Author: Zuo Ye

The Clarity Act is progressing smoothly, with multiple benefits expected mid-year for stablecoins, tokenization, and DeFi development. However, prohibiting passive yield on stablecoins will also cast some uncertainty over the on-chain outlook.

This is not unwarranted anxiety. From ETFs, DAT, to Wall Street's attempts at RWA, the battle for crypto pricing power continues. Compliance often means accepting established frameworks, snuffing out grassroots innovation in the name of stability.

ETFs sacrifice BTCFi, DAT creates systemic crises, RWA rejects existing public chains.

On the surface, the Clarity Act compresses the arbitrage space for offshore dollar stablecoins like $USDT. But in reality, by separating and recombining payment and yield, the US is experimenting with a new model for dollar circulation beyond gold, oil, and credit.

The story of payment stablecoins is basically over; the chapter of yield-bearing stablecoins is about to begin.

Surround on Three Sides, Payment Stablecoins

Setting my heart on money learning pleasure more than Thee.

There has always been a question: How exactly does the Genius Act facilitate the "payment stablecoin" narrative to become reality?

As Wall Street giants lay the groundwork for tokenization on the eve of the Clarity Act's passage, this confusion intensifies. Yes, you heard right—they are laying the groundwork for tokenization business to enable stablecoin yield.

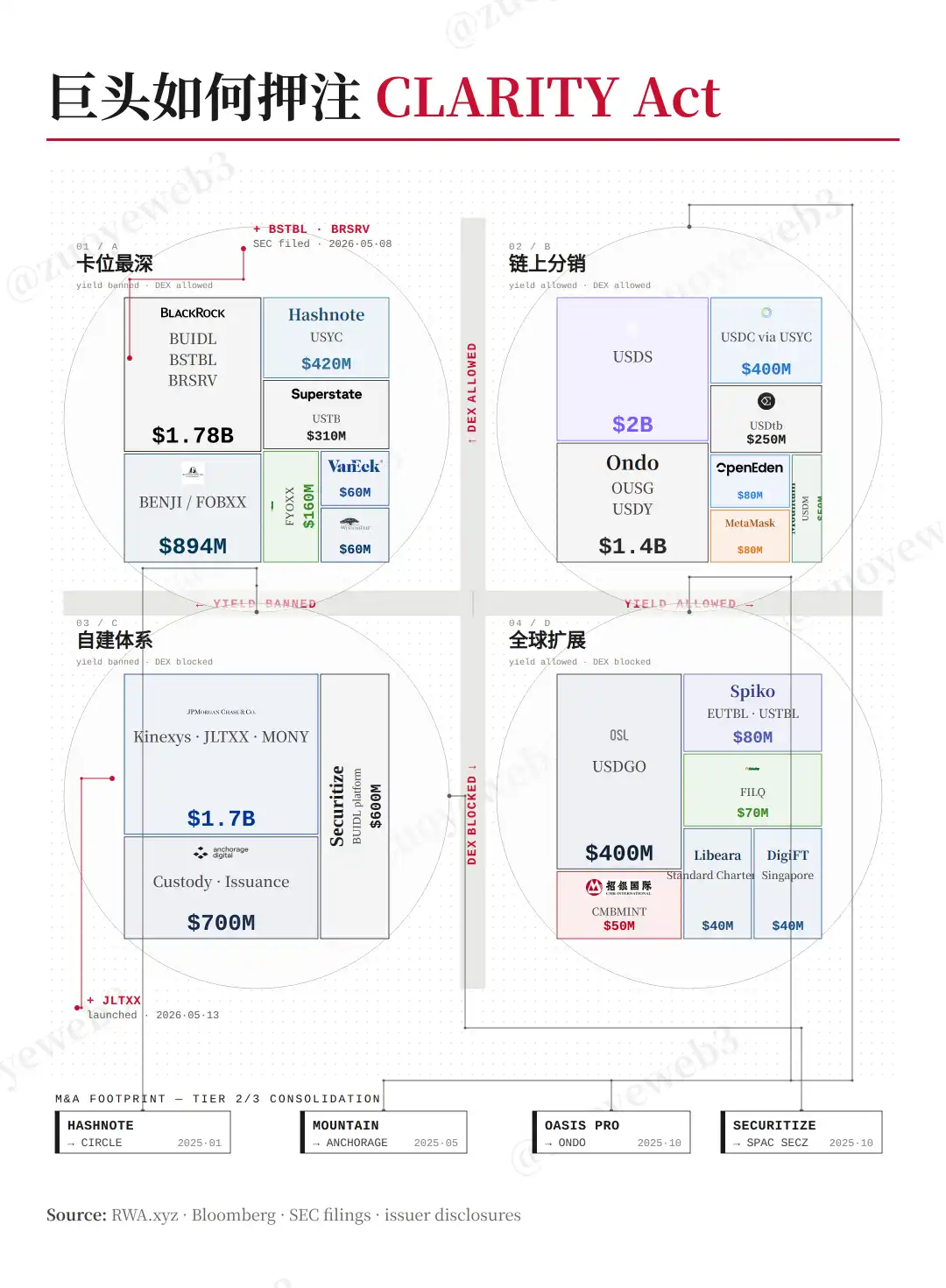

- On May 8th, besides BUILD, BlackRock plans to launch two new TMMFs (Tokenized Money Market Funds): BSTBL and BRSRV.

- On May 13th, besides MONY, JPMorgan Chase launched a second TMMF, JLTXX.

Moreover, BlackRock explicitly stated that the new products aim to meet the growing needs of stablecoin issuers, while JPMorgan also emphasized compliance with relevant qualification requirements of the Genius Act.

Examining the text closely, the Genius Act indeed adds provisions for tokenization, allowing tokenized forms of US Treasuries and dollars to serve as stablecoin reserve assets.

This doesn't explain the relationship between stablecoins, tokenization, and payment. We need to explore further.

Under the Genius Act, stablecoin issuance licenses are allocated to the OCC's federal charter bank mechanism. Such banks cannot take deposits, require full reserves, and must not encroach on commercial bank lending business.

In this scenario, policy creates market demand. Stablecoin issuers either build their own reserves—like USDT and USDC frantically buying US Treasuries, surpassing many sovereign nations—or directly purchase RWA assets like TMMFs. This is crucial for stablecoins like USDS/sUSDS that rely on profit-sharing to attract users.

- It avoids the complex process of subscribing to and redeeming US Treasuries.

- On-chain profit-sharing and real-time yield generation better align with user habits.

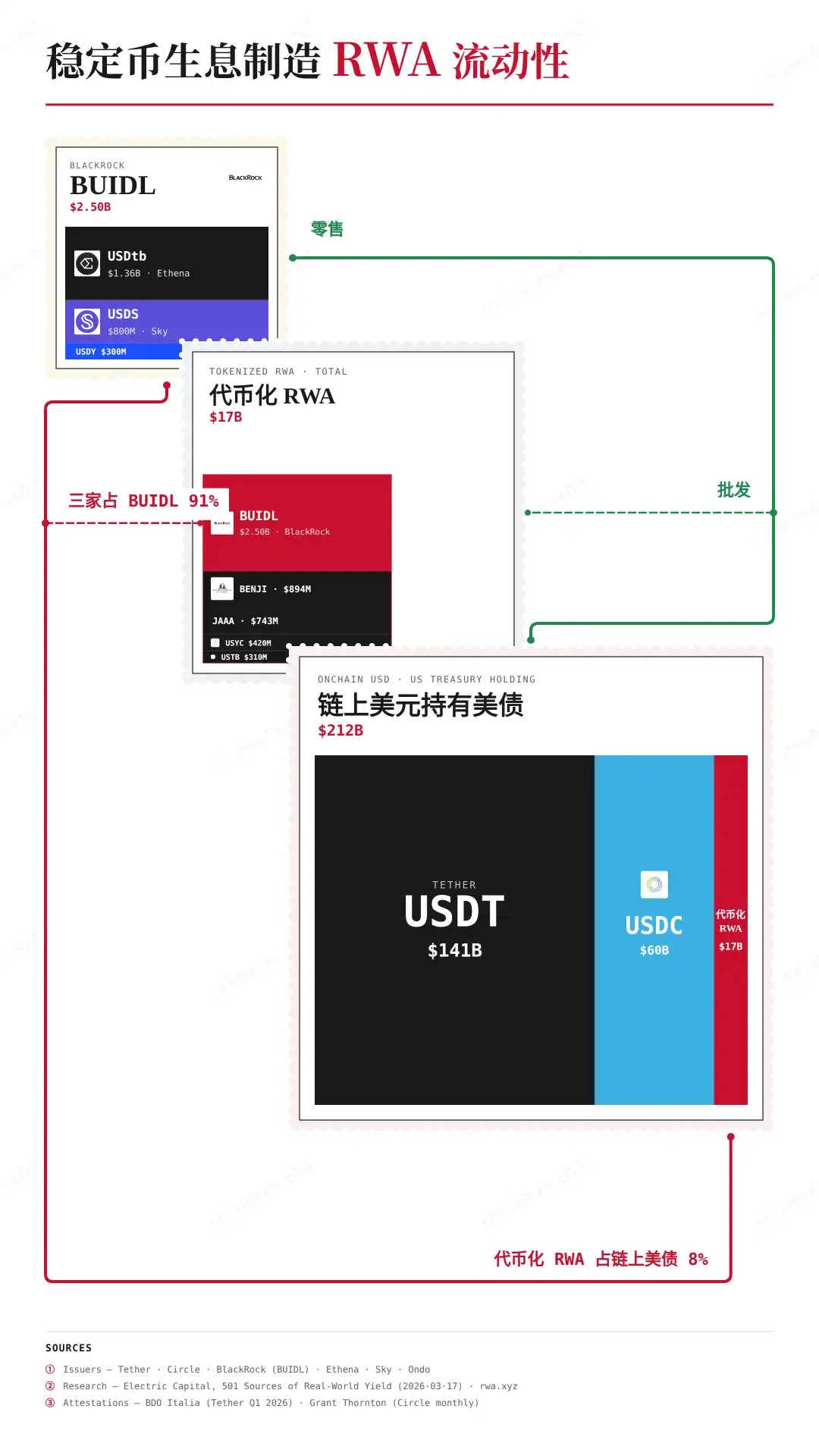

According to data from @ElectricCapital, 98% of BlackRock's BUIDL shares were subscribed to by various yield-bearing stablecoin issuers.

And, most ingeniously, retail investors cannot directly purchase tokenized products. Policy shapes the market structure; this is the secret of how the Genius Act creates "payment stablecoins."

An act cannot solely rely on coercive power to make market participants comply; otherwise, USDT wouldn't have remained underground for so many years. Only by following market trends can it achieve significant results with minimal effort.

Caption: TMMF Supporting Payment Stablecoins

Data Source: @ElectricCapital

BlackRock's tokenized products, while circulating on-chain, cannot be purchased "permissionlessly" and still require compliance with KYC, accredited investor checks, etc., essentially targeting B2B sales.

You cannot monitor decentralized individual transactions, just as the US government cannot monitor the circulation of physical dollar cash. However, monitoring a few giants is much simpler.

By recognizing tokenized assets, the US cleverly constructs a feasible framework among stablecoin issuers, Wall Street giants, and regulators. The stablecoins users receive can only be used for payment because they cannot generate yield.

A single Genius Act binds stablecoins and tokenization together. This also answers the earlier confusion: it makes stablecoins the retail endpoint layer for US Treasuries.

The previous dollar relied on the commercial banking credit mechanism; the future dollar will rely on the intermediary role of tokenization companies.

Arbitrage Space, Yield-Bearing Stablecoins

Caring for worldly things more than God.

If the Genius Act's recognition of tokenization created payment stablecoins, then the Clarity Act's restrictions on tokenization guide the development of yield-bearing stablecoins.

The importance of yield-bearing lies not in the banking sector's fear of deposit outflows—JPMorgan has difficulty opening accounts, Coinbase has difficulty making money.

Consider this: Under the Clarity Act, if users choose to stake for yield, ideally, the stablecoin issuer's interest can only come from US Treasury products.

But this raises new questions. Issuers of on-chain stablecoins like Sky/Ethena, in a sense, don't need an OCC bank license first. Therefore, new arrangements are needed for yield, especially DeFi yield.

Excessive regulatory costs are the essential reason for Congress's "lenient" arrangements for DeFi development. Beyond that, the dollar needs stablecoins as a distribution channel.

Caption: Giants Rushing into the Clarity Act

Image Source: @zuoyeweb3

This distribution is divided into two major categories: first, the B2B customer acquisition path among giants; second, on-chain and cross-regional C2C arbitrage issuance.

Among giants, the bet is on the strictness of the "ban on passive yield," which also changes the intermediary role. If DeFi is also restricted, consortium chain models may revive; if relatively relaxed, deeper cooperation with on-chain stablecoins is possible.

Furthermore, the giants' intermediary model is hard to bypass. Ondo and others choose to serve as the retail distribution layer for giants, while OSL and others choose the overseas compliant dollar stablecoin track.

Extending further, Sky's inclusion of diversified "RWAs" in USDS reserves is essentially leveraged arbitrage, quietly switching from full reserves to fractional reserves.

A mainstream demand emerging next: How to increase stablecoin yields based on US Treasuries? This requires more complex financial engineering designs, which is where various DeFi yield strategies come into play.

It can be seen that the yield mechanism targets offshore dollar stablecoins like $USDT, aiming to replace their position as Treasury buyers with BlackRock's TMMFs.

For on-chain dollars and compliant offshore dollars, new arbitrage spaces will emerge. They cannot stably earn scaled US Treasury yields and must continuously promote utilization growth, indirectly promoting dollar circulation and stable Treasury purchases.

In this process of tightening and loosening, users will be incentivized to use stablecoins because holding them leads to devaluation. The interest generated from usage flows back into the US financial system because the underlying asset is US Treasuries.

This is the true purpose of the Clarity Act: to create individual demand for the dollar on a global scale. Stablecoin issuance requires US Treasuries, stablecoin yield requires US Treasuries, ultimately completing the cycle.

Conclusion

To transcend the limitations of sovereign states, one must rely on rigid demand like payment.

But to promote the adoption of stablecoins, one must rely on direct mechanisms like yield.

The focus of both the Genius Act and the Clarity Act lies in the intertwining of stablecoins and yield. Because DeFi and cross-regional arbitrage cannot be fully controlled, Wall Street is needed as an intermediary to manage yields. This also gives us reassurance: Regardless of whether the Clarity Act passes on schedule, arbitrage mechanisms never sleep.