On January 22, 2026, Capital One announced the acquisition of Brex for $5.15 billion. This was a surprising deal—the youngest unicorn in Silicon Valley was acquired by the oldest bankers on Wall Street.

Who is Brex? The hottest corporate payment card company in Silicon Valley. Two Brazilian prodigies founded Brex at age 20, reached a $1 billion valuation in just one year, and achieved $100 million in ARR within 18 months. In 2021, Brex was valued at $12.3 billion, hailed as the future of corporate payments, serving over 25,000 companies, including star firms like Anthropic, Robinhood, TikTok, Coinbase, and Notion.

Who is Capital One? The sixth-largest bank in the U.S., with $470 billion in assets, $330 billion in deposits, and the third-largest credit card issuer in the country. Its founder, Richard Fairbank, is 74 years old. He founded Capital One in 1988 and spent 38 years building it into a financial empire. In 2025, he completed the $35.3 billion acquisition of credit card lender Discover, one of the largest M&A deals in the U.S. financial industry in recent years.

These two companies represent Silicon Valley's speed and innovation on one hand, and Wall Street's capital and patience on the other.

However, behind the numbers lies a paradox: Brex is still growing at 40-50%, with ARR reaching $500 million and over 25,000 clients. Why would such a company choose to sell, and at a price 58% below its peak valuation?

The Brex team says it's for acceleration and scale, but accelerate what? Why now? Why Capital One?

The answer to this paradox lies in a deeper question: In the financial industry, what does time mean?

Brex Had No Choice

After the acquisition news broke, many regretted that Brex did not choose an IPO. However, in the eyes of the Brex team, the deal came at just the right time.

Before engaging with Capital One, Brex's leadership had focused on raising more private capital, preparing for an IPO, and operating as an independent company.

The turning point came in the fourth quarter of 2025. Brex CEO Pedro Franceschi was introduced to Fairbank, the banking titan who has led Capital One for over 38 years. With a simple logic, Fairbank dismantled Pedro's resolve.

Fairbank laid out Capital One's balance sheet: $470 billion in assets, $330 billion in deposits, and the third-largest credit card distribution network in the U.S. In contrast, despite having the most seamless software interface and risk control algorithms, Brex's cost of capital was always constrained by others.

In the world of Fintech, growth was once the only currency. But by 2026, Fintech companies were simultaneously facing changes in the capital market environment, a reassessment of growth expectations, and an increasingly rapid pace of M&A consolidation in the financial services industry.

According to Caplight data, Brex's current secondary market valuation is only $3.9 billion. Brex CFO Dorfman mentioned a key detail in the post-acquisition review: "The board believed that a 13x gross profit acquisition multiple aligns with the premium standards of top public companies."

This statement implies that if Brex had chosen an IPO, given the market conditions in early 2026, a Fintech company growing at 40% but not yet fully profitable would find it extremely difficult to exceed a 10x valuation multiple in the public market. Even if it successfully went public, Brex's market cap would likely fall below $5 billion, facing long-term liquidity discounts.

On one side was an highly uncertain path to IPO, with the risk of post-IPO price drops and short attacks; on the other was the cash and stock combination offered by Capital One, along with immediate access to the credit backing of a major bank.

If it were merely due to valuation fluctuations, could Brex have chosen to optimize its software and algorithms to weather the capital winter? Reality did not give Brex that option.

The Balance Sheet Devours the World

For a long time, Silicon Valley believed in A16Z's famous mantra: "Software is eating the world."

Brex's founders were devout believers in this creed, but the financial industry hides an iron law that software engineers struggle to understand: in the war of money, user experience is merely the surface; the balance sheet is the true operating system.

As a Fintech company without a banking license, Brex is essentially a shell bank. Every credit it extends relies on the capital support of partner banks, and its deposit interest income must be shared with the banks providing the underlying account support.

This wasn't an issue in the era of low interest rates, as capital was abundant. But in a high-interest-rate environment, Brex's business model began to suffocate.

We can break down Brex's revenue structure: by 2023, about one-third of its revenue came from the interest spread on customer deposits, about 6% from SaaS subscription fees, and the rest relied on credit card transaction fees.

When interest rates remained at 5.5%, Brex faced a squeeze from both ends.

On one hand, funding costs were high, and clients were no longer willing to leave millions of dollars idle in Brex accounts that paid no interest. They demanded higher returns, which directly eroded Brex's interest spread.

On the other hand, risk weights increased. In a high-interest-rate environment, the risk of startup failures grew exponentially. Brex's proud real-time risk control system had to become conservative, slashing credit limits, which led to a significant slowdown in its transaction volume growth.

Fairbank made a含蓄 but sharp comment in the acquisition announcement: "We look forward to combining Brex's leading customer experience with Capital One's strong balance sheet." Translated, this means: your code is beautifully written, but you don't have enough cheap money.

Capital One has $330 billion in low-cost deposits, meaning that for the same $100 loan to a business, Capital One's profitability could be three times that of Brex.

Software can change the experience, but capital can buy the experience. This is the harsh truth of the Fintech industry in 2026. The software system that Brex spent 9 years and $1.3 billion in funding to build was, in the face of Capital One's雄厚 capital, merely a plug-in to be integrated.

But here lies the ultimate question: Why couldn't Brex, like Capital One, patiently wait for the next interest rate cycle? They are not yet 30, with successful track records and ample personal wealth. They could have sustained the company. What made them ultimately surrender?

29-Year-Olds Can't Wait, 74-Year-Olds Can

Because in the financial industry, time is not a friend; it is an enemy. And only capital can turn that enemy into a friend.

The careers of Henrique Dubugras and Pedro Franceschi are almost an epic of speed. They started a business at 16, sold it in 3 years. Started another at 20, became a unicorn in 2 years. They are accustomed to measuring success in years, even months. For them, waiting 5 to 10 years is almost the length of an entire career.

They believe in speed—rapid experimentation, rapid iteration, rapid success. This is the creed of Silicon Valley, and the biological clock of 20-year-olds.

But the opponent they encountered was Richard Fairbank.

Fairbank is 74 this year. He founded Capital One in 1988 and spent 38 years building it into the sixth-largest bank in the U.S. He doesn't believe in speed; he believes in patience. In 2024, he spent $35.3 billion to acquire Discover, and integration took over a year. In 2026, he spent $5.15 billion to acquire Brex, saying they could take 10 years to integrate.

These are two completely different time structures.

For the 20-year-old Dubugras and Franceschi, their time was bought with investors' money. Brex raised $1.3 billion, and investors expected returns within 5 to 10 years, either through an IPO or an acquisition.

Although this acquisition wasn't driven by investors, the need for investor exit was indeed a factor Pedro had to consider in his decision. CFO Dorfman repeatedly emphasized "providing 100% liquidity for shareholders"—this was no coincidence.

More importantly, the founders' own time is limited. Pedro is 29 this year. He could wait 5 years, 10 years, but could he wait 20 years? Could he, like Fairbank, spend 38 years slowly building a company? With competitor Ramp already surpassing them, the IPO window uncertain, and investors needing an exit, Pedro's time was also running out.

The 74-year-old Fairbank's time is bought with depositors' money. Capital One has $330 billion in deposits. Although depositors can theoretically withdraw at any time, statistically, deposits are a relatively stable source of funding. Fairbank can use this money to wait 5 years, wait 10 years, wait for interest rates to fall, wait for Fintech valuations to hit rock bottom, wait for the best acquisition opportunity.

This is the asymmetry of time. Fintech's time is limited, whether for founders or investors; banks' time is relatively infinite because deposits are a relatively stable funding source.

With its story, Brex taught all Fintech entrepreneurs in Silicon Valley a lesson: no matter how fast you are, you can't outpace the patience of capital.

The Innovator's Destiny

Brex's acquisition marks the end of an era—the romantic era that believed Fintech could completely replace traditional banks.

Looking back over the past two years: in April 2025, American Express acquired expense management software Center. In September 2025, after downsizing its consumer finance business, Goldman Sachs turned around and acquired an AI lending startup in Boston. In January 2026, JPMorgan completed the integration of the UK pension tech platform WealthOS.

It can be said that Fintech companies are responsible for the 0-to-1 stage—charging ahead, using venture capital subsidies for market experimentation, user education, and technological innovation. But once the business model is proven, or the industry enters a downturn causing valuations to回归, traditional banks appear like scavengers, harvesting the fruits of these innovations at a lower cost.

Brex burned through $1.3 billion in funding, accumulated 25,000 of the most优质 startup clients, and磨合出 a world-class financial engineering team. Now, Capital One only needs to pay $5.15 billion, a significant portion of which is in stock, to take over all of this.

From this perspective, Fintech entrepreneurs are not disrupting banks; they are working for banks. This is a new form of risk outsourcing. Traditional banks no longer need to conduct high-risk R&D internally; they only need to wait.

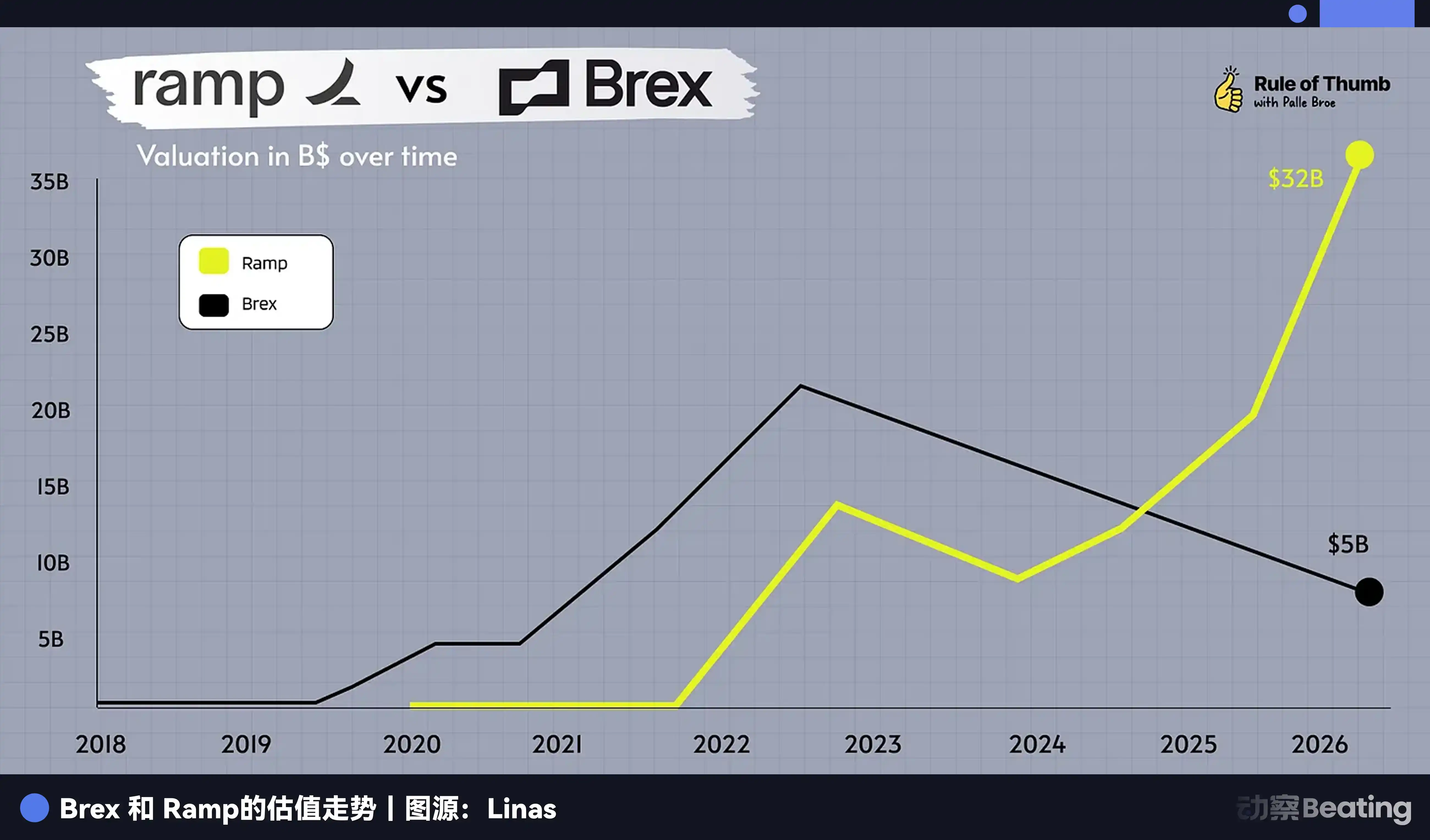

Brex's exit has pushed all the spotlight onto its competitor, Ramp.

As the only super unicorn left in the race, Ramp still appears strong. Its ARR is still growing, and its balance sheet seems more robust. But its time is also running out.

Ramp was founded in 2019. According to the VC investment cycle, it has entered its seventh year, a time when it must deliver. Later-stage investors entered in 2021-2022 at valuations above $30 billion, and their return expectations will far exceed those of Brex's investors.

If the IPO window in 2026 remains open only to a very few profitable giants, will Ramp face the same choice?

History doesn't repeat itself exactly, but it often rhymes. Brex's story tells us that in the ancient industry of finance, there is no such thing as a pure software company. When the external environment changes abruptly, Fintech's time disadvantage is exposed, and they must choose between acquisition and a long struggle. Pedro chose the former. This is not surrender; it is清醒.

But this清醒 itself is the destiny of Fintech.

Just don't forget, Brex once宣称 it would disrupt American Express, even setting the Wi-Fi password in one of its offices to "BuyAmex."