Author:Muyao Shen

Compiled by: Deep Tide TechFlow

Deep Tide Guide: The collapse of BlockFi and Celsius in 2022 plunged the crypto lending industry into a deep freeze, but now, a Vault model touting "transparency and non-custodial" features is making a comeback with $6 billion in assets under management.

This article provides an in-depth analysis of this new format: how it uses smart contracts to avoid the black-box risks of traditional centralized lending, and how, under the pressure to pursue high yields, it might repeat the mistakes of a firm like Stream Finance.

As the "Genius Act" pushes stablecoins into the mainstream, are Vaults the cornerstone of crypto finance's maturation, or the next shadow banking crisis cloaked in transparency?

This article will reveal the old and new logic behind high yields.

Full Text Below:

When the crypto platform Stream Finance collapsed at the end of last year (resulting in the loss of approximately $93 million in user funds), it exposed a familiar breaking point in digital assets: when markets turn, promises of so-called "safe yield" often crumble.

This failure was disturbing not only because of the losses incurred, but also because of the mechanism behind it. Stream had positioned itself as part of a new generation of more transparent crypto yield products, designed to avoid the hidden leverage, opaque counterparty risks, and arbitrary risk decisions that brought down centralized lending institutions like BlockFi and Celsius in the previous cycle.

Instead, it demonstrated how quickly the same dynamics—leverage, off-platform risk exposure, and centralized risk—can return when platforms start chasing yield, even if the underlying infrastructure appears safer or the transparency is more reassuring.

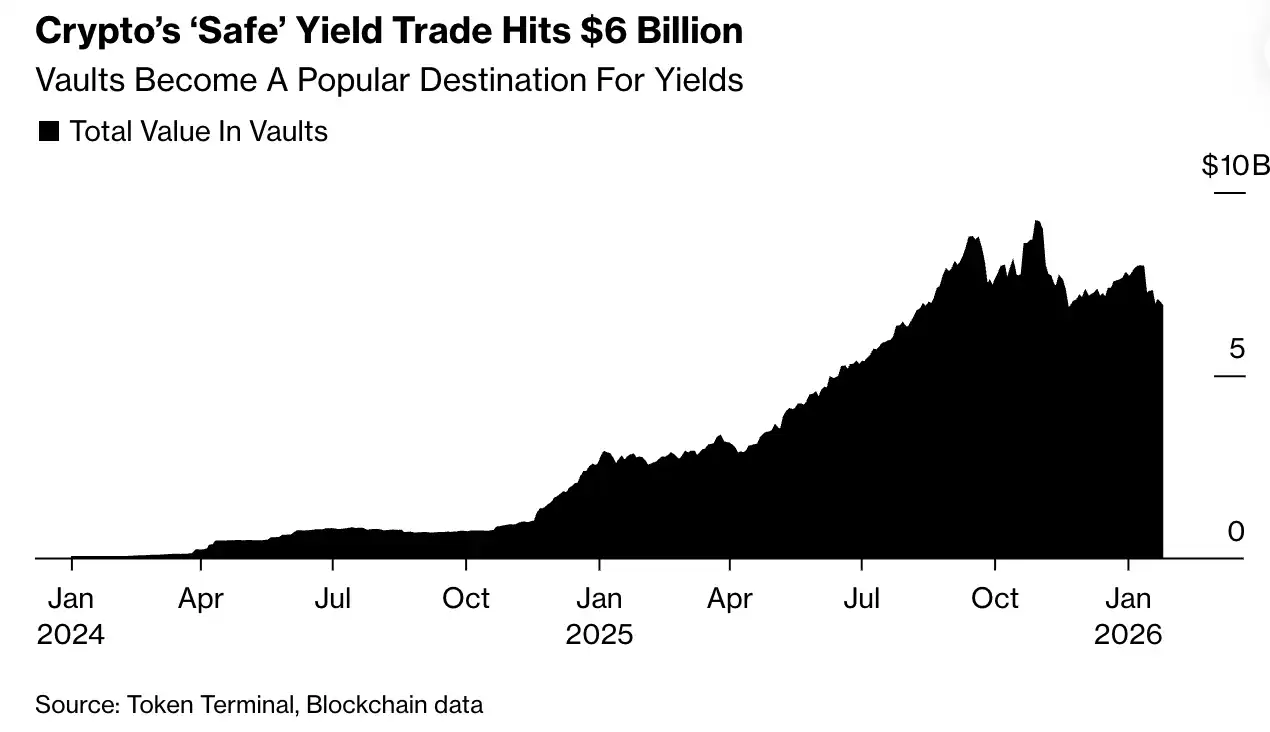

Yet, the broader promise of safer crypto yield remains. According to industry data, Vaults—on-chain pools built around this idea—currently manage over $6 billion in assets. Crypto asset management firm Bitwise predicts that assets in Vaults could double by the end of 2026, driven by growing demand for stablecoin yield.

Cryptocurrency's "Safe" Yield Trade Reaches $6 Billion

At a basic level, Vaults allow users to deposit cryptocurrency into shared pools, and these funds are deployed into lending or trading strategies designed to generate returns. The difference with Vaults lies in how they are marketed: they are promoted as a clean break from the opaque lending platforms of the past. Deposits are non-custodial, meaning users never hand over their assets to a company. Funds are held in smart contracts that automatically deploy capital according to pre-set rules, with key risk decisions clearly visible on the blockchain. Functionally, Vaults resemble a familiar component of traditional finance: pooled funds converted into yield and providing liquidity.

But their structure is distinctly crypto. This all happens outside the regulated banking system. Risk is not buffered by capital reserves or overseen by regulators—it is embedded in software, where algorithms automatically rebalance positions, liquidate collateral, or unwind trades as markets move, automating losses.

In practice, this structure can produce mixed results, as curators (the companies that design and manage Vault strategies) compete on returns, and users find themselves navigating just how much risk they are willing to bear.

"Some players will do a terrible job," said Paul Frambot, co-founder of Morpho, the infrastructure behind many lending Vaults. "They might not survive."

For developers like Frambot, this churn is less a warning sign and more a feature of an open, permissionless market—where strategies are tested in the open, capital flows quickly, and weaker approaches are replaced over time by stronger ones.

The timing of its growth is no accident. With the passage of the "Genius Act," stablecoins are moving into the financial mainstream. As wallets, fintech apps, and custodians race to distribute digital dollars, platforms face a common problem: how to generate yield without putting their own capital at risk.

Vaults have emerged as a compromise. They offer a way to manufacture yield while technically keeping assets off a company's books. Think of it like a traditional fund—but without handing over custody or waiting for quarterly disclosures. This is how curators pitch the model: users retain control of their assets while gaining access to professionally managed strategies that run automatically on-chain.

"The curator's role is similar to a risk and asset manager, like what BlackRock or Blackstone does for the funds and endowments they manage," said Tarun Chitra, CEO of crypto risk management firm Gauntlet, which also operates Vaults. "But, unlike BlackRock or Blackstone, it's non-custodial, so the asset manager never holds the user's assets; the assets are always in the smart contract."

This structure is designed to correct recurring weaknesses in crypto finance. In previous cycles, products marketed as low-risk often hid borrowed money, reused client funds without disclosure, or relied heavily on a handful of fragile partners. The algorithmic stablecoin TerraUSD offered yields nearing 20% by subsidizing returns. Centralized lenders like Celsius quietly parked deposits in high-risk bets. When markets turned, the damage spread quickly—and without warning.

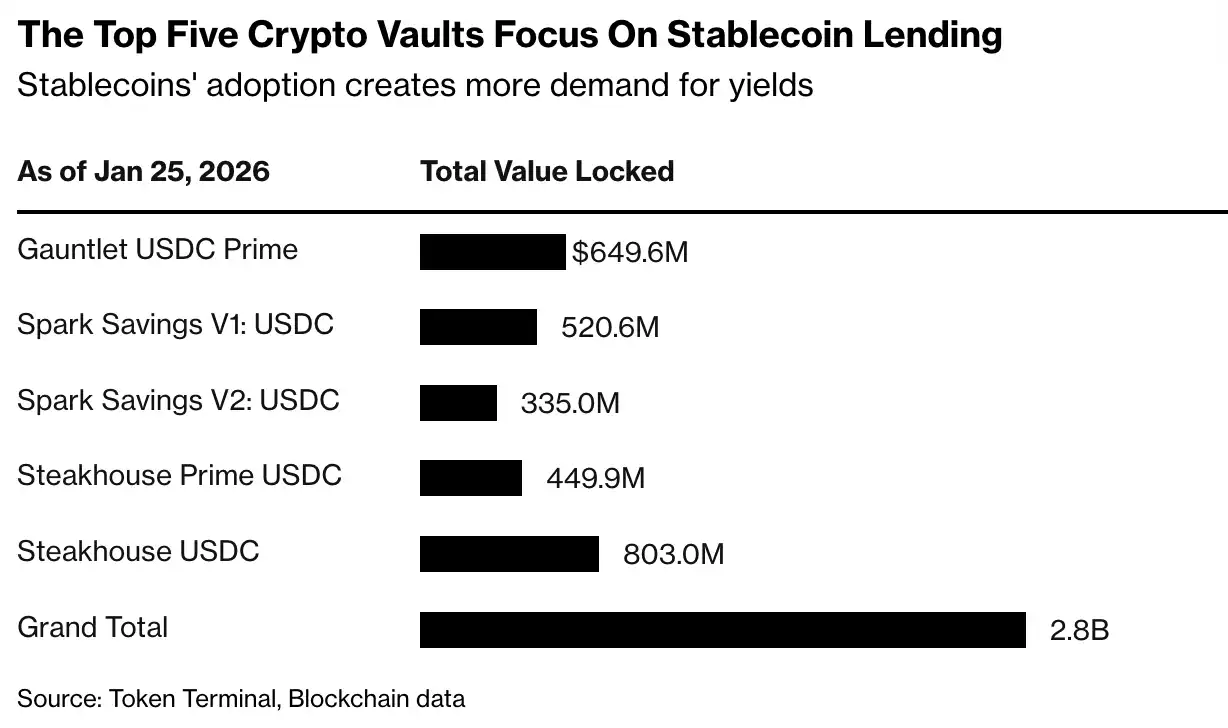

Most Vault strategies today are more restrained. They typically involve floating-rate lending, market making, or providing liquidity to blockchain protocols, rather than pure speculation. The Steakhouse USDC Vault is one such example, lending stablecoins against what it describes as blue-chip cryptocurrencies and tokenized real-world assets (RWAs), offering a return of about 3.8%. Many Vaults are deliberately designed to be "boring": their appeal lies not in outsized returns, but in the promise of earning yield on digital cash without handing over custody or making users creditors of a single company.

"People want yield," said Jonathan Man, portfolio manager and head of multi-strategy solutions at Bitwise, which just launched its first Vault. "They want their assets to be productive. Vaults are just another way to do that."

Vaults could also gain more momentum if regulators move to ban paying yield directly on stablecoin balances—a suggestion floated in market structure legislation. If that happens, the demand for yield won't disappear; it will just shift.

"Every fintech company, every centralized exchange, every custodian is talking to us," said Sébastien Derivaux, co-founder of Vault curator Steakhouse Financial. "Traditional finance companies too."

But this restraint isn't hard-coded into the system. The pressure shaping the industry comes from competition, not technology. As stablecoins proliferate, yield becomes a primary tool for attracting and retaining deposits. Underperforming curators risk losing capital, while those offering higher returns attract more inflows. Historically, this dynamic has pushed non-bank lenders—both in crypto and elsewhere—to loosen standards, add leverage, or shift risk off-platform. This shift has already touched large consumer-facing platforms. Crypto exchanges Coinbase and Kraken have both launched products giving retail customers access to Vault-like strategies, advertising yields as high as 8%.

Transparency, in sum, can be misleading. Public data tools and visible strategies build confidence—and confidence attracts capital. But once money is in place, curators face pressure to deliver returns, sometimes by reaching into off-chain deals that are difficult for users to assess.

Stream Finance later exposed this breaking point; the platform had advertised returns as high as 18%, then reported significant losses related to an unnamed external fund manager. The event triggered a sharp pullback across the Vault industry, with total assets falling from a peak near $10 billion to around $5.4 billion.

Proponents of the model say Stream was not representative. Stream Finance did not respond to a request for comment sent via X private message.

"Celsius, BlockFi, all of these, even Stream Finance, I kind of lump them all together as failures of disclosure to the end user," said Bitwise's Man. "People in crypto always focus more on what the upside might be and less on what the downside risk is."

That distinction may matter for now. Vaults were built in response to the last wave of failures, with the explicit goal of making risk visible rather than hidden. The open question is whether transparency alone is enough to constrain behavior—or whether, as in previous cases of shadow banking, a clearer structure just makes it easier for investors to tolerate risk until the music stops.

"At the end of the day, it's about embracing transparency, but it's also about having proper disclosures for any type of product—DeFi or non-DeFi," Man said.