The US Senate Banking Committee’s crypto market structure push is running into a dense wall of amendments ahead of Thursday’s markup, with lawmakers filing more than 100 proposed changes to the CLARITY Act. The amendment rush puts stablecoin rewards, crypto firms’ access to the Federal Reserve system and even the use of digital assets for tax payments at the center of Washington’s latest fight over crypto regulation.

According to Politico, committee members submitted more than 100 amendments before the markup vote. Crypto journalist Eleanor Terrett reported that Senator Elizabeth Warren alone filed more than 40 amendments, including one that would prevent the Federal Reserve from issuing master accounts to crypto companies. Terrett also flagged an amendment from Senator Jack Reed that would “prohibit crypto from being used as legal tender, for example, to pay taxes.”

That language would cut directly against one of the industry’s longer-running policy goals: expanding digital assets beyond investment and trading into payments, settlement and public-sector use cases. Terrett noted the contrast with prior pro-Bitcoin tax-payment proposals, writing that Representative Warren Davidson had introduced a bill last year “to do that very thing” with BTC.

Crypto Bill Enters High-Stakes Senate Markup

The latest clash comes after Senate Banking Committee Chairman Tim Scott, Senator Cynthia Lummis and Senator Thom Tillis released new market structure text that will serve as the basis for the committee markup. The committee said the text reflects negotiations with Democrats and input from lawmakers, regulators, law enforcement, financial institutions, innovators and consumer advocates. Scott framed the bill as a consumer-protection and national-competitiveness measure.

“Over the past year, we have listened, negotiated, and strengthened this bill because families, small businesses, investors, and innovators all benefit from clear rules of the road,” Scott said. “This bill reflects serious, good-faith work across the Committee and delivers the certainty, safeguards, and accountability Americans deserve.”

The most immediate fault line remains stablecoin rewards. The Senate text would ban rewards on idle stablecoin balances that closely resemble bank deposits, while allowing rewards tied to transaction-based activity, such as stablecoin payments. The SEC, CFTC and Treasury Department would be tasked with issuing joint rules to implement that provision.

Banks are not satisfied. Brendan Pedersen reported that Reed and Senator Tina Smith filed an amendment that would incorporate bank-requested changes to stablecoin yield restrictions, forcing lawmakers to choose between the crypto and banking industries. The amendment would target rewards “substantially similar” to deposit interest, a phrase that goes to the core of the banking lobby’s argument: that crypto platforms should not be allowed to compete with deposits through yield-like incentives while avoiding bank-style regulation.

Terrett reported separately that American Bankers Association members had sent more than 8,000 letters to Senate offices urging lawmakers to revise the stablecoin-yield compromise. The ABA has argued that the current language does not adequately close what it calls a loophole allowing exchanges and other digital asset service providers to bypass the GENIUS Act’s ban on interest or yield on payment stablecoins.

The bill also reaches well beyond stablecoins. Digital commodity exchanges, brokers and dealers would be treated as financial institutions under the Bank Secrecy Act, bringing them into anti-money-laundering, customer-identification and due-diligence regimes. The text would also allow crypto companies to raise up to $50 million annually, and up to $200 million total, without SEC registration, while clarifying that tokenized securities remain subject to securities law.

The political path is still fragile. Terrett said Senate Minority Leader Chuck Schumer appeared engaged in a Democratic member meeting and eager for members to reach a “yes” on the CLARITY Act, but stressed that ethics negotiations needed to move further before Thursday’s markup. Warren, the committee’s top Democrat, has been pressing that issue hard, saying the bill “puts investors, our national security and our entire financial system at risk” and would “turbocharge Donald Trump’s crypto corruption” without stronger conflict-of-interest provisions.

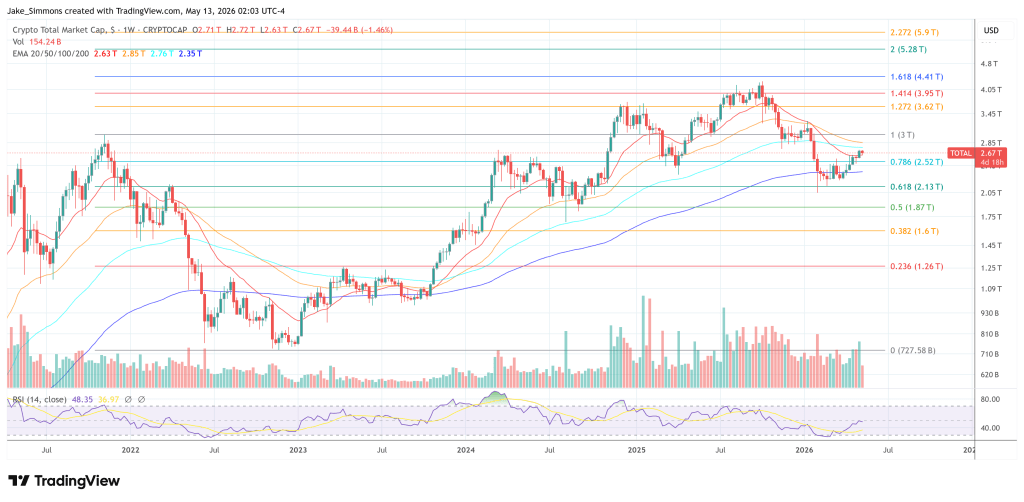

At press time, the total crypto market cap stood at $2.67 trillion.