以太坊上的「meme飞轮」骤然崩塌

自今年 6 月上旬至 7 月上旬,$IMF 作为以太坊主网上的 MemeFi 项目最高上涨了近 70 倍。虽然在创下 7000 万美元市值的历史新高后,$IMF 逐渐回调了 50%,但在昨天,一波最高接近 85% 的巨大下跌引起了市场的震动。

$IMF 的下跌震惊了 Zhu Su

究竟发生了什么,让 $IMF 出现了如此巨大的下跌?

什么是 IMF?

IMF(International Meme Fund)是一个为主网 meme 量身定制的去中心化金融平台,允许用户用手中的 $PEPE、$JOE、$MOG 等 meme 币抵押借出稳定币 $USDS,无需出售即可变现。同时,通过 Accelerate 和 Amplify 等模块,项目方或巨鲸还可加杠杆拉盘、循环借贷护盘,甚至制造「锁仓」假象,实则实现提前出货与影子资金管理。

通过 IMF 可以实现 meme 币的循环借贷,实现「左脚踩右脚」,比如:

· 买入 1 万美元 PEPE

· 将 PEPE 存入 IMF,并借出 5000 美元 USDS 贷款

· 将 USDS 换成 PEPE

· 将剩余的 5000 美元 PEPE 存入以降低贷款价值比(LTV)

目前,IMF 的 TVL 仍有约 1.665 亿美元,总共有约 5400 万美元的 $USDS 存入,有约 2922 万美元的 $PEPE、约 2058 万美元的 $stETH、约 4440 万美元的 $MOG、约 588 万美元的 $JOE、约 494 万美元的 $SPX 和约 750 万美元的 $IMF 作为抵押物。

$IMF 为什么暴跌?

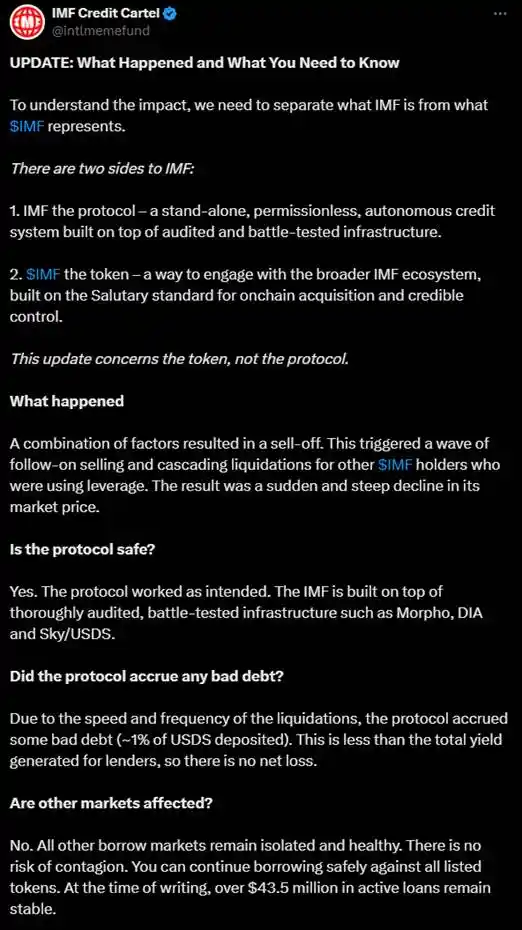

根据 IMF 官方发布的推文,这次 $IMF 突发的暴跌不是因为协议本身出现了问题,而是因为 $IMF 这个代币本身遭遇了抛售,而抛售引发的更多恐慌抛售以及连环清算导致 $IMF 的价格出现了大幅的下跌。

官方还在推文中表示,由于清算的速度和频率,累积了一些坏账(约占存入 USDS 的 1%)。这低于贷款人产生的总收益,因此没有净损失。此外,$IMF 借贷市场发生的问题也不影响平台上其它的借贷币对。

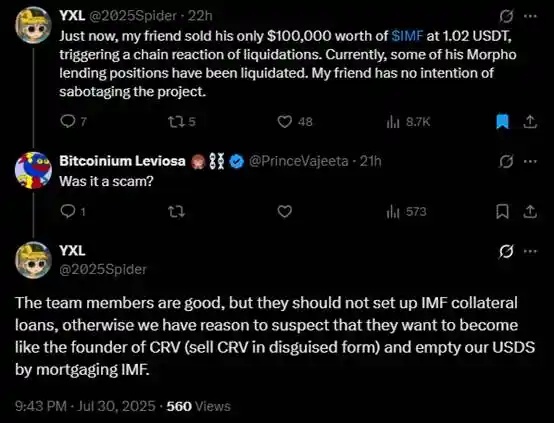

@2025Spider 发表推文称,他的朋友以 1.02U 的价格卖掉了价值 10 万美元的 $IMF,从而引发了连环清算。他表示,他的朋友无意破坏 IMF 项目,并表示项目方应该平仓 IMF 借贷仓位,否则 USDS 会面临巨大风险。他还表示团队的预言机更新速度很慢,当大多数 IMF/USDT 仓位已无力偿债时,预言机仍然没有及时更新到最新的价格。

对于 IMF 开放自家平台币 $IMF 的抵押借贷这件事情,@2025Spider 与华语 KOL「梭教授说」都提出了质疑:

有人在 @2025Spider 的推文下问他,「IMF 是骗局吗」?@2025Spider 表示,团队成员是好的,但是不应该开放 $IMF 的抵押借贷,否则就有理由认为他们想和 CRV 创始人那样通过变相卖出自家代币套现。他还表示,开给 $IMF 的贷款额度超过了 $IMF 的 UniSwap 池子本身,从风控的角度来说这也是不应该的

「梭教授说」则是通过链上的记录,更直接地质疑 IMF 团队自己抵押引发 FOMO 然后自己卖出代币套现:

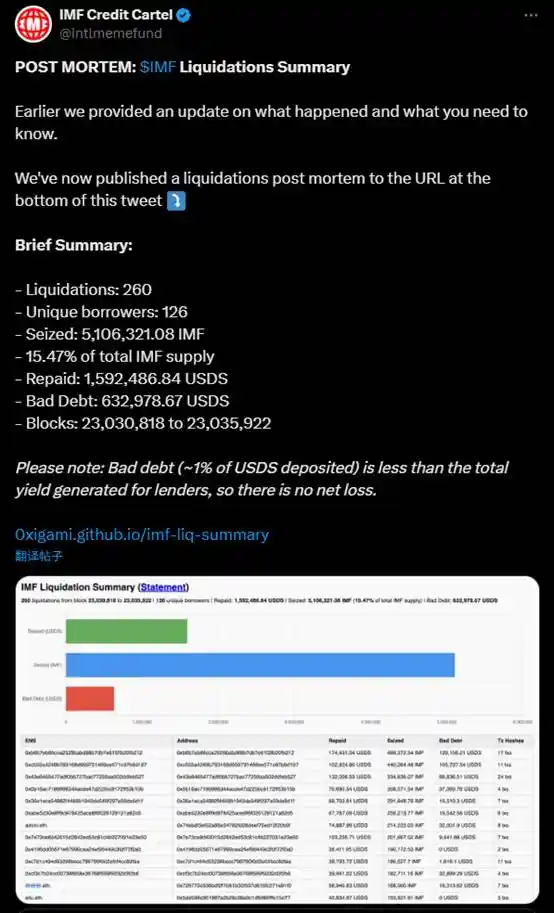

IMF 官推在今天下午发表了该次连环清算事件的详细报告。总计有 260 笔清算,涉及 126 个独立借款人,占 $IMF 总供应量的 15.47% 被清算。

结语

事件发生后,$IMF 从最低点一度反弹近 4 倍,目前相较于最低点仍有接近 3 倍的价格,市值回升到了近 2100 万美元。

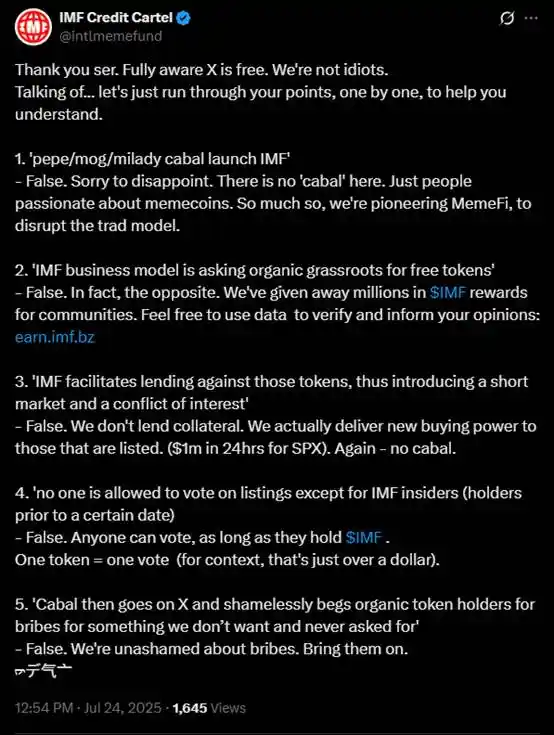

不过,伴随着 $IMF 的争议恐怕并不会结束。在 7 月 24 日时,以太坊上知名 meme 币 $APU 的大户 @alex_eph612 就对 IMF 开炮。他表示,IMF 是 $PEPE、$MOG 和 Milady 的阴谋团体发起的,其商业模型实际上是向其它有机的 meme 币社区索要免费代币以换取 IMF 能够带来的短期买盘,然后阴谋集团再拿着代币出售:

IMF 很快对此进行了回击,声称并没有索要任何贿赂,上架借贷对的标准也是公开的并且由 $IMF 持有者进行投票:

以太坊的「meme 飞轮」,恐怕还要经受风浪。