Original | Odaily Planet Daily (@OdailyChina)

Author | Ding Dang (@XiaMiPP)

The beginning of 2026 delivered a heavy blow to DAT (Digital Asset Treasury) companies.

BTC retreated from the阶段性高点 (stage high) of $120,000 in December 2025 to around $60,000, a drop of nearly 50%. ETH was not spared either, falling below the $2,000 mark, almost erasing all gains since May 2025. That was precisely the time when a group of DAT companies, represented by SharpLink and Bitmine,高调宣布 (loudly announced) their strategic transformations and made large-scale allocations to加密资产 (crypto assets).

What does this mean? It means that those listed companies or institutions that once regarded BTC and ETH as "corporate strategic reserves" are now collectively mired in浮亏 (paper losses), with账面亏损 (book losses) ranging from hundreds of millions to billions of dollars. Top players like Strategy and Bitmine are still gritting their teeth and increasing their holdings, trying to maintain the narrative stability of "long-term believers"; but more small and medium-sized or highly leveraged DAT companies have already begun substantial reductions or even阶段性清仓 (phased liquidation).

Crypto is never short of stories. If 2025 was the year of "writing faith into financial reports," then 2026 is the test of "how faith survives a bear market." When prices retreat, leverage tightens, and the financing environment reverses, can these DAT companies still支撑住 (hold up) their balance sheets?

Odaily Planet Daily will拆解 (break down) several representative cases that have already started "selling to stop the bleeding," looking at how much they sold, why they sold, and what they will do next.

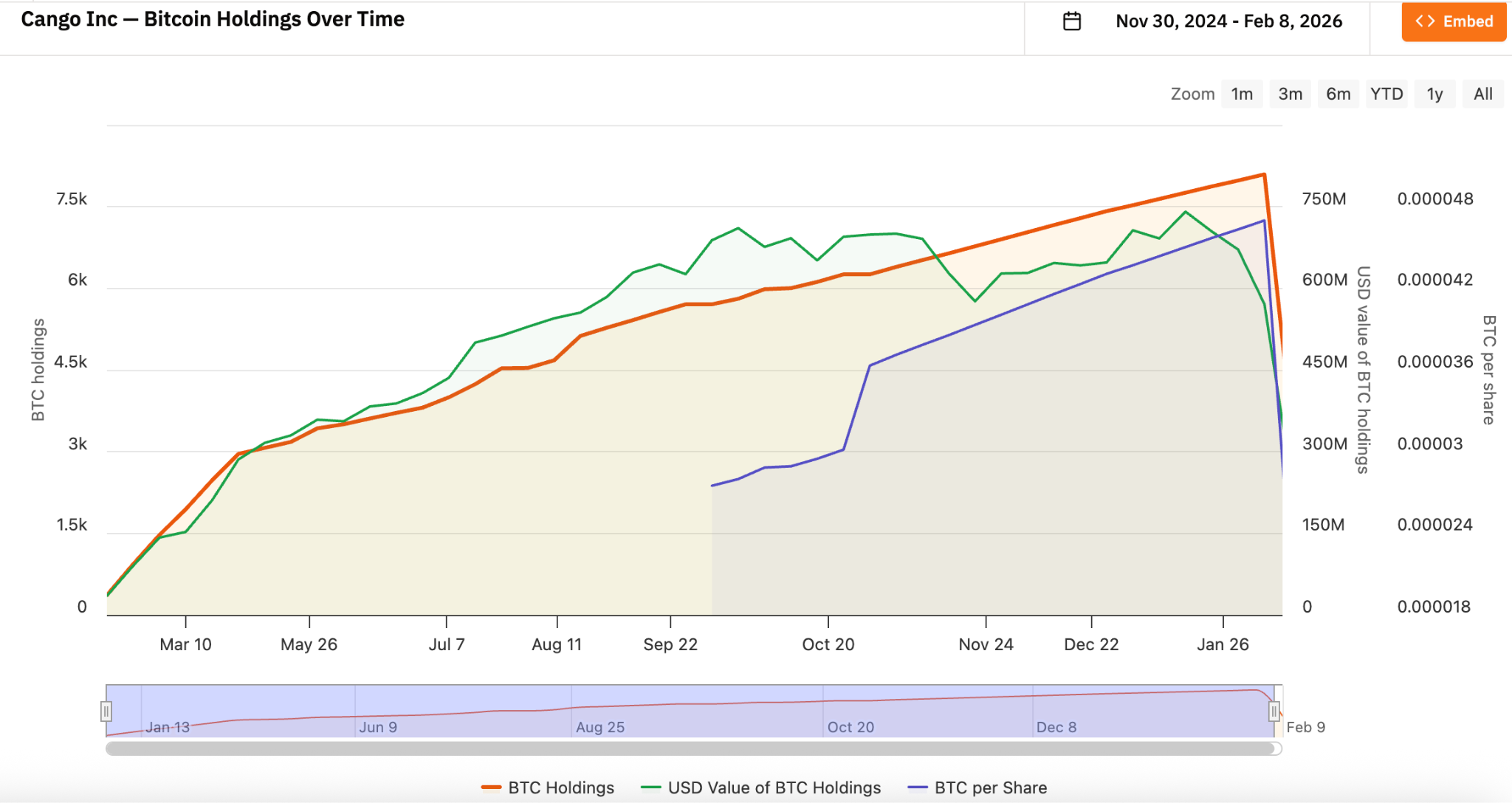

Cango Inc. (NYSE: CANG): The Leverage Limit of the Mining Model

On February 9th, Cango disclosed that it had sold 4,451 bitcoins on the open market, with net proceeds of approximately $305 million, and used all the funds to repay a loan collateralized by BTC. This transaction size was close to half of its previous holdings, leaving only 3,645 BTC on its books after the sale.

Cango was founded in 2010 and is headquartered in China. It was initially a well-known automotive transaction service platform. Starting from November 2024, Cango officially entered the digital asset field, transforming into a Bitcoin mining enterprise through business restructuring and strategic pivoting, and regarding BTC as the core reserve asset of the enterprise. Cango's Bitcoin strategy initially leaned towards HODL + mining accumulation, meaning not selling coins and relying on hash rate to continuously accumulate. This model can be self-reinforcing in a rising price cycle: rising coin prices increase net asset value, increased net asset value enhances financing capability, and financing capability in turn supports hash rate expansion.

Cango began continuously accumulating Bitcoin starting November 2024, and its Bitcoin holdings once ranked as the world's second-largest mining enterprise after MARA Holdings.

Related reading: 《寻找潜力加密美股:灿谷如何从车企一跃成全球第二大比特币矿企?》 (Looking for Potential Crypto Stocks: How Did Cango Leap from an Auto Company to the World's Second Largest Bitcoin Miner?)

But mining is inherently a leveraged industry. Miner purchases, mining farm construction, and power contracts all require upfront capital expenditure, and mining companies often use self-held BTC as collateral to obtain equipment from miner manufacturers with delayed payment, or borrow USD/stablecoins from institutions/platforms to expand mining farms, purchase equipment, and maintain operations. The drawback of this model is that when the BTC price大幅回调 (significantly corrects), the collateral ratio deteriorates rapidly, leverage risk is amplified, and fixed costs like electricity, maintenance, and equipment depreciation do not decrease accordingly, putting extreme pressure on cash flow.

According to Q3 2025 data released in December 2025, Cango's average all-in mining cost (including depreciation) was approximately $99,000 per coin, and the cash cost excluding depreciation was about $81,000 per coin. The Bitcoin price is now far below its shutdown price, forcing it to reduce BTC holdings to "stop the bleeding," improve the balance sheet, and reduce financial leverage.

It is worth noting that Cango has announced it will shift部分资源 (some resources) to artificial intelligence computing infrastructure, seeking business diversification to reduce reliance on a single asset price.

Empery Digital Inc.(NASDAQ: EMPD): The Reverse Pressure of Bull Market Financing Logic

Empery Digital was founded in February 2020 (originally named Frog ePowersports Inc., later renamed Volcon Inc.), headquartered in Texas, USA. It was originally a company focused on all-electric off-road powersports vehicles.

In July 2025, the company announced a Bitcoin treasury strategy. Looking back, this timing恰是 (was exactly) near the high point of this Bitcoin price cycle. The company raised approximately $450-500 million through private placements and credit financing, and陆续增持 (progressively increased holdings of) about 4,000 bitcoins between July and August 2025, with an average cost of approximately $117,000 per coin. Calculated at the current price, the paper loss is close to 57%.

On February 6th, Empery Digital announced the sale of 357.7 BTC at an average price of about $68,000 per coin, obtaining about $24 million, to fund share repurchases and repay部分债务 (part of the debt). It has repurchased over 15.4 million shares so far, at an average price of $6.71, aiming to narrow the NAV discount. Empery now holds approximately 3,724 bitcoins remaining.

The case of Empery Digital actually reflects the typical dilemma of small and medium-sized DATs. They transformed aggressively, their financing relied on the bull market, but when prices corrected, they were forced to "sell coins for buybacks + deleverage." Compared to Cango's mining background, Empery is more like a "pure financial play." Its original main business was unsustainable, so it borrowed heavily to buy BTC at bull market highs, trying to replicate Strategy's path, but the significant correction in BTC exposed its leverage risk and it lacked the space for long-term issuance and capital market operations. If prices continue to fall,持续减持 (continuous reduction) becomes almost inevitable.

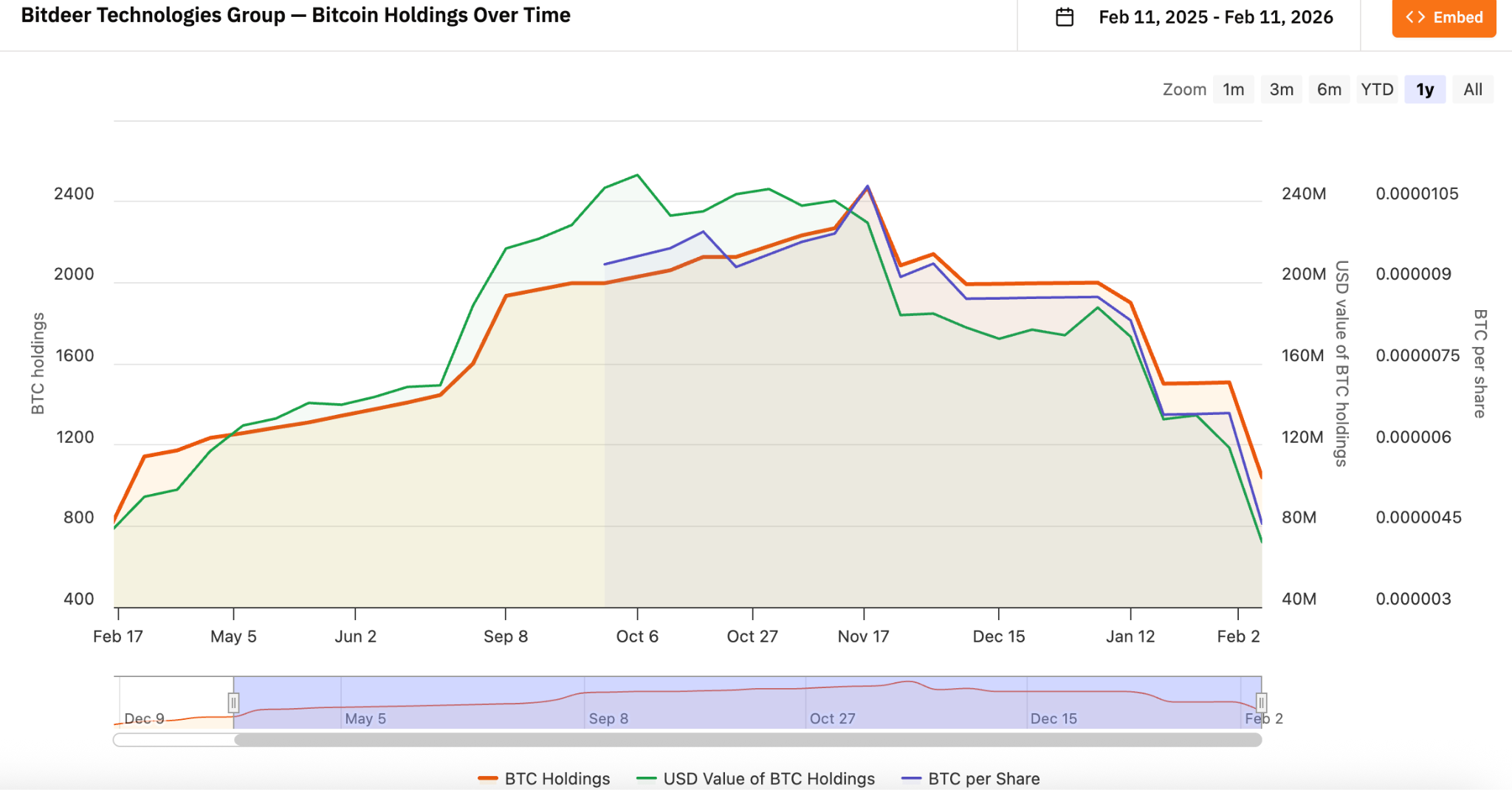

Bitdeer Technologies Group(NASDAQ: BTDR): From Price Betting to Cash Flow Priority

Bitdeer was founded in December 2021 by crypto OG Jihan Wu (co-founder of Bitmain), and is one of the world's major Bitcoin mining enterprises alongside MARA and Riot.

Bitdeer provides a full-chain solution through a vertical integration model, from equipment procurement, logistics, data center design/construction, equipment management to daily operations, while expanding into cloud hash rate, hosting services, and proprietary ASIC miner R&D. This has shifted Bitdeer's business from pure mining to diversified high-performance computing, buffering the impact of Bitcoin price fluctuations to some extent.

Data from bitcointreasuries.net shows that since November 2025, Bitdeer's BTC strategy has shifted to "mine and sell simultaneously", no longer holding fully (HODL), but maintaining cash flow and operational stability by partially realizing gains. Preserving cash flow takes priority over long-term holding. Is this the industry sensitivity of an OG who has experienced multiple bull and bear cycles?

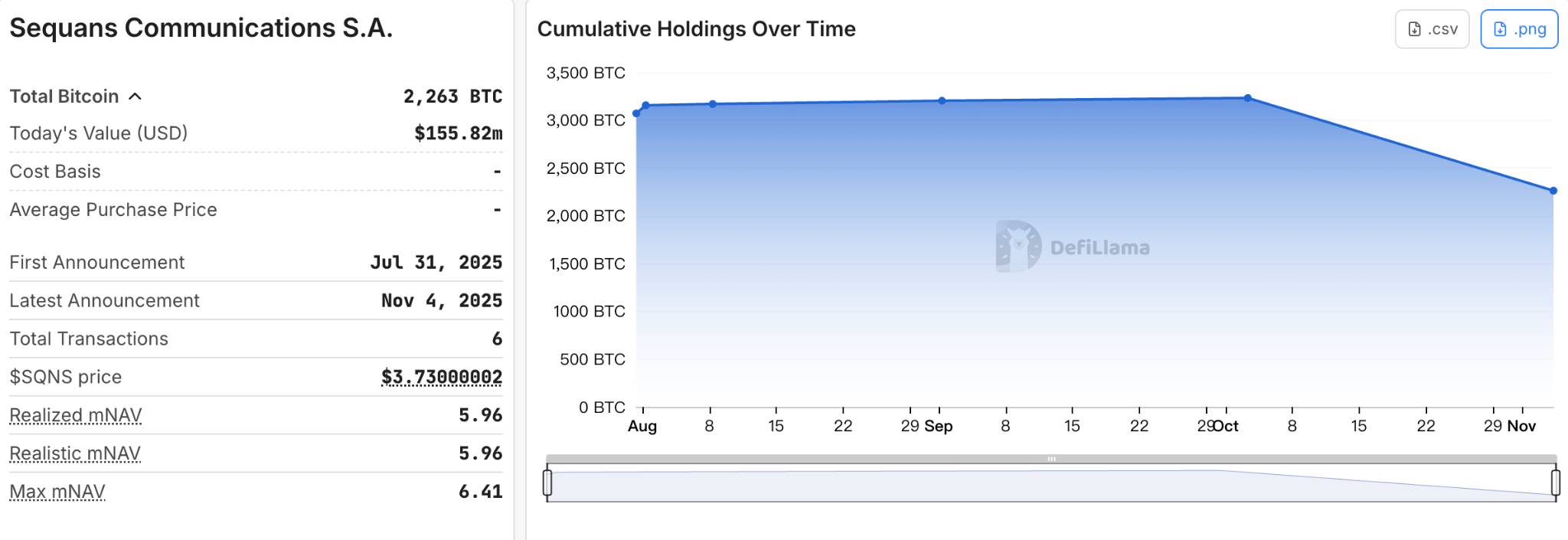

Sequans Communications S.A.(NYSE: SQNS): Selling Coins to Repay Debt Becomes an Industry Turning Point

Sequans was founded in October 2003 and was originally a semiconductor company focused on wireless cellular technology chips and modules. In June 2025, the company raised approximately $380 million through private equity and convertible bonds to accumulate Bitcoin, transforming itself from a pure IoT chipmaker into an "IoT + BTC DAT" hybrid.

Between July and October 2025, Sequans累计增持 (cumulatively increased holdings of) 3,233 bitcoins. Roughly estimated, the average cost was around $116,000.

In November 2025, it executed its first large-scale reduction of 970 BTC, used to redeem about 50% of its convertible bonds, reducing the company's total debt from $189 million to $94.5 million. The company called this a "strategic asset reallocation," not an abandonment of the strategy. But in the market's view, Sequans was the starting point of the "bubble burst" for BTC treasuries—the first DAT company to publicly admit the need to sell coins to repay debt.

ETHZilla Corporation(NASDAQ: ETHZ): A Deleveraging Sample of an ETH Treasury

ETHZilla Corporation was originally a clinical-stage biotech company focused on drug research and treatment development in areas like chronic pain, inflammation, and fibrosis. The company faced issues like cash shortages, poor liquidity, and slow R&D progress, with its stock price remaining low for a long time.

In August 2025, it raised $425-565 million through a private placement, with investors including加密机构 (crypto institutions) like Electric Capital, Polychain Capital, GSR, and Peter Thiel-related entities holding about 7.5%. These funds were directly used to purchase ETH and establish an Ethereum treasury. At its peak, ETHZilla had增持 (increased holdings to) about 102,000 ETH, worth approximately $210 million, with a per-coin entry cost of $3,841.

On November 13, 2025, ETHZilla began its first reduction of 8,293 ETH; on December 25, ETHZilla disclosed it had sold 24,291 ETH, generating proceeds of about $74.5 million. This transaction was part of redeeming outstanding senior secured convertible notes, making it the first sample of ETH treasury reduction. Currently, ETHZilla's ETH holdings are approximately 65,700 coins.

Similar to Empery, ETHZilla also embarked on the path of被迫卖币去杠杆 (forced coin selling for deleveraging). But the company is accelerating its转型 (transformation) towards RWA (Real World Asset tokenization), focusing on auto loans, home loans, land/commercial real estate, etc., with its first RWA token product expected to launch in early 2026, attempting to重塑价值 (reshape value) through business innovation.

Conclusion

The above are just a few representative samples, most of which are in the middle tier of the industry. They neither have the capital market pricing power of a company like Strategy, nor can they exit the stage悄无声息地 (silently) like the smallest companies. Beyond them, some smaller, structurally weaker DAT companies have already悄然消失 (quietly disappeared) in this round of correction;还有一些 (there are also) some companies that originally planned to transform but hadn't真正落地 (truly implemented) a treasury strategy, and have chosen to press the pause button after the financing environment suddenly tightened, even announcing termination before the project even started.

The 2026 correction acts like a mirror, reflecting the fragility and resilience of the DAT model. Those companies that relied purely on "storytelling + leverage" to rise are now paying the price for their aggressive expansion. Crypto faith may still exist, but it must ultimately coexist with the reality of cash flow, leverage management, and business sustainability.

The gap between top players and small and medium-sized companies is being持续拉大 (continuously widened) in this process. Rather than saying this is the end of the DAT model, it is more like the starting point of its stratification phase.