Author: CryptoSlate

Compiled by: Deep Tide TechFlow

Deep Tide Guide: With BTC currently around $67K, miners are barely breaking even on electricity costs, but operational expenses and depreciation keep overall operations in the red. This article uses real financial data from Riot Platforms to build a three-tier cost model, thoroughly deconstructing the often oversimplified number of "mining cost"—providing direct reference value for understanding mining stock valuations and BTC price pressure levels.

Right now, buying Bitcoin is cheaper than mining it, unless your electricity cost is below 7 cents per kWh.

Full Text Below:

Riot Case Reveals the Three-Tier Profit and Loss Structure of US Miners

Bitcoin mining cost is often simplified to a single number: "the cost to mine one BTC." In reality, this number depends on which level of the business you are measuring.

Electricity costs determine whether to turn on the machines today, operational expenses determine if the mining farm can sustain the entire company, and accounting costs determine whether the business ultimately reports a profit.

To analyze these three levels more clearly, CryptoSlate built a Bitcoin mining cost model based on first principles, calculating mining economics from network difficulty, block reward, transaction fees, ASIC efficiency, and electricity price.

The model then incorporated company-level cost data from Riot Platforms' public financial filings to show the actual economic situation.

Under current network conditions, the model shows miners can cover electricity costs but still cannot cover broader operational and accounting expenses.

Riot's Texas operations reveal: even after the BTC price recovery, there remains a significant gap between the electricity break-even point, the operational break-even point, and the full accounting profitability point.

Riot's Mining Economics Reveal a Three-Tier Profit and Loss Structure

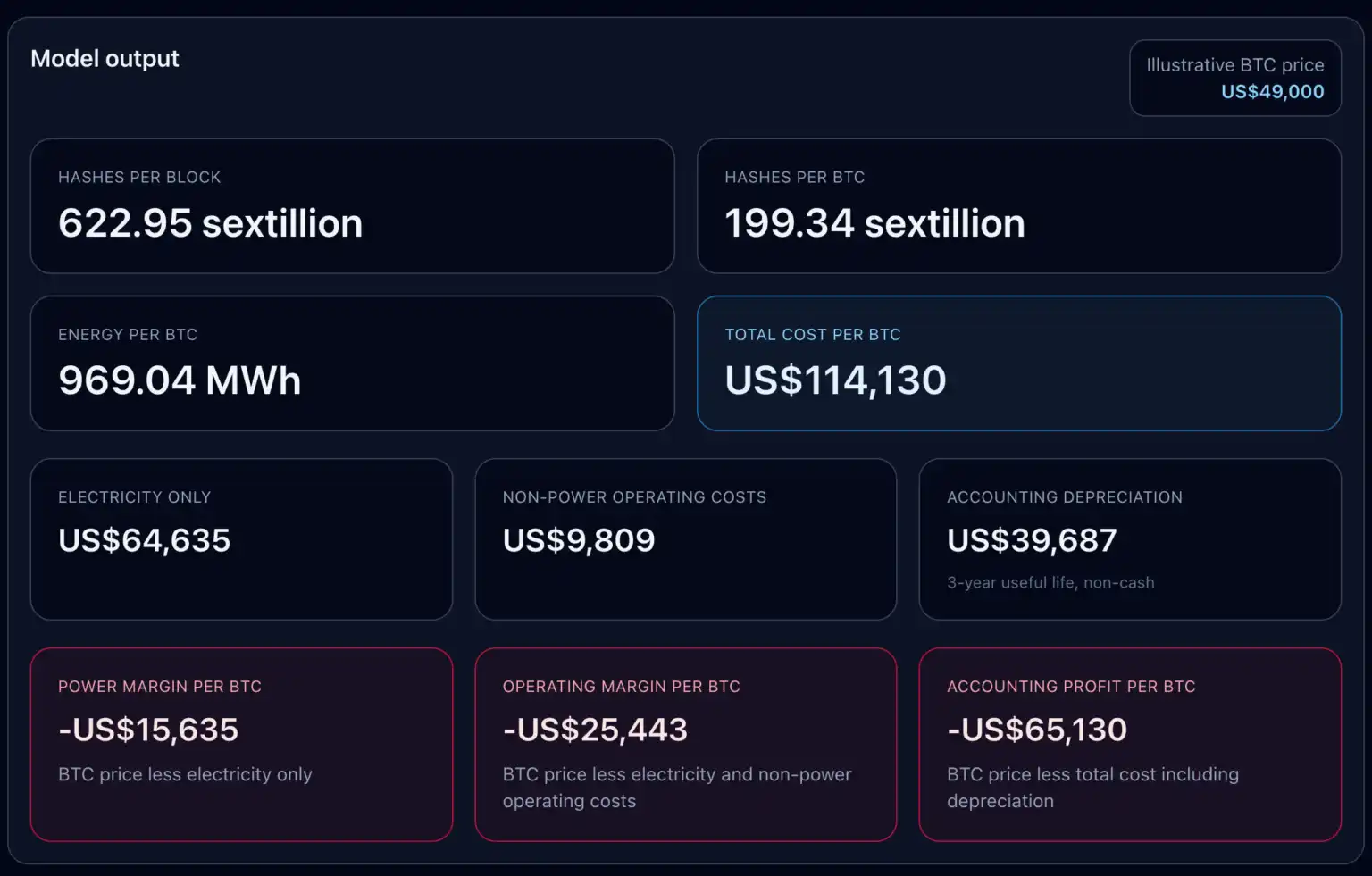

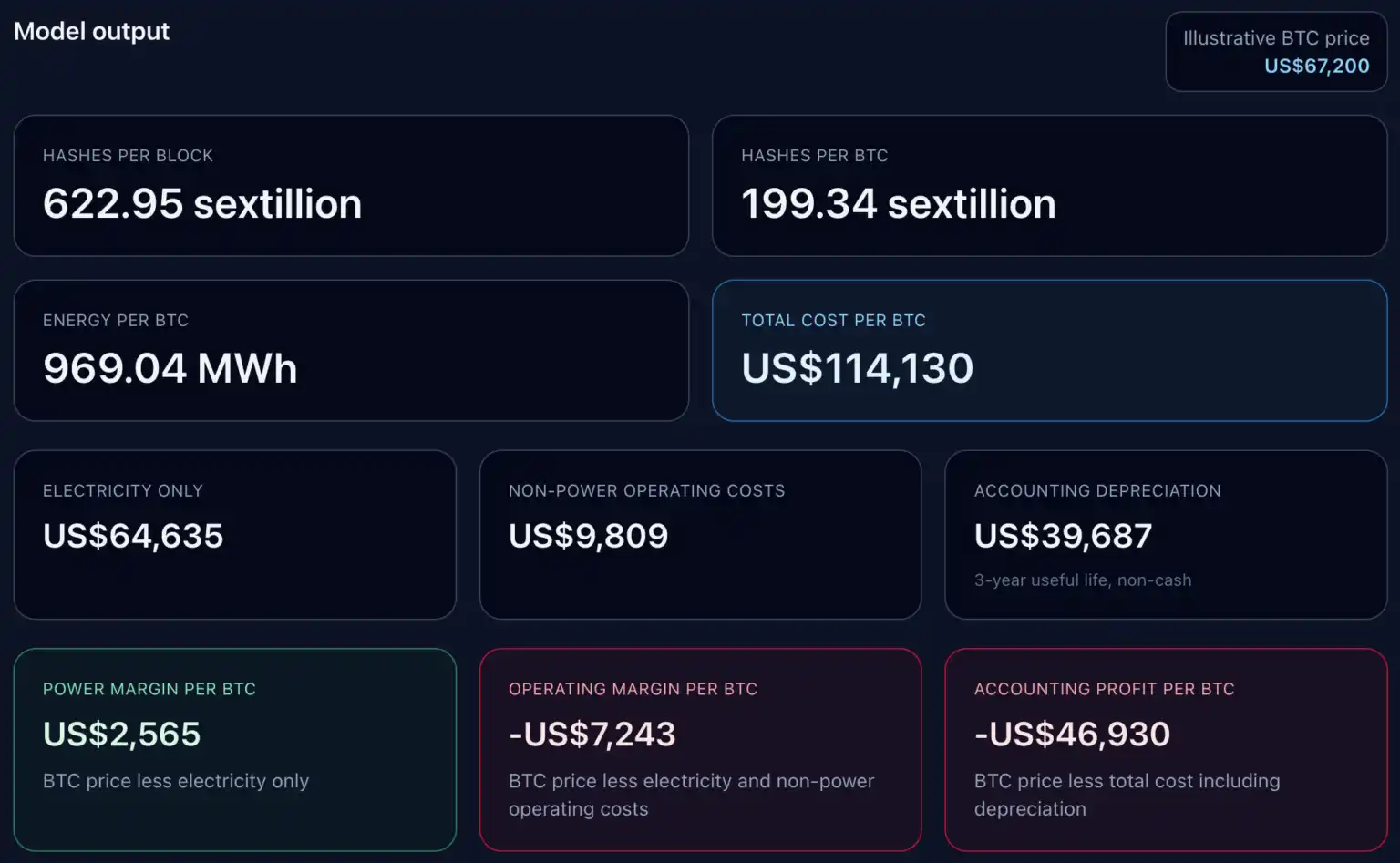

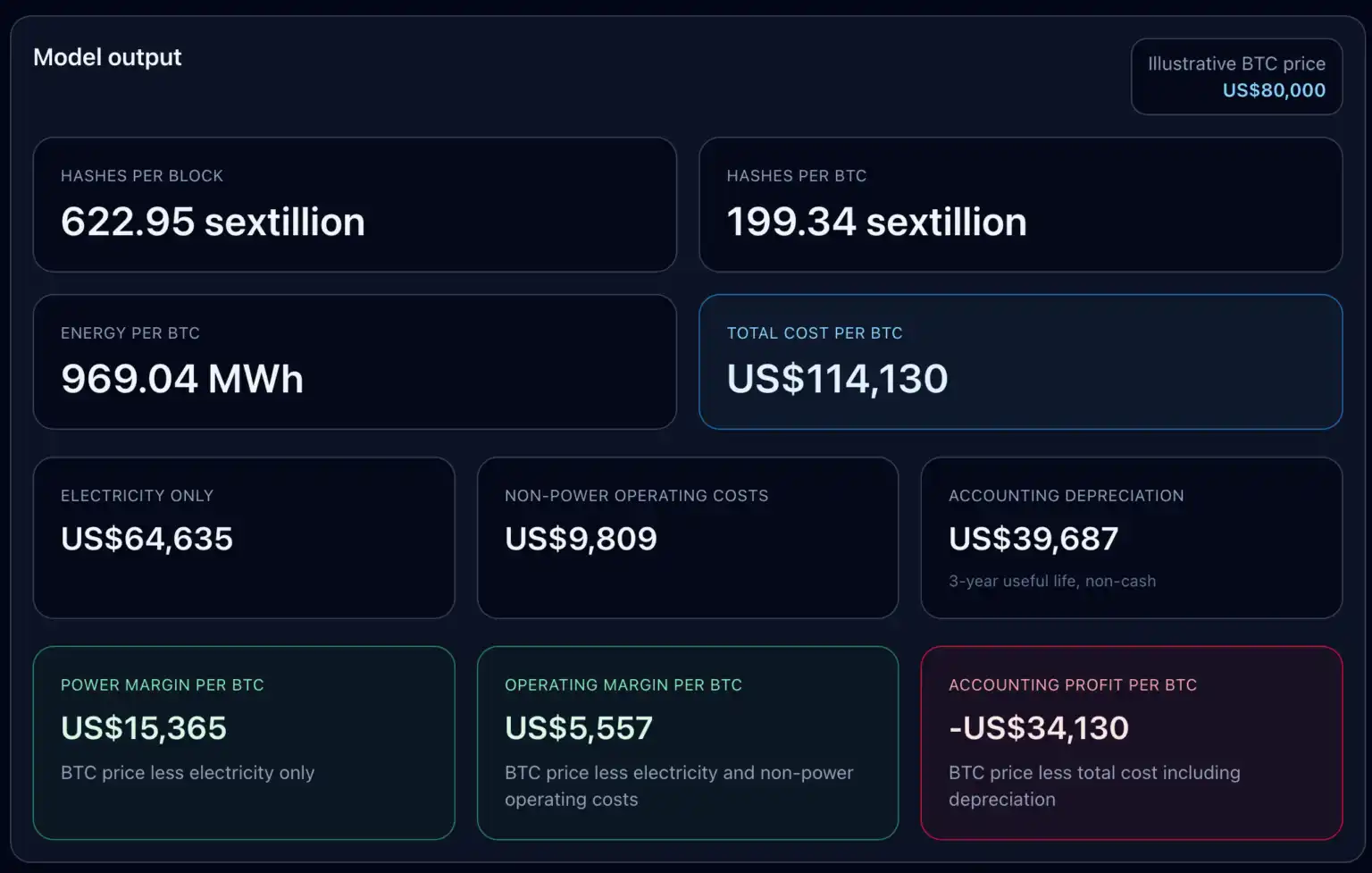

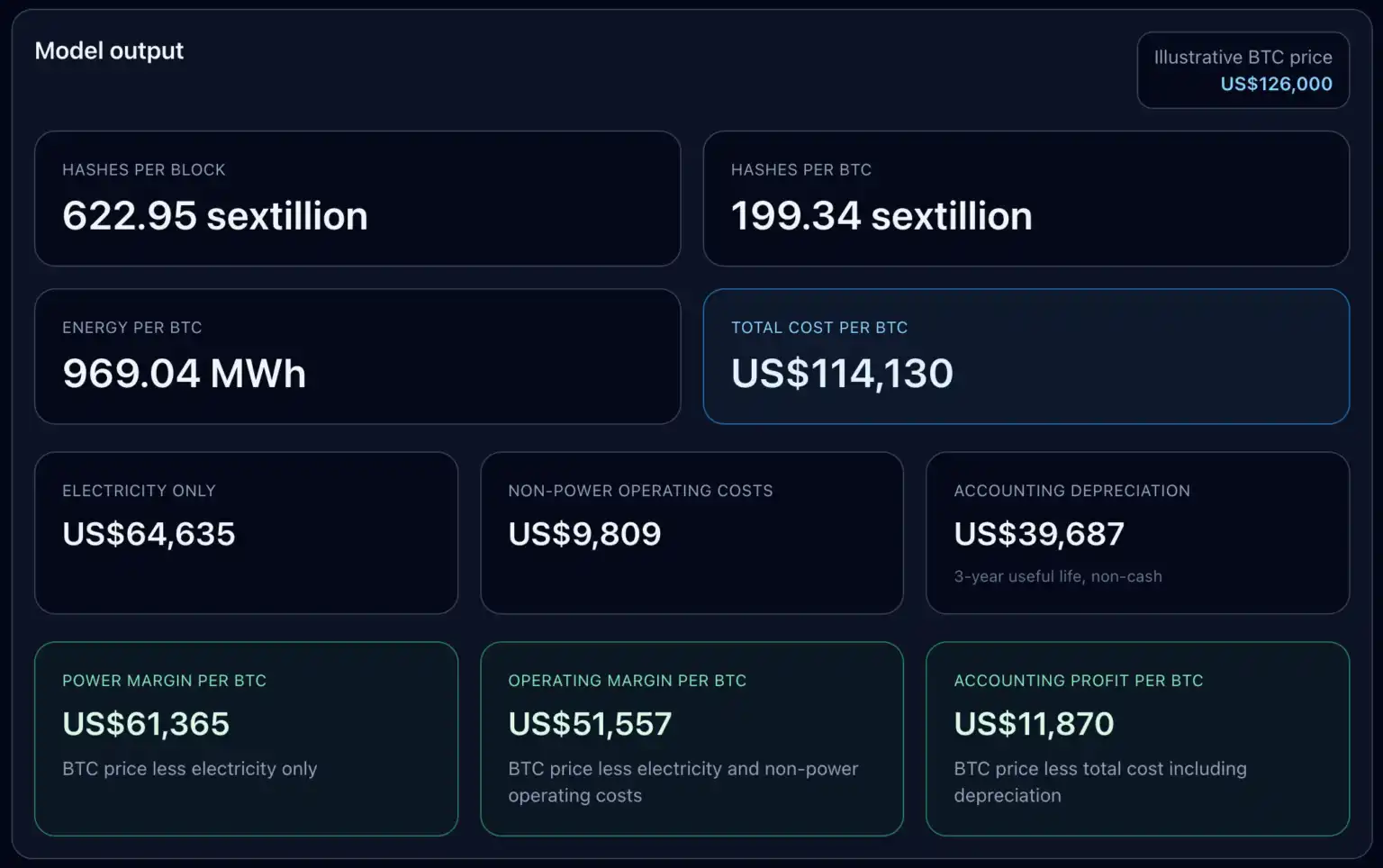

At the current BTC price of $67,200, Riot crosses one break-even point but fails to cross the latter two.

The model is built on the following current network conditions: Bitcoin difficulty 145,042,165,424,850, block reward 3.125 BTC, modern ASIC efficiency around 17-19 J/TH, Texas industrial electricity price approx. $0.0667/kWh. As the current average transaction fee is about 0.02 BTC/block, this model ignores block fees.

The above parameters yield the following results: total network hashrate per block 622.95 exahashes, hashrate required per BTC 199.34 exahashes, energy consumption per BTC 969.04 MWh.

Accordingly, the electricity cost to mine one BTC at the current price is $64,635, resulting in an electricity profit of $2,565/BTC.

After adding non-electricity operational costs of approximately $9,809/BTC from Riot's financial filings, the operational profit becomes negative $7,243, and the total cost increases accordingly. After further adding non-cash depreciation of approximately $39,687/BTC, the accounting profit falls to negative $46,930.

This clearly shows that for large US miners, there is no single number for "the cost to mine one BTC."

First tier: Electricity cost, determines short-term profitability of turning on machines.

Second tier: Adds broader operational costs, determines if self-mining can cover the overall business.

Third tier: Adds depreciation, determines if book profit aligns with cash profit.

The model displays these three tiers side by side, revealing how large the gap between them remains even after the market recovery.

The Break-Even Ladder Defines the Operational Picture

The break-even ladder provided by the model is more illustrative than any single all-in cost number.

Break-even point for electricity cost only: $64,635/BTC.

After adding Riot's non-electricity operational costs, the break-even point rises to approximately $74,444.

After adding accounting depreciation, the full accounting break-even point rises to $114,130.

Therefore, a miner can report positive gains at the electricity level while still being at a loss at the operational or accounting level.

I created four price scenarios to demonstrate how this ladder works in practice.

In the $49,000 bear market scenario, Riot is negative at all levels: electricity profit -$15,635/BTC, operational profit -$25,443/BTC, accounting profit -$65,130/BTC.

In the $67,200 current price scenario, Riot just crosses the electricity break-even point, barely above the threshold. Electricity profit turns positive, but the operational and accounting perspectives remain negative.

In the $80,000 recovery scenario, Riot crosses the operational break-even point, with an operational profit of $5,557/BTC, but remains at a loss of $34,130 at the accounting level.

For all three levels to turn positive simultaneously, BTC needs to return to its all-time high of $126,000, at which point the accounting profit would be $11,870/BTC.

This distinction has practical significance. Riot's depreciation layer is explicitly characterized as a non-cash expense, calculated based on a three-year useful life, representing an accounting allocation rather than a short-term avoidable cash outflow.

But it is still part of this picture because listed miners cannot survive on electricity profit alone—they must report income statements, replace machinery, and bear corporate operating costs.

Therefore, the truly valuable question is: which profit line are investors, analysts, and management actually looking at when judging a miner's profitability.

Riot's Price Stress Test Before the Next Halving

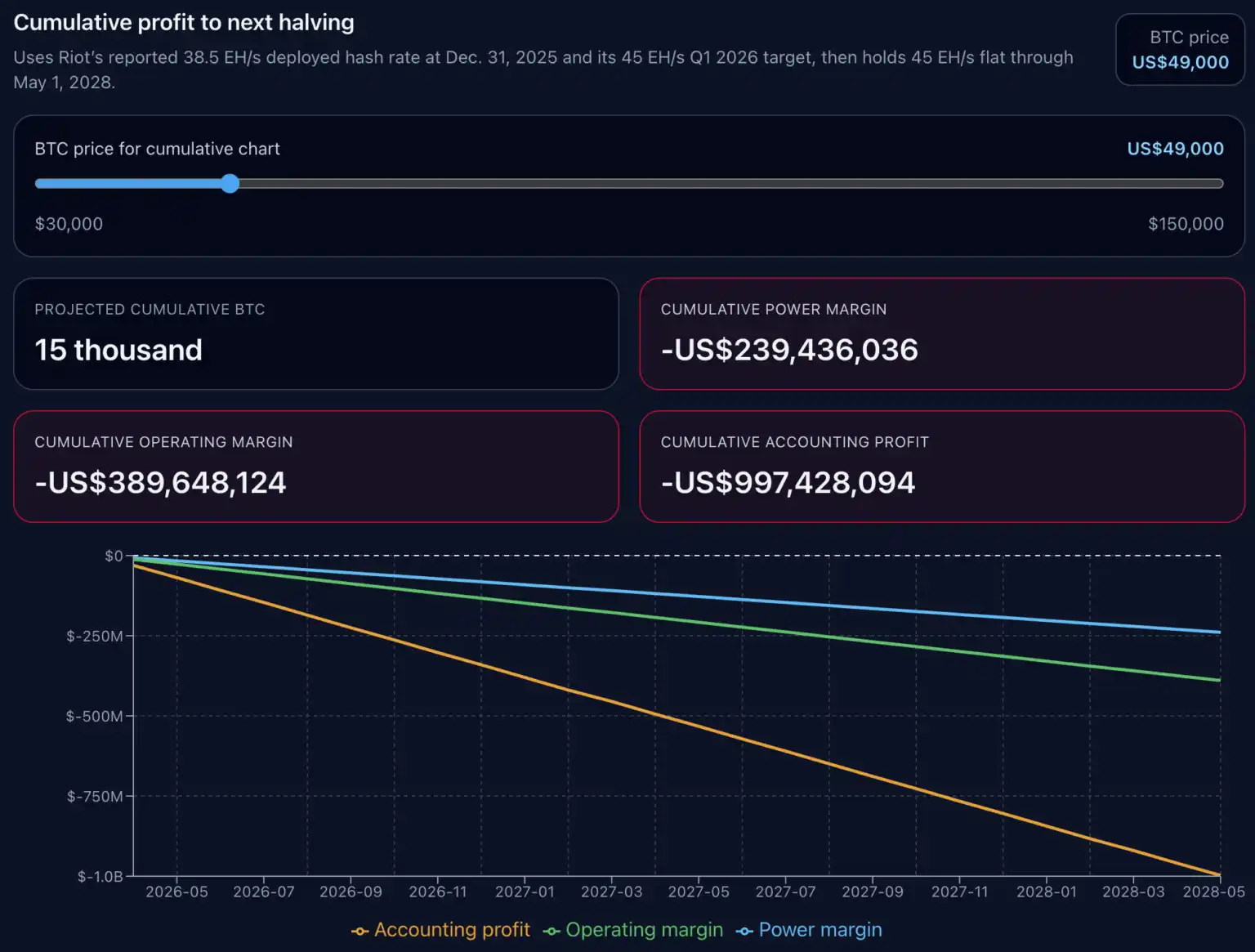

We then extended the cost model to the next halving in 2028.

Based on Riot's latest public filings, assuming a current hashrate of 38.5 EH/s, ramping up to 45 EH/s by March 31, 2026, and maintaining that level until the next halving window.

This model does not reconstruct the entire market but rather keeps the current per-BTC economics constant and projects them along the self-mining hashrate path Riot has reported and planned.

This is a scenario analysis focused on operational leverage, with clear price sensitivity.

In all four scenarios, the projected cumulative total mined BTC is 15,000 coins; what changes is the profit structure.

In the $49,000 scenario, Riot's cumulative electricity profit is -$239,436,036, cumulative operational profit is -$389,648,124, and cumulative accounting profit is -$997,428,094.

In the $67,200 scenario, cumulative electricity profit turns positive to $39,286,667, but cumulative operational profit remains negative at -$110,925,420, and cumulative accounting profit is -$718,705,391.

In the $80,000 scenario, cumulative operational profit turns positive to $85,099,338, but cumulative accounting profit remains negative at -$522,680,632.

Only in the $126,000 scenario do all three lines turn positive, with a cumulative accounting profit of $181,783,343.

Miners can maintain positive electricity returns for extended periods yet still fail to cover broader operational costs; they can also be operationally positive while still far from accounting profitability. The Riot case shows this gap between these two states is substantial.

In the model, the gap between the electricity break-even point and the full accounting break-even point is approximately $49,495/BTC. This spread helps explain why miners might appear healthy at the hashrate scheduling level but seem stretched thin at the reported profitability level.

Our cumulative charts do not predict future difficulty, fees, downtime, demand response income, financing, or new capital expenditures, only assuming current per-BTC economics remain constant and projecting them along Riot's planned hashrate path.

This limitation does not affect the core signal the model conveys: with other economic factors held constant, fixing these parameters, the discussion before the next halving will still largely depend on the BTC price.

For Riot, the model achieves cumulative accounting profitability in the $126,000 scenario, but in absolute terms, this critical point is $114,200.

Implications of the Riot Case for the Entire US Mining Sector

For US miners, the broader implication is direct: price alone cannot solve operational problems; machine efficiency and electricity price remain the first hurdles.

Regarding cost sensitivity, we compared three ASIC presets: Bitmain S21 (17.5 J/TH), MicroBT M60S (18.5 J/TH), and Antminer S19 Pro (29.5 J/TH), all using the Texas industrial reference electricity price.

Within this electricity price range, the per-BTC cost for the S19 Pro remains higher than the newer models. The two new models have similar costs, while the less efficient miner maintains a significantly higher cost line throughout the chart.

This conclusion applies beyond Riot. Riot's non-electricity cost layer and depreciation assumptions are company-specific; other miners may have different overhead bases, different useful life assumptions, different demand response income structures, or different actual electricity mixes. But the applicability of the three-tier analysis framework itself is not affected.

First tier: Electricity cost. Second tier: Operational cost. Third tier: Accounting cost.

Companies that survive low-price cycles often easily cross the first tier. Companies that compound growth through cycles...