NFT市场在2021年获得了爆炸性的发展。世界上最大的NFT市场OpenSea在2021年8月实现了34亿美元的交易量。然而这一令人瞠目结舌的记录仅在短短的几个月内就被打破。

2022年1月,OpenSea达到了50亿美元/月的历史最高交易量。而伴随着用户群体和市值的飞速增长,全球NFT市场的供给端也出现了巨大的增长。

同时,据统计,在2022年1月,每周大约有20,000到50,000个NFT项目发售,每个项目通常由数千至数万枚NFT资产组成。因此当时每周实际发售的NFT数量是相当惊人的。

近乎过剩的供应,加上有限的效用,给NFT市场的发展带来了了巨大的瓶颈。

时间来到六月初,NFT在Google Trend中的搜索热度一路跌至20,相较1月创下的100峰值记录下降了足足80%。而反映在市场之上其颓势也显而易见。

据统计,NFT市场月交易量在1月达到165.4亿美元的历史新高,但在5月其交易量便跌至40亿美元,跌幅一度超过75%。

根据最新出炉的7月数据显示,诸多公链的NFT交易量也已经创下历史新低。

7月,Polygon链上NFT销售额仅为2,999,003.93美元,创16个月内新低;Avalanche链上NFT销售额仅为1,915,150.11美元,创12个月内新低;Solana链上NFT销售额仅为56,119,690.69美元,创下迄今最低纪录;以太坊链上NFT销售额仅为535,698,216.54美元,创下过去12个月的新低。

这一系列的数据似乎都在显示,NFT市场的颓势仍在延续,且正在逐步加深。但不要忘了,万事万物,物极必反,用户在长期低迷的市场氛围之下,会积攒起强烈的踏空情绪,尤其是在当前以太坊带动的二级市场相对活跃的背景之下,这种情绪会愈演愈烈。

又见百倍

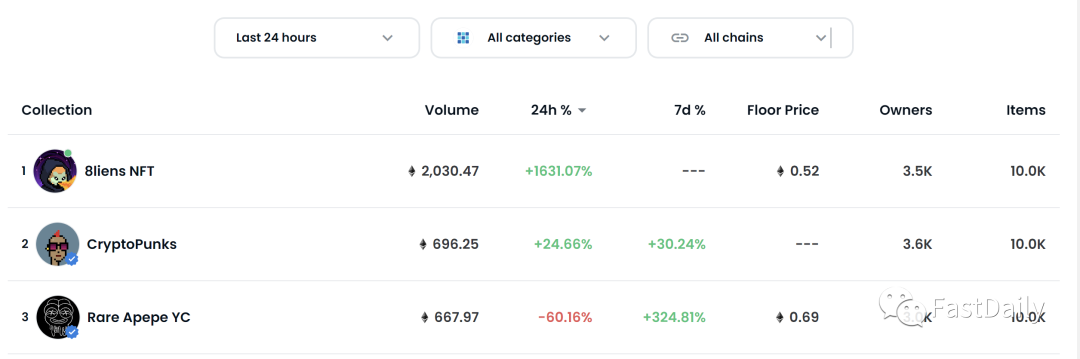

根据OpenSea的最新数据显示,8liens系列NFT在近24小时的交易额达2030.47枚ETH;经计算,其24小时的交易额增幅高达1631.07%,排名更是位列OpenSea第一位。

该NFT项目目前的地板价为0.48 ETH,24小时内涨幅高达167.34%,虽然在绝对数值上并不算太高。但8liens采取了时下流行的free mint模式,这意味着其除了Gas费之外,几乎不存在任何经济成本,从成本收益比的角度来看,它无疑是一桩不错的买卖。

8liens的异军突起不禁令人想起昨天刚刚介绍的千倍项目DigiDaigaku。希望进一步了解的小伙伴可以去看一下下面这篇文章,在这里我就不再过多赘述了。

一天千倍,牛回速归?

Free mint,势不可挡?

DigiDaigaku和8liens之间最大的共同点就在于两者都采用了free mint模式,该种模式最大的特点就在于零成本(除Gas费之外)。这意味着用户可以在规避风险的同时,保证对项目的高参与度,从而实现以小博大。

但Free mint模式本身其实并不算是创新,早在2017年6月,NFT“双王”之一的CryptoPunks就以Free Mint的形式正式推出。不过此后,由于市场整体的fomo情绪,绝大多数项目出于资金和盈利层面的考虑还是选择了有偿铸造以及白名单模式。

说起白名单,NFT玩家们可以说是怨声载道。从前期的拉人头;到后期做各种复杂的列表活动;再到后来创作表情包、地标打卡拍照等,NFT玩家逐步沦为项目方的忠实“舔狗”,而这一切却只为那几个充满变数的白名单。

其实从现在的角度来看,白名单这种营销模式实际上是一种完全由项目方主导的中心化营销套路,它不仅与公平、自由、自治等关键词南辕北辙,其愈发复杂的模式和愈发有限的收益也令大量NFT玩家叫苦不跌。

因此,在玩家的心底,其实早就萌发了更换全新模式的种子。因而,哥布林伴随着Free Mint的出现可谓是众望所归,所以不出意料哥布林势如破竹,其一经推出当即点燃了冷寂的NFT市场。同时在哥布林的带动之下,Free Mint项目也如雨后春笋一般蓬勃涌出,甚至一度出现了不少百倍、千倍项目。

Free mint的困境和未来

即便Free Mint已经逐渐成为当下NFT市场的一种全新范式和趋势,但我们依旧无法否认当下的市场环境依旧极为糟糕,人们愈发失去对长周期项目的持有耐心,操作策略也开始转变为以快打快收的节奏为主。同时,熊市中的玩家们愈发冷静和理智,他们需要更多的用例和叙事。因此,现如今的项目,即使采用了Free Mint的形式,想要取得成功也绝非易事。

当然,选择了Free Mint形式的项目比起付费Mint项目在启动阶段明显更具优势,因为其门槛更低,因此整个沉浸过程也必然更加丝滑。但相应的,这种项目通常非常容易陷入死亡螺旋。

众所周知,NFT一直是一种注意力经济,没有热度就意味着死亡,在当下的环境中更是如此。因此,在NFT售罄后,项目方如果无法快速交付全新的内容,而使项目陷入应用或玩法的真空期,投资者就会趋向于快速抛售变现。

这时NFT的地板价就会面临被砸穿的风险,一旦地板价不保,项目前期积攒的人气也将快速消失,同时丧失市场的流动性。而流动性的消失则意味着后续的版税收入将化为泡影。

作为free mint项目,失去版税收入几乎就意味着失去了一切的资金来源,运营、宣发、叙事将无从谈起,一旦走到这一步项目的死亡或许只是或早或晚的事。

除此之外,Free Mint项目还不得不面对收入来源不稳定的残酷现实。Free Mint项目本身并不会给项目方带来任何初始收入。在售罄后,无论是打算以获取版税为主要收入来源,还是希望通过新概念、新花样让投资者买单,项目方都需要一直维持足够的热度。

但与项目方诉求的矛盾在于,在当前的市场环境下,投资者们普遍倾向于快速套现离场。俗话说的好:一个要走的男人,是怎么都留不住的。因此,要通过怎样的手段留住用户的心对项目方而言无疑是一个重大考验。

![Assessing Sonic’s [S] 12% price drop and why more selling may be next](https://d1x7dwosqaosdj.cloudfront.net/images/2026-06/161e3d66eea4402796d2e6a66d93d453.jpg)