Dollar-backed stablecoins are now more than just a crypto payment tool. Recent reports say that they may also be helping the U.S. extend dollar influence abroad, in a way that keeps real capital at home.

Here’s what you need to know.

Stablecoins – A secret weapon?

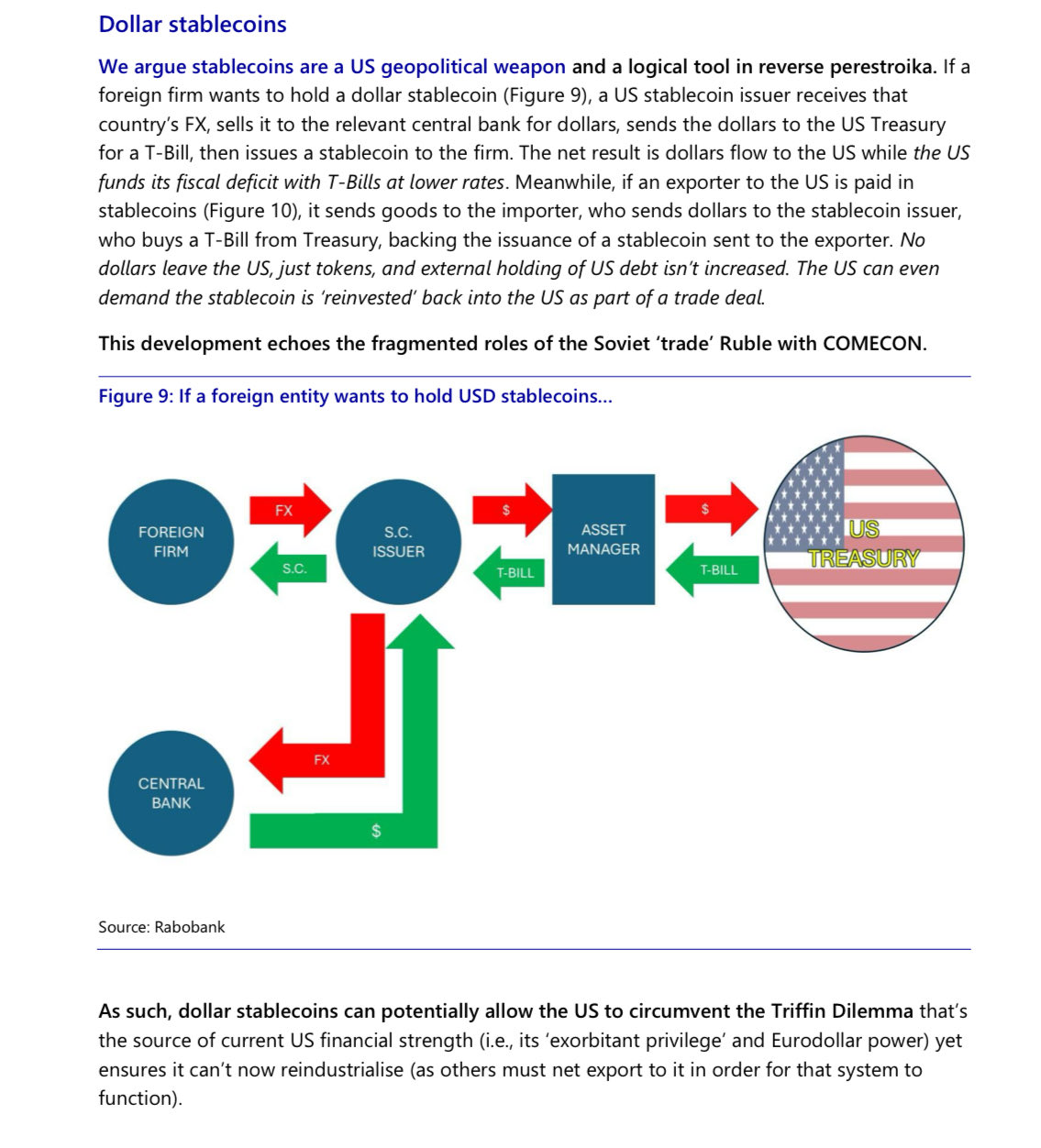

A report by Rabobank has stated that dollar-backed stablecoins are spreading dollar influence, without letting real dollars leave the country.

The idea is that when a foreign firm wants a dollar stablecoin, a U.S. issuer converts that demand into Treasury bill purchases. Dollars flow back to the U.S. government, helping fund deficits at lower rates, while the firm gets digital dollars instead of cash.

In trade, it goes a step further. U.S. importers can pay exporters in stablecoins, while the underlying dollars stay parked in Treasuries. Only tokens move across borders.

With comparisons to the Soviet-era trade ruble, dollars are exported digitally… all while keeping the power at home.

Non-dollar stablecoins step up

That growing influence hasn’t gone unnoticed, with non-USD-pegged alternatives gaining ground.

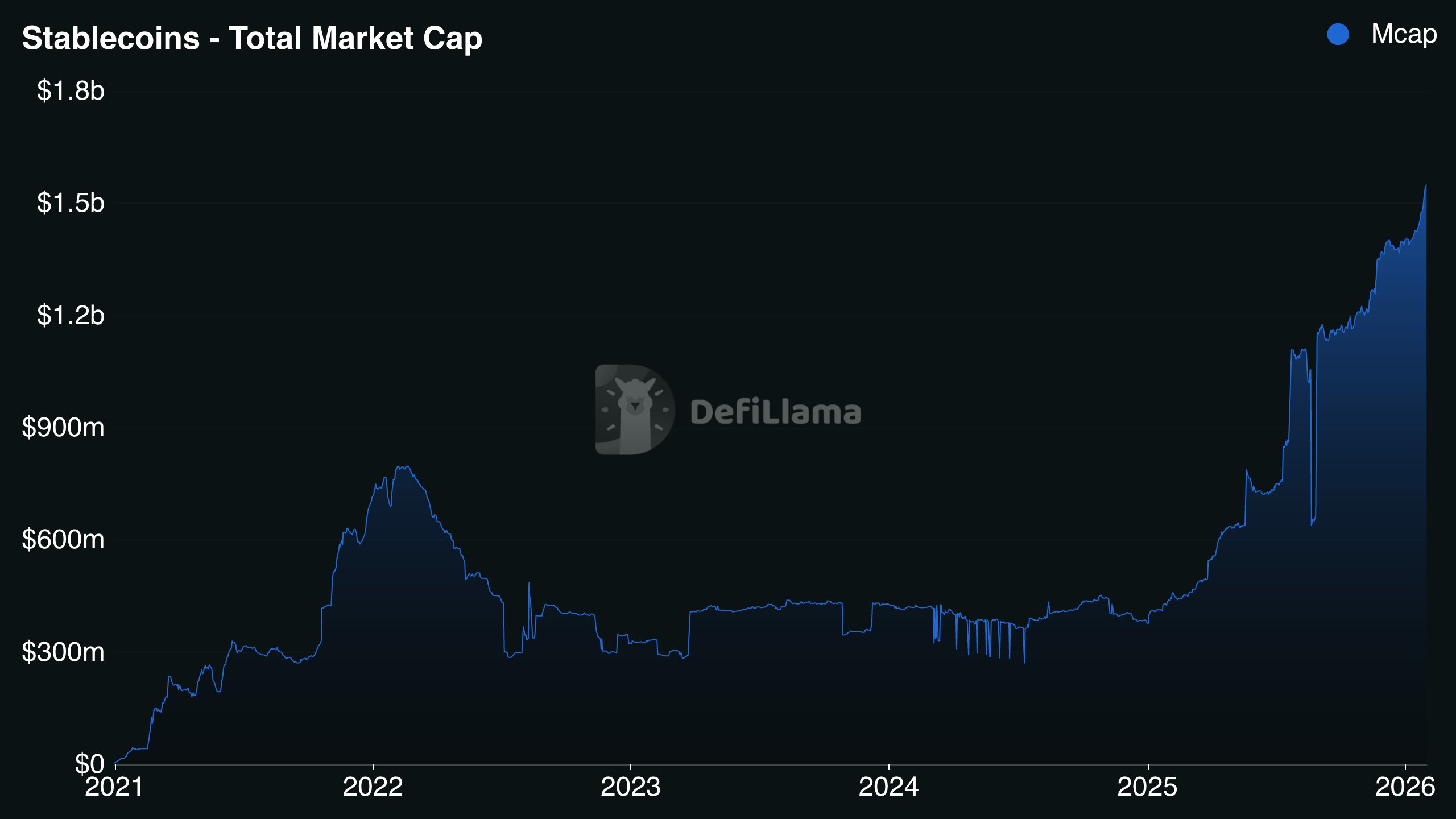

For long, more than 99% of stablecoins were pegged to the U.S. dollar. That number is now decreasing at the margins.

Over the past year, non-USD stablecoins have surged 260% in supply, pushing their combined market cap to about $1.55 billion.

It’s still small next to dollar-backed giants, but it certainly matters.

All of this theory matters because…

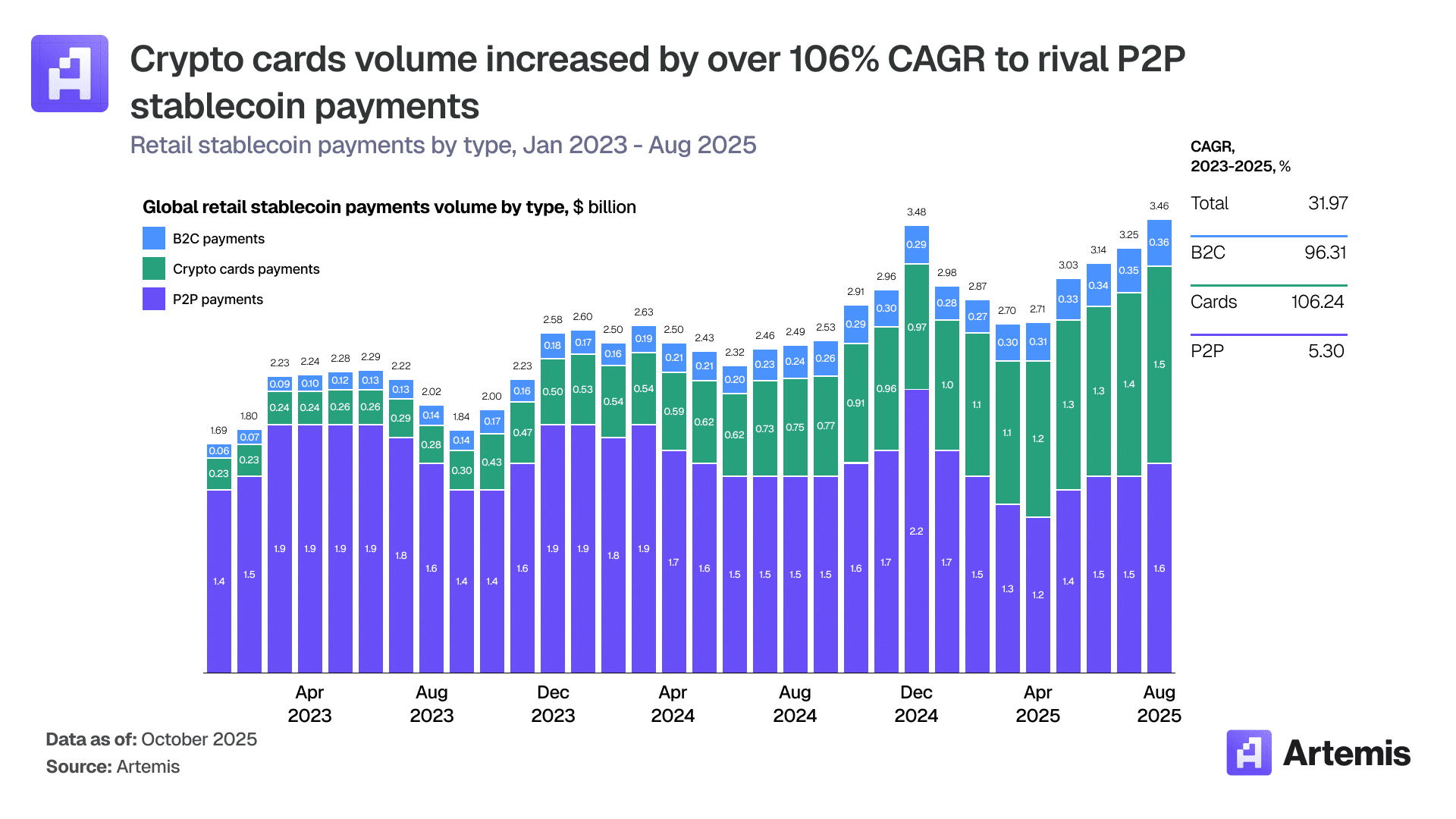

…it’s already showing up in day-to-day payments. One of the fastest-growing payment modes for stablecoins right now is crypto cards.

Once a niche product, crypto cards are now an $18 billion market.

Monthly volumes went from about $100 million in early 2023 to over $1.5 billion today, growing at a 100%+ annual rate.

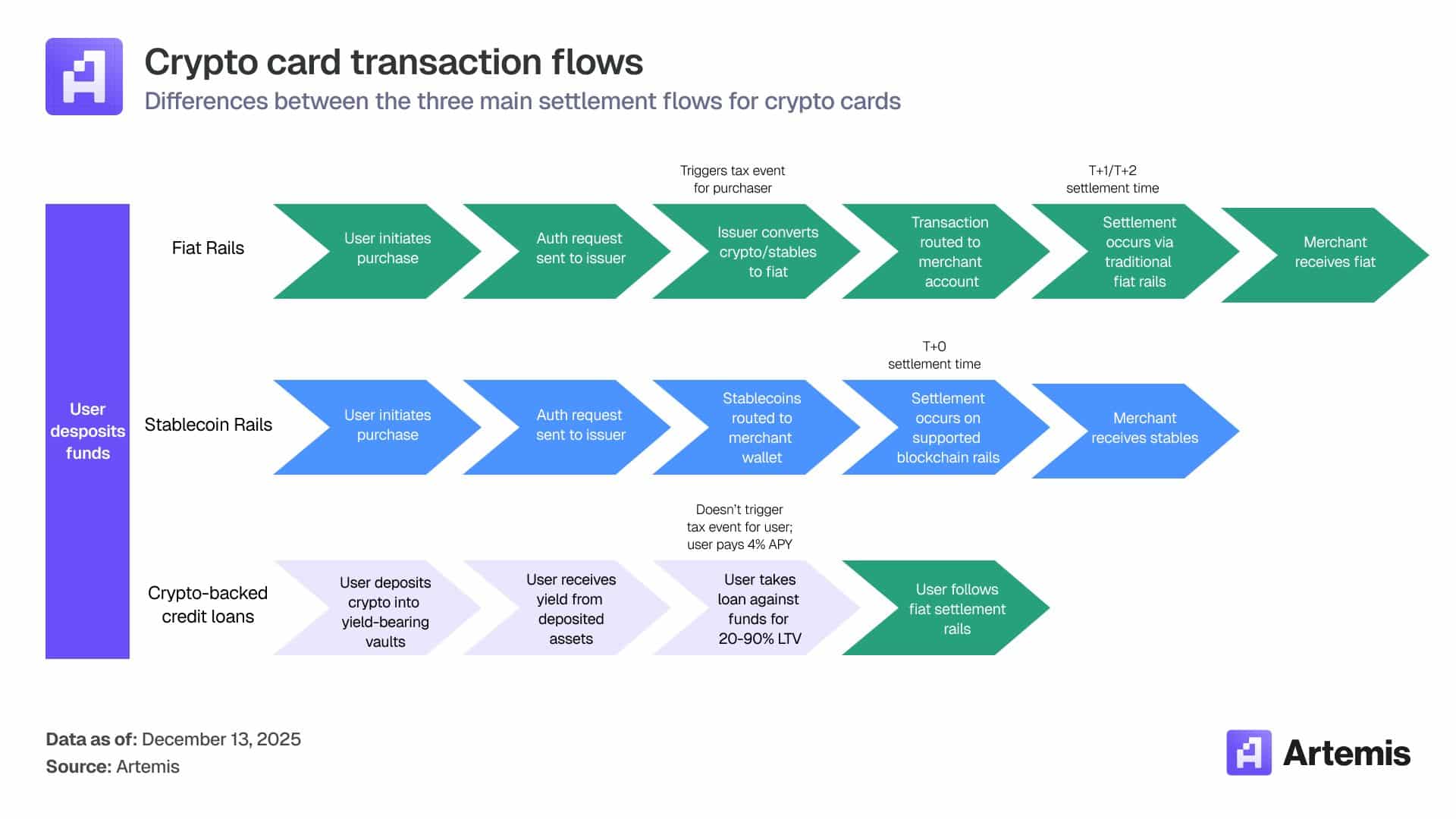

Importantly, these cards don’t replace Visa or Mastercard.

Rather, they sit on top of them. Stablecoins fund the transaction in the background, while card networks handle acceptance. For users and merchants, what looks like normal payments are actually digital dollars doing the work.

Final Thoughts

- Dollar-backed stablecoins are exporting U.S. monetary power, without exporting actual dollars.

- As crypto cards grow, digital dollars are moving fast.

Next: BONK drops 18% as memecoins slide – Is another leg down coming?