Written by: CryptoVizArt, Frederik Theissen, Glassnode

Compiled by: Luffy, Foresight News

Bitcoin price has remained below the true market average and the short-term holder cost basis for five consecutive months, placing it in a deeply undervalued range.

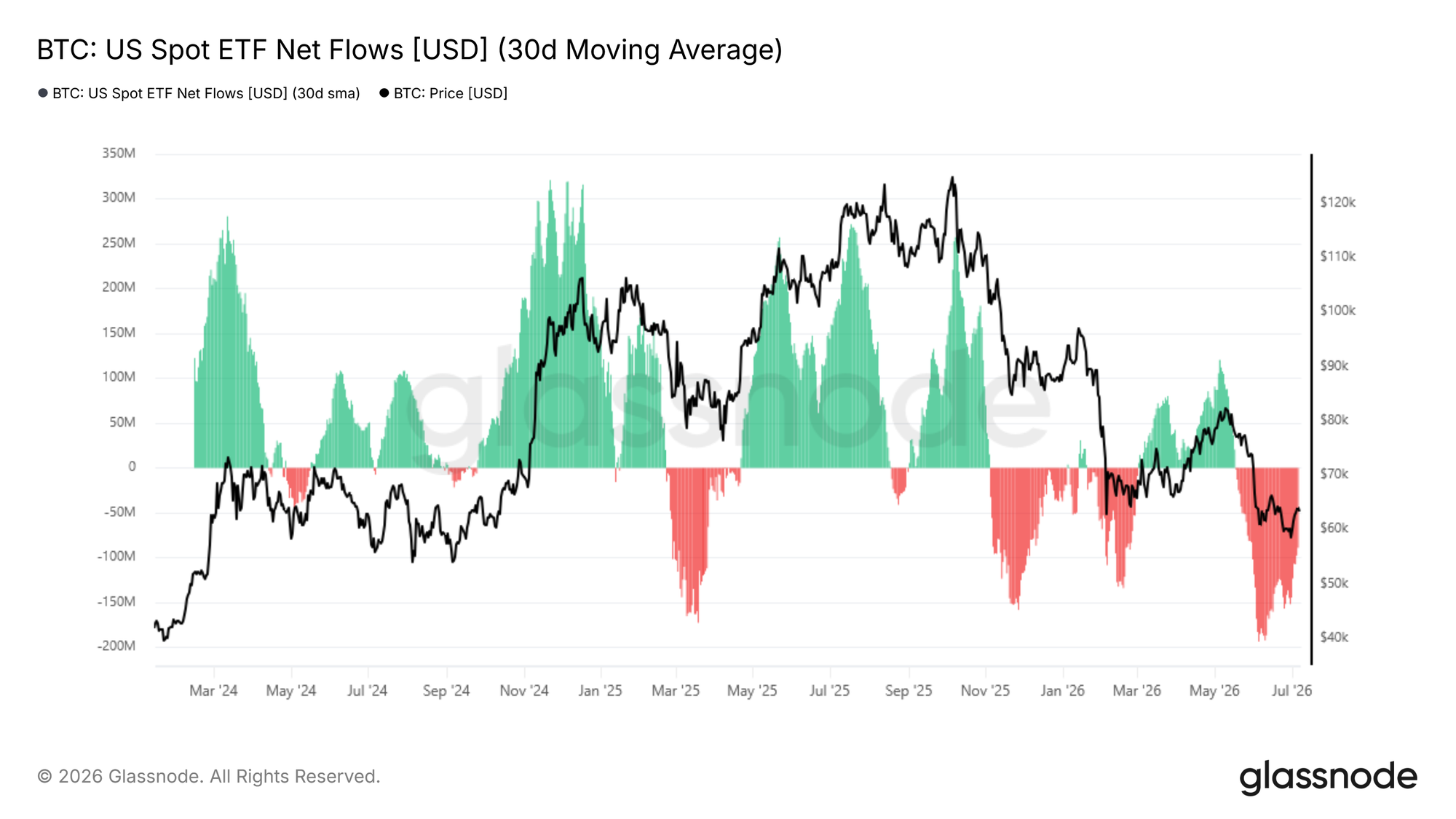

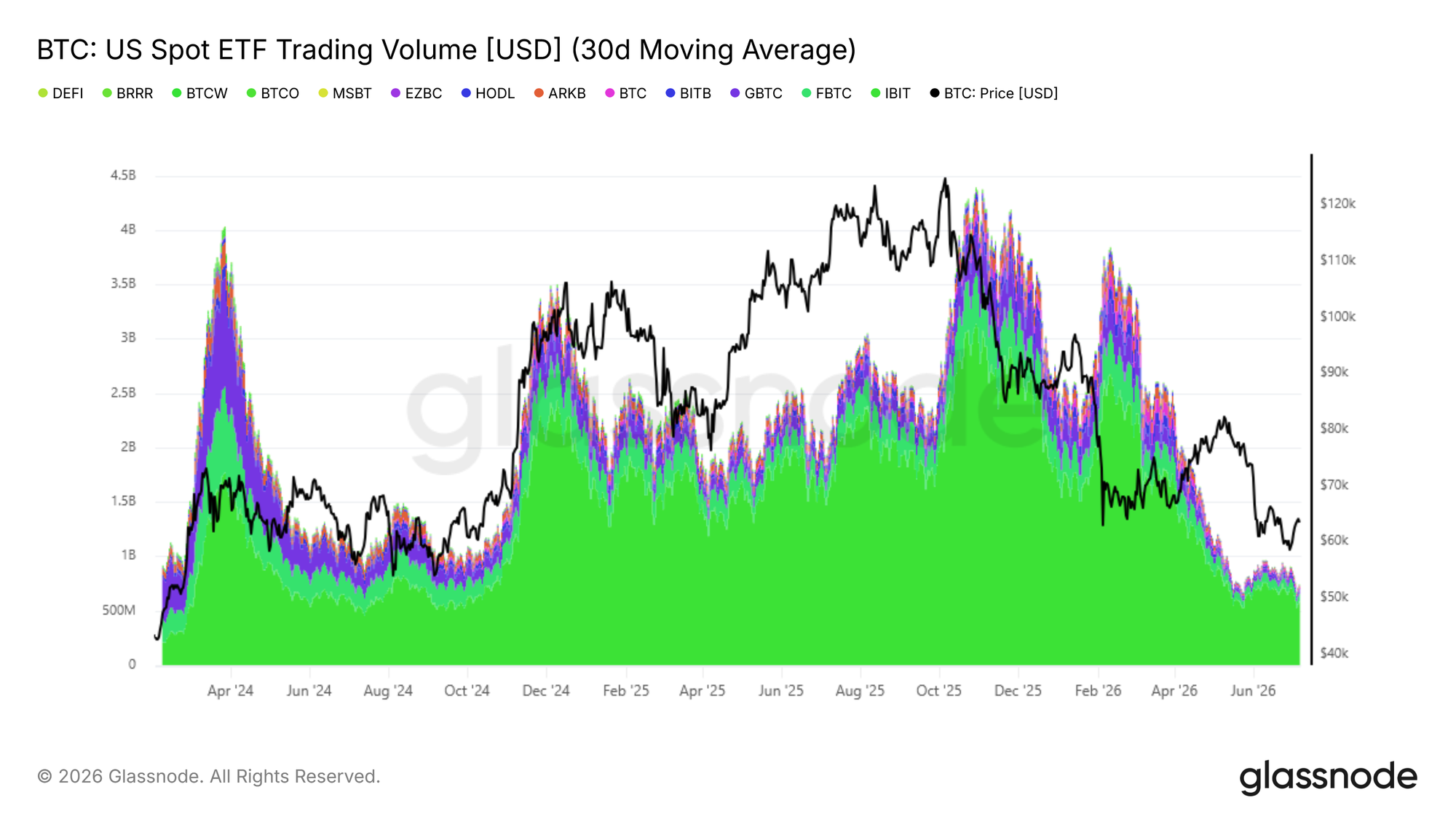

The proportion of realized losses by long-term holders has now risen to 43% of total on-chain realized losses. The daily peak of realized losses reached $280 million, hitting the highest level since December 2022. Spot ETF outflows have moderated but remain in a state of net monthly outflow. The daily average trading volume of ETFs fluctuates between $650 million and $950 million, roughly 80% lower than the market peak in October 2025, indicating institutional buying demand has not yet stabilized.

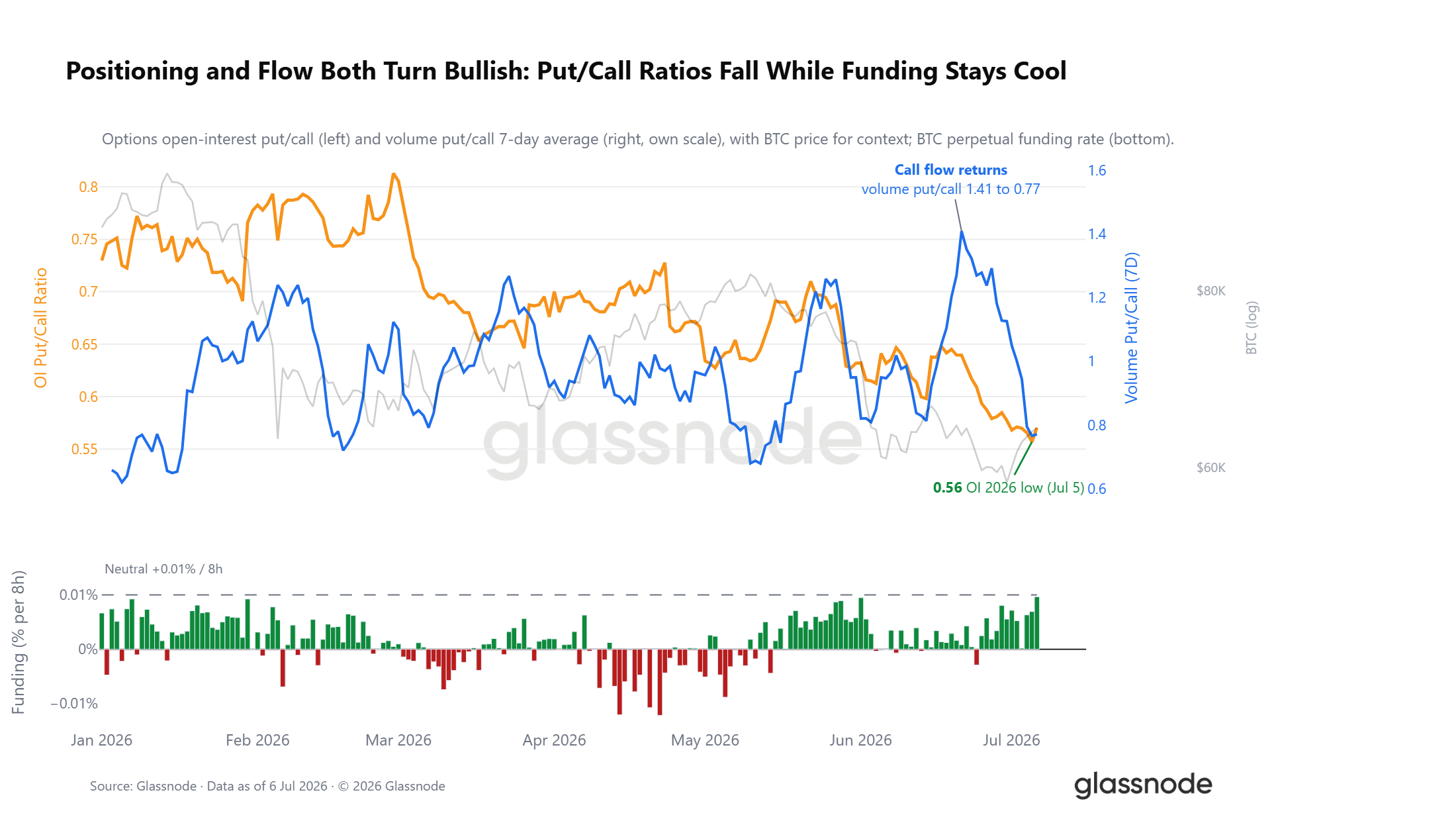

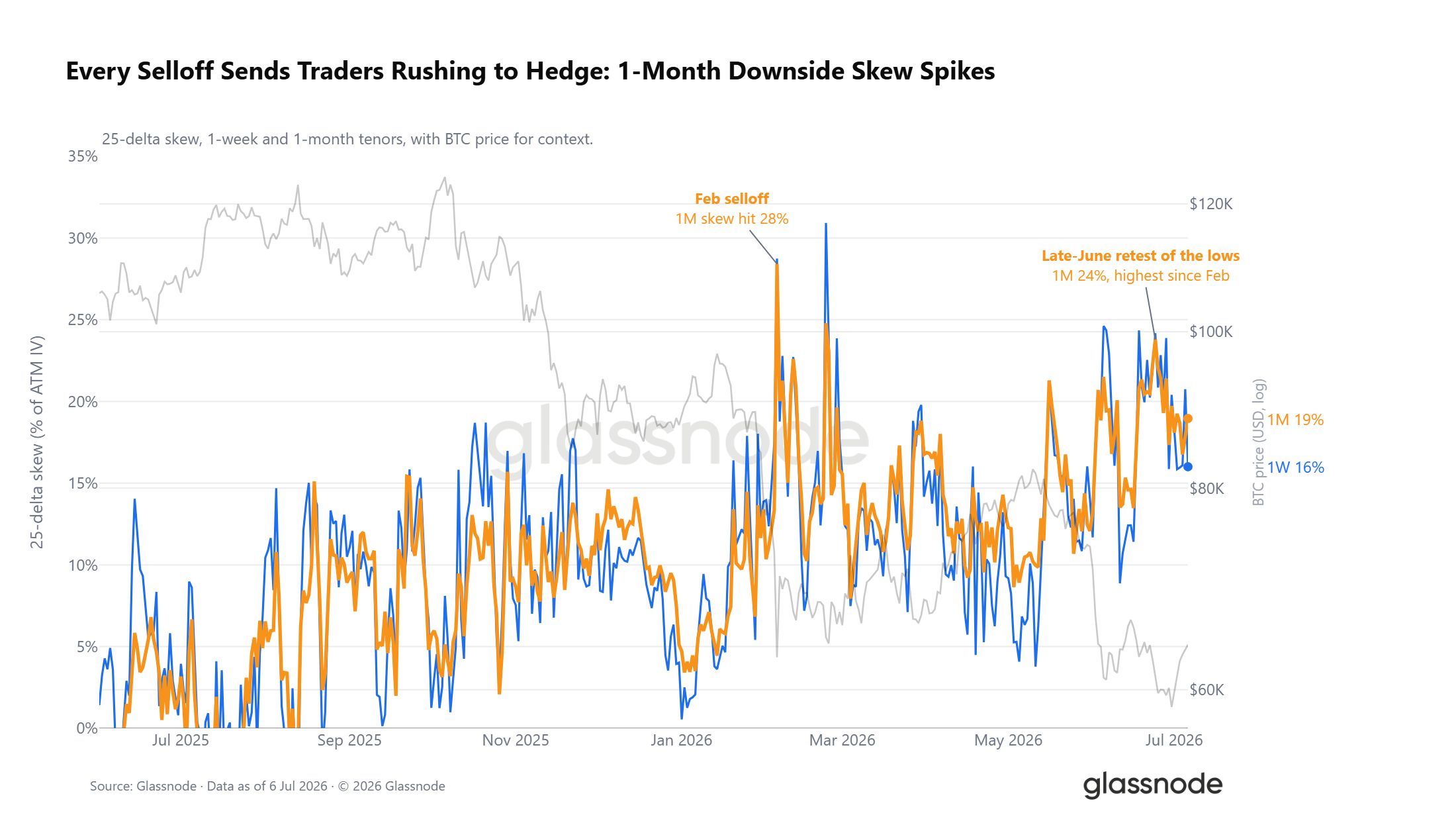

Derivatives positioning has shifted to a cautiously bullish bias, with the put/call ratio dropping to its lowest level in 2026. However, the options volatility surface still maintains a premium for downside protection, and the spot price remains significantly below the maximum pain point. The market has entered the later stages of bottoming, while selling pressure from long-term holders continues to narrow, forming an important precondition for a market reversal and recovery.

Macro Perspective

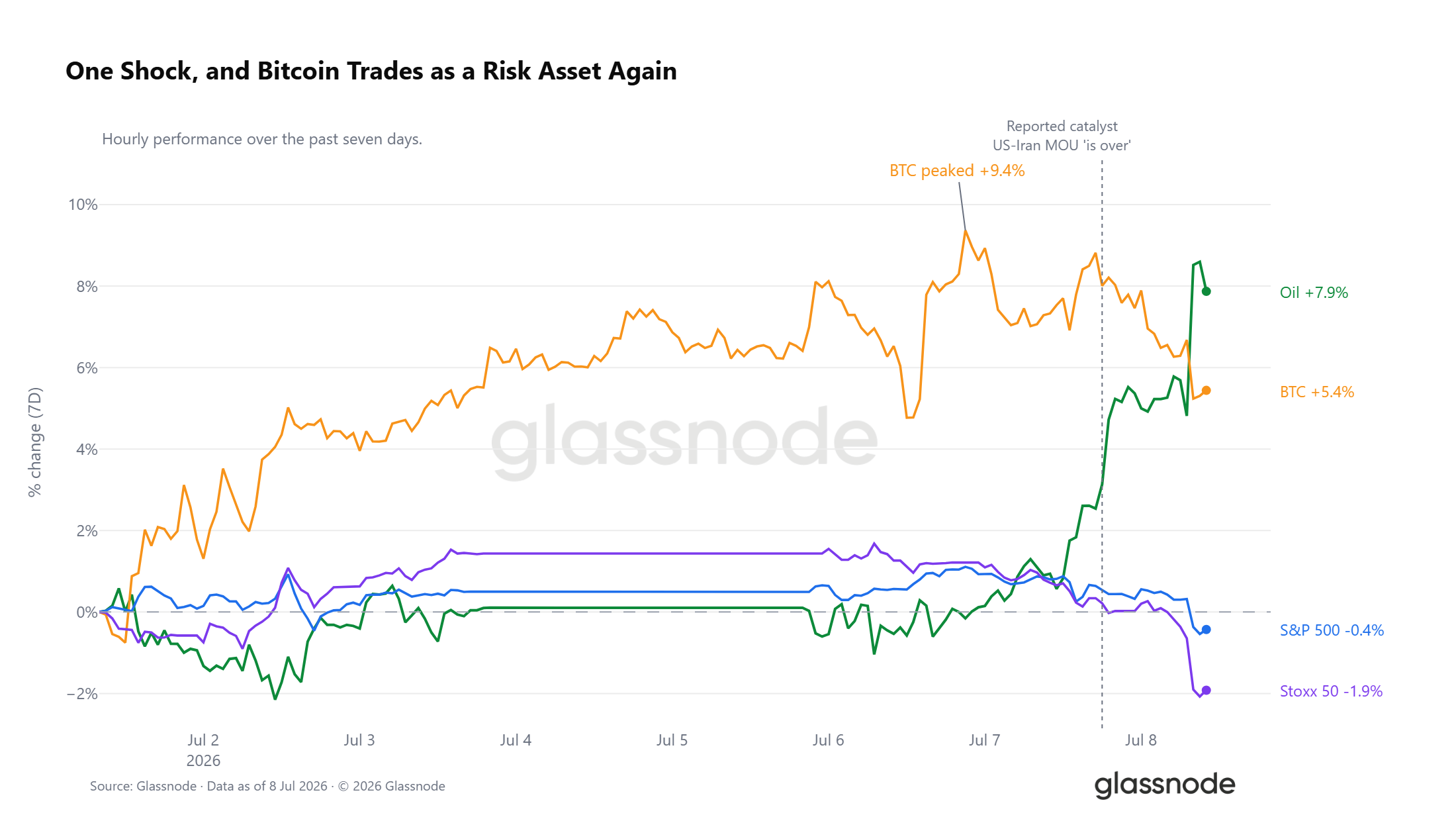

Crude Oil Soars, Risk Assets Face Collective Pressure

WTI crude oil has surged 7.9% over the past 7 trading sessions, with most gains concentrated recently, following market news that the US-Iran Memorandum of Understanding has expired. This shock has impacted all asset markets. Bitcoin rose as much as 9.4% this week but has since pulled back to a weekly gain of 5%; the S&P 500 and Euro Stoxx indices have turned negative, with European equities leading the decline among global risk assets. Bitcoin's current trend is highly synchronized with risk assets.

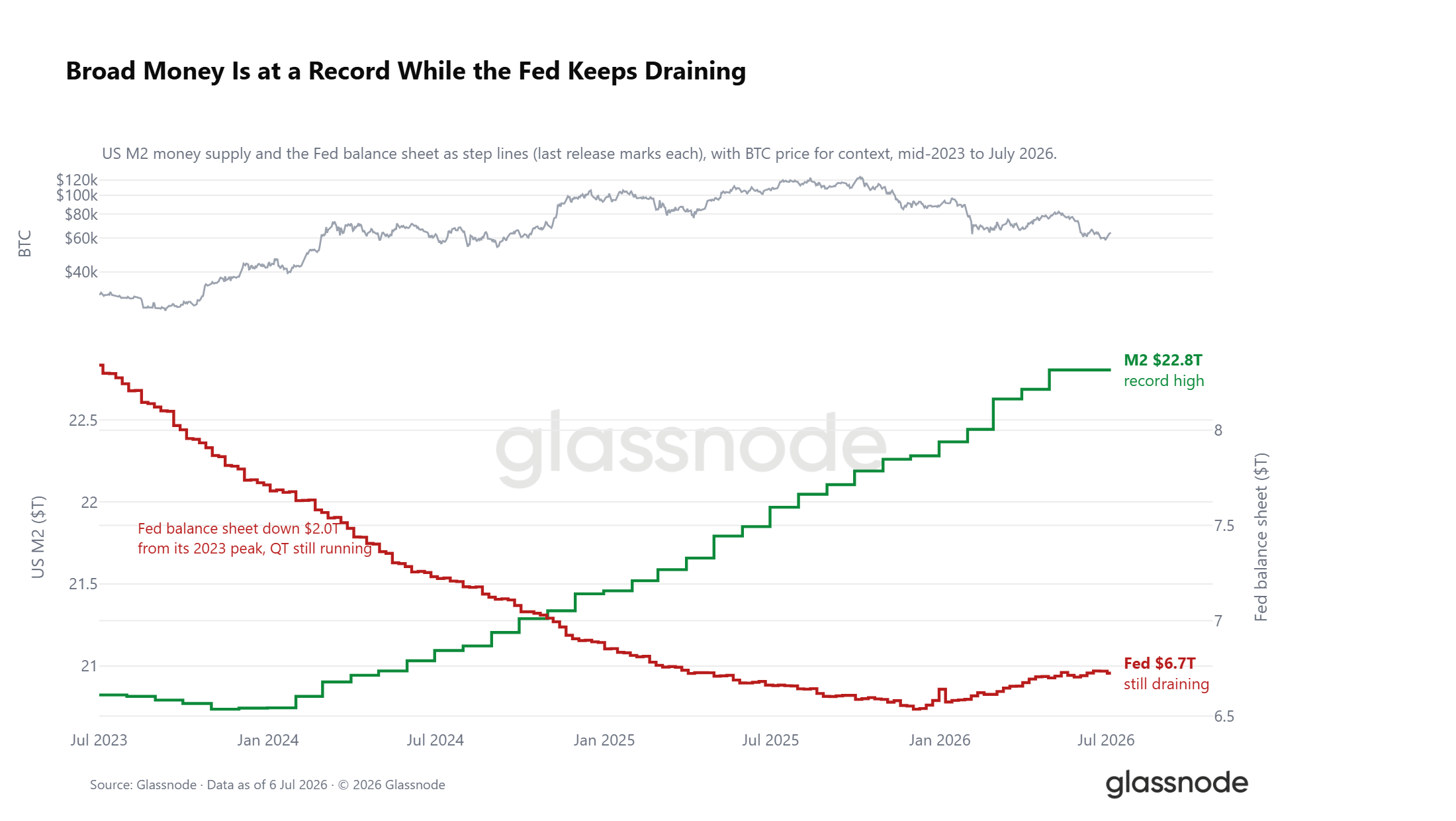

Liquidity Environment: Bull-Bear Contradictions Intensify

Amid the external shock from crude oil, the market liquidity environment presents a fragmented picture. The broad US money supply M2 has climbed to a historical high of $22.8 trillion. Historically, periods of broad money expansion tend to boost market risk appetite. However, the Federal Reserve's balance sheet continues to shrink, currently down $2 trillion from its 2023 peak. These two liquidity signals form a strong counterbalance: broad money supply continues to rise, while quantitative tightening continues, keeping real interest rates around 1% and the opportunity cost of holding non-yielding digital assets high. The macro tailwind window is not completely closed but has not yet formed clear easing support.

On-Chain Data

A Five-Month Deeply Undervalued Range

Over the past week, Bitcoin rebounded from $58,300 to $64,400, showing short-term recovery. However, the price remains significantly below the true market average of $76,600 and the short-term holder cost basis of $72,200. The market cannot exit the deeply undervalued range until the price reclaims these two key levels; otherwise, the market remains vulnerable to downside catalysts from external negative factors.

The duration of this discounted pricing period is noteworthy. Since early February 2026, the price has consistently traded below the cost basis of active investors and the breakeven point for recent entrants, spanning nearly five months. This is one of the longer-lasting deep discount cycles in Bitcoin's history.

Sustained turnover of coins during a prolonged period of discount, with new capital continuously accumulating below the cost basis of previous buyers and active market participants, has historically been the foundation for forming a cycle bottom. This presents long-term allocation attractiveness for value investors. Various indicators suggest the bottoming process is entering its later stages, but the possibility of a retracement to $53,000 cannot be entirely ruled out.

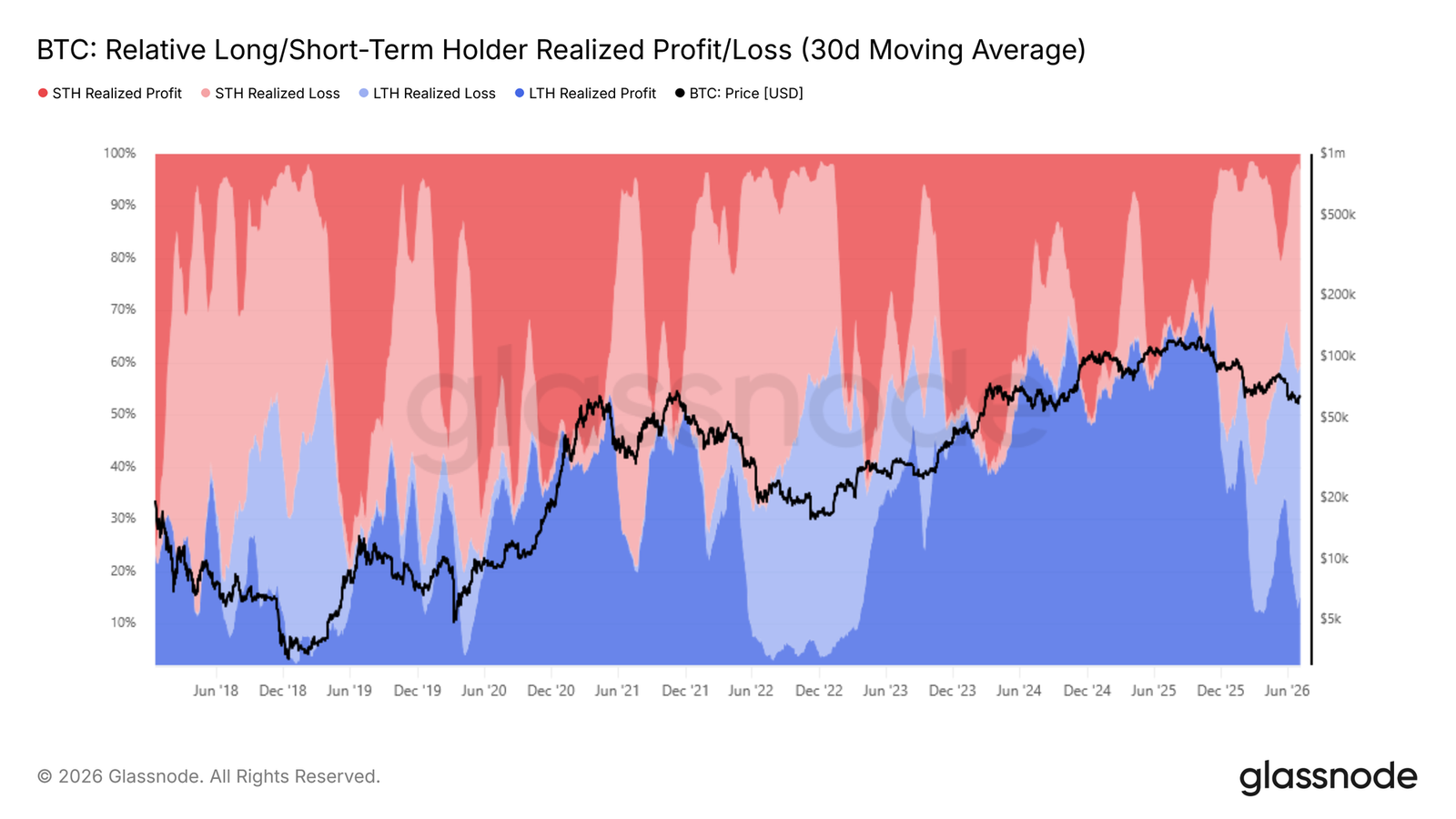

Concentrated Stop-Losses from Long-Term Holders with High-Cost Basis

The market is building a cycle bottom. The core current issue is identifying the main source of selling pressure. The relative indicator of profit/loss realization by long-term and short-term holders shows the distribution proportion of realized profits/losses across the entire market between these two cohorts, directly reflecting the scale of profit/loss-taking.

After the price fell below the true market average, the 30-day moving average of realized loss amounts by long-term holders has climbed from 15% in early February 2026 to the current 43%. Loss-driven selling from this group has become the core bearish force suppressing the price.

These investors mostly entered near cycle highs. After enduring months of deep drawdowns, their holding confidence has gradually depleted, leading to concentrated selling. This coin structure directly explains why each rebound faces concentrated selling from deeply trapped holders, preventing the price from firmly stabilizing above the current range's upper bound.

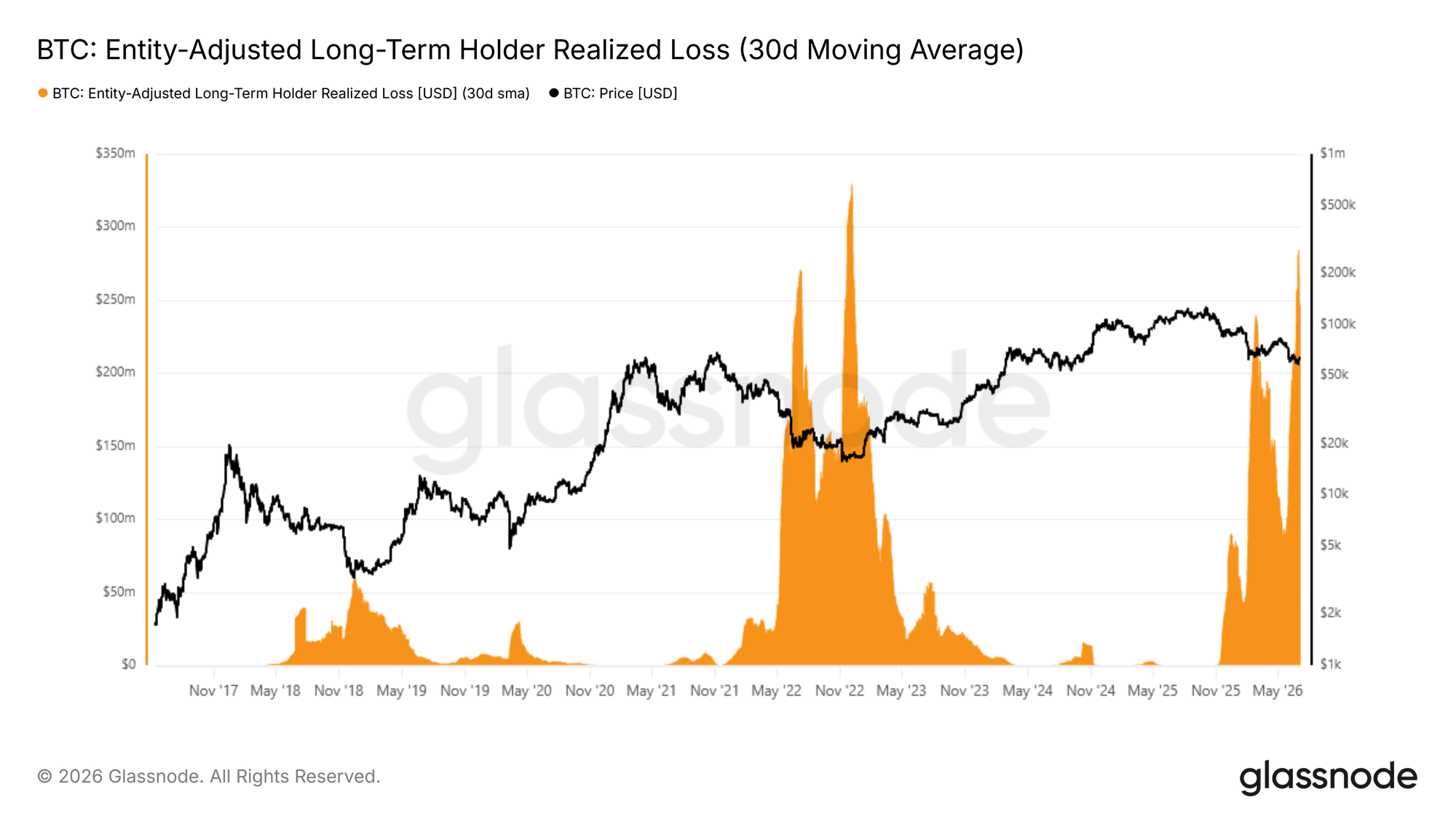

Stop-Loss Selling Pressure Shows No Signs of Abating Yet

With long-term holder realized losses becoming the market's primary downward pressure, the next key observation is whether this selling pressure begins to subside.

The Entity-Adjusted Long-Term Holder Realized Loss indicator (30-day smoothed average) measures the loss amount from sells by users holding for more than 155 days, excluding internal address transfers, precisely reflecting genuine stop-loss exit behavior. This indicator recently hit a new daily peak, with daily realized loss volume reaching approximately $280 million. This is the highest level since December 2022 and represents the second major wave of long-term holder stop-losses in this bear market.

The key difference is that after the first stop-loss peak, selling pressure temporarily receded. However, the current wave shows no signs of contraction in scale. A significant decline in this indicator is necessary for the market to establish a foundation for a shift towards a bull market. Its trend over the coming weeks and months will be the core signal for judging whether the market has truly cleared out selling pressure.

Off-Chain Market

ETF Outflows Slow, But Outflow Trend Not Reversed

Shifting from on-chain to off-chain markets, spot ETF fund flows provide direct insight into institutional capital behavior. The 30-day moving average of ETF net flows reflects the daily net capital outflow (or inflow) into US spot Bitcoin ETFs, smoothing out single-day volatility to reveal underlying institutional holding trends.

Since mid-May 2026, this indicator entered a state of monthly net outflow. The daily outflow peaked at $193 million in early June and has now subsided to a daily net outflow of $88.9 million. The slowdown in outflow size is a mild positive, but the market continues to experience persistent monthly capital bleeding, indicating institutional buying demand has not stabilized. Only when fund flows consistently narrow to a balanced range can we anticipate short-term price expansion to the upside.

Institutional Trading Volume Remains Sluggish

Besides net inflow data, US spot ETF trading volume helps assess the degree of institutional confidence recovery. The 30-day moving average of daily ETF trading volume currently fluctuates between $650 million and $950 million, comparable to levels seen in Q4 2024. However, this is about 80% lower than the daily peak of $4.4 billion recorded in October 2025.

The current trading volume reflects only basic institutional participation and remains extremely sluggish compared to bull market peaks, indicating that the long-term bullish confidence of ETF investors has not substantively returned. Only when daily trading volume consistently increases while net outflows continue to narrow, and these two signals appear simultaneously, can institutional demand recovery be confirmed. Until both indicators improve in tandem, off-chain data corroborates on-chain metrics, suggesting the market remains predominantly in a bearish structure.

Derivatives Market

Short Covering, Positioning Shifts to Cautiously Bullish

Despite weak risk sentiment, derivative positioning has shown a contrarian shift. The Options Open Interest Put/Call Ratio has dropped to 0.56, the lowest level in 2026. The market currently has approximately two call options for every put option. Option flow confirms this trend: two weeks ago, when Bitcoin revisited lows, the market frantically bought puts for hedging, causing the Put/Call Volume Ratio to spike. With sustained buying of calls, this ratio has rapidly declined, even though the spot price has only recovered part of its losses.

Perpetual swap funding rates also support this positioning shift. The average perpetual funding rate has remained below the 0.01% bull-bear equilibrium line for a long time, far from levels indicating crowded long positioning. The derivatives market has cleared out short-side risk and has shifted to a cautiously bullish stance overall amid external bearish shocks, which is the opposite of the crowded short positioning seen before the previous major decline.

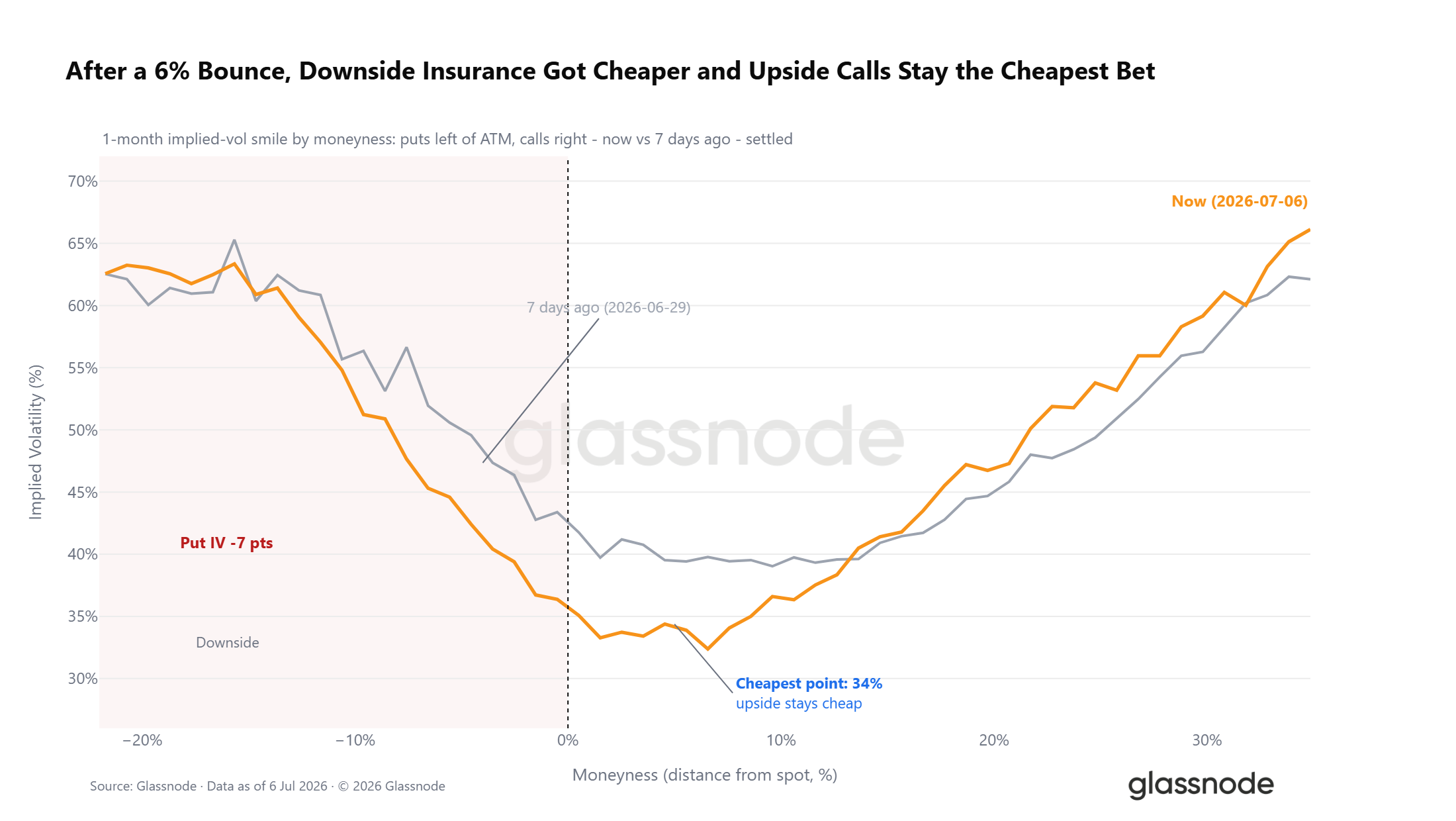

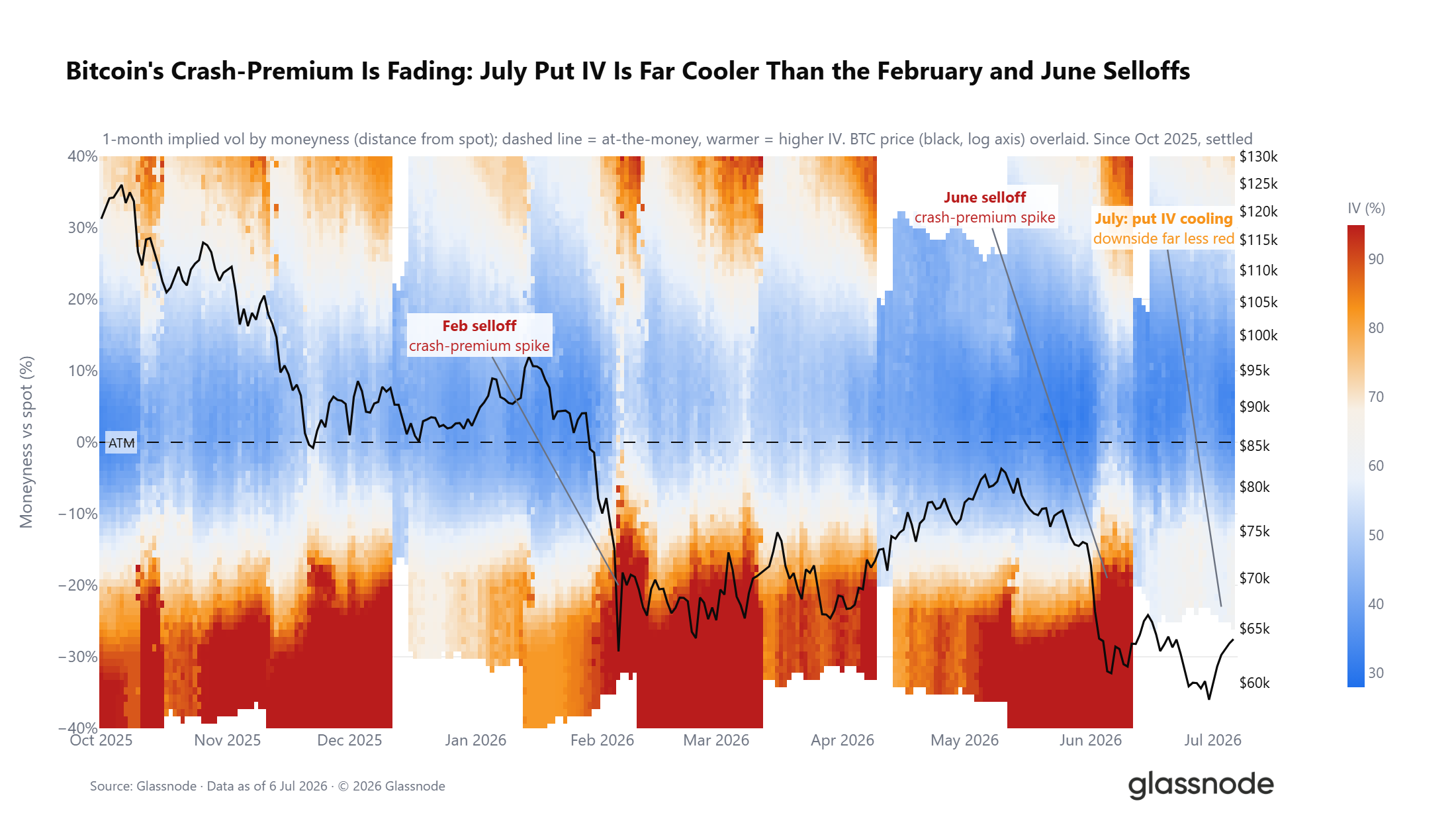

Options Surface Continues to Price Downside Risk

While overall positioning leans bullish, the options volatility surface provides a contrary signal. The 25-delta volatility skew (premium for downside protection relative to upside exposure) remains in positive territory across all tenors. Every sell-off this year has pushed this premium higher, peaking at 24% in late June. This represents the strongest defensive sentiment in front-month contracts since the February plunge. Even with a market bias towards longs, traders are still willing to pay a premium to purchase downside hedging instruments.

Spot Price Deviates from Max Pain Point

Besides positioning and volatility skew, the relative position of the spot price to the options market structure offers further insight. The current Bitcoin spot price is approximately 6% below the aggregate Max Pain point of $66,000. The Max Pain point is the strike price at which the maximum number of open contracts expire worthless upon option expiration, and prices tend to gravitate toward this level before expiry.

This week's decline widened the spread between the spot price and Max Pain, but the deviation is far less extreme than during the February plunge and sits near the middle of the 2026 trading range. Throughout the year, the Max Pain level has consistently acted as a gravitational center for price action, with the spot price oscillating around it, rarely experiencing sustained significant deviations. A sustained price above $66,000 would turn short-term signals optimistic. Further widening of the spread would reinforce the overall defensive sentiment reflected in options positioning.

Cost of Crash Hedging Continues to Decline

While volatility skew and positioning signals show divergence, the absolute cost of hedging downside risk presents a clearer trend. Following the market's modest rebound, the pricing across the bearish end of the 1-month volatility curve has shifted lower. The implied volatility for put options 5% below the spot price has declined significantly. The lowest pricing points on the volatility curve are concentrated in far-out-of-the-money call options.

While overall defensive sentiment persists, the absolute cost traders pay to hedge against declines has decreased noticeably. This trend becomes clearer over a longer timeframe: the volatility premium driven by extreme put buying during the February and June sell-offs has gradually faded since July. The DVOL volatility index has fallen to a 12-month low, indicating the market has entered a low-volatility regime. Cautious sentiment still dominates, but hedging demand is gradually receding.

Summary

A comprehensive assessment of data from three dimensions—on-chain, off-chain, and derivatives—clearly shows characteristics of a late-stage bear market.

On-chain data reveals a persistent, nearly five-month period of deep undervaluation. Long-term holders' daily stop-loss realization peaked at $280 million, indicating large-scale coin redistribution is underway. However, a sustained decline in this stop-loss indicator is a prerequisite for an effective market reversal.

In off-chain data, ETF outflow size has moderated from its June peak, but monthly net outflows persist. Daily average trading volume is down 80% from the October 2025 peak, reflecting weak institutional bullish confidence.

In derivatives, market positioning has shifted to cautiously bullish, with the put/call ratio hitting a yearly low. However, volatility skew and the options surface continue to price in downside risk.

Overall, the fundamental conditions for a market bottom are largely in place, but the key confirming signals have not yet materialized. A subsequent market recovery requires meeting three conditions: a sustained cooling of long-term holder stop-loss selling pressure, stabilization of institutional fund flows, and price stabilization above the true market average. Only under these conditions would the probability of a transition to a bull market cycle significantly increase.