Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

Amid the persistently sluggish crypto market and the ongoing contraction of liquidity, entrepreneurs within the industry are facing unprecedented pressure to find a breakthrough.

However, Odaily recently learned that multiple startup teams have begun to view the Hyperliquid ecosystem as a potential breakthrough direction. They aim to capture value for themselves while helping Hyperliquid attract traffic by building trading front-ends, strategy platforms, AI Agents, and HIP-3 custom markets (which allow for custom oracles, leverage limits, and settlement rules).

In the past, the idea of building a front-end to attract users for a particular DEX sounded unimpressive, as there was a prevailing market perception that the real value capture lay with the liquidity, matching engine, and underlying protocol itself, not with the front-end interfaces that depended on them.

But as the market elevates Hyperliquid's positioning to the level of an "on-chain Nasdaq," the value and potential of this business are also undergoing a transformation.

Odaily note: Refer to "After 220 Days of Trade.xyz's Launch, Hyperliquid Is Becoming the 'New Nasdaq'"

Analogous to traditional stock markets, retail investors do not trade directly on Nasdaq or the New York Stock Exchange. The platforms that actually build relationships with users are often brokerages like Robinhood, Interactive Brokers, and Charles Schwab — the exchanges provide the underlying market, liquidity, and matching capabilities; the brokers handle the user interface, product design, and experience optimization.

If the hypothesis that Hyperliquid becomes the next-generation Nasdaq holds true, then applications built on Hyperliquid that directly interface with users and optimize their trading experience are no longer just simple front-ends. Instead, their role becomes more akin to "brokers" in the traditional financial system.

Starting with HIP-3, How Do These 'Brokers' Generate Revenue?

Before understanding these specific "broker" platforms, we need to briefly answer two questions. First, what is HIP-3? Second, how should projects built around HIP-3 generate profits?

First, it's important to clarify that not only HIP-3 projects can "venture" around Hyperliquid. In theory, any team can build its own products based on Hyperliquid's underlying liquidity and trading capabilities. Some choose to build trading front-ends, some choose mobile applications, some choose strategy platforms, AI Agents, or asset management tools. Together, they share the responsibility of attracting traffic and expanding the user base for Hyperliquid.

Among all these directions, HIP-3 represents the track with relatively the highest potential and where there are already some successful cases. Simply put, HIP-3 allows third-party teams (Builders) to deploy perpetual contracts based on Hyperliquid's underlying liquidity and matching system and operate their own trading markets.

This means that startup teams no longer need to reinvent the wheel by building a new chain or setting up a new matching system from scratch, nor do they need to bear the R&D and security costs of high-performance trading infrastructure. Instead, they can directly leverage Hyperliquid's already mature infrastructure to focus on the product layer closest to the users.

In a sense, this is highly similar to the brokerage system in traditional finance. Nasdaq itself doesn't handle user advisory, UI design, community operations, or providing strategy products for users. These tasks are ultimately performed by brokerages like Robinhood. Therefore, the significance of HIP-3 can be understood as further opening up the market space for "brokers" operating atop Hyperliquid.

As for the revenue models of these "brokers," while some projects may generate income through derivative services (such as performance fees from asset management and strategies), the most direct source of revenue for such "broker" projects at present remains fee sharing and the appreciation potential of HYPE.

According to Hyperliquid's current mechanism requirements, third-party deployed markets adopt a fee standard higher than that of the native market, with a significant portion of this fee being returned to the deployer or front-end operator. This means that once a front-end successfully controls the user gateway, it unlocks real, sustainable, and directly transaction volume-linked cash flow. If a front-end can achieve a daily trading volume of tens of billions of dollars, the fee rebates alone could form a revenue scale of immense potential.

Furthermore, Hyperliquid officially requires third parties deploying custom trading applications to stake at least 500,000 HYPE (the official has indicated that this requirement will be gradually lowered in the future). Considering the recent strong price action and fundamental conditions of HYPE, the appreciation potential of HYPE itself is also a core source of revenue for such projects.

As for the future, the token issuance of the upper-layer "broker" projects themselves could also become a potential revenue source, which needs no further elaboration.

Overview of Representative Projects

Trade.xyz: Bringing US Stocks, Commodities, and Indices to Hyperliquid

If one were to find a project that best showcases the potential of the Hyperliquid ecosystem, Trade.xyz is undoubtedly the top choice.

To describe what Trade.xyz does in one sentence, it is "bringing assets from traditional financial markets onto Hyperliquid." Currently, Trade.xyz has successively launched perpetual contract products including the Nasdaq Index, S&P 500 Index, gold, crude oil, and some US stocks. For crypto users, this means they can participate in the price fluctuations of traditional financial markets directly through Hyperliquid's liquidity system without leaving the on-chain environment.

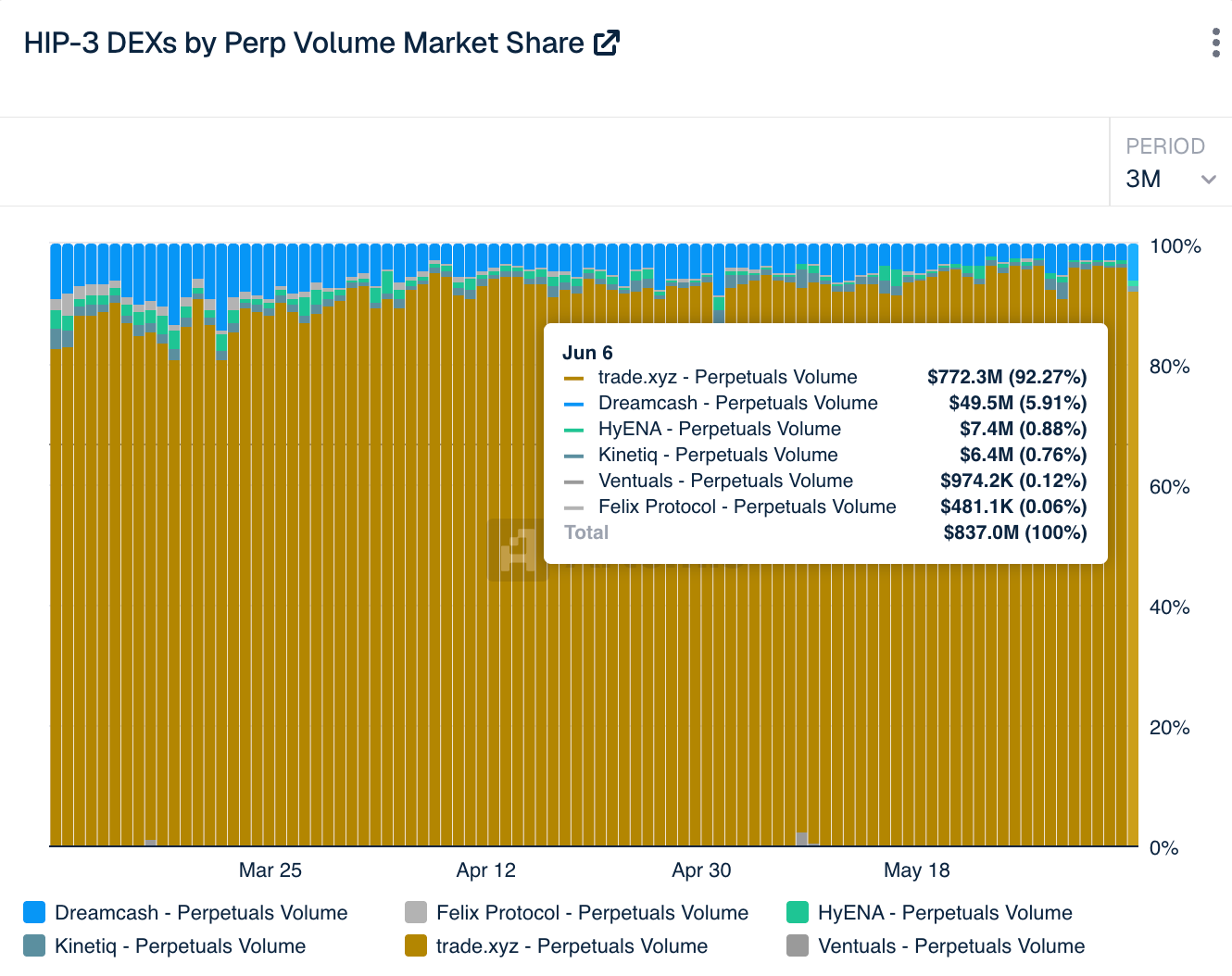

As of now, Trade.xyz holds an absolute dominant share in both Open Interest (OI) and daily trading volume within the HIP-3 markets. Real-time data from Artemis and The Block shows that it monopolizes over 90% of the current HIP-3 market share.

For Hyperliquid, the significance of Trade.xyz lies in expanding the asset boundaries of the ecosystem. In the eyes of many, whether Hyperliquid can ultimately grow into an "on-chain Nasdaq" depends not on how much trading volume it can generate, but on whether it can become a unified trading network covering diverse asset classes, thereby accommodating new user groups and market demands.

For Trade.xyz itself, its value lies in being the first to occupy the promising track of on-chain trading for traditional financial assets. Today, the explosive trading volume and revenue data of Trade.xyz have already proven the strategic success of the platform.

Dreamcash: Capturing Mobile Traffic

If Trade.xyz aims to expand Hyperliquid's asset boundaries, then Dreamcash focuses on expanding its user boundaries.

For a long time, cryptocurrency trading products have shared a common problem — they are often designed for professional traders. Complex on-chain operations, obscure jargon, and high-threshold fund management methods have kept a large number of potential users at bay. Even for a platform like Hyperliquid, which already offers a fairly excellent trading experience, its primary user base remains native cryptocurrency traders.

Dreamcash attempts to address exactly this issue. Unlike many products emphasizing trading functionality, Dreamcash resembles more of a trading App from the mobile internet era. The project team has invested significant effort into mobile experience, a points incentive system, and user growth mechanisms, hoping to lower the barrier for ordinary users to access on-chain trading through more lightweight, gamified product design. Users only need to log in with an email or social media account to, within seconds, add leverage to cryptocurrencies or global macro assets with one click, similar to buying and selling stocks.

As of the time of writing, Dreamcash has surpassed 100,000 cumulative downloads across both iOS and Android platforms.

Ventuals: Pioneer in the Pre-IPO Market

Ventuals has not chosen to focus on mainstream assets already present in the market. Instead, it has extended its reach to the area with the highest barriers and most difficult access for ordinary investors in the traditional financial system — private equity in the primary market.

In traditional financial markets, equity subscriptions for highly imaginative tech unicorns like OpenAI, SpaceX, and Anthropic are often monopolized by top-tier investment banks and multi-billion-dollar funds. Retail investors not only lack access but also face extremely long lock-up periods and poor liquidity. The core logic of Ventuals is precisely to leverage the characteristics of HIP-3, which allows custom liquidation and settlement rules, packaging these Pre-IPO equities of unlisted companies into on-chain perpetual contracts. This allows global retail investors to directly participate in the long-short speculation of these unicorns' valuations before they officially go public.

A crucial reason why Nasdaq has become one of the world's most important capital markets is its continuous role in meeting the financing and pricing needs of new economy enterprises. To some extent, what Ventuals is attempting is similar — enabling on-chain markets not only to trade existing assets but also to provide price discovery mechanisms for future assets.

Of course, this direction still has a long way to go before maturity, but it is already one of the most noteworthy evolutionary directions for on-chain capital markets.

Based: The Next Stop, a "Super App"

Based aims to build a crypto "super app" covering trading, prediction markets, payment, and consumption scenarios.

Currently, Based offers trading terminal products on the web, desktop, and mobile (iOS, Android). Through Based, users can trade spot and perpetual futures on Hyperliquid, access prediction markets via Polymarket, and use Based Visa to spend cryptocurrency in the real world.

After the launch of HIP-3, Based took another step forward from being a mere front-end aggregator for Hyperliquid — it collaborated with Ethena to launch HyENA, a custom trading protocol based on Hyperliquid. Unlike other HIP-3 projects that mainly innovate around trading instruments, HyENA focuses on margin itself. The protocol introduces a margin system centered around a yield-bearing stablecoin (USDe), aiming to allow users to continuously generate yield from their idle margin while trading.

In a sense, this is more akin to introducing the logic of money market funds from traditional finance into on-chain trading scenarios. In the traditional brokerage system, idle cash in client accounts is often automatically allocated to money market funds to improve capital utilization efficiency. What HyENA is attempting is to reconstruct this experience in the on-chain environment.

Minara AI: When Agents Become Users

If projects like Trade.xyz, Dreamcash, and Based are still competing for human user gateways, then what Minara AI represents is another, more futuristic direction — the Agent gateway.

Minara's core product is a financial execution layer for AI. Users can directly issue trading instructions in natural language to AI tools like Claude or Cursor, and Minara will execute operations such as opening/closing positions and leverage management by calling Hyperliquid's underlying trading capabilities. In other words, in Minara's vision, the entity directly using the trading interface in the future might not be a human, but rather the AI Agent configured by the user.

In a sense, this trend extends beyond just the Hyperliquid ecosystem and is one of the most noteworthy trends across the entire internet world.

The Open, Combinatorial Relationship Constitutes Hyperliquid's Strongest Moat

As more and more teams choose to build upper-layer applications based on Hyperliquid, a more industry-wide question is being pondered by an increasing number of people — What does this combinatorial relationship between Hyperliquid and these on-chain "brokers" mean for competition within the exchange sector?

In the past, most people's understanding of exchanges remained at the stage of "competing on product." The competition was about who had a better UI, who listed more coins, who charged lower fees, and who could attract more users.

But Hyperliquid is driving a completely different competitive direction. More and more market participants are beginning to realize that what Hyperliquid aims to be is not the user-facing trading platform we are familiar with, but rather a set of financial infrastructure that can be directly invoked by APIs, programs, and even AI systems. The user-facing part is then handled by the upper-layer "brokers" built on top of it.

In a sense, this is very similar to the evolutionary path of software under the wave of AI. In the traditional internet era, products competed on UI, gateways, and user time. But in the AI era, more and more products are receding into "capability layers" — the API itself is becoming the new traffic gateway.

This is the new evolutionary direction that Hyperliquid is leading. It is precisely for this reason that more and more practitioners have begun to understand Hyperliquid as a "Financial Operating System" (Financial OS). It only needs to provide unified capabilities at the foundational layer, while the upper-layer "brokers" are responsible for creating specific scenarios.

Once this structure is formed, a strong symbiotic relationship is established between Hyperliquid and these upper-layer "brokers." For Hyperliquid, each additional upper-layer application equates to a new traffic gateway, a new user channel, and a new trading scenario. The protocol itself does not need to operate these products directly but can continuously share transaction fees and expand the network's liquidity depth. For these upper-layer applications, they are highly dependent on the liquidity, matching efficiency, and on-chain trading experience that Hyperliquid has already established. They don't need to build a new chain, reconstruct the order book, or re-cold-start liquidity. They just need to focus on two things — bringing users in and keeping them engaged.

This implies that the future competitive logic might no longer be a competition between one exchange and another, but could gradually evolve into competition between different financial networks. When more and more applications, Agents, and trading gateways choose to build on the same liquidity network, the network itself will develop an increasingly strong gravitational effect. And the platforms that successfully gather the most developers, the most applications, and the most user gateways will also possess the deepest liquidity and the broadest market coverage.

Perhaps this is Hyperliquid's strongest moat, and also the most imaginative aspect of the new Nasdaq.