Author:fiona.stand

The day the Dow hit 50,000, NVIDIA's market cap soared past $5.7 trillion, and the Nasdaq reached a new high. Wall Street seemed to have rediscovered the printing press. At the same time, BTC failed for the fourth time to break through 82,000, falling below 80,000.

U.S. stocks are celebrating, while the crypto market is bottoming out.

Over the past few years, crypto users have been conditioned by two things: one is 30% APY, but upon clicking, you find it's all governance token emissions, and the token price drops 90% before the rewards even arrive; the other is 3% stablecoin yield, safe but like a lukewarm cup of water handed over at a bank counter—not bad, but not exciting either.

By 2026, yields for mainstream stablecoins were mostly compressed into the narrow range of 3-4%. Coinbase 3.35%, Aave 3.31%, Ethena 3.60%—everyone is queuing under the same interest rate ceiling.

So, when I first saw DUSD showing around 8.46% APY, and with rewards settled in DUSD and not reliant on token subsidies, my reaction was likely the same as yours—is this number real?

After joining StandX, I decided to verify in the simplest and most honest way possible: test it with my own money. $10,000, two accounts, one set of BTC long/short hedging positions—no directional bets, no chasing trends, just to see if DUSD could really generate money on its own.

8 days later, the answer is here.

Test Result: $10,000 Principal, 8 Days, $17 Profit with Zero Directional Risk

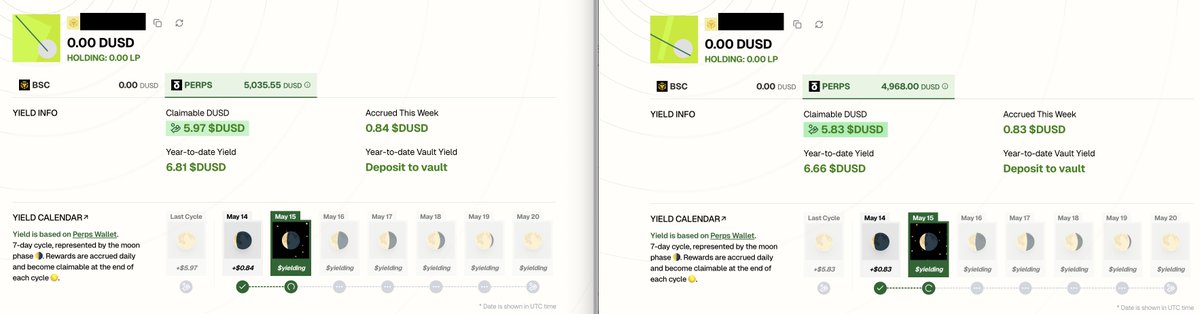

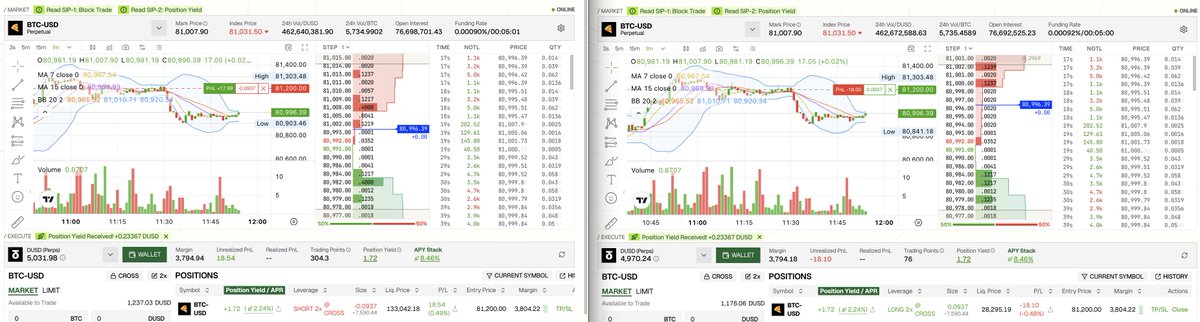

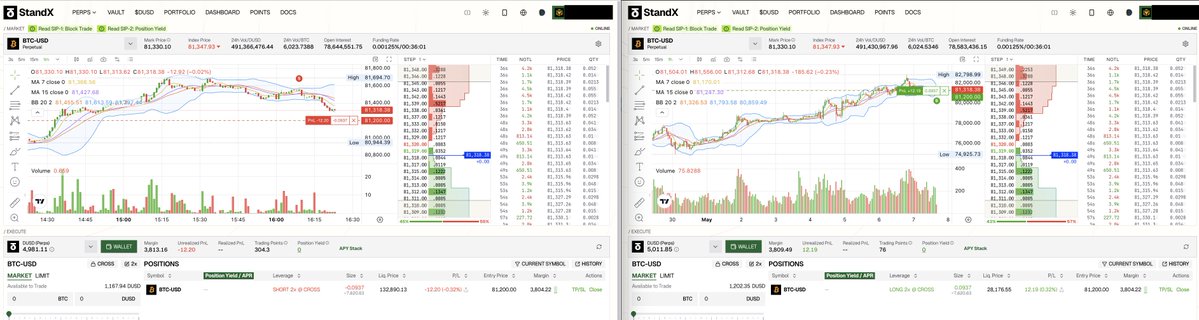

Last week, I created two accounts on StandX, each depositing 5,000 DUSD. I used the unique Block Trade feature to hedge them against each other (one long, one short). The net directional risk is zero—BTC price movements are irrelevant to me.

Current Account Summary (Two accounts combined):

-

💰 DUSD Yield Earnings (Base + SIP-3):$13.47($6.81 + $6.66)

-

💰 Position Yield Earnings (SIP-2):$3.44($1.72 \times 2)

-

📊 Total Earnings:$16.91, annualized approximately 7.8%

-

🎯 Trading Points: 380+ points

-

⚡ Directional Risk: Zero

-

🔥 Wear and Tear: Zero

APY Stack is currently showing 8.46%, and earnings are still growing daily.

📌 Note: The total earnings of $16.91 translate to an annualized rate of about 7.8%, which differs from the APY Stack showing 8.46%. This is because 7.8% is the historical average for the 8-day period from May 7th to May 15th, whereas 8.46% is today's real-time snapshot—recent increases in platform trading volume have driven up fee income, so the current APY is higher than the average of the past 8 days. Over a longer timeframe, the two figures will converge.

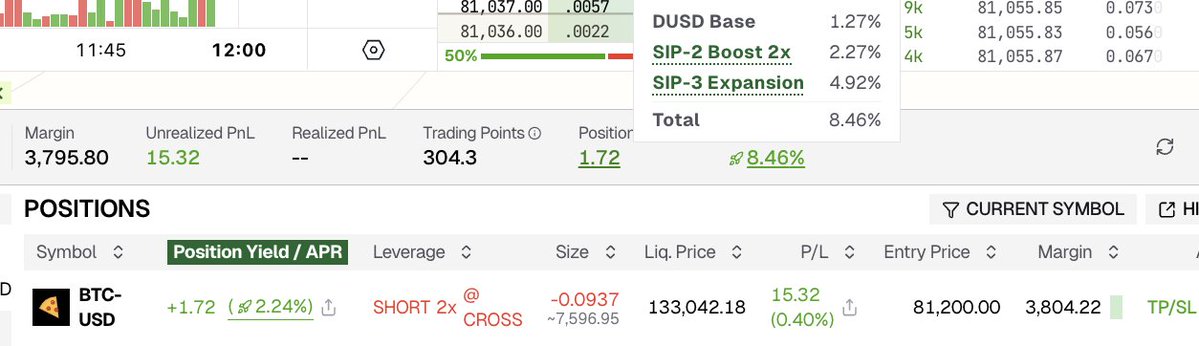

Earnings Breakdown — Where Does the 8.46% APY Come From?

-

First Layer: DUSD Base — 1.27%

The base yield that all DUSD holders receive, sourced from Funding Rate (similar to Ethena's USDe strategy).

-

Second Layer: SIP-2 Position Yield Boost — 2.27%

This is a mechanism unique to StandX. Many people's first reaction is, "Isn't this just a subsidy?"—it's not. Behind SIP-2 lies a carefully designed flywheel logic:

You Open a Position → Platform Liquidity Increases → Trading Volume Increases → Fee Income Increases → SIP-2 Earnings Increase → Attracts More Users to Open PositionsWhy does this flywheel work? Opening a position—whether long or short—provides the foundational liquidity for the platform. The essence of SIP-2 is protocol revenue sharing ( Protocol Revenue Sharing ): the platform shares real transaction fees back with users who provide liquidity, following the same logical framework as Hyperliquid's fee distribution.

💡 Leverage = Earnings Amplifier: 2x leverage corresponds to 2x boost—you use 1,000 DUSD to open a 2x position, taking on a 2,000 DUSD risk exposure, and earnings are calculated based on risk exposure, not principal. Higher risk, higher reward. Logically fair—bigger waves bring bigger fish.

-

Third Layer: SIP-3 Universal Fee Distribution — 4.92%

This is currently the largest source of earnings and also the most generous layer. A portion of the transaction fees generated by StandX is distributed directly to every DUSD holder—regardless of whether you have open positions, trade, or even log into the platform. As long as you have DUSD in your wallet, you automatically get a share. A true universal sunshine bonus.

Key Point: All three layers of earnings are settled in DUSD (a USD stablecoin). Every cent you earn is real, hard U, with no inflated governance token incentives.

In a World of 3% Yields, How Can 8% Be Sustainable?

Just compare horizontally. After the Federal Reserve cut rates three times in a row by the end of 2025, the federal funds rate settled at 3.50–3.75%, pushing down the ceiling for "safe returns" across the market. From Aave's 3.31% to Ethena's 3.60%, all mainstream stablecoin yield products are squeezed into an extremely narrow range. DUSD's 8.46% is more than double that.

Moreover, this yield is sustainable, not cyclical. Most yield-bearing stablecoins (including Ethena sUSDe) heavily rely on funding rates—look good in bull markets, but get compressed in bear markets. DUSD is different: over 7% of its 8.46% comes from transaction fees ( SIP-2 + SIP-3 ), which is independent of market direction. As long as people trade, there is fee income, and there is yield. The introduction of SIP-3 is a structural upgrade that transcends bull and bear cycles—it transforms DUSD from "relying solely on funding rates" to being "driven by a dual-engine of fees + funding rates." This is unique among all yield-bearing stablecoins.

Replicate My Strategy in 3 Steps with Zero Wear and Tear

The whole process takes less than five minutes. You need two wallets, 5,000 USDT each, and a small amount of BNB for Gas.

-

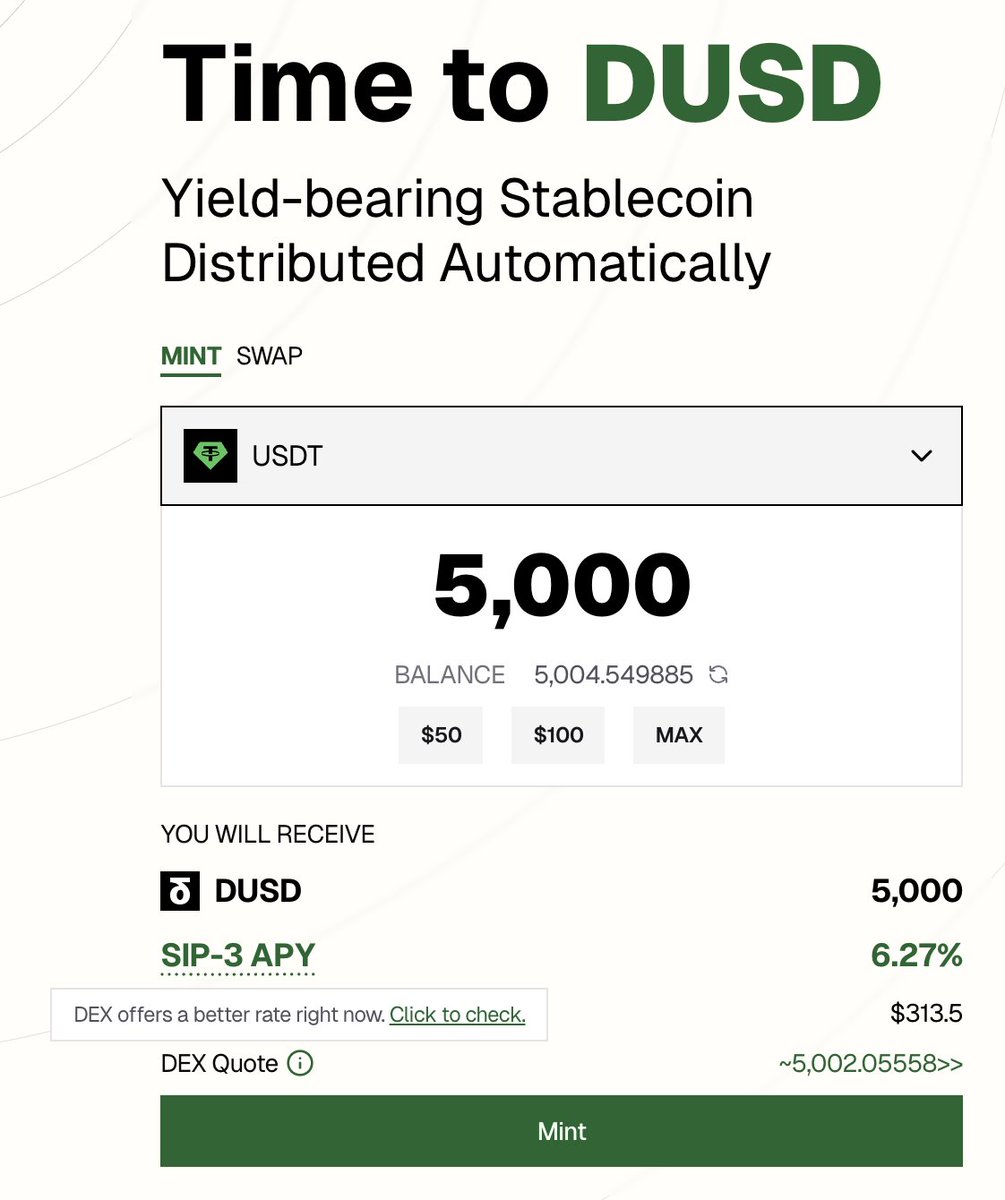

Obtain DUSD and Deposit into Perps Wallet

Log in to both wallets at

standx.com$DUSD page Select Swap (gets you a few extra dollars compared to Mint) Swap 5,000 USDT for approximately 5,002 DUSD. Note the prompt at the bottom of the page; our system helpfully informs you when the DEX quote is more favorable.

-

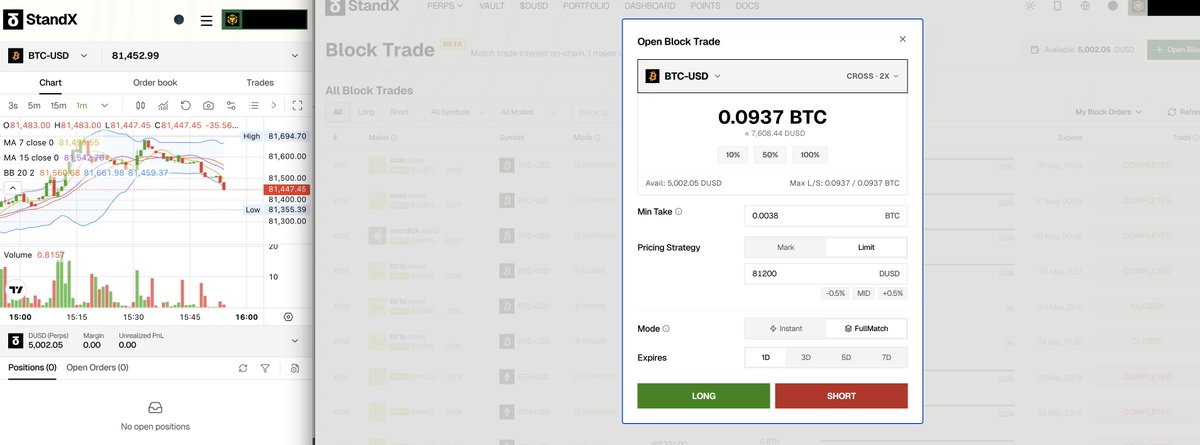

Account A Creates a Block Trade Long Position

PERPS Block Trade + Open Block Select BTC-USD, CROSS · 2X, Limit Price, FullMatch Click LONG PUBLISH ONCHAIN. After publishing, copy the share link and send it to the other wallet.

-

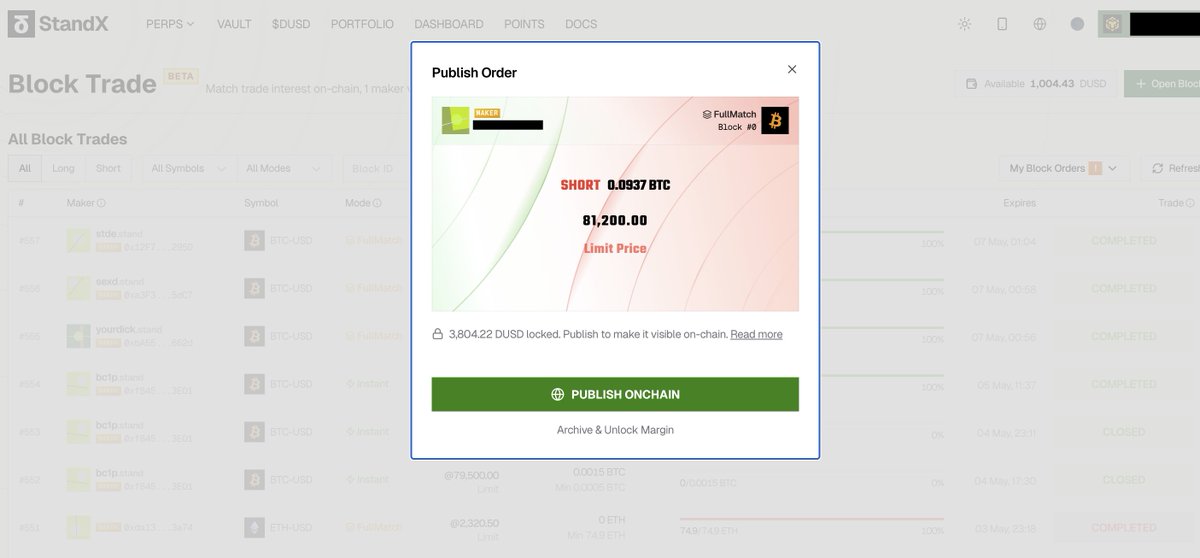

Account B Accepts the Block Trade Short Position

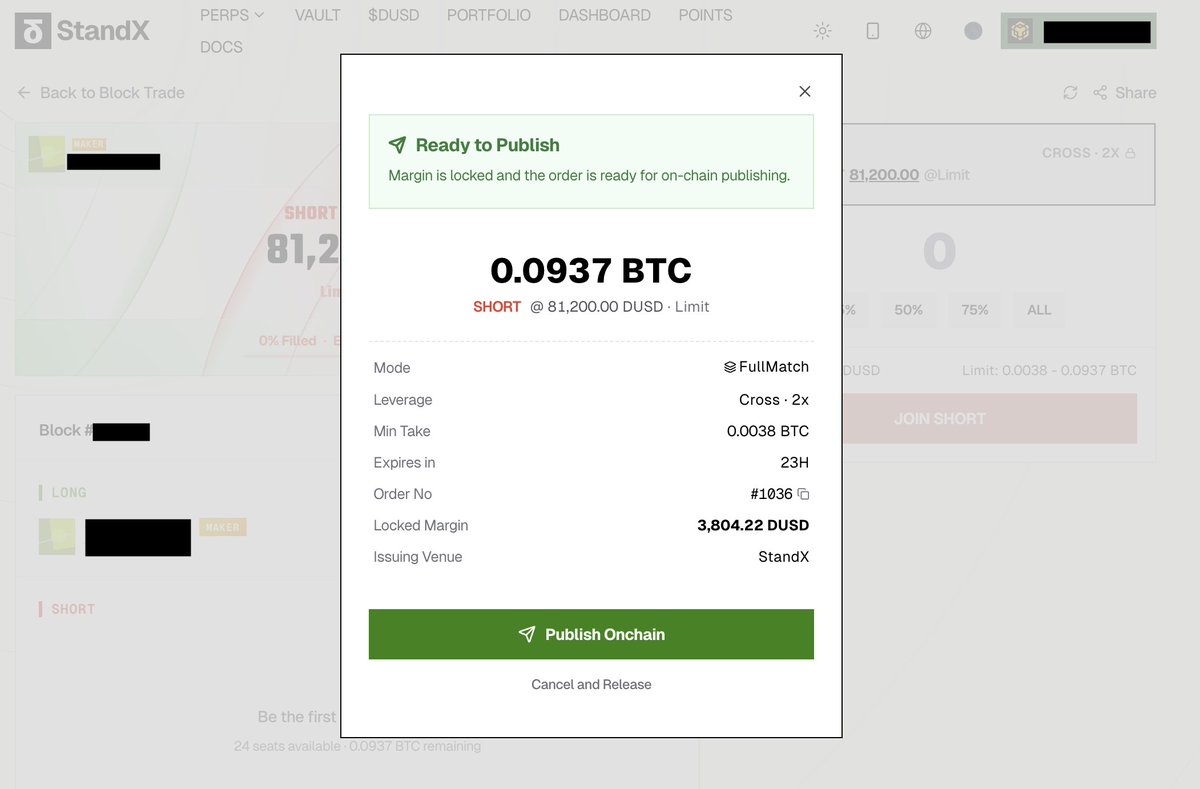

Switch to Wallet B Go to Block Trade Change the leverage to CROSS · 2X (default might be 10X) Click JOIN SHORT Confirm Publish Onchain.

Done! The two accounts are perfectly hedged. On the left -$12.20, on the right +$12.19, net PnL is nearly $0.

Why is this strategy "zero wear and tear"?

Airdrop farming used to be like factory work. You repeatedly open and close positions, trade volume, check in, transfer funds, twisting your wallet addresses into the machines designed by project teams like an assembly line worker. Finally, the airdrop arrives, and the project says: Thanks for participating, but this batch of addresses has low weighting. Worse, you didn't work for free—spreads, slippage, fees, Gas, all slowly wear down your principal. Block Trade is completely different—not only does it accumulate points with zero loss, but your principal also steadily generates earnings.

Risk Disclosure

-

Smart Contract Risk: This is the underlying risk of all DeFi. StandX contracts are audited, but no protocol can guarantee 100% security.

-

Yield Volatility: 8.46% is not a fixed yield. The Base layer fluctuates with funding rates; the SIP-2/3 layers depend on platform trading volume. However, the fee-driven structure offers better cyclical resilience than a pure funding rate model.

Preview of Next Article

I'd like to talk about StandX from a different angle. As someone who used to evaluate projects from the VC side and now works on Growth inside a project, I increasingly feel that this team has some severely underrated qualities. For instance, why some DEXes ranked higher than us on DefiLlama have price differences on BTC perpetual contracts that are $20-30 larger compared to StandX (high trading volume ≠ good trading experience), or the design logic behind each product proposal from SIP-1 to SIP-3. Having a great product but being unknown might be the most common and unfortunate thing in this sector. The next article will try to bridge that information gap.

If you try this strategy, feel free to share your earnings screenshots in the comments.

Disclaimer: I am responsible for Growth work at StandX. This article contains personal test data and industry analysis, and does not constitute investment advice. DeFi protocol risks include but are not limited to smart contract vulnerabilities, liquidity risk, funding rate volatility, etc. DYOR.

Data Source: StandX platform test data (May 7-15, 2026). All APY data is time-sensitive; please refer to real-time data.