Written by: TradFiHater

Compiled by: AididiaoJP, Foresight News

When Bitcoin's creator Satoshi Nakamoto released the whitepaper, mining was so simple: any gamer with an ordinary home computer could potentially accumulate a fortune worth tens of millions of dollars in the future.

On a home computer, you could have built a vast wealth legacy, freeing future generations from hard labor, as Bitcoin's potential return rate reached as high as 250,000 times.

But at that time, most gamers were addicted to Halo 3 on Xbox, and only a few young people used their home computers to earn fortunes far exceeding those of modern tech giants. Napoleon built his legend by conquering Egypt and Europe, while you only needed to click 'Start Mining'.

Over fifteen years, Bitcoin has become a global asset, and its mining has evolved into a large-scale industry requiring billions of dollars in funding, specialized hardware, and enormous energy consumption. Today, mining each Bitcoin on average consumes 900,000 kWh of electricity.

Bitcoin has spawned a completely new paradigm, starkly opposed to the financial world we are familiar with, dominated by traditional institutions. It might be the first truly meaningful rebellion against the elite since the failed Occupy Wall Street movement. Notably, Bitcoin was born precisely after the 'Great Financial Crisis' of the Obama era, a crisis largely stemming from the indulgence of high-risk 'casino-style' banking. The Sarbanes-Oxley Act of 2002 was intended to prevent a repeat of the dot-com bubble, yet ironically, the 2008 financial collapse was far more severe.

Whoever Satoshi Nakamoto was, his invention appeared at a perfectly opportune moment—a spasmodic yet deliberate rebellion against a powerful and ubiquitous traditional financial system.

From Disorder to Regulation: The Cycle of History

Before 1933, the U.S. stock market was largely unregulated, relying only on scattered state 'Blue Sky Laws,' leading to severe information asymmetry and rampant fraudulent trading.

The liquidity crisis of 1929 became the 'stress test' that broke this model, proving that decentralized self-regulation could not curb systemic risk. The U.S. government performed a 'forced reset' with the Securities Acts of 1933 and 1934: replacing the 'caveat emptor' principle with a central enforcement agency (the U.S. Securities and Exchange Commission, SEC) and a mandatory disclosure system, establishing uniform legal standards for all public assets to restore market trust in the system's solvency. Today, in the decentralized finance (DeFi) space, we are witnessing the exact same process unfold.

Until recently, cryptocurrency operated as a permissionless 'shadow banking' asset, functionally similar to the pre-1933 U.S. stock market but far more dangerous due to a complete lack of regulation. Its governance relied primarily on code and hype, failing to adequately assess the immense risks this 'beast' might bring. The series of cascading implosions in 2022 became the '1929-style stress test' for the crypto world, demonstrating that decentralization does not equal infinite returns and sound money; instead, it created a risk node capable of devouring multiple asset classes.

We are witnessing a forced shift in the zeitgeist: the crypto world is transitioning from a libertarian, casino-like paradigm to a compliant asset class. Regulators are attempting to make cryptocurrency perform a 'U-turn': once legalized, funds, institutions, the wealthy, and nations can hoard it like any other asset, thereby enabling its taxation.

This article aims to dissect the origins of cryptocurrency's 'institutional rebirth,' a transformation that has become inevitable. Our goal is to extrapolate the logical endpoint of this trend and attempt to depict the final form of the DeFi ecosystem.

Regulation Lands: Step by Step

Before DeFi entered its first true 'dark age' in 2021, its early development was not dominated by全新 legislation, but rather by federal agencies continuously extending existing laws to cover digital assets.

The first major federal action occurred in 2013: the U.S. Financial Crimes Enforcement Network (FinCEN) classified cryptocurrency 'exchangers' and 'administrators' as Money Services Businesses, subjecting them to the Bank Secrecy Act and anti-money laundering (AML) regulations. 2013 can be seen as the year DeFi was first 'acknowledged' by Wall Street, while also paving the way for future regulation and suppression.

In 2014, the Internal Revenue Service (IRS) defined virtual currency as 'property' rather than 'currency' (for federal tax purposes), causing every transaction to potentially generate capital gains tax. Thus, Bitcoin gained a legal characterization, meaning it became taxable—a far cry from its original 'rebellious' intent!

At the state level, New York introduced the controversial BitLicense in 2015, the first regulatory framework requiring disclosure from cryptocurrency businesses. Finally, the SEC capped the狂欢 with the 'DAO Report of Investigation,' confirming that many tokens constituted unregistered securities according to the 'Howey Test.'

In 2020, the Office of the Comptroller of the Currency (OCC) briefly allowed national banks to provide custody services for cryptocurrencies, but this move was later questioned by the Biden administration—almost a 'standard procedure' for successive presidents.

The Shackles of the Old World: Europe's Path

Across the ocean in the 'Old World,' antiquated customs similarly dictate the development of cryptocurrency. Influenced by a rigid Roman law tradition (distinct from the Anglo-American common law system), an anti-individual-liberty atmosphere pervades, limiting the possibilities of DeFi within a regressive civilization. It must be remembered that the American spirit is deeply influenced by Protestant ethics, a spirit of autonomy that shaped American entrepreneurial culture, liberal ideas, and pioneering spirit.

In Europe, Catholic tradition, Roman law, and feudal remnants have collectively fostered a截然不同的 culture. Therefore, it is not surprising that established countries like France, the UK, and Germany have taken different paths. In a society that prefers obedience over risk-taking, cryptocurrency is destined to be harshly suppressed.

Europe's crypto early era was defined by a fragmented bureaucracy rather than a unified vision. The industry scored its first legal victory in 2015: the European Court of Justice ruled in a case that Bitcoin transactions were exempt from value-added tax (VAT), effectively acknowledging the 'monetary'属性 of cryptocurrency.

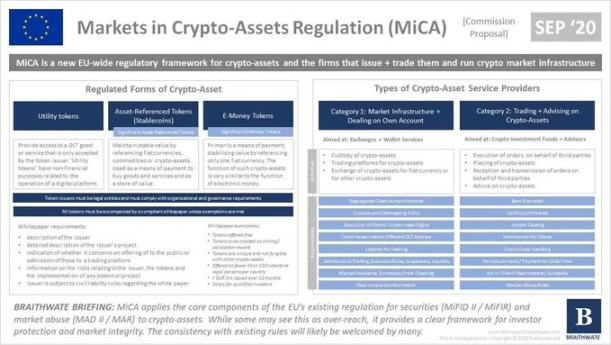

In the absence of unified EU law, national regulations varied until the Markets in Crypto-Assets Regulation (MiCA) emerged. France established a strict national framework through the PACTE Law, Germany introduced a cryptocurrency custody licensing system, while Malta and Switzerland competed to attract businesses with宽松优惠的 regulations.

In 2020, the Fifth Anti-Money Laundering Directive (5AMLD) ended this chaotic era, mandating strict customer identity verification across the EU, effectively eliminating anonymous trading. The European Commission finally realized that 27 sets of conflicting rules were unsustainable and proposed MiCA in late 2020, marking the end of the 'patchwork era' and the beginning of unified regulation.

America's 'Visionary' Model?

The shift in the U.S. regulatory system is not genuine systemic reform but more driven by opinion leaders. The power transition in 2025 brought a new philosophy: mercantilism压倒 moralism.

Trump's launch of his controversial 'Meme Coin' in December 2024 was perhaps a symbolic event. It showed that the elite were also willing to 'Make Cryptocurrency Great Again.' Today, several 'Crypto Popes' are leading the direction, committed to securing greater freedom and space for founders, developers, and retail investors.

Paul Atkins taking the helm at the SEC was more like a 'regime change' than an ordinary personnel shift. His predecessor, Gary Gensler, viewed the crypto industry with near hostility, becoming the 'public enemy' of a generation of crypto practitioners. An Oxford University paper even analyzed the pain caused by Gensler's policies. Many believe that due to his aggressive stance, years of development in the DeFi space were delayed; the regulator meant to guide the industry was severely out of touch.

Atkins not only halted numerous lawsuits but also essentially apologized for previous policies. The 'Crypto Project' he promotes is a model of bureaucratic agility. This project aims to establish an extremely dull, standardized, and comprehensive disclosure system, allowing Wall Street to trade crypto assets like Solana as it does oil. According to a summary by Allen & Overy, the plan's core includes:

-

Establishing a clear regulatory framework for U.S. crypto asset issuance.

-

Ensuring freedom of choice for custodians and trading venues.

-

Encouraging market competition and promoting the development of 'super apps.'

-

Supporting on-chain innovation and decentralized finance.

-

Setting up innovation exemption mechanisms to ensure commercial viability.

Perhaps the most critical shift occurred at the Treasury. Former Secretary Janet Yellen viewed stablecoins as a systemic risk. Current Secretary Scott Bessent, an official with a hedge fund mindset, saw the essence: stablecoin issuers are the 'only net new buyers' of U.S. Treasury bonds.

Bessent深知 the severity of the U.S. deficit. Against the backdrop of global central banks slowing their buying of U.S. debt, stablecoin issuers' 'insatiable appetite' for short-term Treasury bonds is a major boon for the new Treasury Secretary. He views USDC, USDT, etc., not as competitors to the dollar, but as its 'vanguard,' extending dollar hegemony to countries where fiat currencies are collapsing and people prefer holding stablecoins.

Another典型 of 'short covering turning into long positions' is JPMorgan Chase CEO Jamie Dimon. He once threatened to fire any employee trading Bitcoin, but has now executed the most profitable '180-degree turn' in financial history. JPMorgan's launch of cryptocurrency-backed lending业务 in 2025 is seen as 'raising the white flag.' According to The Block:

JPMorgan plans to allow institutional clients to use Bitcoin and Ethereum as loan collateral, marking a deeper foray by Wall Street into the cryptocurrency space.

Bloomberg, citing informed sources, reported that the plan will be rolled out globally and will rely on third-party custodians to hold the collateral assets.

When Goldman Sachs and BlackRock began eroding JPMorgan's custody fee income, the 'war' quietly ended; the banks won the war by 'not fighting.'

Finally, Senator Cynthia Lummis, once seen as a 'lone crypto fighter,' has now become the staunchest supporter of the new U.S. collateral system. Her proposal for a 'Strategic Bitcoin Reserve' has moved from fringe theory on internet forums to serious congressional hearings. Her calls, while not directly pushing up Bitcoin's price, are sincere efforts.

The legal landscape in 2025 consists of two parts: 'settled' and 'still pending.' The current administration is so enthusiastic about cryptocurrency that top law firms have纷纷开设 real-time policy tracking services. For example, Latham & Watkins' 'U.S. Crypto Policy Tracker' closely follows the dynamics of various regulatory agencies that are sparing no effort in formulating new rules for DeFi. However, we are still in the 'exploratory stage.'

Currently, two bills dominate the U.S. debate:

-

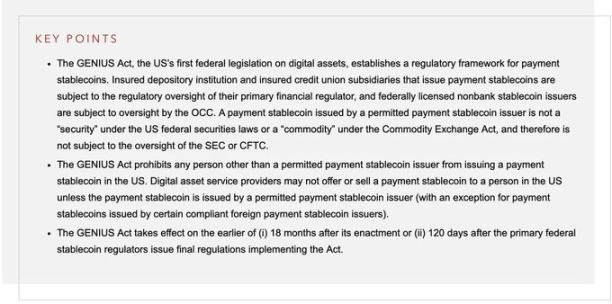

The GENIUS Act: Passed in July 2025. This act marks Washington's终于着手 regulation of stablecoins—the most important crypto asset class after Bitcoin. It mandates that stablecoins must have 1:1 reserves, thereby transforming stablecoins from a systemic risk into a geopolitical tool similar to gold or oil. The act effectively authorizes private issuers like Circle and Tether to become 'officially recognized buyers' of U.S. Treasury bonds, achieving a win-win.

-

The CLARITY Act: This market structure bill, aimed at clarifying the distinction between securities and commodities and resolving the jurisdictional dispute between the SEC and the CFTC, remains stuck in the House Financial Services Committee. Until this bill passes, exchanges exist in a comfortable but fragile 'gray area,' operating on temporary regulatory guidance rather than solid statutory law.

Currently, the bill has become a political football between Republicans and Democrats, seemingly used as a 'weapon' by both sides.

Furthermore, the repeal of Staff Accounting Bulletin No. 121 is of great significance. This accounting rule previously required banks to list custodied crypto assets as liabilities on their balance sheets, effectively preventing banks from holding cryptocurrencies. Its repeal is like opening the 'floodgates,' signaling that institutional capital can finally enter the crypto market without fear of regulatory reprisal. Meanwhile, Bitcoin-denominated life insurance products have begun to appear, and the future seems bright.

The Old World: Inherently Risk-Averse

Just as the Church once sent scientists to the stake, European authorities today have crafted complex and obscure laws whose result may merely be to scare away entrepreneurs. The gap between the vibrant, rebellious young American spirit and the僵化保守, faltering Europe has never been greater. When Brussels had the opportunity to break free from its usual rigidity, it chose to entrench itself.

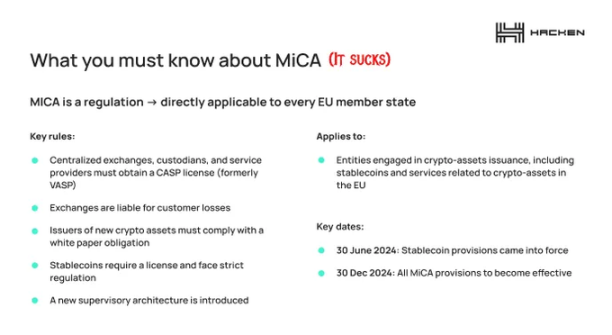

MiCA, fully implemented by the end of 2025, is a bureaucratic 'masterpiece' and an innovation 'disaster.'

MiCA is advertised as a 'comprehensive framework,' a term in Brussels parlance that often means 'comprehensive torture.' It does provide clarity—clarity that makes one want to flee.

The fundamental flaw of MiCA is 'misclassification': it regulates crypto founders as if they were sovereign banks. The compliance costs are high enough to drive most crypto startups to failure.

A memorandum from Norton Rose Fulbright objectively剖析了 the regulation:

Structurally, MiCA is an 'exclusion mechanism.' It forces digital assets into highly regulated categories and imposes on Crypto-Asset Service Providers (CASPs) a burdensome compliance architecture comparable to MiFID II, which was designed to regulate financial giants.

According to its Titles III and IV, the regulation imposes strict 1:1 liquidity reserve requirements on stablecoin issuers, effectively prohibiting algorithmic stablecoins through legal means (deeming them 'insolvent' from the start). This itself could trigger new systemic risks—imagine being declared 'illegal' overnight by Brussels?

Furthermore, issuers of 'significant' tokens will face enhanced supervision from the European Banking Authority (EBA), including capital requirements daunting enough to deter startups. Today, it is almost impossible to open a crypto business in Europe without a top-tier legal team and capital comparable to traditional financial giants.

For intermediaries, Title V彻底否定了 the offshore, cloud exchange model. Service providers must establish a physical office in an EU member state, appoint a resident director who passes the 'fit and proper test,' and implement strict asset segregation and custody. The 'whitepaper' requirement turns technical documentation into a legally binding prospectus, with any material misstatement or omission leading to strict civil liability,彻底刺破了 the anonymity 'corporate veil' cherished by the industry. One might as well just open a digital bank.

Although MiCA introduces a 'passporting right,' allowing service providers approved in one member state to operate across the entire European Economic Area, this 'unification' comes at a high cost.

It builds a regulatory 'moat'; only extremely well-capitalized institutional players can afford the enormous costs of AML integration, market abuse monitoring, and prudential reporting.

MiCA not only regulates the European crypto market but effectively prevents entrepreneurs lacking legal and financial resources from entering—precisely the situation for most crypto founders.

On top of EU law, the German regulator BaFin has沦为平庸的 a 'compliance paperwork processor,' its efficiency evident only in processing手续 for an increasingly萎靡 industry. France's ambition to become a European 'Web3 hub' has crashed into the high walls it built itself. French startups are not writing code; they are 'voting with their feet.' Unable to compete with U.S. speed or Asian innovation, talent is flowing en masse to Dubai, Thailand, and Zurich.

But the real 'death knell' is the stablecoin ban. The EU, under the guise of 'protecting monetary sovereignty,' has effectively banned non-euro stablecoins like USDT, which is tantamount to strangling the most reliable sector of the DeFi ecosystem. The global crypto economy operates on stablecoins. Forcing European traders to use illiquid 'euro stablecoins' that are无人问津 outside the eurozone, Brussels is digging itself a 'liquidity trap.'

The European Central Bank (ECB) and the European Systemic Risk Board (ESRB) have urged the EU to ban the 'multi-issuance' model (where global stablecoin companies treat tokens issued inside and outside the EU as interchangeable). The ESRB, led by ECB President Christine Lagarde, warned that a run on EU-issued tokens by non-EU holders could 'amplify financial risks within the EU.'

Meanwhile, the UK is considering setting a personal holding limit for stablecoins at £20,000, while lacking regulation for those riskier 'shitcoins.' Europe's risk-averse strategy urgently needs a complete overhaul; otherwise, regulation itself could trigger a systemic collapse.

The reason might be simple: Europe wants its citizens to remain bound to the euro, unable to participate in the U.S. economy to escape their own stagnation or even recession. As Reuters quoted the ECB warning:

Stablecoins could吸走 precious retail deposits from euro area banks, and any run on stablecoins could have broad implications for global financial stability.

The Ideal Model: The Swiss Approach

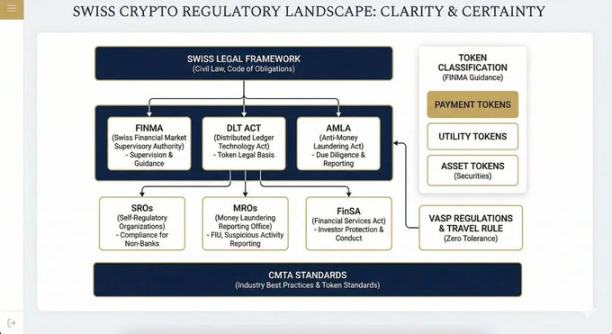

Some countries, free from partisan struggles, foolish decisions, and outdated laws, have successfully navigated the binary trap of 'over-regulation' and 'under-regulation,' finding an inclusive path. Switzerland is such a典范.

Its regulatory landscape is diverse, effective, and friendly,深受从业者和用户喜爱:

-

Financial Market Supervision Act (FINMASA): Enacted in 2007, it integrated banking, insurance, and anti-money laundering regulators, establishing the independent and unified Swiss Financial Market Supervisory Authority (FINMA).

-

Financial Services Act (FinSA): Focuses on investor protection, creating a level playing field for various financial service providers through strict conduct rules, client classification, and disclosure.

-

Anti-Money Laundering Act (AMLA): The core framework for combating financial crime, applicable to all financial intermediaries (including crypto service providers).

-

Distributed Ledger Technology Act (DLT Act): Passed in 2021, it amended ten federal laws, formally recognizing the legal status of crypto assets.

-

Virtual Asset Service Provider Ordinance: Enforces FATF rules with a 'zero-tolerance' attitude.

-

Article 305bis of the Swiss Criminal Code: Explicitly defines money laundering as a criminal offense.

-

Industry Standards: Issued by the Capital Markets and Technology Association (CMTA),虽非强制 but widely adopted.

-

Regulatory System: Parliamentary legislation, FINMA issuing detailed rules, self-regulatory organizations (SROs) for daily supervision, the Money Laundering Reporting Office (MROS) reviewing suspicious reports and referring for prosecution. The structure is clear, with明确权责.

Therefore, the Crypto Valley (Zug) has become a 'sanctuary' for crypto entrepreneurs. Its logically clear framework not only permits innovation but also provides a clear legal umbrella, reassuring users and allowing banks willing to take可控 risks to cooperate放心.

American Embrace and Utilization

The New World's acceptance of cryptocurrency is not purely out of a thirst for innovation (France has yet to send a man to the moon), but more a pragmatic choice under fiscal pressure. Having拱手让予 Silicon Valley the dominance of Web2 internet since the 80s, Europe seems to view Web3 as just another 'tax base' to be harvested, rather than an industry to be nurtured.

This suppression is structural and cultural. Against the backdrop of an aging population and an overburdened pension system, the EU cannot tolerate the rise of a competitive financial industry beyond its control. This is reminiscent of feudal lords imprisoning or killing local nobles to eliminate potential threats. Europe has a lamentable 'self-destructive tendency,' sacrificing the potential of its citizens to prevent uncontrolled change. This is foreign to the U.S., where the culture崇尚 competition,进取, and a Faustian will to power.

MiCA is not a 'development' framework but a 'death sentence.' It aims to ensure that if European citizens engage in crypto transactions, they must do so within the state monitoring grid to guarantee the government 'gets its cut,' like an obese monarch trying to squeeze dry the peasants. Europe is positioning itself as the world's 'luxury consumption colony' and 'eternal museum,' for amazed Americans to come and mourn a past that cannot be revived.

Countries like Switzerland and the UAE have jumped out of historical and structural defects. They lack the imperial baggage of defending a global reserve currency or the bureaucratic inertia of a 27-nation bloc. By exporting 'trust' through laws like the DLT Act, they have attracted foundations with core intellectual property like Ethereum, Solana, and Cardano. The UAE followed closely behind; no wonder more and more French people are 'invading' Dubai.

We are heading towards a period of 'radical jurisdictional arbitrage.'

The crypto industry will experience a geographical split: the consumer-facing side will remain in the U.S. and Europe, subject to full identity verification, high taxes, and integration with traditional banks; while the core protocol layer will migrate entirely to rational jurisdictions like Switzerland, Singapore, and the UAE.

Users will be global, but founders, VCs, protocols, and developers will have to consider leaving their home markets to find more conducive places to build.

Europe's fate is恐将沦为 a 'financial museum.' It is building a glossy but useless, even致命 for actual users, legal system for its citizens. One can't help but ask: Brussels technocrats, have you ever bought Bitcoin, or cross-chain transferred a stablecoin?

Cryptocurrency becoming a macro asset is inevitable, and the U.S. will maintain its position as the global financial center. Bitcoin-denominated insurance, crypto-backed loans, crypto reserves, unlimited VC support, a vibrant developer ecosystem—the U.S. is building the future.

A Worried Conclusion

In summary, the 'Brave New World' being built in Brussels resembles not a coherent digital framework, but an awkward patchwork trying to graft 20th-century bank compliance clauses onto 21st-century decentralized protocols, designed mostly by engineers who know nothing about the ECB's temper.

We must actively advocate for another system: one that prioritizes real-world needs over administrative control. Otherwise, we will彻底扼杀 Europe's already anemic economy.

Unfortunately, cryptocurrency is not the only victim of this 'risk paranoia.' It is just the latest target of a well-paid, complacent bureaucratic class. This group wanders the lifeless postmodern corridors of capitals, their heavy-handed regulation恰恰暴露了他们缺乏现实经验. They have never experienced the繁琐 of account verification, the奔波 of applying for a new passport, the艰辛 of obtaining a business license. Therefore, although Brussels is filled with so-called 'technocrats,' crypto-native founders and users have to deal with a group mired in incompetence,只会制造有害立法.

Europe Must Pivot, Act Now

While the EU is busy tying itself up in red tape, the U.S. is actively planning how to 'normalize' DeFi, moving towards a framework beneficial to multiple parties. Re-centralization to some extent through regulation is inevitable; the collapse of FTX早已在墙上写下预警.

Investors who suffered heavy losses crave justice; we need to break free from the current cycle of meme coin mania, cross-chain bridge vulnerabilities, and regulatory chaos—this 'Wild West.' We need a structure that allows traditional capital (Sequoia, Bain, BlackRock, Citi, etc., have already taken the lead) to enter safely, while protecting end-users from predatory capital.

Rome wasn't built in a day, but the crypto experiment is fifteen years old, and its institutional foundations are still深陷泥潭. The window to build a functional crypto industry is closing rapidly; hesitation and compromise in war will lose everything. Both sides of the Atlantic need swift, decisive, and comprehensive regulation.

If this cycle is truly about to end, now is the best time to salvage the industry's reputation and compensate the serious investors who have been harmed by bad actors for years.

Those weary traders from 2017, 2021, 2025 demand a thorough清算, and a final answer to the cryptocurrency question; and most importantly, for our world's favorite assets to迎来他们应得的、崭新的历史高点.