Author: Ada, Deep Tide TechFlow

On June 4th, US Eastern Time, US tech stocks experienced severe volatility triggered by Broadcom's earnings guidance, revealing the first cracks in the AI valuation narrative.

Broadcom's FY2Q results themselves were not poor, with revenue of $22.2 billion and EPS of $2.44 both beating consensus estimates, and AI semiconductor business growing 143% year-over-year. However, its guidance for the current quarter failed to meet the market's already elevated expectations. CEO Hock Tan also revealed during the earnings call that its major custom chip client Google might diversify its supply chain, and that the expansion of the chip business would drag down gross margins. This combination pierced the core narrative that had supported AI trading for the past several months, triggering sharp capital rotation that day.

The Dow Jones Industrial Average surged 1.7% to a new record high, driven by traditional sectors. However, the Nasdaq Composite Index closed down 0.09%, and the Nasdaq 100 closed down 0.5%. Within this "barbell-shaped" divergent market, AI and semiconductor stocks faced broad selling pressure: Broadcom -12.59%, Micron -7%, Marvell pre-market down as much as 7%, AMD pre-market down over 4%.

Yet, amidst this wave of selling, AAOI charted an independent course starkly opposed to the sector sentiment.

Broadcom's Guidance Punctures Expectations, First AI Sector Valuation Correction

Broadcom became the catalyst that broke the AI trade not because its performance was bad, but because its guidance failed to match expectations that had been pushed to the limit.

Hock Tan disclosed during the earnings call that AI chip sales for this fiscal year (ending October) would reach $56 billion. While a massive number, it fell short of market expectations. Coupled with his comments about Google diversifying its supply chain, the market began to question the valuation premium Broadcom had enjoyed over the past year, supported by its ASIC business. Broadcom hit an intraday low of $403, erasing approximately $300 billion in market cap for the day, marking its largest single-day drop since January 2025.

The selling pressure quickly spread across the entire AI compute chain. The memory sector also saw heavy selling. Micron, viewed as a core supplier of HBM for AI accelerators and deeply tied to AI capital expenditure sentiment, fell about 7% for the day. Other storage-related names like SanDisk and Western Digital also weakened. While CrowdStrike's own Q2 revenue guidance wasn't poor, it was indiscriminately sold off amid the overall cooling of the AI trade.

Bridgewater founder Ray Dalio joined the chorus warning about AI valuations that day, explicitly distinguishing between "buying AI stocks" and "investing in AI technology," cautioning that current valuations "may be getting excessive." This echoed recent consecutive warnings about AI capital expenditures and high valuations from JPMorgan CEO Jamie Dimon and Apollo CEO Marc Rowan.

The direction of capital rotation was also telling—it flowed into traditional economy stocks represented by the Dow Jones, rather than a systemic retreat from risk assets. This indicates the market wasn't engaging in broad risk-off behavior but was structurally reducing positions within the AI sector.

AAOI's Independent Rally: Over 10% Gain in a Single Day, Reaching New Short-Term High Intraday

In this environment, AAOI posted a single-day gain of 11.76%, rising intraday from around $171 to $209.64 and closing at $202.89, forming a sharp contrast with the steep declines of Broadcom and Micron.

AAOI has experienced multiple rounds of intense volatility prior to this. The stock hit an all-time high of $233.67 on May 13th, fell 9% in a single day on May 29th, rebounded 17.18%-18.81% on June 1st, and again charted an independent 11.76% gain on June 4th. In the past 30 days alone, there have been over four trading sessions with single-day price swings exceeding 10%. This level of volatility has itself become the norm for AAOI's current valuation structure, with its trading volume on May 11th reaching 214% of its three-month average.

The medium-term catalysts driving AAOI's strength are relatively clear. On May 8th (the day after the company reported Q1 earnings), Rosenblatt raised its price target for AAOI from $140 to $220 in one go, reaffirmed its "Buy" rating, and listed it as a "Top Pick." Raymond James raised its target from $72.50 to $160 around the same time, while B. Riley raised its target to $129 but maintained a Neutral rating. Rosenblatt's core logic includes: 800G optical module revenue from Amazon beginning to contribute; potential qualification with Oracle opening a second revenue stream; and strong demand across the company's product generations from 100G/400G/800G to the emerging 1.6T.

The supporting data for the company's fundamentals are also specific. AAOI has publicly disclosed cumulative orders for 800G and 1.6T optical modules exceeding $324 million; in April 2026, it received a $20.9 million grant from the Texas Semiconductor Innovation Fund to expand its Sugar Land, Texas factory to 210,000 square feet; it also announced new 388,000 square feet of capacity in Pearland, targeting monthly production capacity of 700,000 units for 800G and 1.6T optical modules by 2027. Management guides to reaching an annualized run rate of $1.4 billion for its optical module business by Q3 2027.

However, AAOI's fundamentals are not without flaws. Its actual Q1 2026 earnings missed expectations, with a GAAP net loss of $14.3 million and revenue of $151.1 million, both slightly below market consensus. Q2 guidance for adjusted EPS is between -$0.03 and +$0.03, hovering around breakeven. When maintaining its Neutral rating, B. Riley noted that AAOI's 800G volume production would be delayed to the second half of the year, and there were execution risks from over-reliance on customer forecasts. Additionally, AAOI executives collectively sold approximately $12.6 million worth of stock in mid-May. While their remaining holdings are still substantial, the timing of the sales coincided with the stock's peak.

In short, AAOI is currently in a state of tension characterized by a "strong narrative, weak Q1 earnings, and significant valuation premium," which is the fundamental reason for its high single-day price volatility.

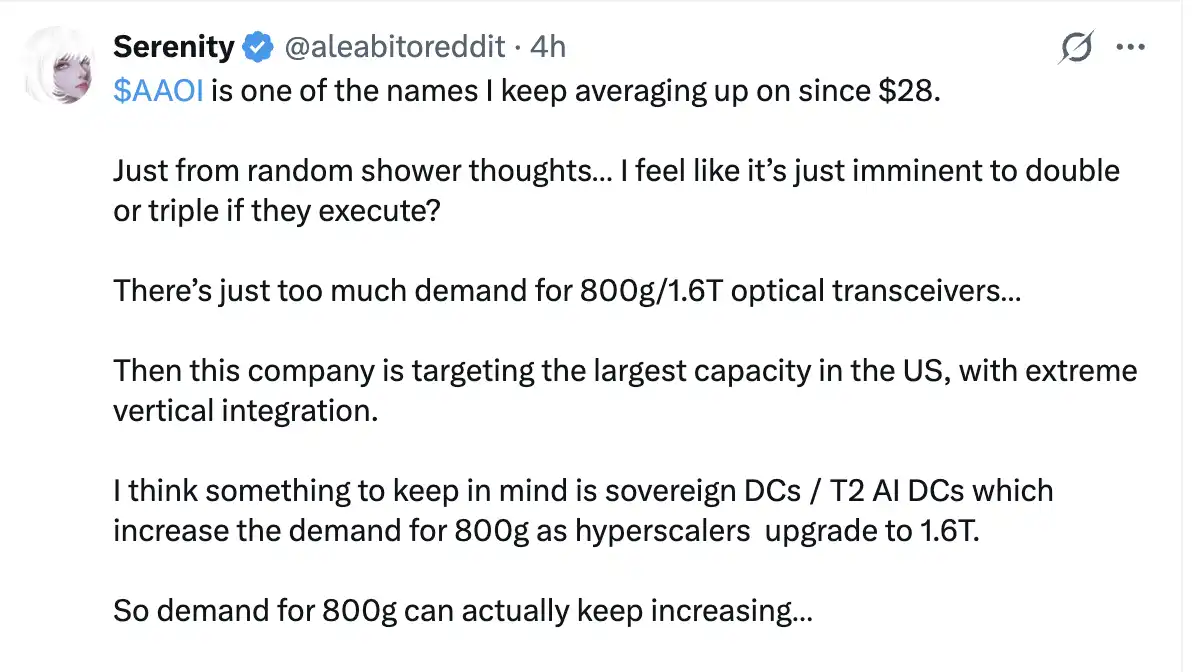

It's worth noting that AAOI has a potential additional driver: Serenity, known in Chinese circles as the "New Stock God," has posted multiple times expressing bullishness on AAOI, considering it his most favored optical communications exposure in the US stock market. He started building a position from $28 and believes it could be "the next SanDisk."

Logic Behind the Counter-Trend Strength: 'Differentiated Pricing' Within the AI Sector

AAOI's counter-trend strength on June 4th should not be interpreted as a counterexample to AI valuation concerns, but rather as an early signal that the market is beginning to engage in "differentiated pricing" within the AI sector.

One of Serenity's public judgments in April was that optical communication stocks might exhibit greater resilience than large-cap tech stocks: "Even if the S&P 500 falls another 20%, optical communication companies could still outperform." This logic is rooted in supply chain scarcity, with InP substrates, laser light sources, and 800G optical module capacity all in a state of structural tightness in the near-to-medium term, placing pricing power on the supply side rather than the demand side.

The selling pressure triggered by Broadcom's guidance essentially represents a correction to the "custom ASIC + high customer concentration" narrative, not a correction to the total demand for AI infrastructure. From this perspective, optical communication stocks, strongly tied to downstream compute deployment, do not directly overlap in narrative terms with Broadcom's core issues (customer concentration, potential Google supply chain diversification).

However, risks remain. AAOI's current stock price implies a valuation that already incorporates extremely high execution expectations, assuming it achieves the $1.4 billion annualized optical module revenue run rate by Q3 2027 while maintaining high margins. If Q2 or Q3 earnings fail to validate the 800G production ramp-up timeline, or if any issues arise with customer concentration risks (Amazon, Microsoft), the valuation structure could experience severe turbulence. The actual Q1 earnings were already weak; this crack is currently masked by order growth and capacity expansion narratives but has not been fully eliminated.

For observers in the Chinese market, what is noteworthy about AAOI's counter-trend move is not the gain itself, but the directional choice of capital differentiation within the market. When the overarching AI narrative shows its first cracks, the willingness of capital to buy into AAOI precisely during Broadcom's sell-off itself indicates a judgment: Broadcom's problems are not equivalent to all AI capital expenditure problems, and optical communications remains a recognized "physical bottleneck" narrative. Whether this judgment holds true will ultimately depend on the actual earnings reports in the coming quarters.