Author: Nishil Jain

Compiled by: Block unicorn

Preface

In the 1960s, the credit card industry was in chaos. Banks across the United States were trying to establish their own payment networks, but each network operated independently. If you held a Bank of America credit card, you could only use it at merchants that had a cooperation agreement with Bank of America. When banks tried to expand their business to other banks, all credit card payments encountered the problem of interbank settlement.

If a merchant accepted a card issued by another bank, the transaction had to be settled through its original check settlement system. The more banks that joined, the more settlement problems arose.

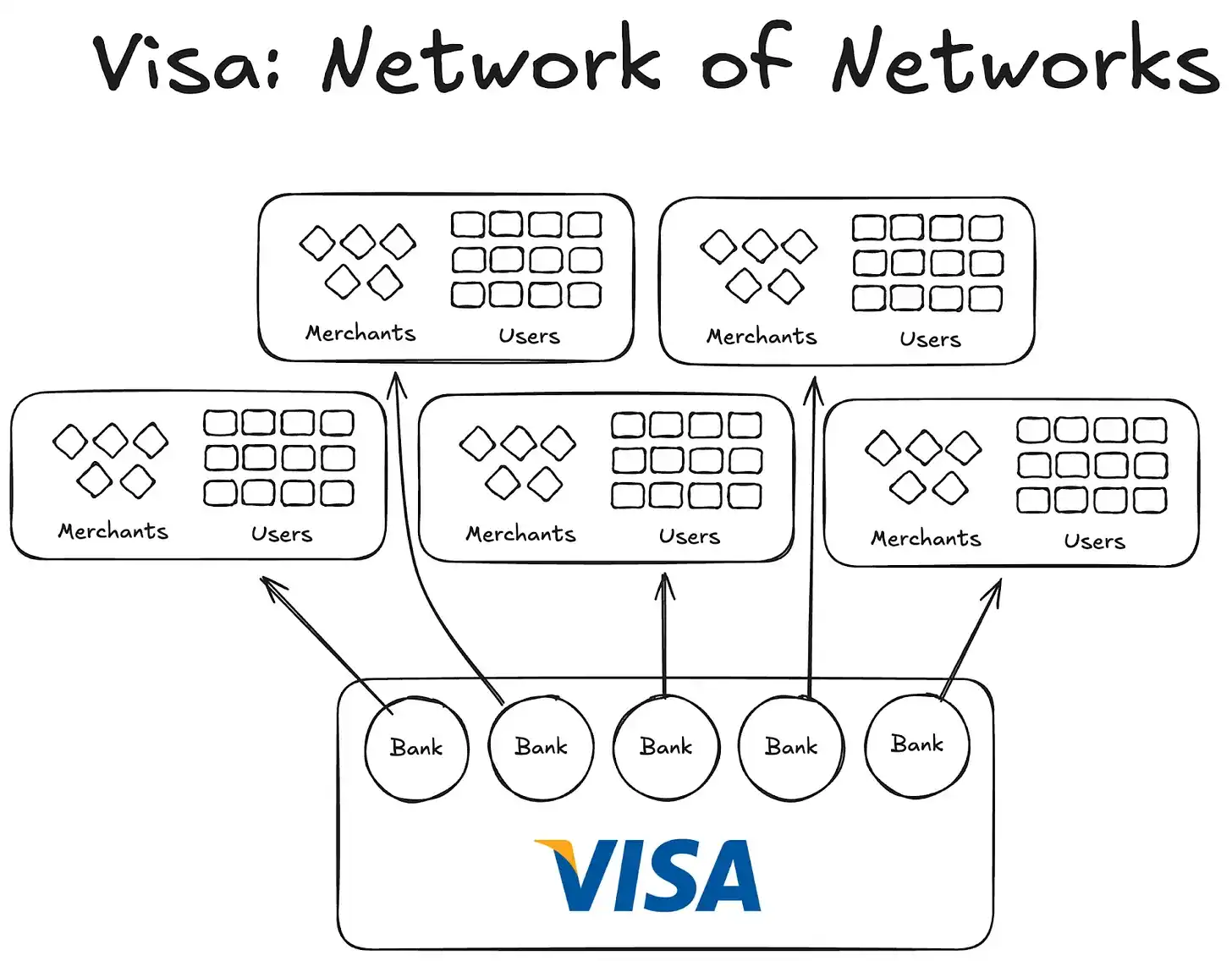

Then Visa emerged. Although the technology it introduced undoubtedly played a huge role in the credit card payment revolution, the more important success lay in its global universality and its success in getting global banks to join its network. Today, almost every bank in the world has become a member of the Visa network.

While this seems very normal today, imagine trying to convince the first thousand banks, both inside and outside the United States, that joining a cooperation agreement instead of building their own network was a wise move. Then you begin to realize the scale of this endeavor.

By 1980, Visa had become the dominant payment network, processing about 60% of credit card transactions in the United States. Currently, Visa operates in over 200 countries.

The key was not more advanced technology or more funding, but the structure: a model that could coordinate incentives, decentralize ownership, and create compound network effects.

Today, stablecoins face the same fragmentation problem. And the solution may be the same as what Visa did fifty years ago.

Experiments Before Visa

Other companies that appeared before Visa failed to develop.

American Express (AMEX) tried to expand its credit card business as an independent bank, but its scale expansion was limited to continuously adding new merchants to its banking network. On the other hand, BankAmericard was different; Bank of America owned its credit card network, and other banks only utilized its network effects and brand value.

American Express had to approach each merchant and user individually to open their bank accounts, while Visa achieved scale by accepting banks itself. Each bank that joined the Visa cooperative network automatically gained thousands of new customers and hundreds of new merchants.

On the other hand, BankAmericard had infrastructure issues. They did not know how to efficiently settle credit card transactions from one consumer bank account to another merchant bank account. There was no efficient settlement system between them.

The more banks that joined, the worse this problem became. Thus, Visa was born.

The Four Pillars of Visa's Network Effects

From the story of Visa, we learn about 2-3 important factors that led to the accumulation of its network effects:

Visa benefited from its status as an independent third party. To ensure that no bank felt threatened by competition, Visa was designed as a cooperative independent organization. Visa did not participate in competing for the distribution pie; the banks competed for it.

This incentivized participating banks to compete for a larger share of the profits. Each bank was entitled to a portion of the total profits, proportional to the total transaction volume it processed.

Banks had a say in the network's functions. Visa's rules and changes had to be voted on by all relevant banks and required 80% approval to pass.

Visa had exclusivity clauses with each bank (at least initially); anyone joining the cooperative could only use Visa cards and the network and could not join other networks—thus, to interact with Visa banks, you also needed to be part of its network.

When Visa's founder, Dee Hock, traveled across the United States to persuade banks to join the Visa network, he had to explain to each bank that joining the Visa network was more beneficial than building their own credit card network.

He had to explain that joining Visa meant more users and more merchants would be connected to the same network, which would promote more digital transactions globally and bring more benefits to all participants. He also had to explain that if they built their own credit card network, their user base would be very limited.

Implications for Stablecoins

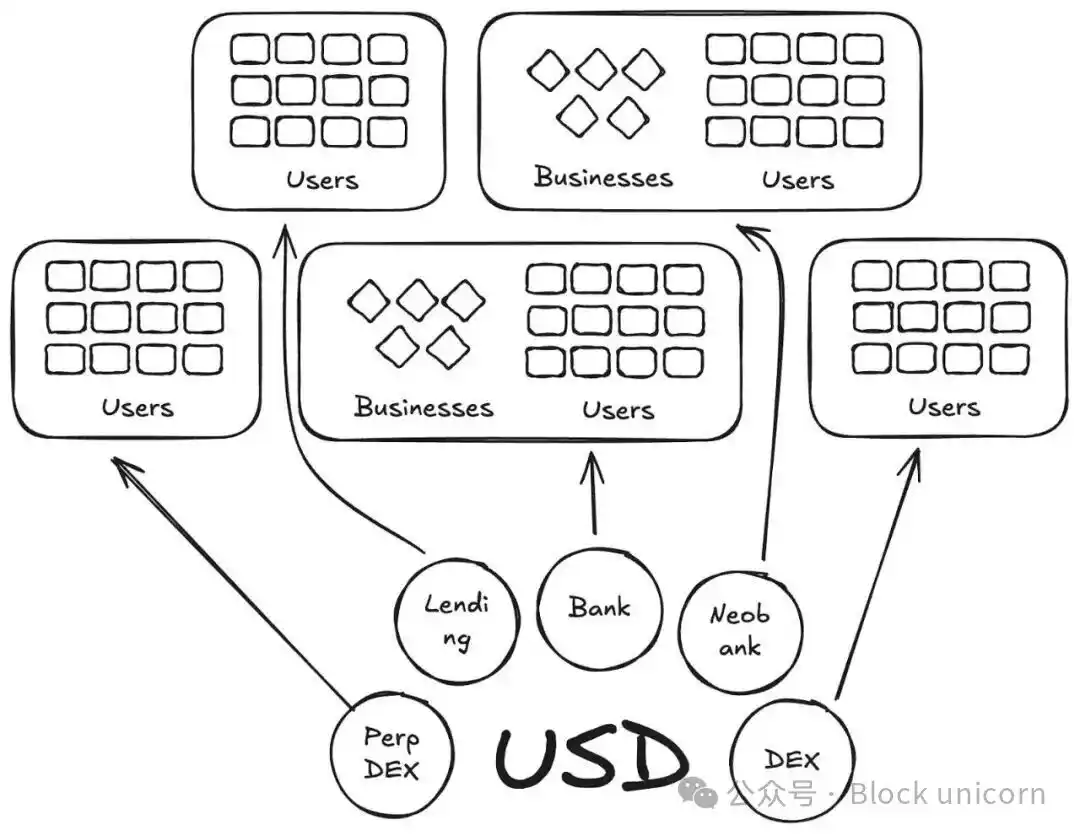

In a sense, Anchorage Digital and other companies now offering stablecoin-as-a-service are replaying the BankAmericard story in the stablecoin space. They provide the underlying infrastructure for new issuers to build stablecoins, but liquidity continues to fragment into new tokens.

Currently, over 300 stablecoins are listed on Defillama. Moreover, each newly created stablecoin is limited to its own ecosystem. As a result, no single stablecoin can generate the network effects needed to go mainstream.

Since the same underlying assets support these new coins, why do we need more coins with new code?

In our Visa story, these are like BankAmericards. Ethena, Anchorage Digital, M0, or Bridge—each allows a protocol to issue its own stablecoin, but this only exacerbates industry fragmentation.

Ethena is another similar protocol that allows yield transmission and white-label customization of its stablecoin. Just like MegaETH issuing USDm—they issued USDm through tools that support USDtb.

However, this model failed. It only fragments the ecosystem.

In the credit card case, the brand differences between banks did not matter because it did not create any friction in user-to-merchant payments. The underlying issuance and payment layer was always Visa.

However, for stablecoins, this is not the case. Different token codes mean an infinite number of liquidity pools.

Merchants (or in this case, applications or protocols) will not add all stablecoins issued by M0 or Bridge to their list of accepted stablecoins. They will decide based on the liquidity of these stablecoins in the open market; the coins with the most holders and the highest liquidity should be accepted, while the rest will not.

The Way Forward: The Visa Model for Stablecoins

We need independent third-party institutions to manage stablecoins of different asset classes. Issuers and applications supporting these assets should be able to join cooperatives and access reserve earnings. At the same time, they should also have governance rights and be able to vote on the direction of their chosen stablecoin.

From a network effects perspective, this would be a superior model. As more issuers and protocols join the same token, it will facilitate the widespread adoption of a token that retains earnings internally rather than flowing into others' pockets.