Written by: Thejaswini M A

Compiled by: Chopper, Foresight News

Any default option will eventually become the choice for the majority. This is known as the "default effect" in behavioral economics.

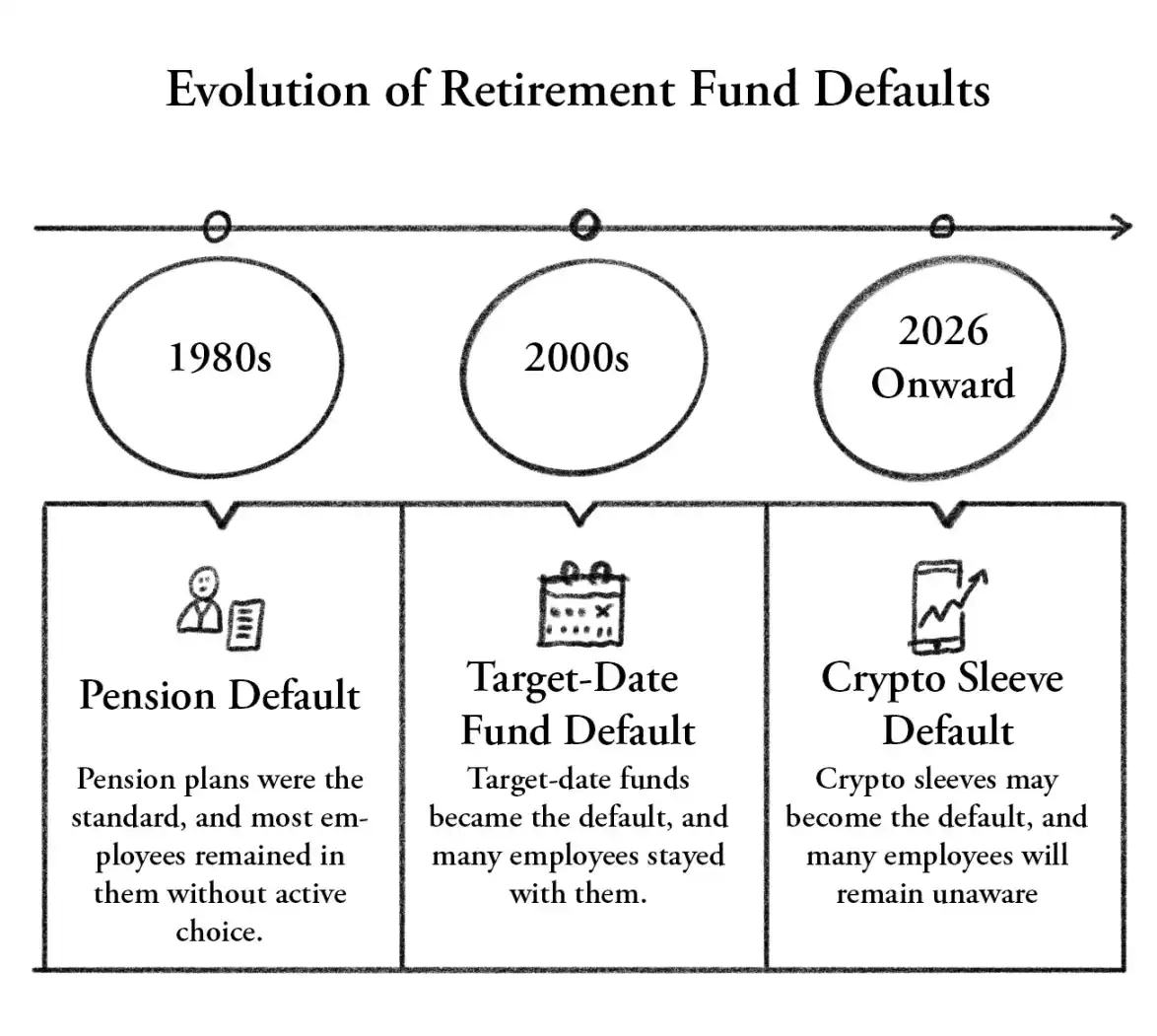

The history of the entire U.S. pension system is a history of default options. In the 1980s, the default option shifted from traditional pensions to 401(k) plans, which most employees passively accepted without fully understanding what they were giving up. In the early 2000s, target-date funds became the default option for the vast majority of pension plans, and tens of millions of people ended up holding these funds without ever actively choosing them.

Each shift in the default option involved the transfer of massive amounts of capital and ultimately changed the way a generation retired. Most of those affected didn't realize it until they checked their statements later.

A new default option is set to emerge in the coming years. Right now, it doesn't look like a default option; it looks more like a proposed rule from the Department of Labor, currently undergoing a 60-day public comment period. It is carefully worded, emphasizing fiduciary duty and compliance with the Employee Retirement Income Security Act (ERISA). They often start as options, gradually become popular, and eventually become the default.

On March 30, the U.S. Department of Labor issued a rule that, for the first time, opened the door to cryptocurrencies for the $12 trillion U.S. 401(k) pension market. Indiana had already legislated in March, requiring state pension plans to offer at least one cryptocurrency investment option by July 2027; the Wisconsin pension system already holds $321 million in Bitcoin ETFs; Michigan has allocated $45 million to Bitcoin and Ethereum ETFs. Florida and New Jersey are also advancing similar policies.

First, let's look at how cryptocurrencies were previously kept out.

The Wall Blocking Cryptocurrencies

Before this rule, cryptocurrencies were not explicitly banned by law from entering 401(k) plans. The real barrier was more effective than a ban.

Under the Employee Retirement Income Security Act (ERISA), which regulates pension plans, fiduciaries are personally liable for investment decisions that lose money. It's not the company or the fund that is held accountable, but the individual who made the decision.

Since 2016, there have been over 500 lawsuits alleging ERISA violations; since 2020, related settlements have exceeded $1 billion. Pension plan managers have seen their peers sued over excessive fees, poor index fund choices, and issues with mutual fund share classes. These lawsuits are endless, come from unexpected angles, and target individuals directly.

Consider the incentive structure this creates: You manage a pension plan, you buy Bitcoin, and then Bitcoin crashes 50%. A plaintiff's lawyer sends a letter, and you spend three years defending yourself in discovery.

Conversely, if you don't* add Bitcoin, even if it goes to $200,000, no one will sue you for it.

The rational choice was always: stay away from crypto. And almost everyone did.

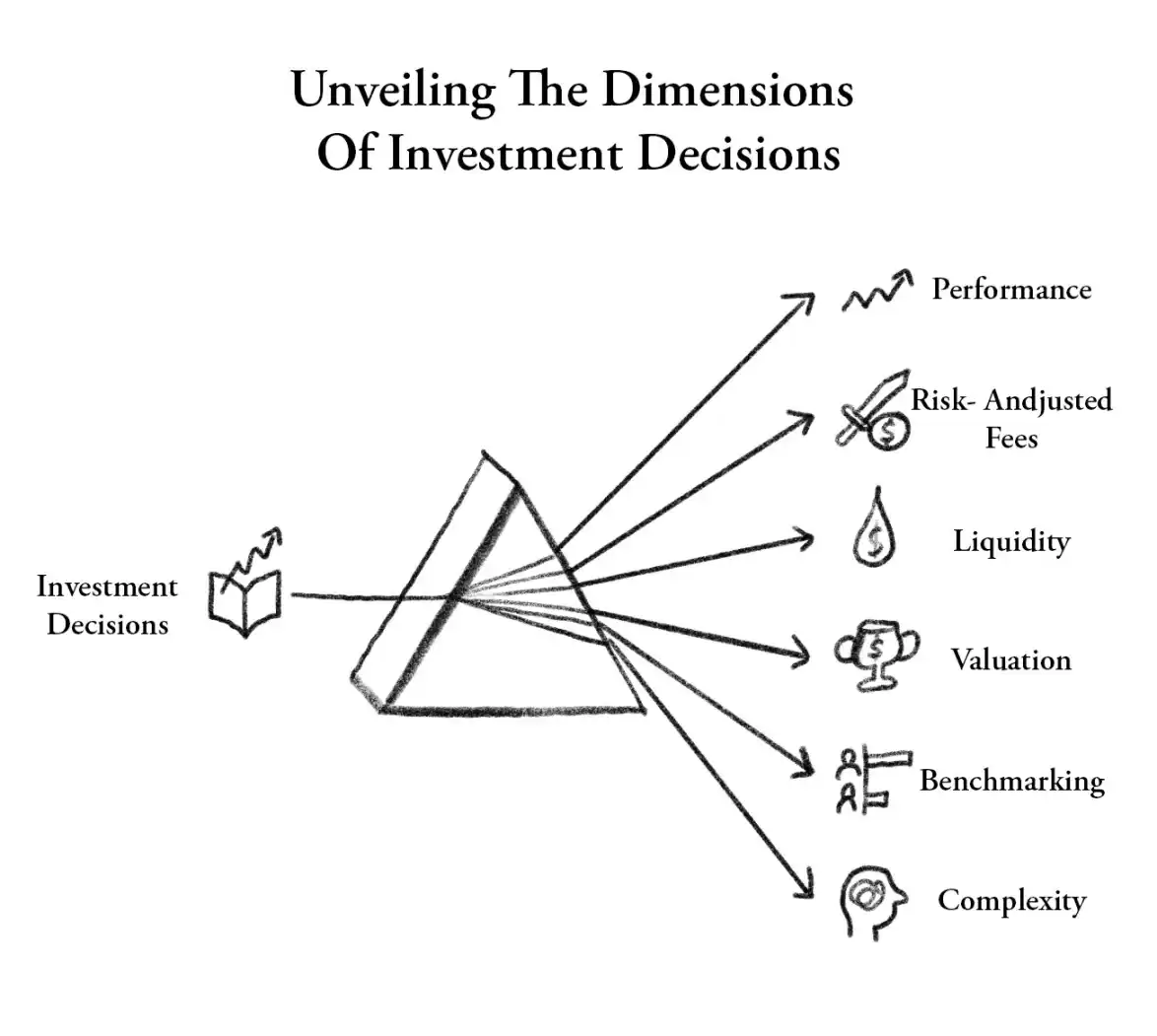

The Biden administration's Labor Department in 2022 went further, explicitly stating that fiduciaries must exercise "extreme care" before touching digital assets. That guidance has now been withdrawn and replaced with a six-factor safe harbor rule: as long as a fiduciary follows a written process reviewing performance, fees, liquidity, valuation, benchmarks, and complexity, they will be deemed to have fulfilled their prudent duty under ERISA. As long as the process is compliant, even if the asset price falls, they are protected from personal liability.

Don't mistake the rule change for a shift in market fundamentals. For the average investor, crypto's volatility remains the same. This rule really protects the fund managers. It corrects the imbalanced legal risk that marginalized crypto for a decade, finally allowing fiduciaries to feel safe saying yes.

The Conduit: Target-Date Funds

The Labor Department itself anticipates that the primary access point will be target-date funds. This is crucial for understanding the practical impact on the average saver.

Most people, upon starting a job, are defaulted into a target-date fund. You just pick the fund closest to your expected retirement year, say the 2045 fund, and it automatically adjusts its stock/bond allocation as you age, becoming more conservative closer to the target date. The vast majority of people who hold these funds never look at them a second time.

If crypto assets are allocated through target-date funds, investors won't actively go out and buy Bitcoin. Their retirement portfolio will automatically allocate 1%–3% to Bitcoin, managed and automatically rebalanced by a professional institution.

Just as many people have gold in their 401(k) without knowing it. That's how gold entered the pension system—through the same vehicle, the same logic, without asking the actual owners of the money.

Fidelity led the charge in 2022, offering plan sponsors the option to include Bitcoin in their investment menu even before the Biden administration's guidance. At the time, Fidelity allowed plan sponsors to include digital asset investments in their portfolio, with participants to invest up to 20% of their account balance in Bitcoin. What has been missing is the legal assurance for plan sponsors to feel comfortable allocating to Bitcoin without assuming personal liability. That assurance is now being formulated.

$12 Trillion

U.S. 401(k) plans hold about $12 trillion. Even a 1% allocation would mean roughly $120 billion flowing into digital assets, more than the total value locked in all of DeFi. Even just 0.1% would be $12 billion, on par with the top five Bitcoin ETFs.

Every previous wave of institutional crypto adoption came from active decisions: ETF buyers actively buying, MicroStrategy actively holding, banks actively building custody products. Those decisions can be reversed: a CFO can sell the treasury position, ETF investors can redeem.

The 401(k) channel is structurally different, something the industry has been waiting for since the spot ETF listings. Pension money is passive money, held for 30-year horizons. It doesn't panic sell on crashes, isn't swayed by the fear and greed index, and doesn't care what oil did last week.

As Morgan Stanley's Amy Oldenburg points out, currently about 80% of crypto ETF trading comes from self-directed investors, not advisor-recommended allocations. The 401(k) market is almost entirely driven by professional advisors. The DOL's new rule opens up a channel that was previously structurally difficult to access because the people controlling the gate bore excessive personal risk.

This has been a point crypto has emphasized for years: the real wave of adoption won't come from traders or tech early adopters, but when the infrastructure of ordinary people's savings systems automatically turns towards crypto. Target-date funds are that infrastructure.

Risks and Concerns

A 50% drop in a trading account is just a bad quarter. A 50% drop in a 55-year-old teacher's retirement account is a different matter entirely.

Bitcoin has drawn down over 80% in past bear markets, around 50% in this cycle, which some interpret as "maturity." But losing half your retirement savings doesn't feel any better because it's called "progress."

TD Cowen's Jaret Seiberg writes that he remains skeptical that fiduciaries will move until courts confirm the safe harbor truly protects against lawsuits. ERISA is a process-based law, but its ultimate interpretation lies with the courts.

The safe harbor might hold on paper, but if a target-date fund with crypto allocation drops 40% in a bear market, triggering the first wave of lawsuits, whether it holds up is an open question.

The comment period for the rule ends on June 1st. The Labor Department can modify the rule, withdraw it, or simply push it forward. Even if the final version is unchanged, moving from a proposed rule to actual money in pension accounts involves compliance teams, investment committees, recordkeeper system integrations, and fiduciary reviews. This will take months, more likely years.

Indiana's July 2027 deadline is a hard mandate, while the federal rule is a soft permission—their implementation timelines will be starkly different.

In the 1980s, stocks entered pensions through mutual fund; in the early 2000s, international stocks entered through target-date funds; followed by REITs, TIPS, commodities. Their arrival wasn't because retirement savers asked for them.

Cryptocurrency is now at that inflection point. Spot ETFs are the product, the DOL rule is the regulatory配套, Fidelity/Schwab/Morgan Stanley are the distribution channels, the CLARITY Act writes the asset classification into statute law, providing the legal basis for prudent examination by fiduciaries.

All the pieces are in place, except the last one.

Someday in the future, a pension plan manager adds Bitcoin to a target-date fund. Bitcoin crashes 60%. A retiree loses a chunk of their savings. Lawyers file a lawsuit.

At that moment, the only question that matters is: Will the judge agree that the safe harbor protected the person who made that decision.

Right now, nobody knows the answer. The Labor Department believes it will. TD Cowen believes it could take years to find out.

Until the first case is heard and adjudicated, every pension plan manager in America is being asked to trust a piece of paper that has never been tested in court.