Author: Symbiotic

Compiled by: Hu Tao, ChainCatcher

-

All three methods allow holders to exit immediately, so their speeds are comparable. The real difference lies in the capital structure behind the exit.

-

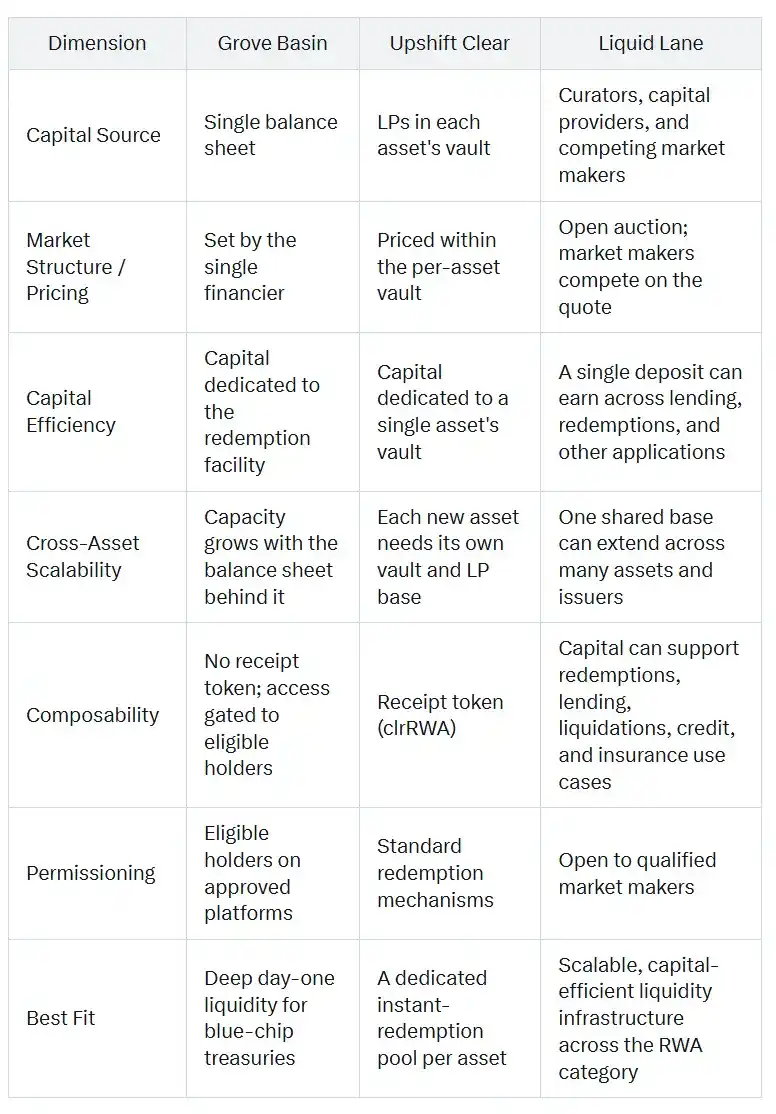

The key distinction is how each model handles redemption capital: Grove Basin uses a single balance sheet, Upshift Clear sets up a dedicated vault for each asset, while Symbiotic's Liquid Lane settles through a public market via a shared liquidity layer.

-

Grove Basin provides instant liquidity for tokenized vaults, with capital from Sky's balance sheet, launched in partnership with institutional collaborators. Upshift Clear extends this model to independent liquidity provider (LP) capital, with each supported asset having a dedicated vault.

-

Launched by Symbiotic, Liquid Lane is built on shared capital that can support multiple assets simultaneously, continues to earn yield from multiple sources between redemptions, and settles through an open RFQ marketplace where qualified market makers compete.

-

The result is higher capital efficiency per deposit, and the capacity of the liquidity layer grows with increased market participation, precisely where reliable exit mechanisms are hardest to provide and most valuable.

Exit is the Unresolved Half of the Tokenization Problem

Tokenization solves how assets get on-chain, but barely addresses how holders redeem them. A tokenized treasury or private credit fund can be issued, transferred, and distributed efficiently on-chain, while the underlying redemption process still takes approximately T+1 day for a treasury and 60 to 180 days for private credit, real estate, and structured products. The time gap between a token settling in one block and a fund settling in months is the crux of this long-standing issue.

This gap is crucial because DeFi markets need confidence that tokenized assets can be converted into liquid value when needed. With reliable liquidity infrastructure, RWAs can move beyond simple asset representation to become efficient financial primitives: they can serve as credit collateral, leverage backing, debt coverage, and assets underwriting risk in on-chain markets.

Emerging Instant Liquidity Architectures

Three models have emerged aiming to provide immediate exit pathways for tokenized real-world assets, but they differ in their sources and structuring of capital:

-

Balance Sheet Model. In this model, a well-capitalized single entity provides liquidity immediately from its own reserves when an eligible holder redeems for stablecoins, then waits in the background for the underlying settlement. Grove’s Basin is an example, funded from Sky’s balance sheet.

-

Dedicated Vault Model. Independent liquidity providers fund separate pools for each supported asset, earning the redemption spread. Upshift Clear, initially launched in partnership with Superstate, adopts this model.

-

Shared Liquidity Layer Model. Independent capital providers fund a common capital base that supports multiple assets simultaneously, settling through an open, competitive market. Symbiotic’s Liquid Lane is built on this model.

The question worth exploring is which architecture is best suited for liquidity that must scale across assets, issuers, and risk profiles while remaining capital efficient.

How to Evaluate a Liquidity Layer for Tokenized Assets

Exit speed itself is nearly uniform and tells little. The meaningful comparison is everything that happens in the five-dimensional space behind the exit.

-

Who supplies the capital and bears the risk? Where does the liquidity come from? Who bears the duration and credit risk of the underlying asset during the redemption settlement?

-

Redemption Pricing. The mechanism that determines the discount a holder pays for early redemption—whether it's a single provider's quote, fixed parameters of a dedicated pool, or bidding among multiple participants.

-

Capital Efficiency and Cost of Supply. How much committed capital a model requires to support redemptions and the opportunity cost of tying up that capital for settlement events. This cost ultimately reflects in the spread holders pay and whether liquidity providers can sustain the model.

-

How does the model scale to different asset types? What is required to extend coverage to new assets and issuers as the market grows?

-

Composability. Whether and how holders' claims and providers' funds can be used elsewhere in on-chain finance. This determines if liquidity is siloed in a single venue or can support other uses.

These five categories describe how robust and scalable a liquidity model is as the tokenization market grows in size and variety. The next sections apply them to each model in turn.

Balance Sheet Liquidity for Tokenized Treasuries and Credit

Grove Basin provides instant stablecoin liquidity for RWAs by prefunding when an eligible holder initiates an approved redemption via a supported tokenization platform. Grove Basin serves as a programmable credit facility against pending settlements.

Strengths of this design:

-

Immediate balance sheet depth. Since Basin is funded by an existing reserve base, it can provide considerable liquidity from day one.

-

Simple user experience. Basin operates through supported tokenization platforms, so eligible holders can exit faster while the traditional redemption process continues in the background.

-

An ideal solution for bonds and money market funds with short settlement cycles. These typically settle in T+1 to T+2, making the balance sheet bridge efficient for bridging the gap.

These trade-offs stem from the same design choices:

-

Capacity depends on a single balance sheet. The liquidity ceiling is ultimately tied to the size and risk appetite of the funding balance sheet. This means capacity growth relies on a single reserve base, not a broader capital market forming around the opportunity.

-

Access is restricted. Basin is only available to eligible holders, approved transactions, and supported platforms. This allows the model to control how liquidity scales but also limits how widely it can be accessed and reused across the broader market.

-

First application is for the most liquid part of the market. Tokenized T-bills and money market funds have inherently shorter settlement cycles.

Grove Basin is a powerful, vertically integrated solution to improve exit mechanisms for tokenized treasuries. Its main drawback is that liquidity depth, risk allocation, and economic benefits are tied to a single balance sheet model.

Upshift Clear: Asset-Specific Vaults for Instant Liquidity

Upshift Clear, initially launched with Superstate, applies the instant redemption model to independent USDC liquidity providers through dedicated vaults. LPs deposit USDC into a vault to back RWAs, receiving a composable receipt token clrRWA and earning fees from the redemption spread.

Strengths of this model:

-

Independent capital. Liquidity comes from LPs who opt in, so capacity can grow with the market, independent of any single institution's reserves.

-

General-purpose design. The platform aims to support any RWA with a standard redemption mechanism, providing issuers with a repeatable path to instant redemptions.

-

Clear, voluntarily assumed risk. Upshift Clear prices the settlement spread as a yield opportunity LPs knowingly take on, achieving a clear risk-reward match.

-

Composable receipts. The clrRWA token can circulate in DeFi, so LP positions aren't confined to the vault itself.

Where the model is more constrained:

-

Capital siloed by asset. Each supported asset has its own dedicated funding pool, so each new asset must attract its own liquidity. As coverage expands, the number of pools grows with the number of assets, potentially fragmenting market liquidity coordination.

-

Capital serves one asset at a time. Funds within a specific vault are committed to that specific asset, limiting what each dollar can do between redemption events.

-

The launch asset tests a more specific liquidity problem. Superstate's USCC is a ~$267M crypto arbitrage fund, advantaged by instant exit, but its liquidity challenges differ from longer-duration private credit or structured assets. It provides a solid starting point for the model, while raising a broader question: how well does the same design perform for less liquid, longer-duration assets?

Upshift Clear offers a flexible option for issuers looking to set up dedicated instant redemption pools for specific assets. Its main drawback is that liquidity, risk, and capital efficiency are allocated on an asset-by-asset basis.

Liquid Lane: Shared, Efficient, Cross-Asset Liquidity

Symbiotic Liquid Lane is a shared liquidity layer for tokenized assets. Redemption funding comes from Symbiotic vaults, which can support multiple tokenized assets simultaneously, rather than being tied to a single balance sheet or isolated in pools dedicated to a single asset. Between settlement events, these funds continue to earn yield from multiple sources and are ready when holders need to exit.

Vault managers decide how to deploy the capital. They choose which issuers and assets to support, set risk parameters, and develop vault strategies based on asset type, redemption patterns, and yield opportunities. This makes the liquidity layer configurable, not one-size-fits-all: different managers can build different strategies on the same shared infrastructure.

When a holder wants to redeem, qualified market makers bid on the redemption discount via a request-for-quote layer. Once a quote is accepted, vault funds settle the redemption atomically on-chain immediately, while the issuer's redemption process proceeds in the background.

The resulting model has four structural advantages:

-

Shared capital across multiple assets. A single vault can support redemptions for multiple RWA types. New assets tap into the same capital base, so liquidity capacity grows with market participation, not fragmented asset-by-asset.

-

Funds earn yield between redemptions. Collateral isn't idle waiting for redemption demand. It can earn underlying lending yields in whitelisted lending markets like Morpho and Aave, earn redemption spreads when settling redemptions, and back financial obligations in other Symbiotic applications (e.g., credit and insurance). Thus, a single deposit generates yield from multiple sources, maximizing capital efficiency and DeFi composability.

-

Configurable risk and yield strategies. Managers can tailor vault strategies by choosing supported assets, issuers, limits, and risk parameters. This means liquidity can be deployed according to different risk appetites and market views, rather than forcing all assets into the same pool design.

-

Open, competitive settlement. Liquid Lane uses a competitive request-for-quote (RFQ) marketplace where qualified market makers bid to settle exit trades. The redemption discount is set by market competition, and the yield is split among makers, capital providers, and managers.

This design aims to serve the part of the market where providing reliable exit is hardest and thus most valuable: tokenized private credit, structured assets, and other products with lengthy redemption windows. These can have windows of 60 to 180 days, and reliable exit infrastructure would transform how assets are held, financed, and used on-chain.

Initial integrations for Liquid Lane include Fasanara (first vault manager) and Midas (first issuer via mGLOBAL and mF-ONE), alongside additional vault managers such as Avantgarde Finance, Barter, and Kpk.

Side-by-Side Comparison

Conclusion: From Liquidity Patches to Shared Infrastructure

Tokenized assets need reliable exit mechanisms to achieve broad adoption. The question is whether these exits are built as one-off solutions or as infrastructure that can scale with the market.

If each asset requires its own liquidity pool, each issuer its own financing channel, or each exit relies on a separate reserve, the market gets faster exits but not truly scalable liquidity. A sustainable liquidity model is different: it is shared, efficient, and flexible—growing with market participation without fragmenting capital each time coverage expands.

That is what Symbiotic Liquid Lane aims to be. It turns redemption liquidity from a single-purpose mechanism into a shared layer for the tokenized market: a single capital base that can support multiple assets, multiple obligations, and multiple yield sources.

For issuers, this means increased demand, distribution, and assets under management (AUM), as tokenized assets become easier to hold and use as collateral. For market makers, it means participating in RWA settlement without needing to hold idle inventory upfront. For capital providers, it means a single deposit earning across lending, redemption, and Symbiotic applications.

Liquid Lane is the shared liquidity infrastructure for RWAs: cross-asset, capital-efficient, T+0.