Written by: Thejaswini M A

Compiled by: Saoirse, Foresight News

I never fully bought into it. Not because I'm smarter than anyone else, but because those who shout the loudest about decentralization are often the ones most eager to funnel your money into their ecosystems. In any history, this combination has never been a good sign.

But I kept watching. You had to, because it's the most fascinating show right now. An entire industry built on the radical idea of "trustless money," yet filled with people who are almost entirely untrustworthy. The irony is everywhere.

Now, as all obvious things eventually become widely known, a conclusion is slowly being reached—one that some of us have long understood: Decentralization has always been more of a performance than a genuine belief. The goal was to harvest "dumb money." Those who used to chant "banks are the enemy" are shaking hands with the most centralized political forces on the planet, simply because it benefits their investment portfolios.

I'm not even angry. I'm just observing, because the show is too good to miss.

October 31, 2008. The aftermath of the financial crisis. Satoshi Nakamoto released a nine-page whitepaper. He proposed an electronic currency that required no banks, no governments, no permission from anyone. Two parties transact directly, no intermediaries taking cuts, no central authority deciding if you're qualified to trade.

To be fair, the original idea was compelling. It was born directly from a world where hedge funds and central banks over-leveraged the economy, profited from ordinary people's losses, and were bailed out by government rescues when things went wrong. The anger behind it was entirely justified. If a system that lets elites reap huge profits while the public foots the bill doesn't make you angry, what will?

The brilliance of Satoshi's design was that it removed the human element. No single point of control, no single point of failure. Instead, there were thousands of nodes, equal to each other, verifying each other. You can't bribe an entire network, you can't threaten it with a phone call. Nor can a regulator freeze someone's wallet on a whim.

The ownerless design was a beautiful concept.

People like to attribute the industry's corruption to venture capital influx, NFT chaos, or the FTX collapse. But these are just symptoms. The real problem emerged much earlier—almost from the beginning, if you were paying close attention.

The problem with decentralization is this: it's expensive, slow, and requires coordination among thousands of participants with no inherent motive to agree. Centralization is efficient, fast, and profitable. So, when real money entered the scene, economic laws began to work as they always do. The industry started to bifurcate, though few were willing to say it out loud.

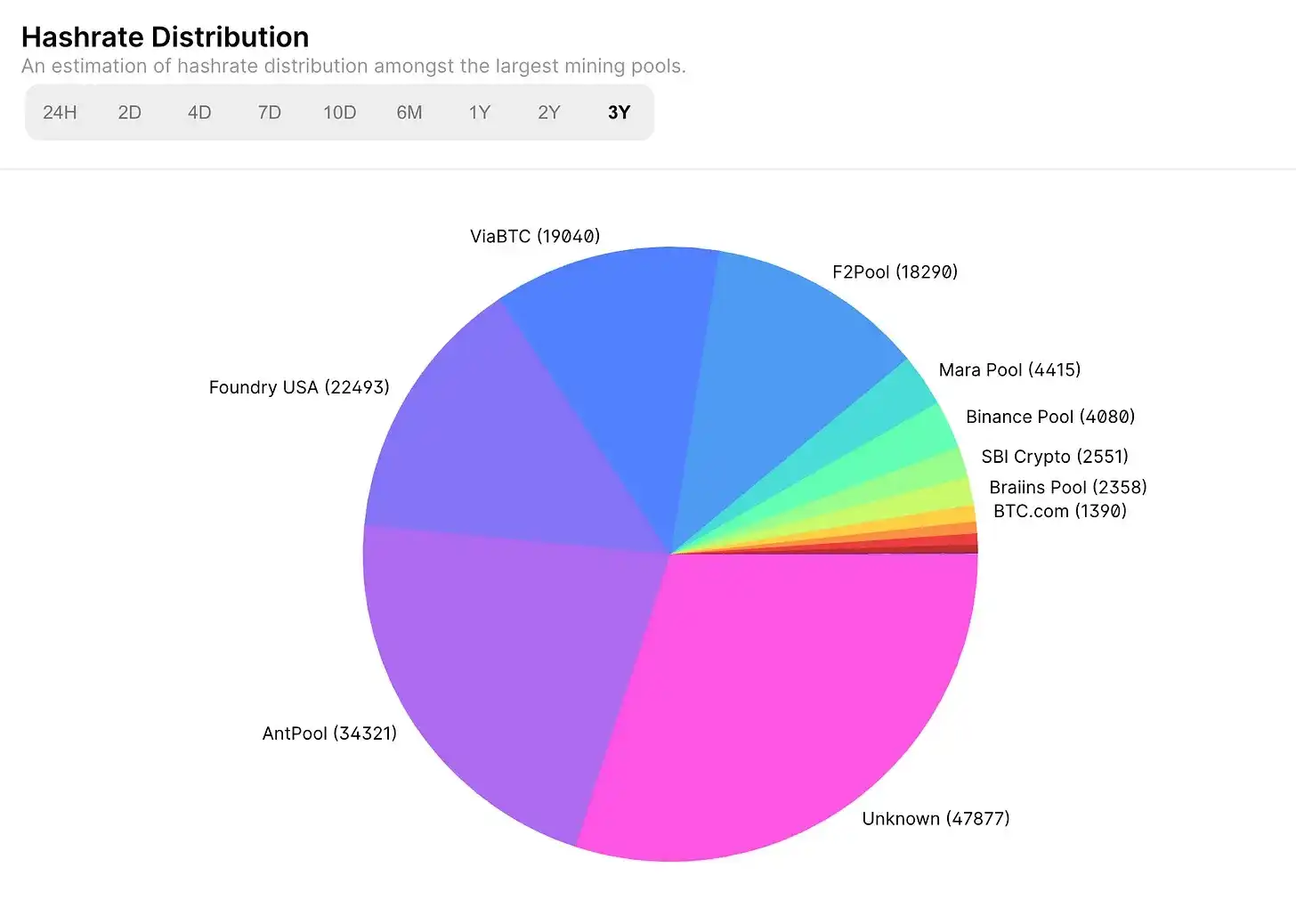

In May 2017, the top two Bitcoin mining pools accounted for less than 30% of the total hashrate, and the top six for less than 65%. It was the most decentralized moment in Bitcoin's mining history. Nine years on, that peak is long gone. By December 2023, the top two pools controlled over 55% of the hashrate, and the top six a staggering 90%.

Today, Foundry USA controls about 30% of the network's hashrate, Antpool about 18%, together approaching 50%. And by March 2026, the abstract risk became reality: Foundry mined six blocks in a row, triggering a rare two-block reorganization, overwriting legitimate blocks from Antpool and ViaBTC. Small miners watched helplessly as their valid work was erased from the ledger. Bitcoin has never suffered a 51% attack, and the network's integrity remains, but the centralization risk the whitepaper aimed to prevent is no longer theoretical—it's numbers on a chart trending dangerously.

The whitepaper described a system where no single entity could do this. This year, it turns eighteen. Draw your own conclusions.

I want to be precise here, because lazy critiques easily miss the mark. Trust me, I've tried.

Look at all the crypto products today with real users, real trading volume, real revenue: the vast majority are not decentralized.

But did they ever claim to be? Confusing this makes your critique sound sharp but aimed at the wrong target.

Stablecoins are the crypto industry's only undisputed success story. Used for trading, cross-border remittances, as payment tools in countries with constantly depreciating currencies. As of 2025, USDT and USDC together account for 93% of the stablecoin market cap, handling unprecedented trillions in transaction volume.

@visaonchainanalytics

USDC and USDT are both issued by companies, and both can freeze wallets. Not to mention, their reserves are held in banks—the very institutions this industry was supposed to replace. The decentralized stablecoin DAI, often cited as proof the ideal lives on, holds only a 3-4% market share. No one ever sold you USDT as a decentralized product; its selling point has always been efficiency.

Move dollars across borders in minutes, settle in seconds, no correspondent banks, no SWIFT codes, no three-day clearing periods. They kept the issuer but removed all the inefficient, expensive middlemen between the issuer and the user. The "revolution" that traditional finance truly lost was to a centrally issued dollar reissued on a blockchain by a company. And that was its promise, and it delivered.

Hyperliquid, with billions in trading volume, incredibly fast, the product itself is impressive. But in any practical sense, it is controlled by 16 validators. During the JELLY incident in March 2025, these 16 validators reached consensus, delisted a token within two minutes, turning a potential $12 million protocol loss into a profit. Two minutes. Getting Ethereum governance to decide anything in two minutes would probably require a natural disaster, and even then, someone in a forgotten timezone would blog a dissenting opinion.

Some called it FTX 2.0, a mischaracterization. Hyperliquid made a corporate decision. What it truly earned credit for was: fixing the problem, compensating users, introducing on-chain validator voting for future delistings, and moving on. The issue was, for a time, Hyperliquid's marketing spent significant effort insisting it wasn't a company, while operating exactly like one.

Prediction markets. Polymarket had crypto's first true mainstream breakout moment during the 2024 US election. Journalists quoted its prices, people who never held ETH used it. No one asked if it was decentralized enough, they only cared if it was accurate. And it was. Occasional articles discussed insider trading and its "truth machine" positioning, some from me. It was just a useful product, using crypto as plumbing, not an ideological banner.

I could write a whole section on DAOs, but "Decentralized Autonomous Organization" might be the most comical three-word combination in the language. I'll stop here.

These are the things that actually work, and most are far more usable than the schemes described in whitepapers.

The crypto world today is divided into two types.

One is the infrastructure layer Built for efficiency, scale, and real usage, trading decentralization for performance, and mostly being upfront about it.

The other is the protocol layer: Bitcoin, Ethereum, Solana, which remain structurally distinct from all previous systems, where decentralization is not a marketing slogan but a design attribute preserved under immense adversarial pressure. Products compromise for user demands, and users just want things that work. Under the competitive pressure of real money, the industry inevitably centralizes. This is just规律, not a moral failure. The revolutionary rhetoric of the protocol layer is constantly borrowed by the product layer, even though the two are no longer the same thing.

Founders who quoted the Cypherpunk Manifesto in their 2019 keynotes were sitting in Senate hearings by 2023, claiming they always wanted constructive cooperation with regulators. For a large part of the industry, decentralization was just a regulatory strategy disguised as ideology: if no one is in charge, no one can be held accountable. This ideology was sufficiently confusing for lawyers and regulators, buying time to raise funds, launch products, and in many notable cases, exit. When regulation became inevitable, this ideology was shelved to avoid trouble.

There are still true believers in the industry. They entered crypto because they witnessed governments destroying currencies, freezing accounts for political reasons, excluding entire groups from basic financial services. They became the moral fig leaf for an industry inherently driven by profit. Profit-seeking is fine, but no need for pretense.

In my view, this trade-off might be worth it, and those making the choice know it, even if they won't admit it so bluntly. The pure form of decentralization was struggling against reality from the start. No one conspired to kill decentralization. The fact is, when people choose between a "useful product" and a "principle that doesn't work," they choose the former every time. Silently, without announcement, without a eulogy.

What I find truly darkly humorous is how this story plays out politically.

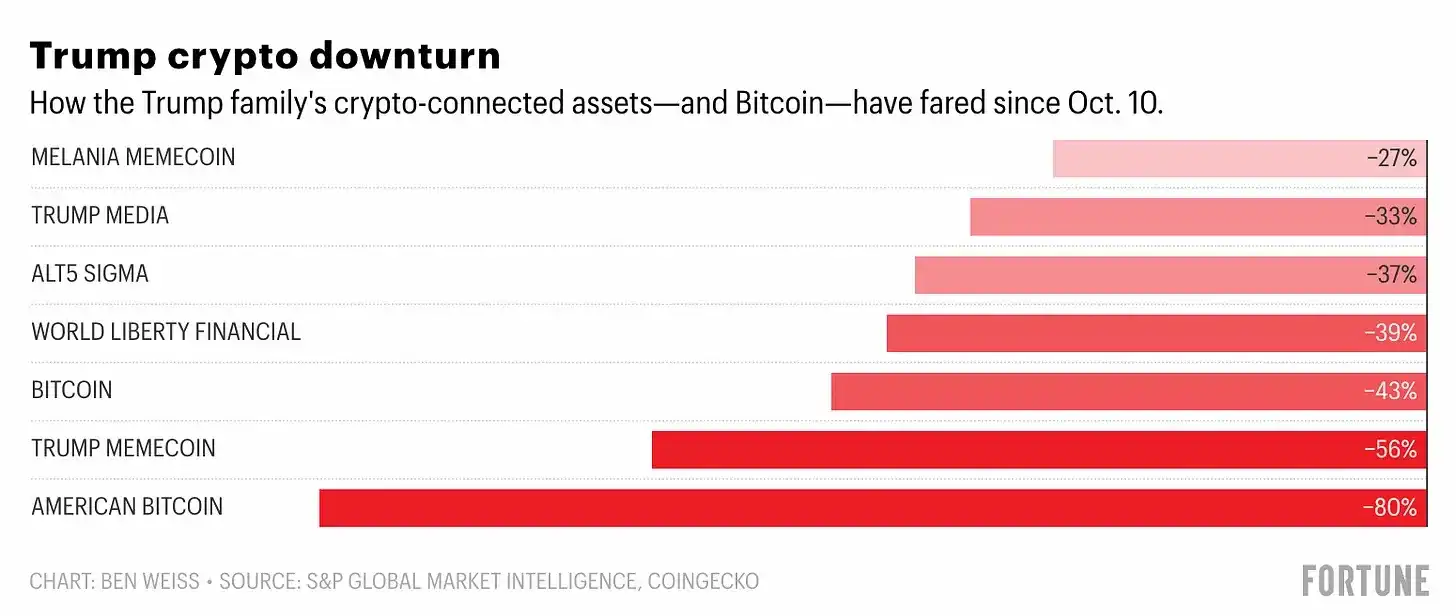

Before signing any crypto-related legislation or appointing any pro-crypto regulators, Trump Organization's revenue surged 17-fold in the first half of 2025, reaching $864 million, with over 90% coming from crypto-related projects. According to Wall Street Journal analysis, by early 2026, the Trump family cashed out at least $1.2 billion from World Liberty Financial alone. His 19-year-old son Barron was listed on the project's website as a "DeFi Visionary." Honestly, a moment of silence for whoever wrote that copy.

@fortune.com

This is the man who called Bitcoin a scam in 2021 but was on stage at a Bitcoin conference by 2024. The crowd that for years argued "the government has no right to control your money" watched a sitting president directly profit from the industry he regulates, and the mainstream reaction was predicting coin prices and cheering "bull market."

Economics has a concept called revealed preference: what you actually do reveals more about your beliefs than what you claim. The revealed preference of the decentralization movement under real political pressure is: We care about decentralization until it costs us; after that, we only care about the price.

I don't want to judge too much. I'm just recording it, because someone should.

The "we're going to change the world" fervor of 2017 and 2021 has largely dissipated. The NFT crowd moved on, in the metaverse people found other topics to confidently be wrong about. Those who remain are quieter, less messianic, and much more honest about what they're actually doing. The protocol layer operates as designed, the application layer has built amazing products. This revolution still gave birth to practical financial infrastructure, changed how value moves globally, and made a large number of people extremely wealthy.

All I'm saying is this: be honest about what you're doing.

If you're building a centralized exchange with a better experience using crypto rails, say it. If your stablecoin is company-issued, can freeze wallets, and reserves are in banks, say it. If your DAO is effectively controlled by three wallets and everyone in the room knows it, you might as well say it too. Users can handle honesty. What they can't handle long-term is the gap between narrative and reality. And eventually, they vote with their feet.

Satoshi has been silent for fifteen years. Perhaps he foresaw all this, choosing to watch the spectacle quietly from the shadows. Or perhaps, he just knew when to leave the stage.