CryptoQuant’s head of research has highlighted how the recent high levels of Bitcoin HODLer selling were inflated by internal exchange moves.

Recent Bitcoin Long-Term Holder Selling Hasn’t Been At True Record Levels

In a new post on X, CryptoQuant head of research, Julio Moreno, has talked about the recent selloff from the Bitcoin long-term holders (LTHs). The LTHs refer to investors who have been holding onto their coins for a period longer than 155 days. Statistically, the longer an investor keeps their tokens dormant, the less likely they are to sell them at any point. As such, the LTHs with their long holding times are considered to include the resolute hands of the market that are unlikely to part with their coins.

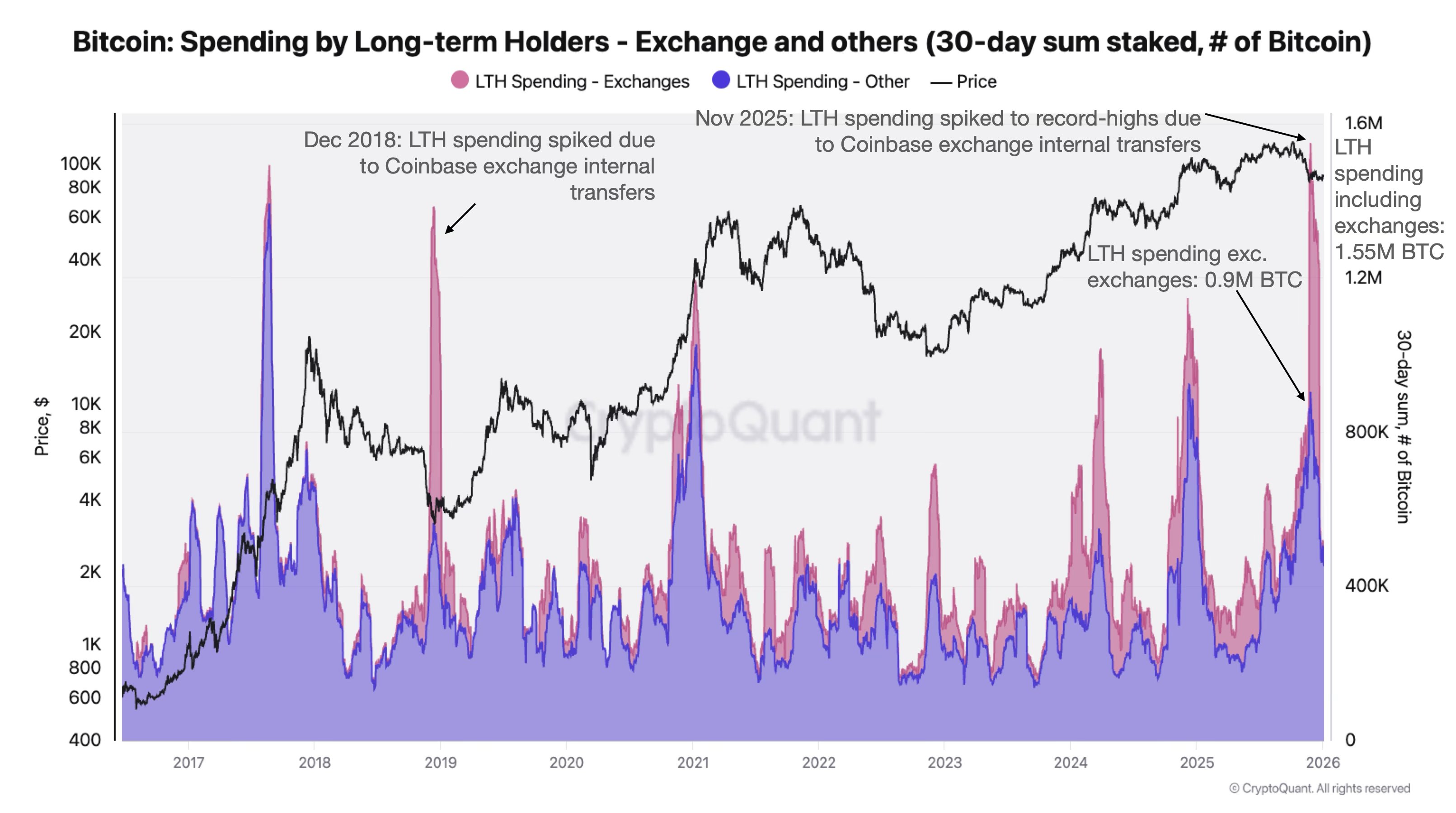

That said, there are times when these diamond hands do take to selling. One major such selloff occurred in November of this year, as the chart shared by Moreno shows.

The trend in the spending done by the BTC LTHs over the past decade | Source: @jjcmoreno on X

At the height of the Bitcoin LTH distribution in November, the 30-day sum of spending hit a record high of 1.55 million BTC. The analyst has pointed out, however, that this figure doesn’t tell the entire story.

The value of the LTH distribution doesn’t exclude sources that don’t correspond to economic transactions. For example, internal wallet moves. It turns out that such transfers skewed the market picture notably this time around. “A significant portion of LTH spending was due to exchange internal transactions,” explained Moreno.

According to CryptoQuant data, at least 0.65 million of the “HODLer selling” actually corresponded to internal wallet shuffling from cryptocurrency exchange Coinbase. Thus, the distribution from the group didn’t quite reach the levels that could be considered as new records.

This wasn’t the first time that internal exchange transactions exaggerated LTH selling. As is visible in the chart, there was a sharp spike in Coinbase’s internal transfers of LTH-aged coins back in December 2018 as well.

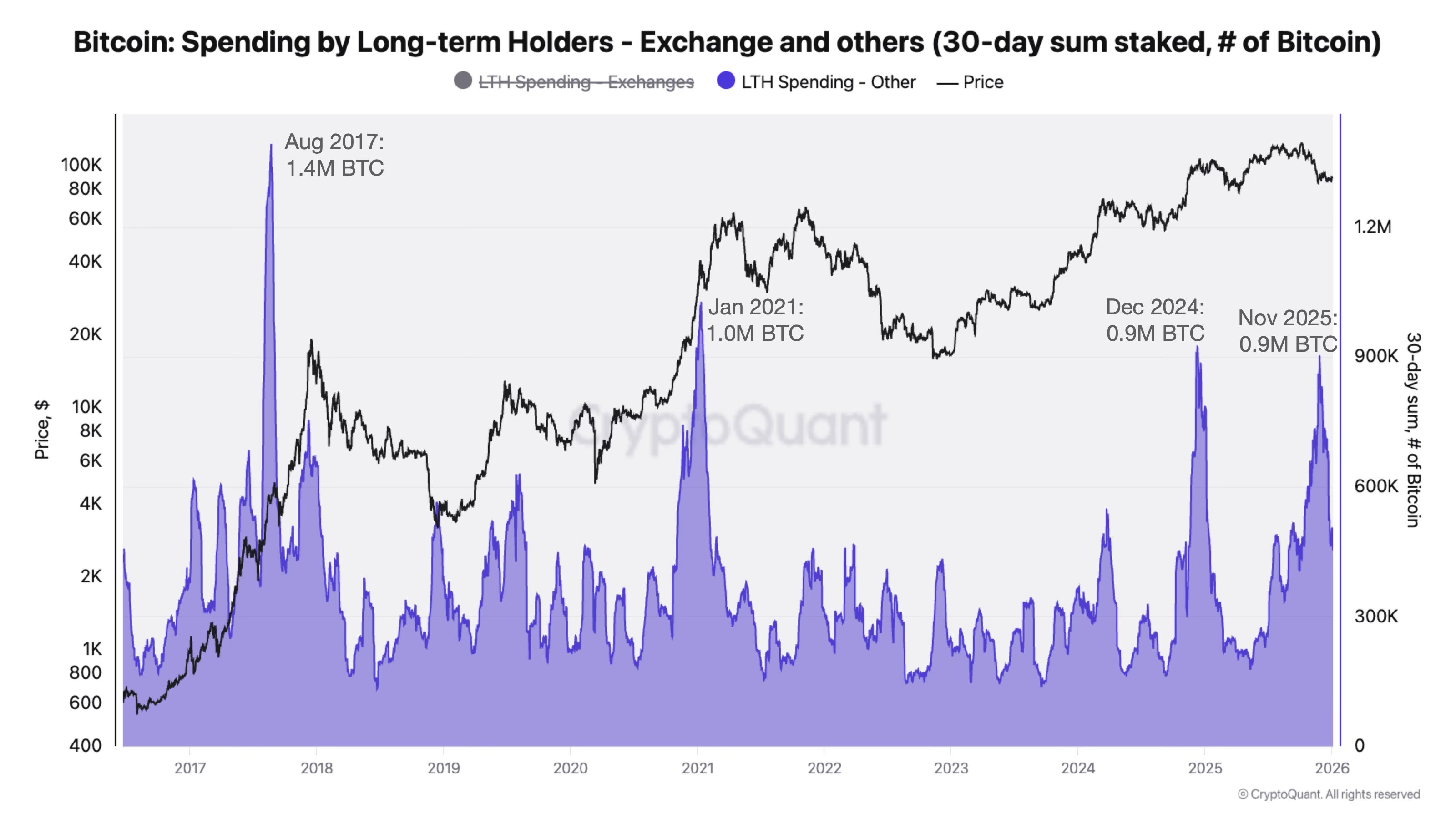

While adjusting for internal Coinbase shuffling lessens the scale of the latest diamond hand selloff, it doesn’t quite eliminate it. The monthly LTH spending still hit a notable level of 0.9 million BTC at the peak in November.

The only time in the current cycle that the metric exceeded this mark was in December 2024. In fact, as the chart below displays, this selloff was the fifth highest on record.

The LTH spending excluding exchanges | Source: @jjcmoreno on X

The record for the highest amount of Bitcoin LTH selling is still maintained by August 2017, which witnessed 1.4 million BTC in movements from the cohort.

BTC Price

At the time of writing, Bitcoin is floating around $93,800, up almost 7% in the last seven days.

Looks like the price of the coin has been climbing over the last few days | Source: BTCUSDT on TradingView