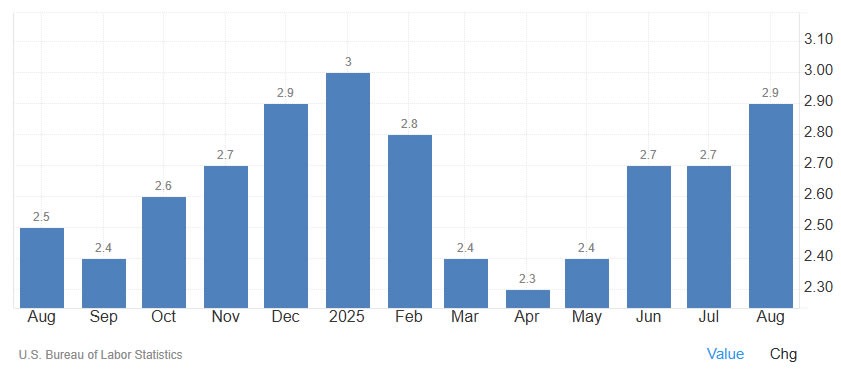

Наблюдатели за криптовалютным рынком внимательно следят за отложенным отчетом по инфляции в США за сентябрь, который, как ожидается, будет опубликован в пятницу. Предполагается, что он впервые в 2025 году превысит 3%, что может оказать негативное влияние на криптовалютный рынок.

Бюро статистики труда США планирует опубликовать индекс потребительских цен (ИПЦ) за сентябрь в пятницу. Публикация отложена из-за продолжающейся приостановки работы правительства, которая длится уже 24 дня.

По данным Trading Economics, экономисты прогнозируют, что инфляция в сентябре вырастет на 0,4% в месячном исчислении и на 3,1% в годовом исчислении. Таким образом, это будет первый раз в 2025 году, когда общий ИПЦ превысит 3%.

Публикация данных по ИПЦ может повлиять на криптовалюты

Отчет по ИПЦ станет первой крупной публикацией данных после приостановки работы правительства США в ближайшее время.

Инвестор Тед Пиллоуз заявил, что если ИПЦ составит 3,1% или выше, вероятность снижения ставки может снизиться, но если он составит 3% или ниже, «это будет хорошо для рынков».

Аналитик Ash Crypto согласился с ним, заявив, что значение выше 3,1% будет медвежьим для рынков, «поскольку это будет самый высокий показатель ИПЦ с июня 2024 года».

Значение около 3,1% будет соответствовать ожиданиям, но ниже 3,1% - «идеальный сценарий для рискованных активов».

«Снижение ставок произойдет, и рост ИПЦ в месячном исчислении составит всего 0,1% или 1,2% в годовом исчислении. Это также увеличит вероятность дальнейшего снижения ставок и приведет к притоку ликвидности в рискованные активы. Мы понимаем, что ФРС заявила, что сейчас сосредоточена на ситуации с занятостью, но то, будут ли завтрашние данные по ИПЦ сильно отличаться от ожиданий или нет, все равно может повлиять на их решения, - заявил агентству Bloomberg Мэтт Мейли, главный рыночный стратег Miller Tabak. - Таким образом, если данные действительно не соответствуют консенсусу, они все равно окажут серьезное влияние на рынки».

Однако, по данным Barron’s, более высокие, чем ожидалось, показатели инфляции вряд ли удержат Федеральную резервную систему от снижения ставок.

Центральный банк больше сосредоточен на ослаблении рынка труда, и, согласно прогнозам рынков фьючерсов CME, вероятность снижения ставки в следующую среду составляет 98,3%.

Однако продолжающаяся приостановка работы правительства может осложнить экономическую ситуацию в преддверии декабрьского заседания ФРС, на котором ожидается очередное снижение ставки.

Ожидается, что инфляция в США снова вырастет. Источник: Trading Economics.

Рынки демонстрируют незначительный рост

На сегодняшний день капитализация рынка криптовалют выросла на 1,8%, достигнув 3 800 000 000 000 долларов.

Лидером роста стал биткоин, который в конце торгов в четверг кратковременно поднялся выше 111 000 долларов, а затем на момент написания статьи упал до отметки 110 500 долларов.