Goldman Sachs executed a rare strategic about-face in less than a month—transitioning from actively pitching the HALO concept to investors to proactively shorting its "overheated" component stocks, reflecting concerns about the crowding in heavy-asset trades.

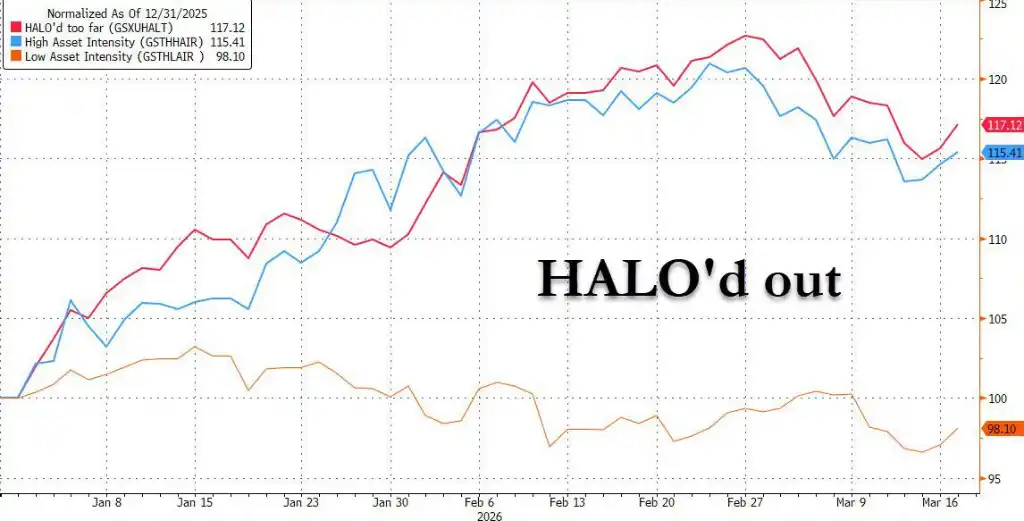

On Tuesday, Faris Mourad, head of Goldman's thematic trading team, introduced the short basket GSXUHALT in a latest report, specifically targeting U.S. companies that are asset-intensive but have zero or negative earnings growth expectations, yet whose stock prices have surged significantly with the HALO trend. Goldman believes the market's pursuit of heavy-asset stocks has become indiscriminate, with gains in some individual stocks severely disconnected from fundamentals.

The immediate implication of this shift for the market is that the honeymoon period for the HALO trade may be over. Goldman data shows the GSXUHALT basket has begun to decline after peaking at the end of February, and the firm recommends investors pair this short position with their favored thematic long opportunities.

One Month Ago: Goldman Strongly Promoted HALO, Heavy-Asset Narrative Swept Wall Street

Going back to February 24th, Goldman Sachs Global Investment Research published a report titled "The HALO Effect: Heavy Assets, Low Obsolescence in the AI Era," joining major banks like JPMorgan in actively promoting the HALO concept—the combination of Heavy Assets and Low Obsolescence.

The logic at the time was clear and powerful: The rapid rise of AI is creating a dual impact on light-asset industries. On one hand, AI is disrupting profitability expectations in sectors like software and IT services, leading the market to reassess the terminal value of these industries; on the other hand, tech giants have embarked on an unprecedented capital expenditure cycle to maintain a competitive advantage in computing power—according to Goldman data, the top five U.S. tech giants are expected to have capital expenditures of approximately $1.5 trillion between 2023 and 2026, with spending in 2026 alone potentially exceeding $650 billion, surpassing their total pre-AI era spending.

Goldman's data at the time was equally impressive: Since 2025, its heavy-asset portfolio (GSSTCAPI) has cumulatively outperformed its light-asset portfolio (GSSTCAPL) by 35%. At the macro level, higher real interest rates, geopolitical fragmentation, and supply chain restructuring were seen as collective structural tailwinds for heavy-asset stocks.

About-Face: Indiscriminate Market Pursuit, Some Heavy-Asset Stock Gains Have Lost Fundamental Support

However, just one month later, Goldman's stance changed significantly.

Mourad pointed out in the latest report that the companies covered by the GSXUHALT basket are those that rose with the overall heavy-asset trend but themselves have no earnings growth expectations and returns that significantly lag behind high-quality HALO targets. In other words, the market, in chasing "AI-insulated" attributes, has indiscriminately poured funds into all heavy-asset stocks, no longer distinguishing between high and low quality.

Data confirms this judgment: The GSXUHALT basket's gains have actually surpassed those of the high-quality high asset intensity basket (GSTHHAIR), meaning low-return, no-growth heavy-asset stocks have instead beaten truly competitive peers. Meanwhile, the basket's stock price movement was still in sync with earnings expectations until late last year, after which a significant divergence appeared.

In screening for GSXUHALT components, Goldman selected companies from the highest asset-intensity industries in the Russell 1000 index, while剔除 all targets related to long-term trends like satellites, robotics, quantum computing, and AI, retaining only stocks with significant year-to-date gains but flat or downward revised earnings expectations. The basket's average asset intensity ratio is approximately 1.4.

Valuation Signal: Heavy-Asset Premium at Historically Medium-High Levels

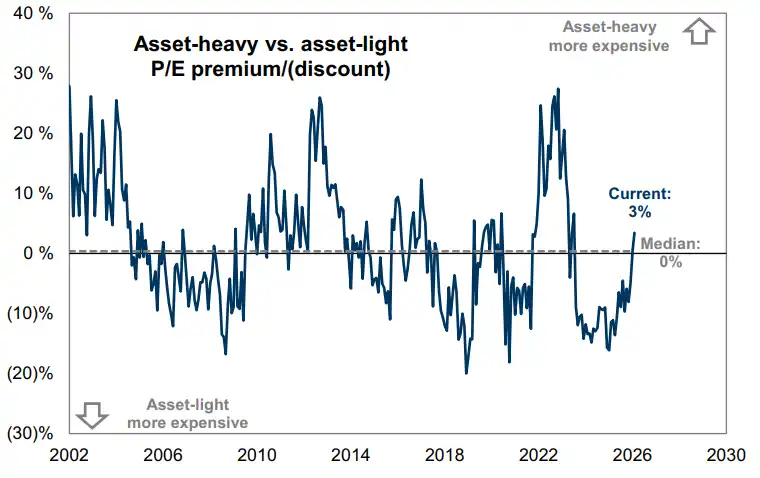

Goldman's research last month already indicated that heavy-asset stocks are currently trading at a valuation premium relative to light-asset stocks. As of last month, the P/E premium for heavy-asset stocks was about 3%, sitting at the 62nd percentile over the past few decades. While still below historical peaks seen in 2004, 2012, and 2022, they are no longer cheap.

Since last November, Goldman's sector-neutral heavy-asset basket (GSTHHAIR) has cumulatively outperformed the light-asset basket (GSTHLAIR) by about 20%. In Goldman's view, the root of this strong performance by heavy assets lies in investors' strong demand for "AI-insulated" assets—namely, the search for physical asset-class stocks that are less susceptible to AI disruption and have underperformed for years.

Goldman recommends pairing the GSXUHALT short position with the firm's favored thematic long opportunities. The report notes that recent market adjustments have created the largest "buy the dip" opportunity in global equities since "Liberation Day," allowing investors to establish long exposure in directions supported by long-term trends while shorting heavy-asset stocks lacking fundamental support.

Behind this strategic shift is Goldman's clear judgment on the internal differentiation within the HALO trade: Not all heavy-asset stocks are worth holding. The time has come to distinguish between targets with true competitive moats and upward earnings momentum and those merely riding the coattails of the "heavy asset" label.