Original | Odaily Planet Daily (@OdailyChina)

Author | Golem (@web 3_golem)

On the evening of June 18, SpaceX's Starship No. 36 exploded during its 10th static fire test, creating a huge fireball on-site. Fortunately, there were no casualties. This was SpaceX's most severe ground incident recently, with all test facilities damaged. Western media described it as a "catastrophic failure."

The "ripple effect" of this explosion quickly spread to the capital markets. From June 18 to present, SpaceX has fallen for three consecutive trading days. On June 22, it dropped over 16.43%, with its market value evaporating approximately $400 billion in a single day, setting the second-largest historical single-day market value loss record for a global company.

Worse still, SPCX has fallen below its IPO first-day closing price ($160.95). According to Hyperliquid data in after-hours trading, SPCX once dipped below the IPO opening price ($150). If it truly opens below $150 on June 23 when the U.S. stock market opens, it would mean all investors who bought and held SPCX in the secondary market would be at a loss.

Is this continuous decline due to a loss of investor confidence in SpaceX or short-term market sentiment correction? How will SpaceX's stock price move next? Odaily Planet Daily will provide a brief analysis in this article.

$20 Billion Bond Financing May Just Be the Trigger

The direct trigger for SPCX's drop of over 16% on June 22 was SpaceX's announcement that day to initiate its first senior unsecured bond offering. Although SpaceX's 8-K filing with the U.S. SEC did not disclose the specific issuance size, according to a Bloomberg report last week, SpaceX is planning a bond offering of at least $20 billion. SpaceX confirmed that the proceeds from this fundraising would be used to repay bridge loans, pay related fees, and for general corporate purposes. This bridge loan arose from SpaceX's acquisition of Musk's own company, xAI, in February this year.

However, conducting a bond financing less than two weeks after going public is not good news for investors. The additional interest expense from issuing bonds is a minor issue; it signifies that SpaceX still needs extra financing, which brings significant negative implications.

SpaceX had already raised $85.7 billion in its IPO, and according to disclosures, it also had approximately $100.8 billion in cash and cash equivalents on its books. This has become the latest point of attack for short-sellers. A company that just went public and has over $100 billion in cash on its books is now borrowing from the market again. This suggests that SpaceX's free cash flow has not yet materialized, and the cash burn rate of Starship and AI infrastructure capital expenditures have far exceeded market estimates.

CFRA Research, which has consistently given SpaceX a sell rating, also questioned the necessity of SpaceX's massive financing, commenting, "With Elon Musk, you never know what's going on in his mind."

Well-known tech hedge fund manager Dan Niles also posted on the X platform, stating that SpaceX's bond issuance and the compute power agreement with Reflection AI might remind investors that the market now has another ultra-large-scale AI competitor requiring massive financing. He had previously expressed concerns about its high valuation multiple times.

Impacted by the Global Pullback in AI Concept Stocks

The announcement of bond financing might only be the trigger for SpaceX's decline; its stock price pressure is also impacted by the global correction in AI concept stocks.

On June 23, not only did U.S. AI concept stocks close lower, but AI sectors in other global markets were also correcting. On June 23, South Korea's KOSPI became the worst-performing major Asian stock index, falling over 9%. The Korean stock market triggered a circuit breaker in the morning and continued to fall in the afternoon; SK Hynix and Samsung Electronics both dropped over 12%. Meanwhile, Hong Kong's AI leaders also plunged, with MINIMAX down 15% and Zhipu down over 9%. Mainland China's A-share four major indices also collectively fell in the morning session.

The global pullback in AI concept stocks is mainly because investors are beginning to worry that AI infrastructure investments are too large, while the commercial return cycle is too long. Whether capital expenditures will ultimately yield corresponding returns is a concern. SpaceX is also seen as one of the representative companies of this logic, with investment scale far outpacing the speed of commercial returns, naturally leading to a sharp drop in its stock price.

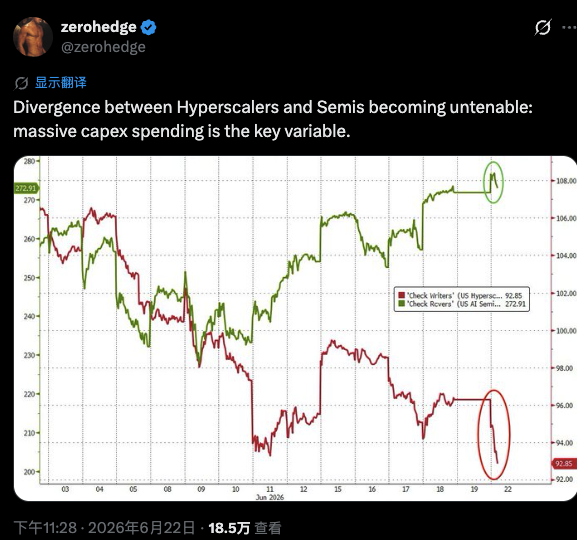

U.S. financial media zerohedge posted on the X platform on June 22, stating that the divergence between hyperscale cloud providers and semiconductors is intensifying, with massive capital expenditures being the key factor.

Retail Buying Dries Up, Lock-up Expiration Negative Anticipated Early

Since its listing, SpaceX has been the most popular stock among retail investors in the U.S. market. With initially less than 5% of shares floating, the SPCX stock price was essentially inflated by retail investors. According to Vanda Track statistics, retail investors net bought $405 million worth of SPCX in its first five trading days. Retail buying volume for SPCX had surpassed their combined buying volume of all other "Magnificent Seven" stocks during the same period—NVDA, MSFT, AMZN, META, GOOGL, and GOOG combined for only $278 million.

However, retail buying cannot serve as long-term support for SPCX's stock price. On the contrary, the more aggressive the initial retail buying, the faster the momentum dissipates once those who truly wanted to buy have done so and sentiment cools.

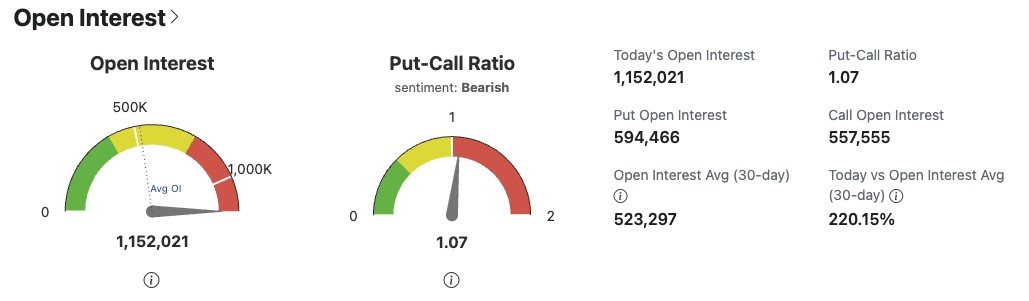

SpaceX options trading began on June 16, with bullish sentiment dominating initially. However, according to OptionCharts data, the current Put-Call Ratio for SPCX is 1.07. From a sentiment perspective, investors are already leaning neutral to bearish. While it's not a consensus bearish view yet, it at least proves that retail investors are starting to become timid.

This sharp decline in SPCX has occurred with only 5% of shares floating. What will happen to SPCX when the lock-up period expires? To some extent, the current stock decline is also an early realization of the negative impact from the lock-up expiration. Investors might be waiting to re-enter their positions after SpaceX's first round of share unlocks.

According to regulations, after SpaceX releases its Q2 earnings report in mid-August, 20% of shares will be unlocked. If the stock price rises 30% above the IPO price and meets this standard for 5 out of 10 trading days, an additional 10% can be unlocked.

22V Research strategist Jeff Jacobson stated that insiders might sell up to 44% of SpaceX shares before early September, which would increase the current float by approximately 900%.

SpaceX's next potential positive catalyst is its possible inclusion in the Nasdaq 100 index in July. However, due to three consecutive days of declines, investor panic regarding SpaceX has outweighed anticipation for this potential positive news.

Bull and Bear Arguments

Different from the first week of listing, the market's bearish view on SpaceX now dominates. The main bull and bear arguments are as follows.

Correction After Shorting Tools Become Available; Valuation Already Reflects Future Growth

On June 18, after SpaceX announced a $60 billion equity acquisition of Cursor, the well-known independent investment research firm Morningstar not only did not raise its expectations for SpaceX's AI business but further lowered its fair value estimate from the previous $63 to $62. They believe that, without substantive quarterly financial reports to support it, the current stock price is entirely driven by narrative.

Future Fund co-founder Gary Black previously pointed out that before SpaceX options trading began, SpaceX's trading logic was completely detached from fundamentals."It traded more like a meme stock than a fundamentally-driven company." Therefore, the current plunge is an inevitable correction after shorting tools became available.

On June 22, the major U.S. investment bank KeyBanc Capital Markets (KBCM) gave SPCX a Neutral rating. Although it did not provide a target price, its analysts stated that SpaceX's current valuation already fully reflects future growth, and the stock price could be halved. While there are long-term growth drivers, a lot of the positive news is already "priced in."

Cathie Wood Becomes a Firm SPCX Bull

Dusk witnesses devout believers. Cathie Wood-led ARK Invest is not only a Bitcoin bull but now also one of SpaceX's most steadfast bulls. On SpaceX's IPO day, ARK Invest aggressively bought approximately 3.3 million shares, with a holding value exceeding $500 million on that day. On June 22, the day SPCX plunged, ARK bought about 210,000 shares of SPCX (worth approximately $38.9 million) through several of its ETFs (including ARKK, ARKQ, etc.).

Previously, in 2024, ARK's model estimated SpaceX's enterprise value would reach $2.5 trillion by 2030, approaching $3.1 trillion in an optimistic scenario. At that time, ARK's model corresponded to a company that was not yet public, with a valuation of approximately $180-$350 billion. Now, SpaceX has successfully gone public, and its market value once approached ARK's model estimate from back then. ARK's decision to increase its position at this time perhaps reflects its long-term optimism towards SpaceX's disruptive innovations like reusable rockets, Starlink, and the space economy.