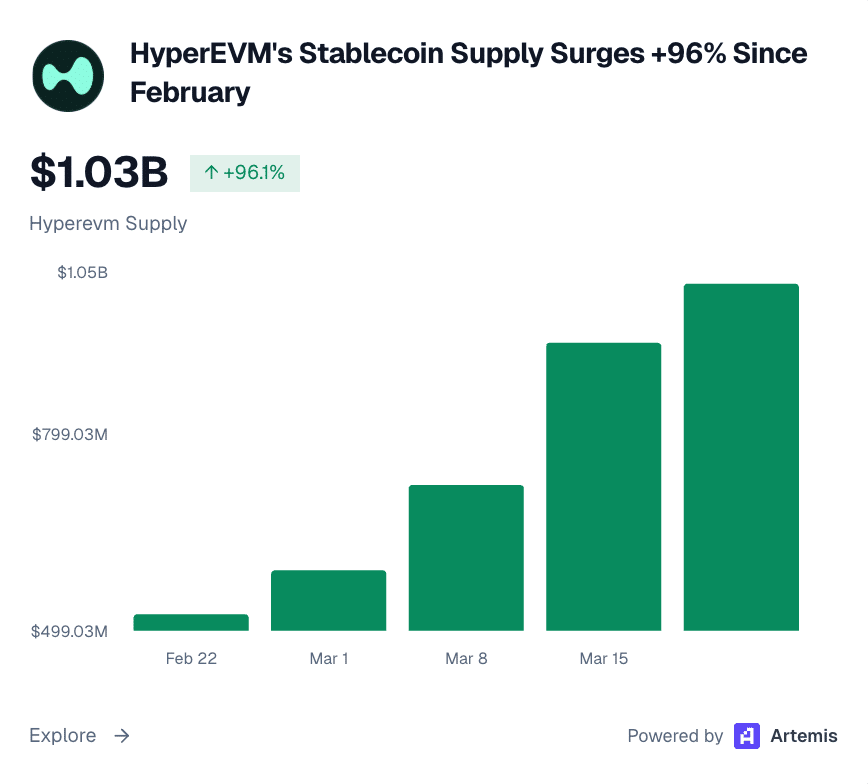

HyperEVM is emerging as a strong liquidity hub, with stablecoin supply and TVL both surpassing $1 billion soon after launch. At the same time, Hyperliquid [HYPE] L1 holds over $5 billion in stablecoins, which reinforces broader ecosystem momentum.

However, bridges such as HyperCore receive the majority of inflows, which transfer USDHL, USDe, and feUSD across chains, indicating a reallocation of liquidity rather than its creation.

USDhl minting adds treasury-backed supply while supporting demand through HYPE-linked incentives, which sustains short-term activity. As these flows continue, unique active wallets steadily increase, reflecting growing participation.

Simultaneously, platforms like Hyperlend, DEXs, and perpetual venues absorb this capital and drive usage. Still, this growth leans on incentives and yield opportunities, which may fade. For now, HyperEVM shows traction, although lasting expansion depends on steady organic demand.

Stablecoin supply near $318B reflects growth

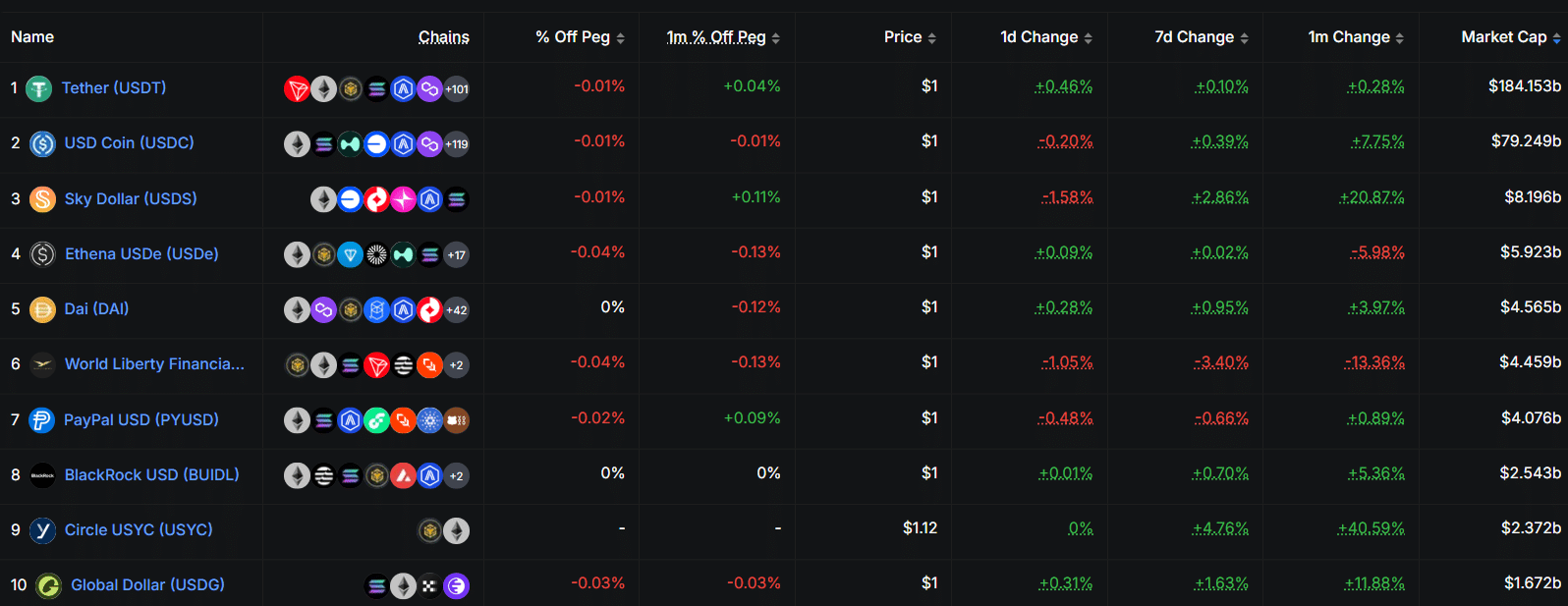

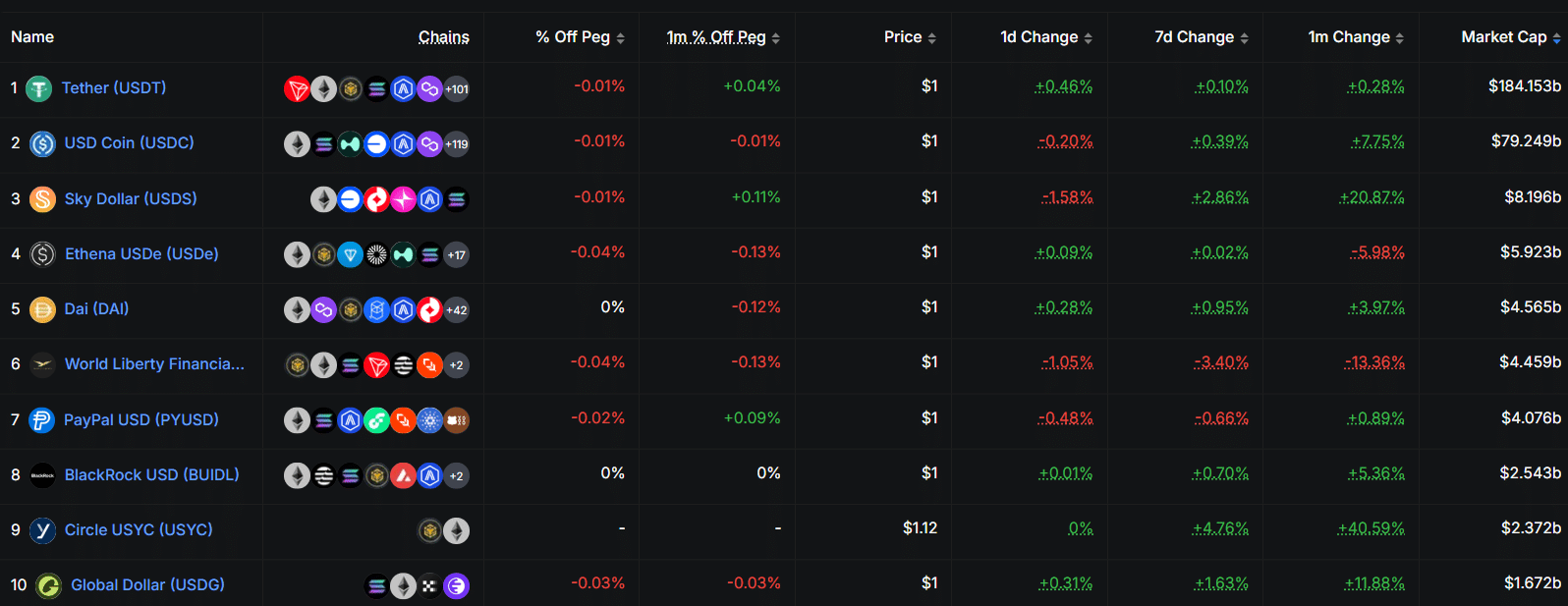

Stablecoin supply is approaching $318 billion, rising 0.47% weekly and 2.86% monthly, which reflects controlled expansion rather than aggressive inflows. Building on this trend, Tether [USDT] still dominates at $184 billion, although its 0.10% weekly growth shows slowing momentum.

Meanwhile, USDC at $79.24 billion expands faster with 7.75% monthly gains, while USDS and USYC surge by 20.87% and 40.59%, highlighting shifting demand. As these changes unfold, minting continues to exceed burns, suggesting fresh capital entering through fiat on-ramps.

However, part of this rise also reflects capital rotating into yield-bearing and regulated assets. In parallel, the stablecoin ratio holds near 9–10% of the $2.5 trillion crypto market cap, showing relative balance.

This steady structure suggests liquidity is gradually expanding, yet not accelerating sharply, leaving the market split between real inflows and internal redistribution.

Stablecoins move from storage to utilization across crypto markets

Stablecoin growth is increasingly translating into active deployment, as DEX volume reaches $7.65 billion and rises 8.91% weekly. Building on this, Uniswap [UNI] processes $1.289 billion, while PancakeSwap [CAKE] sustains steady stablecoin-pair activity, reinforcing spot demand.

Perpetual Open Interest holds near $48–51 billion, showing sustained positioning without sharp liquidations. As flows deepen, stablecoin netflows turn positive, with ERC-20 inflows around $484 million moving toward exchanges.

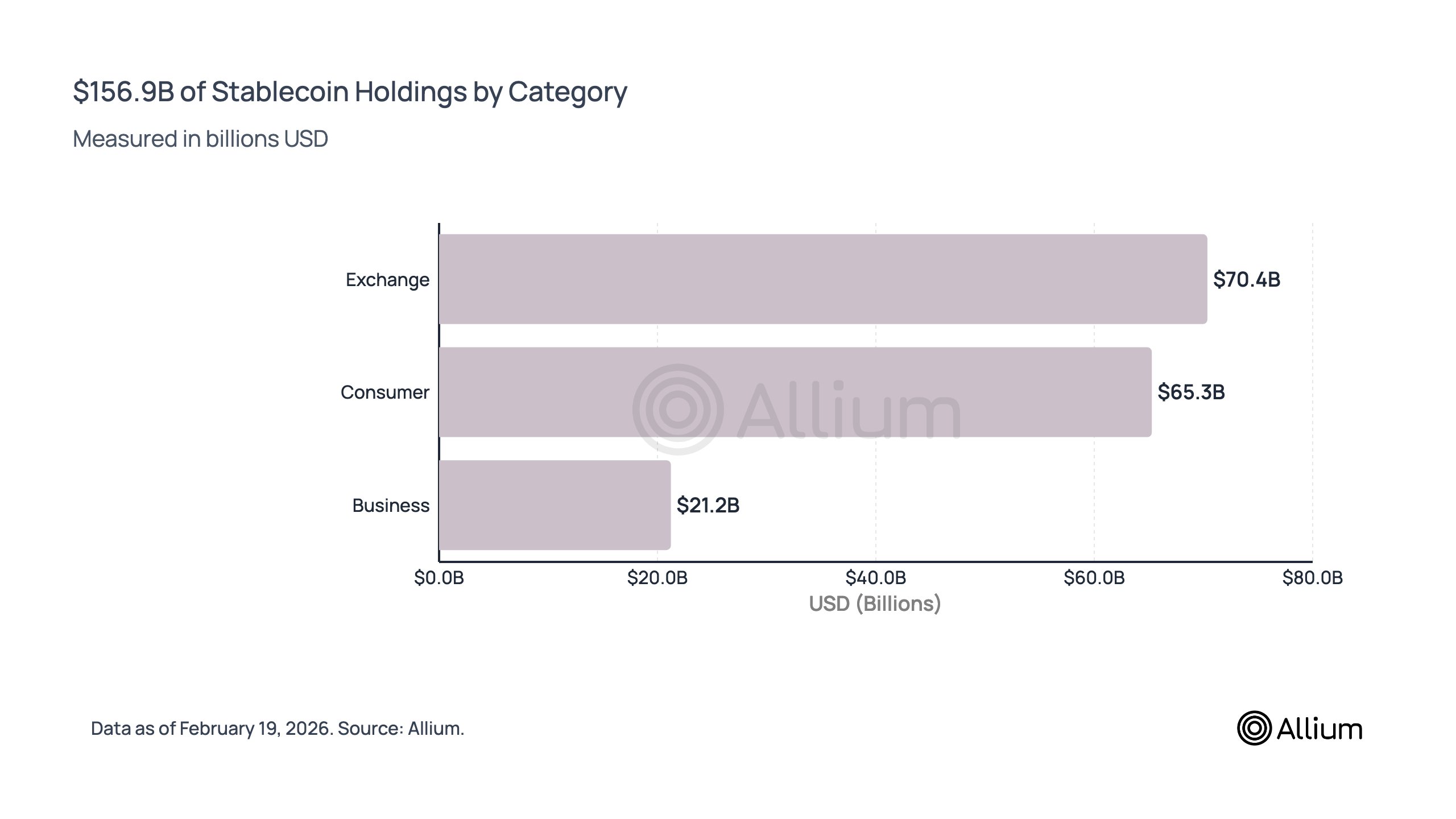

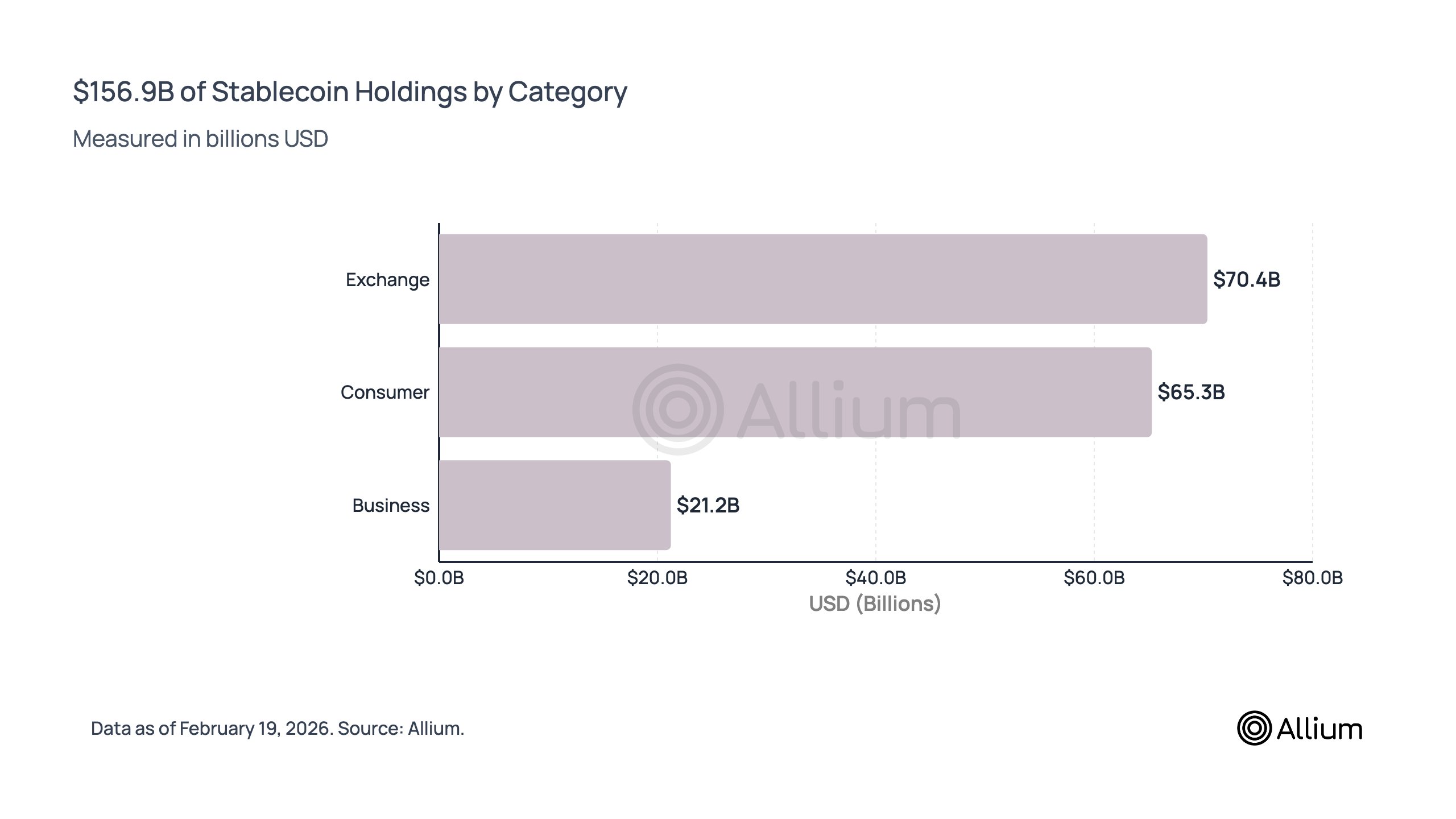

This shift aligns with holdings data, where exchanges control $70.4 billion, or 45%, anchoring liquidity concentration. From here, consumer balances reach $65.3 billion, or 41%, reflecting growing retail usage.

Business holdings at $21.2 billion support payment flows tied to $374.5 billion in volume. As distribution broadens, capital appears actively deployed, although exchange dominance suggests part of liquidity remains positioned rather than fully utilized.

Final Summary

- Hyperliquid ecosystem growth reflects rising liquidity and user activity, yet heavy reliance on bridged inflows and incentives questions sustainability.

- Stablecoins, led by Tether [USDT], show gradual expansion and active deployment, although a portion of liquidity still rotates internally across exchanges and DeFi.