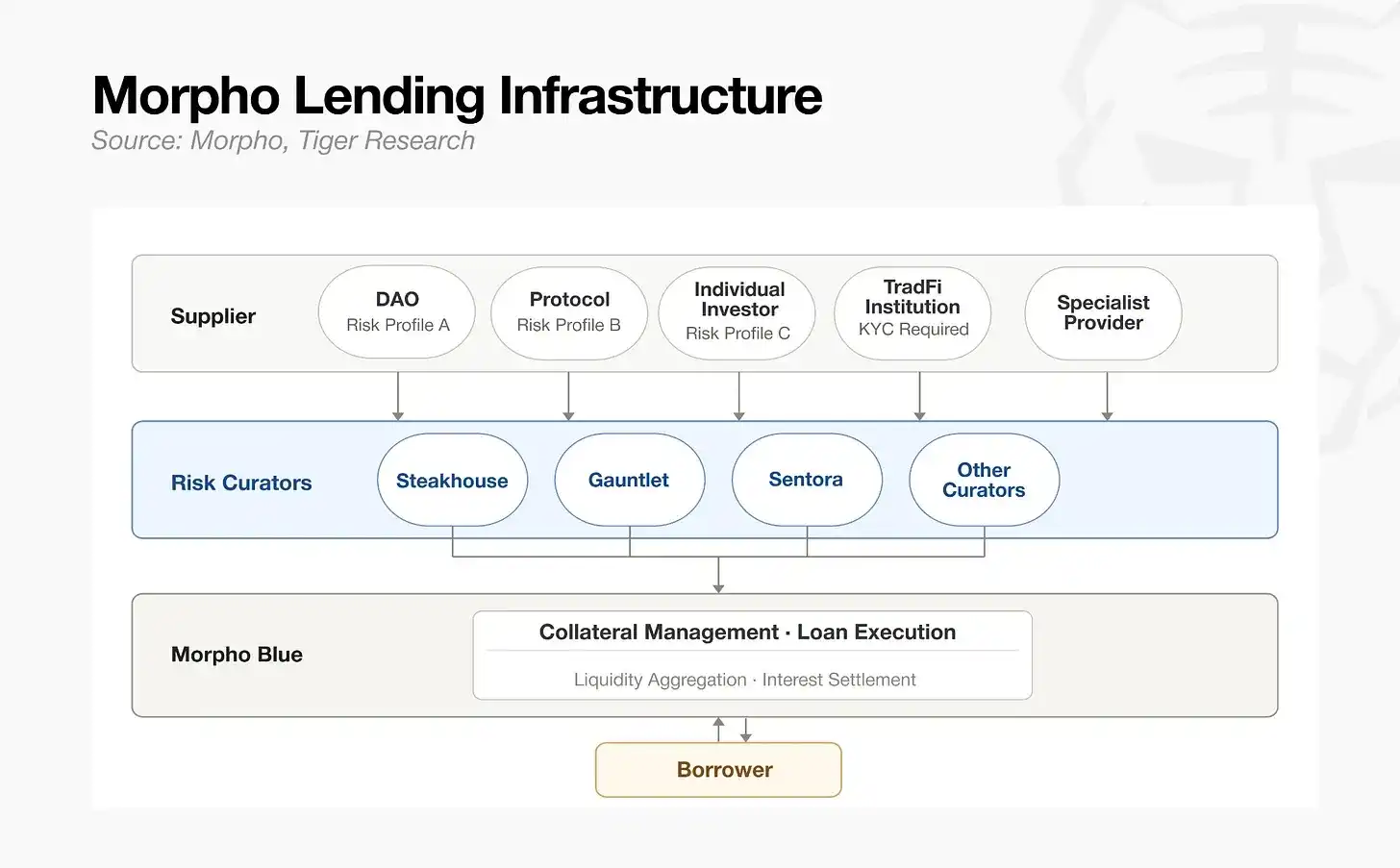

The industry landscape was fundamentally rewritten with the advent of Morpho. This project split collateral asset types and loan/bond terms into independent markets, replacing the traditional single pool with a modular multi-vault architecture, completely restructuring asset operation models. The function of risk operators consequently underwent a complete transformation. Practitioners were no longer confined to passive risk control within a fixed protocol framework. External professional teams could now autonomously formulate risk control rules and independently build and operate dedicated lending vaults. With the underlying infrastructure and risk assessment authority completely decoupled, risk operators officially transitioned from protocol-wide risk managers to professional asset operators in the crypto market, independently managing multiple sets of fund vault businesses.

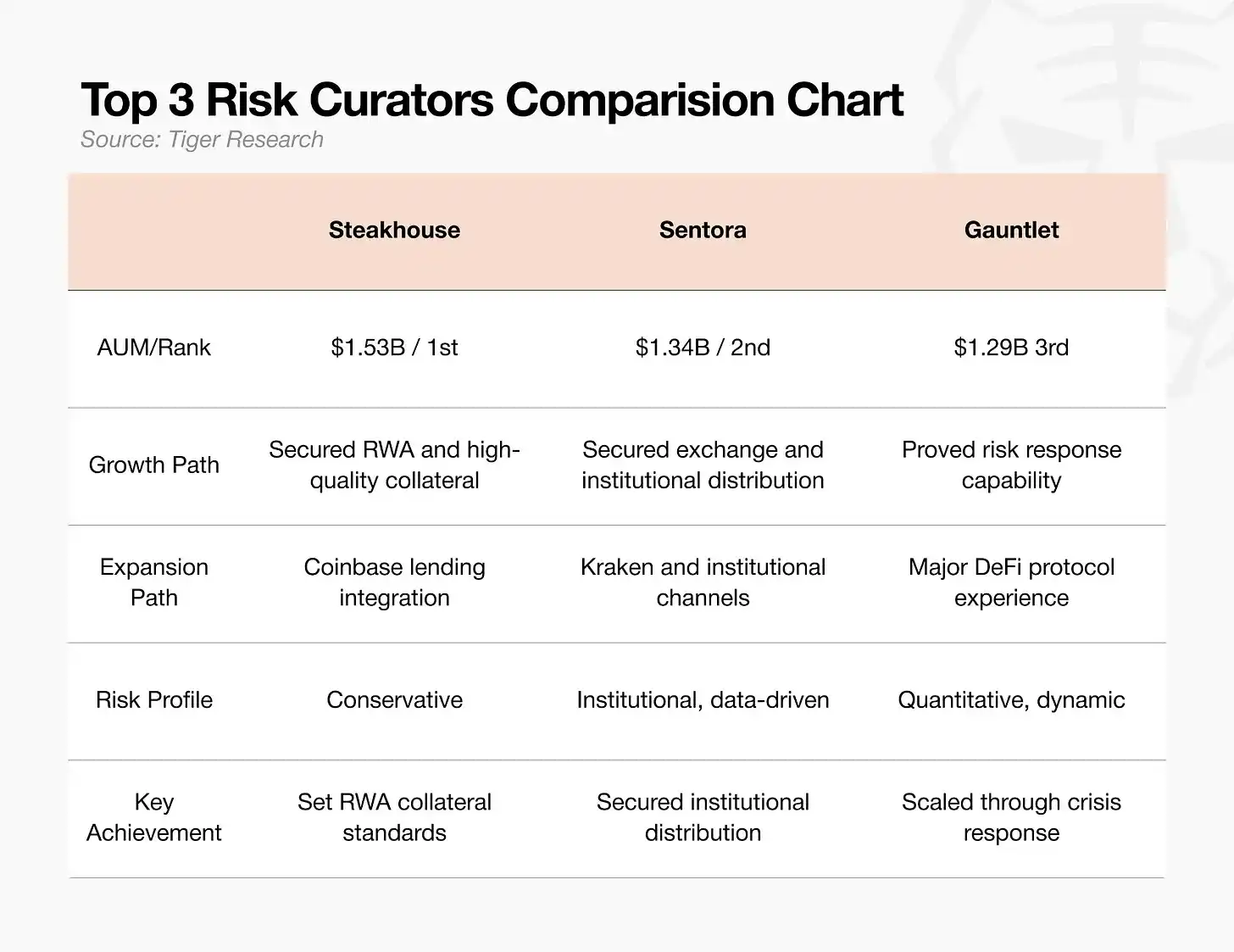

III. Current Landscape of Top Players

As of May 2026, the global risk operator sector manages approximately $70 billion in Assets Under Management (AUM), with the top three teams commanding 70% of the market share. This sector only entered an explosive growth phase in 2025, and capital has quickly concentrated towards capable teams. Capital highly favors operating entities with mature, proven track records.

The three leading teams have different entry paths:

- Steakhouse: A stable risk operator institution, pioneering the compliant onboarding of high-quality Real World Assets (RWA) like U.S. Treasuries for collateral. As the exclusive backend risk control partner for Coinbase's lending business, it possesses top-tier traffic channels. As of February 2026, its AUM reached $15.3 billion, ranking first in the industry. It also leads in defining the entry standards for compliant RWA collateral eligible for the DeFi ecosystem.

- Sentora: Built on AI-powered risk models and institutional-grade data systems, deeply integrated with Kraken exchange as a backend service provider, securing institutional capital inflow channels. With $13.4 billion AUM, ranking second, it focuses on bridging the capital flow between exchanges and institutional clients.

- Gauntlet: A veteran on-chain quantitative risk modeling institution, specializing in simulating various market risk parameters. In October 2025, it handled a massive $775 million inflow, abnormally repairing annualized returns within just 10 days. Its exceptional capability in managing large capital inflows and crisis handling is widely recognized. Currently managing $12.9 billion AUM, it is the industry benchmark for stabilizing large capital inflows.

Current sector competition has moved beyond mere AUM comparison. The core focus of contention has shifted to three key moats: collateral eligibility standards, capital distribution channels, and emergency risk response capabilities.

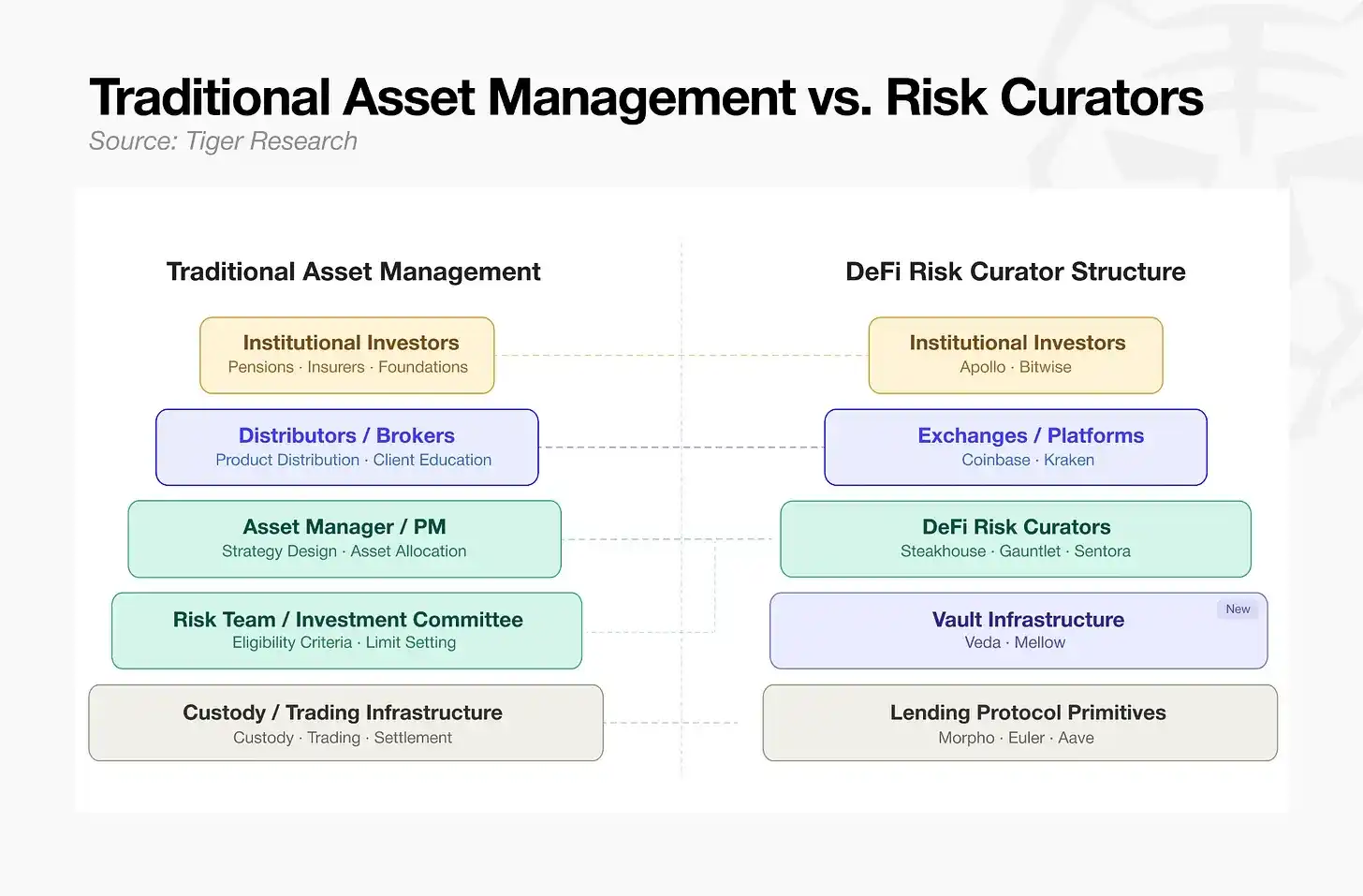

IV. Traditional Asset Management vs. DeFi Risk Operator System

With Morpho completing market modularization, different categories of collateral assets require independent professional teams for assessment and control. Professional risk teams like Steakhouse have consequently entered as dedicated DeFi risk operators, and DeFi operation models are gradually aligning with mature traditional asset management processes.

From top to bottom, the current DeFi infrastructure clearly replicates the full-process division of labor in traditional finance:

- Top Layer - Capital Raising & Distribution: Institutional investors are the core capital source. Massive funds flow into the on-chain ecosystem via major centralized exchanges and comprehensive service platforms, corresponding to the functions of brokers and distributors in traditional finance.

- Middle Layer - Strategy Formulation & Risk Control: Coordinated by DeFi risk operators planning fund operation models, analogous to portfolio fund managers and risk committees in traditional asset management, setting asset entry thresholds, position limits, and building overall fund operation strategies.

- Bottom Layer - Product Structuring & Custody: Utilizing fund vaults as vehicles to translate operational strategies into investable on-chain financial products. The underlying lending protocols are responsible for asset storage and on-chain settlement execution, undertaking the functions of asset custodians and transaction clearing infrastructure in traditional finance.

From capital raising and strategy operation to asset custody and settlement, the entire operational flow has comprehensively aligned with the mature traditional finance system. For traditional financial institutions, on-chain lending is no longer an unfamiliar emerging sector but a standardized market with clear logic and a well-established system, significantly lowering the entry barrier for institutions.

V. Benchmarking Traditional Asset Management: Sector Opportunity Distribution

After undergoing a traditional asset management-style functional split, on-chain lending has officially opened its doors to various institutions. However, entry barriers differ significantly across the sector's layers:

- Distribution Channel Layer: Directly facing the end-user market, leading crypto institutions have already established monopolies. Direct competition by traditional financial institutions offers low cost-effectiveness.

- Strategy Management Layer: The core competition lies in financial professional judgment capabilities and talent reserves. Asset risk assessment, control, and product packaging are core主营业务 of traditional asset management. Without needing to develop complex underlying technical systems, institutions can rely on mature modular infrastructure to deploy their own risk control systems, quickly establishing a stable profit-generating business model. This is the optimal entry point for the sector.

- Asset Custody & Underlying Infrastructure Layer: Focuses on blockchain technology R&D and implementation, belonging to a technology-intensive field with extremely high requirements for underlying public chain development capabilities. It is extremely difficult for traditional financial institutions to independently build systems to enter this layer.

Compared to other sectors relying on traffic resources or underlying technology, the strategy management and risk control layer has the lowest entry barrier. Traditional financial institutions, leveraging their decades-honed mature risk control systems, can rapidly capture a leading position in the industry.

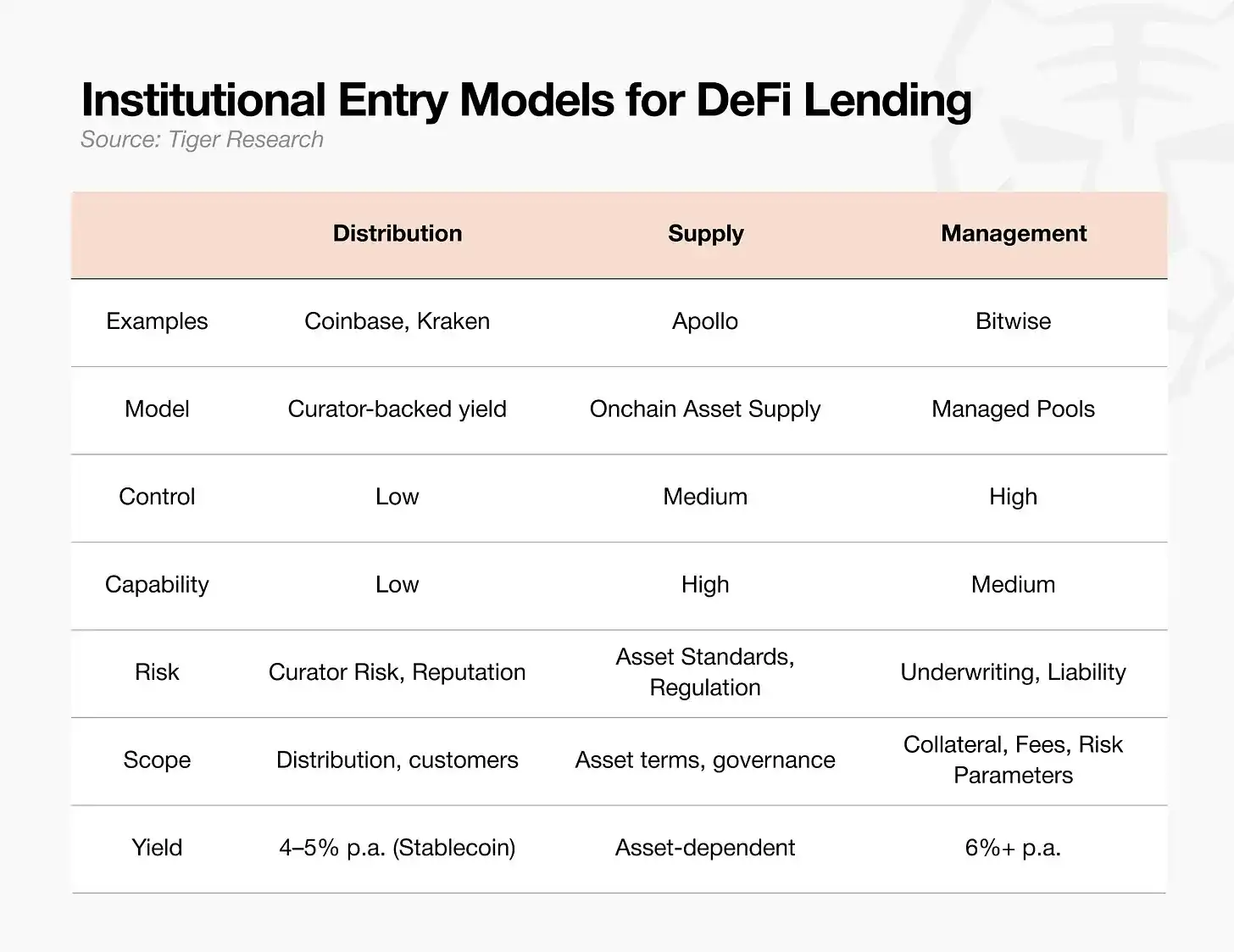

Currently, there are three main models for institutional entry into DeFi. Regardless of the chosen path, the sector's core competitive edge remains the professional risk assessment capability of the risk operator teams.

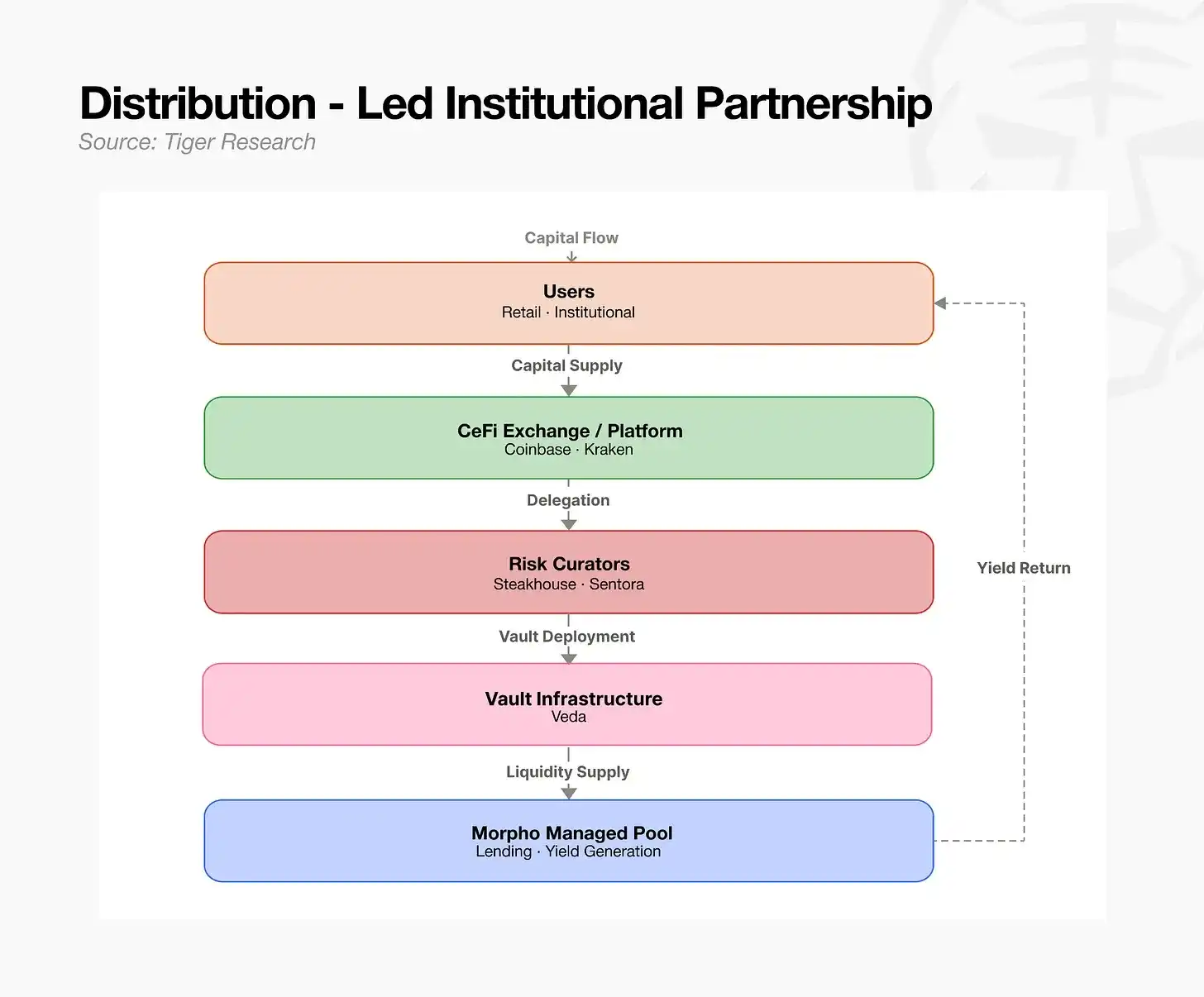

5.1 Channel Distribution Model: Leveraging Professional Teams as Backend

Leveraging mature external risk operator teams as backend services to quickly capture market share. Suitable for exchanges and fintech platforms with massive user traffic but lacking independent on-chain risk control operational capabilities. In this model, investment strategies are fully outsourced, but the brand reputation risk and operational responsibility risk brought by the partner team are still borne by the platform itself. Centralized exchanges holding end-user traffic and unwilling to independently delve into complex on-chain lending risk control businesses commonly adopt this model: connecting with authoritative, compliant external risk control teams as business backends to launch lending financial services. The platform is responsible for channeling large capital inflows using its own traffic, while collateral review and full-process risk control are entirely entrusted to the partner risk operator team.

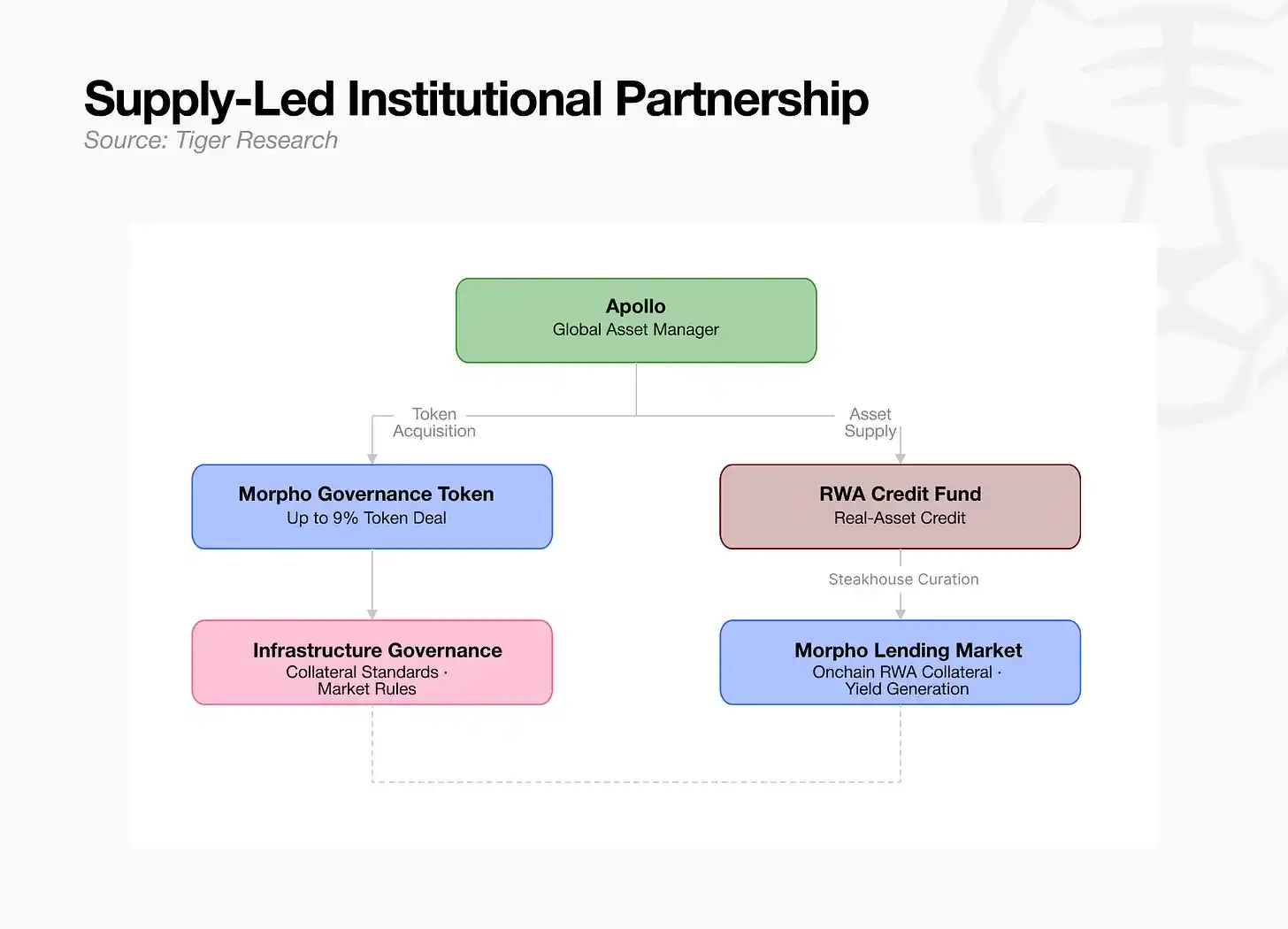

5.2 Asset Supply Model: Compliant Onboarding of Offline Premium Assets

Asset management institutions holding Real World Assets (RWA) or high-quality underlying credit assets directly channel their existing assets into the on-chain market. Taking Apollo as an example, while supplying assets on-chain, the institution also invests in governance tokens of lending protocols, deeply participating in setting industry collateral eligibility rules suitable for their own assets. The core challenge of this model lies in completing standardized compliance梳理 of assets and establishing完善配套监管适配体系. Large私募 institutions and offline实体 asset holders can directly connect their存量优质资产 to on-chain financial channels. Apollo goes beyond单纯的资产供给层面 by increasing holdings of governance tokens of leading lending protocols, deeply participating in industry rule-making, and promoting its own offline assets to become officially compliant collateral with higher market recognition and stronger risk control priority. However, asset suppliers cannot arbitrarily include any asset as collateral. The market requires professional third parties to objectively verify the true safety of assets, confirming they can be quickly and fully liquidated in on-chain清算 scenarios. This环节离不开风险操盘团队的严谨资质审核与信用背书. Ultimately, the long-term落地 of the asset supply model still relies on the asset management institution's own professional risk verification capabilities.

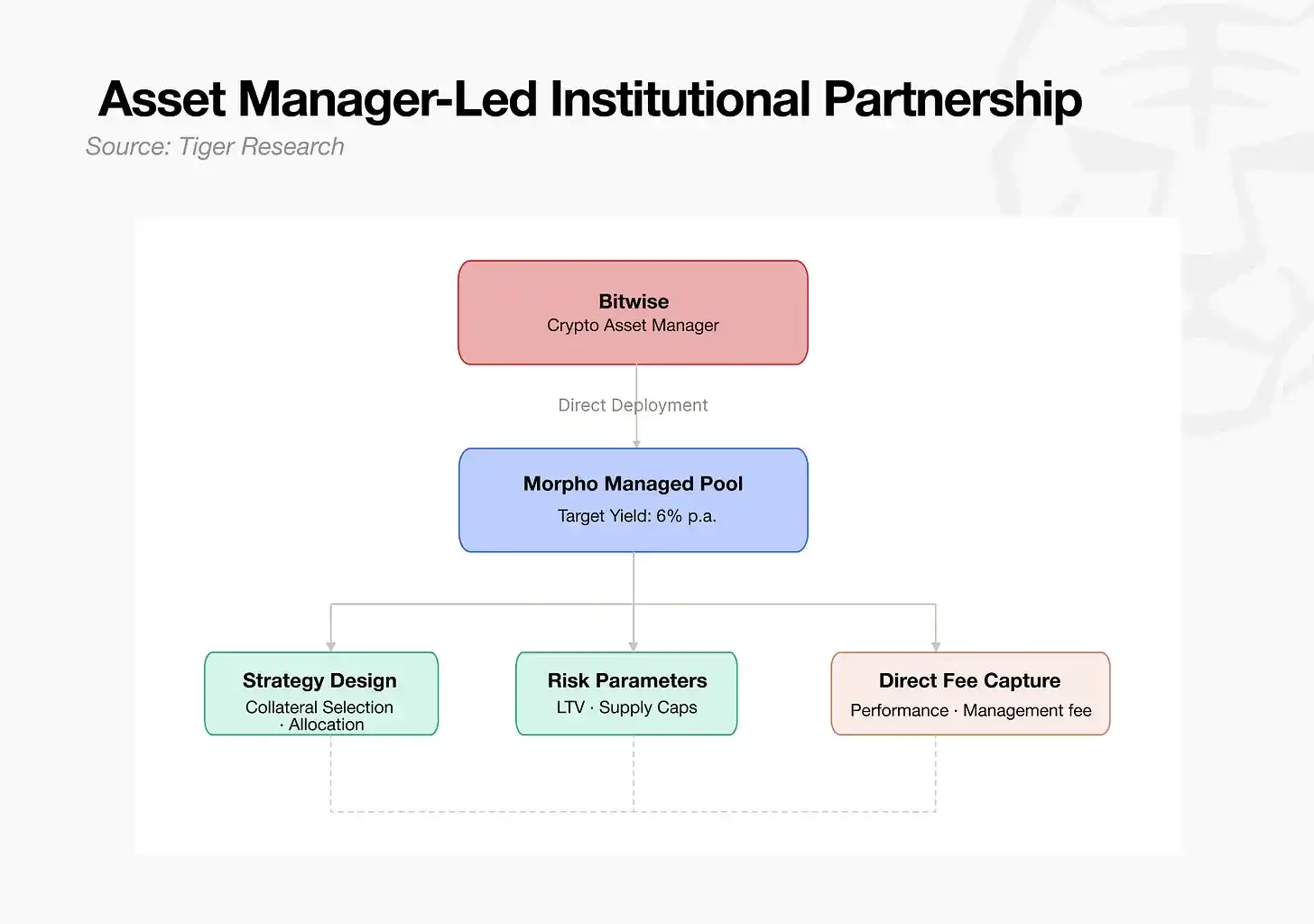

5.3 Independent Operation Model: Building an In-House Team to Become a Risk Operator (Representative Institution: Bitwise)

The asset management institution independently develops investment strategies and builds and operates its own dedicated on-chain fund vaults. Bitwise率先 defined on-chain fund vaults as Version 2.0 Exchange-Traded Funds (ETFs), formally entering the sector in depth. This model holds the highest autonomy over fee pricing and collateral eligibility standards, but all operational risks and losses are fully borne by the institution. It suits large asset management institutions that have组建自有专业风控团队. Traditional asset managers transforming into independent risk operators without relying on external platforms fall into this category. Bitwise leverages its mature asset portfolio construction system and risk control framework to independently design and fully control the operation of on-chain vaults, directly earning stable management fees on-chain.

VI. Industry Landscape on the Eve of Massive Traditional Capital Entry

From an industry development trend perspective, as the on-chain lending ecosystem continues to mature, traditional large asset management institutions possess the strongest advantages for sector entry. After the DeFi ecosystem completed its modular functional split, the market's core刚性需求 has shifted: the industry no longer acutely lacks smart contract development talent but极度渴求 the professional financial capabilities honed over decades in traditional finance, such as抵押品尽调审核 and risk limit setting. The practical risk control experience accumulated by traditional asset managers over decades can be seamlessly adapted and migrated to on-chain financial scenarios.

However, the current overall market size of DeFi is still unable to accommodate the direct, large-scale entry of the world's top-tier巨型资管机构: The global traditional asset management industry totals a staggering $147 trillion, with BlackRock alone managing around $14 trillion. In contrast, the entire crypto DeFi sector size is only about $80 billion, with the risk operator细分赛道规模 at merely $70 billion—less than 1/2000th of BlackRock's AUM.

This vast disparity in scale恰恰印证 the sector's immense future growth potential. Institutional capital has always prioritized risk control, entering only mature markets with完善风控体系. Once risk operator teams establish safe and stable on-chain capital流转体系, and配套行业监管框架落地成型, the industry will witness a qualitative leap. Even a微小资金分流 from the $147 trillion traditional asset management market could rapidly catalyze爆发式增长 for the $80 billion DeFi market.

Many industry红利 exist only during the sector's early development stages. Currently,全球优质头部风险操盘团队 are屈指可数. Large-scale institutional entry urgently requires完善成熟的行业运行规则. Teams that率先搭建行业底层运行体系 will牢牢掌握行业规则制定主导权. Later entrants, while benefiting from a more完善、风控更规范的市场环境, will只能遵循既定行业规则参与市场竞争, missing out on the core话语权与先发优势 of early布局.