Author: Zhao Ying, Bao Yilong, Wall Street Insights

Amazon's stock has fallen for nine consecutive days, marking its longest losing streak in nearly 20 years.

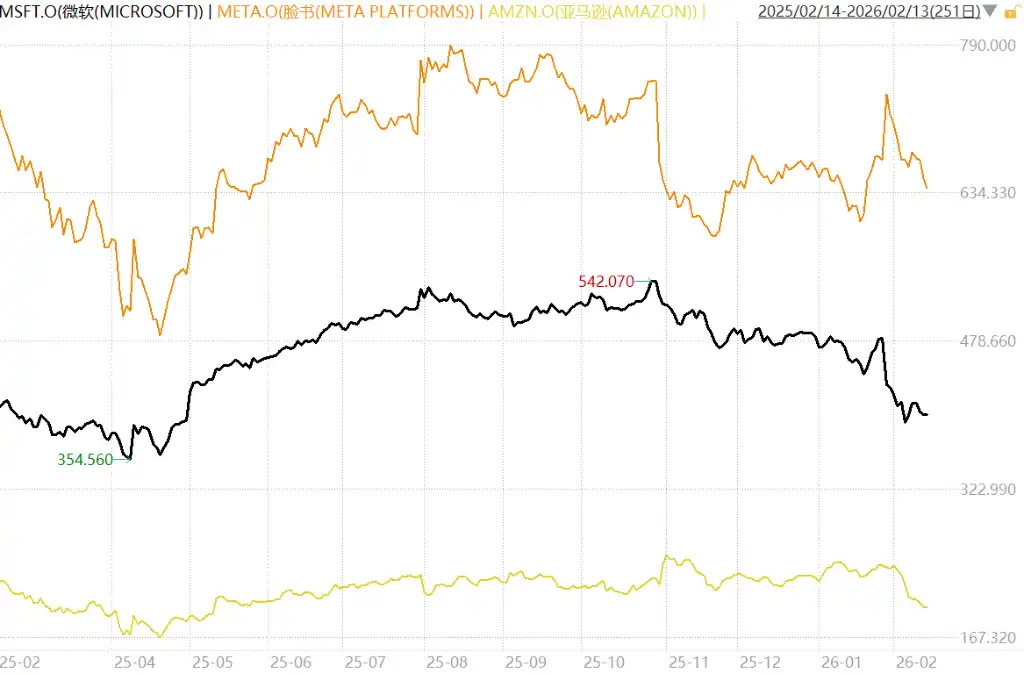

After entering a technical bear market on Thursday, becoming the second Mag7 company to fall into a bear market, Amazon's stock continued to decline on Friday.

Investors are strongly resisting the aggressive AI spending plans of tech giants, leading to significant declines in these star stocks.

On Friday, Amazon's stock closed at $198.79, down more than 23% from its recent high, officially crossing the bear market threshold the previous day, Thursday.

Among the four major hyperscale cloud service providers, Amazon has the highest planned capital expenditure for 2026, reaching $200 billion.

Amazon, Microsoft, Meta, and Alphabet are expected to collectively spend $650 billion on capital expenditures in the AI field by 2026.

Meta could be the next Mag7 member to fall into a bear market. As of Friday's close, it was down 19.6% from last year's high, just 0.4% away from the bear market threshold of a 20% decline. Although Meta's Q4 revenue and profits exceeded Wall Street expectations, increased AI spending and margin pressures have dampened investor confidence.

Microsoft was the first Mag7 member to enter a bear market. The company's stock fell into a bear market on January 29, after the Azure cloud business growth reported the previous day fell short of investor expectations. As of Friday's close, Microsoft's stock was down 27.8% from its recent high.

(Chart of Amazon, Microsoft, and Meta's performance over the past year)

Investors Rotate Within Mag7, Free Cash Flow Pressure Highlights

Mike Treacy, Vice President of Risk at Apex Fintech Solutions, stated that the recent sell-off highlights the growing divergence among Mag7 members.

Since last fall, investors have shifted away from OpenAI-related deals involving Microsoft, NVIDIA, and Oracle, favoring the Alphabet and Broadcom ecosystems instead.

Treacy pointed out that Alphabet's vertically integrated technology stack has somewhat offset concerns about excessive spending, shielding the stock from the worst of the tech sell-off. Alphabet's stock closed Thursday down 9.2% from its recent high.

Treacy noted that Google's self-sufficiency should command a premium relative to other companies that may be adversely affected by a single link in the industry chain.

Amazon, Microsoft, and Meta's stocks have been hit harder because investors lack confidence that these companies' AI spending will yield sufficient returns on investment.

For Amazon, the increased level of expenditure could lead to negative free cash flow this year, meaning the company may need to start raising more funds in the debt market.

Treacy believes that the next major catalyst for AI trades will be NVIDIA's earnings report on February 25. This report will show whether the AI boom is cooling down or if NVIDIA has successfully captured the tens of billions of dollars its largest clients are investing into the field.

Related reading: Trading Moment: AI Panic Escalates Ahead of CPI, Bitcoin Grinds Bottom, May Struggle to Repeat "Spring Festival Rally"