Author: Predictefy

Compiled by: Deep Tide TechFlow

Deep Tide Guide: In January 2026, prediction markets processed over $23 billion in nominal trading volume. In the same month, Hyperliquid alone processed over $225 billion. Outcome trading could bring tens of billions of dollars in new trading volume to prediction markets.

Predictefy analysis indicates that the key to HIP-4 lies in integrating outcome contracts into the same margin framework as perpetual futures, bringing event trading into the same environment as other crypto derivatives.

This could bring tens of billions of dollars in new trading volume and open interest to prediction markets in a short period. Conservative estimates suggest partial adoption could reach $28 billion in monthly trading volume, moderate adoption $33 billion, and strong integration over $40 billion.

Full text below:

Prediction markets processed over $23 billion in nominal trading volume in January 2026. Hyperliquid alone processed over $225 billion in the same month. Outcome trading could bring tens of billions of dollars in new trading volume to prediction markets.

Prediction markets are growing rapidly, but they primarily operate in isolation. You can trade event outcomes, but these positions are not within the same systems traders use to manage broader market risks.

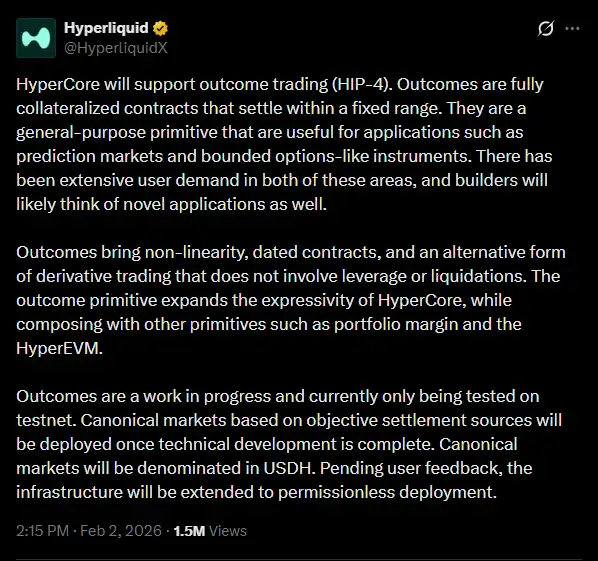

HIP-4 changes this. On Hyperliquid, outcome contracts share the same margin framework with perpetual futures, bringing event trading into the same environment as other crypto derivatives.

This could bring tens of billions of dollars in new trading volume and open interest to prediction markets in a short time. Here’s how it works.

Prediction Markets Are Already Substantial

Over the past year, prediction markets have moved beyond niche activity.

- Weekly trading volume on major platforms has repeatedly exceeded $6 billion

- A recent month recorded approximately $23.8 billion in nominal trading volume

- Market share remains concentrated, with platforms like Polymarket, Opinion, and Kalshi dominating most activity

Despite this growth, prediction markets still primarily function as standalone venues. Event exposure, directional crypto exposure, and volatility exposure typically require separate platforms, collateral pools, and risk systems. This fragmentation limits capital efficiency and constrains the types of strategies traders can implement.

Outcome Contracts Bring Risk into Core Infrastructure

Outcome contracts introduced via HIP-4 have several defining characteristics:

- Positions are fully collateralized

- Settlement occurs within a fixed and bounded payment range

- No liquidation mechanism

- Contracts are event-based or time-based

- Positions are integrated into the same margin framework as perpetual futures

Binary contracts themselves are not new. The structural change lies in their integration into a unified derivatives engine. Event exposure can now share collateral with perpetual positions, allowing risk to be managed at the portfolio level rather than the individual market level.

Improvements in Capital Efficiency

Previously, implementing event-driven strategies typically required traders to:

- Deposit collateral on a prediction market platform

- Deposit separate collateral on a perpetual futures venue for hedging

- Manage risk and margin independently across venues

This setup increased capital requirements and operational complexity.

With outcome contracts in a shared trading environment, event exposure and directional hedging can be managed together. Portfolio margin systems can recognize offsetting risks, reducing total margin usage. This aligns event trading with established derivatives risk management practices.

Current Market Size and Trading Volume Growth Potential

Prediction markets processed approximately $20-25 billion in monthly trading volume in January 2026 under today's isolated structure, with event trading located outside the broader derivatives stack.

In contrast, Hyperliquid recorded over $225 billion in perpetual futures volume in the same month, with daily perpetual trading volumes reaching the multi-billion dollar range. The pool of derivatives liquidity is already much deeper than standalone prediction market activity.

If HIP-4 improves capital efficiency and makes event positions easier to hedge within the same system, trading activity could expand through structural churn—more strategies running on the same capital.

Conservative scenario suggests:

- Partial adoption → $28 billion monthly prediction market trading volume

- Moderate adoption → $33 billion

- Strong integration → Over $40 billion

These estimates reflect strategy integration, not hype cycles, and do not include the ongoing monthly growth already seen in prediction market volume, which could push total volumes even higher.

Prediction Markets Begin to Resemble Options Infrastructure

Outcome contracts introduce:

- Non-linear payouts

- Event-driven settlement

- Bounded risk profiles

These characteristics overlap with options-like exposure. This creates a foundation for:

- Event volatility strategies

- Structured products incorporating outcome positions

- Systematic portfolios combining event and market risks

- Protocols building new products on top of outcome primitives

Prediction markets shift from being primarily narrative-driven to becoming available components in broader financial strategies.

Competitive Landscape

Standalone prediction market platforms retain advantages in brand recognition, liquidity depth, and simplicity. However, platforms integrating event risk with perpetual contracts and other derivatives offer:

- Shared collateral pools

- Instant hedging within the same environment

- Portfolio-level risk netting

Even partial migration of more advanced trading flows could affect where capital-efficient and hedge-intensive activities concentrate.

Signals of Adoption

Structural adoption will be reflected in trading behavior, not just headline volume:

- Pairing of outcome positions with perpetual hedges

- Growth in open interest around macro and policy events

- Emergence of vaults or structured strategies built on outcome exposure

- Narrowing spreads relative to standalone prediction market venues

These signals indicate outcomes are being used as financial instruments, not isolated event trades.

Conclusion

Prediction markets have achieved scale but have until now been structurally separated from the broader derivatives stack.

HIP-4 introduces a framework where event risk can coexist with perpetual futures within shared trading infrastructure. As this model evolves, prediction markets may increasingly function as components of diversified risk portfolios, rather than standalone betting venues.