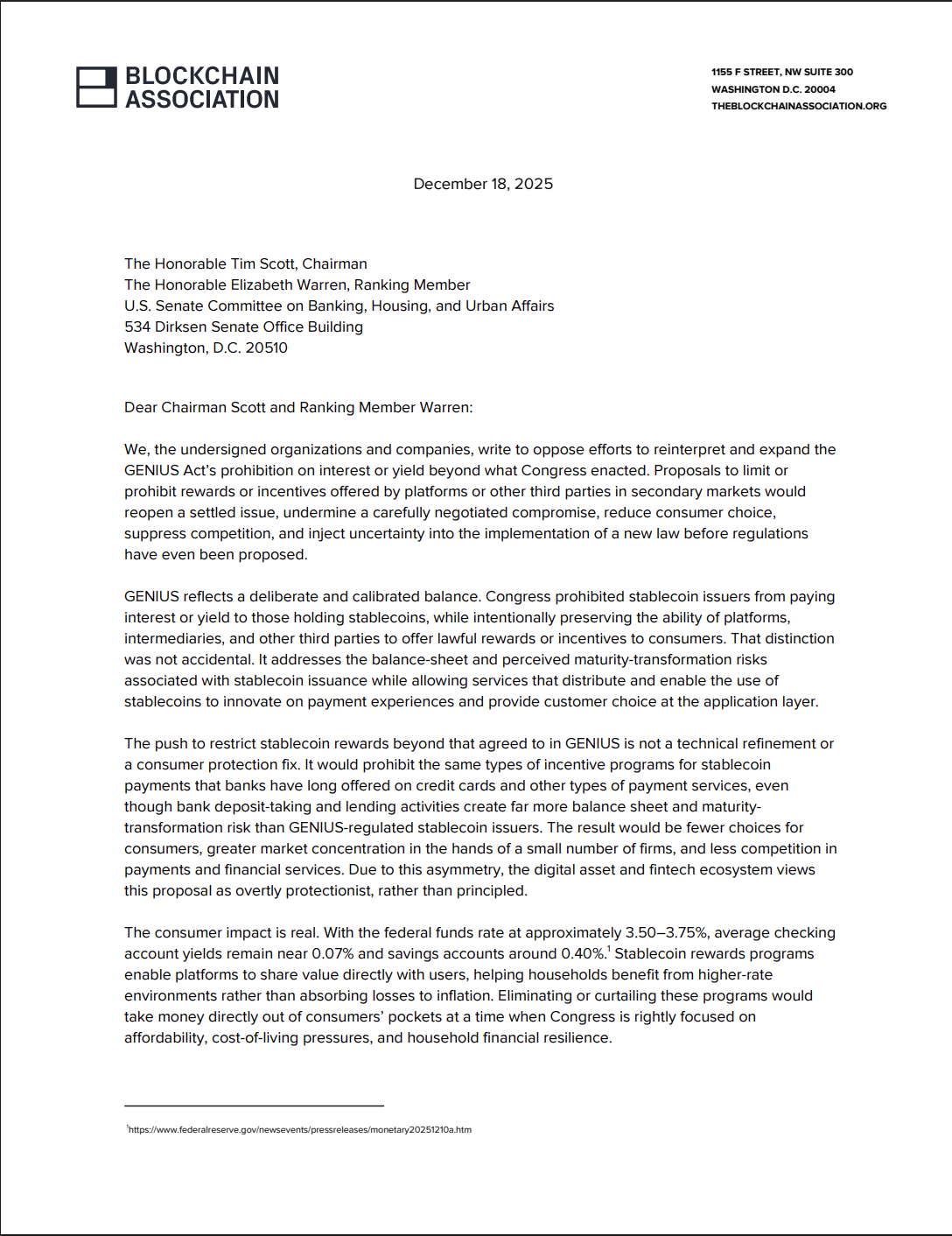

The Blockchain Association, a non-profit crypto advocacy organization, wrote a letter to the US Senate Committee on Banking, signed by over 125 crypto industry groups and companies, opposing the ban on third-party service providers and platforms offering customer rewards to stablecoin holders.

Expanding the prohibition on stablecoin issuers sharing yield directly with customers, outlined in the GENIUS stablecoin regulatory framework, to include third-party service providers stifles innovation and leads to “greater market concentration,” the letter said.

The letter compared the rewards offered by crypto platforms to those offered by credit card companies, banks and other traditional payment providers.

Prohibiting crypto platforms from offering similar rewards for stablecoins gives an unfair advantage to incumbent financial service providers, the Blockchain Association said.

“The potential benefits of payment stablecoins will not be realized if these types of payments cannot compete on a level playing field with other payment mechanisms. Rewards and incentives are a standard feature of competitive markets.”

The Blockchain Association has issued several statements and letters pushing back against efforts to prohibit crypto platforms from sharing yield-bearing opportunities with customers, arguing that these rewards help consumers offset inflation.

Related: Bank of Canada lays out criteria for ‘good money’ stablecoins

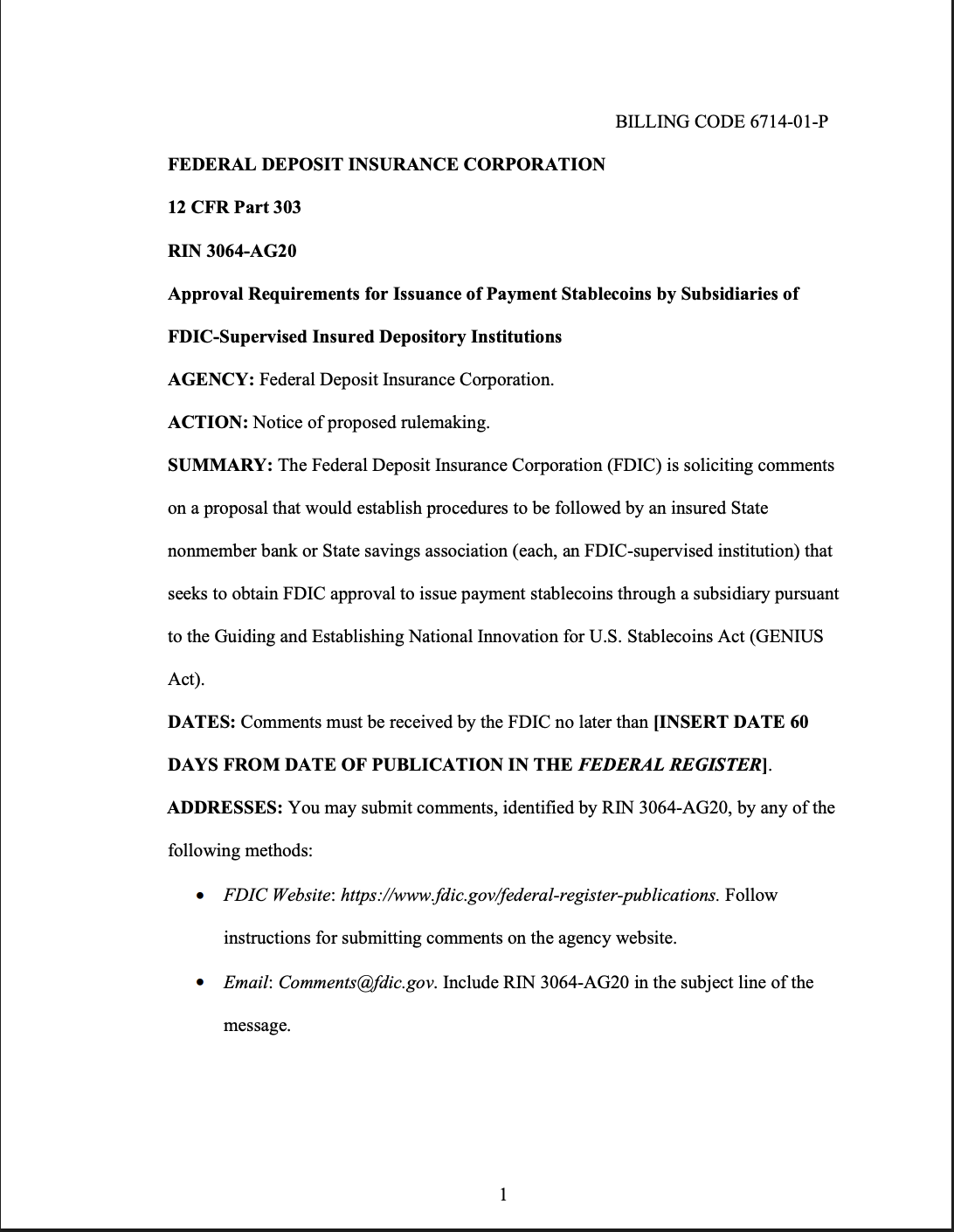

FDIC paves the way for banks to issue stablecoins, industry group says stables aren’t a threat

The Federal Deposit Insurance Corporation (FDIC), the US regulatory agency that oversees and insures the banking sector, published a proposal on Tuesday that would allow banks to issue stablecoins through subsidiaries.

Under the proposal, both the bank and its stablecoin subsidiary would be subject to FDIC rules and assessments for financial fitness, including reserve requirements.

The Blockchain Association continues to push back on claims that yield-bearing stablecoins and sharing rewards with customers threaten the banking sector and bank lending.

“Evidence does not support claims that stablecoin rewards threaten community banks or lending capacity,” the Blockchain Association said, adding that it is difficult to make the case that bank lending is actually constrained by customer deposits.

Despite this, the banking industry has lobbied against yield-bearing stablecoins and crypto platforms sharing yield with clients over fears that interest offered on digital asset products will erode the market share of banks.

Magazine: Unstablecoins: Depegging, bank runs and other risks loom