核心要点

以太坊巨头正逢高减持,而永续合约偏向空头,这引发了清算潮,并将追高的多头困在突破点下方的反复震荡中。

以太坊 [ETH] 是否被刻意压制在 4000 美元下方?

价格走势的确呈现出一种循环模式。一方面,交易员们在提前布局突破行情。随着美联储会议(FOMC)临近,波动性备受关注,这势必将考验比特币 [BTC] 的主导地位。

另一方面,市场对 “现货买入后紧接着大举加空” 这一重复模式的担忧日益加剧。到了这个阶段,我们看到的是否是一种即便面对宏观催化剂也不为所动的协同操纵?

以太坊的震荡区间并非随机,而是人为设计

自 7 月 21 日以来,以太坊 ETF 已吸引近 19 亿美元资金流入。与此同时,交易所储备从 890 万枚 ETH 降至 870 万枚。

仅通过现货渠道就形成了 20 万枚 ETH 的供应紧缩,ETF 需求持续吸纳流通筹码。然而,以太坊仍未能突破 4000 美元关口,截至发稿时跌至 3871 美元。

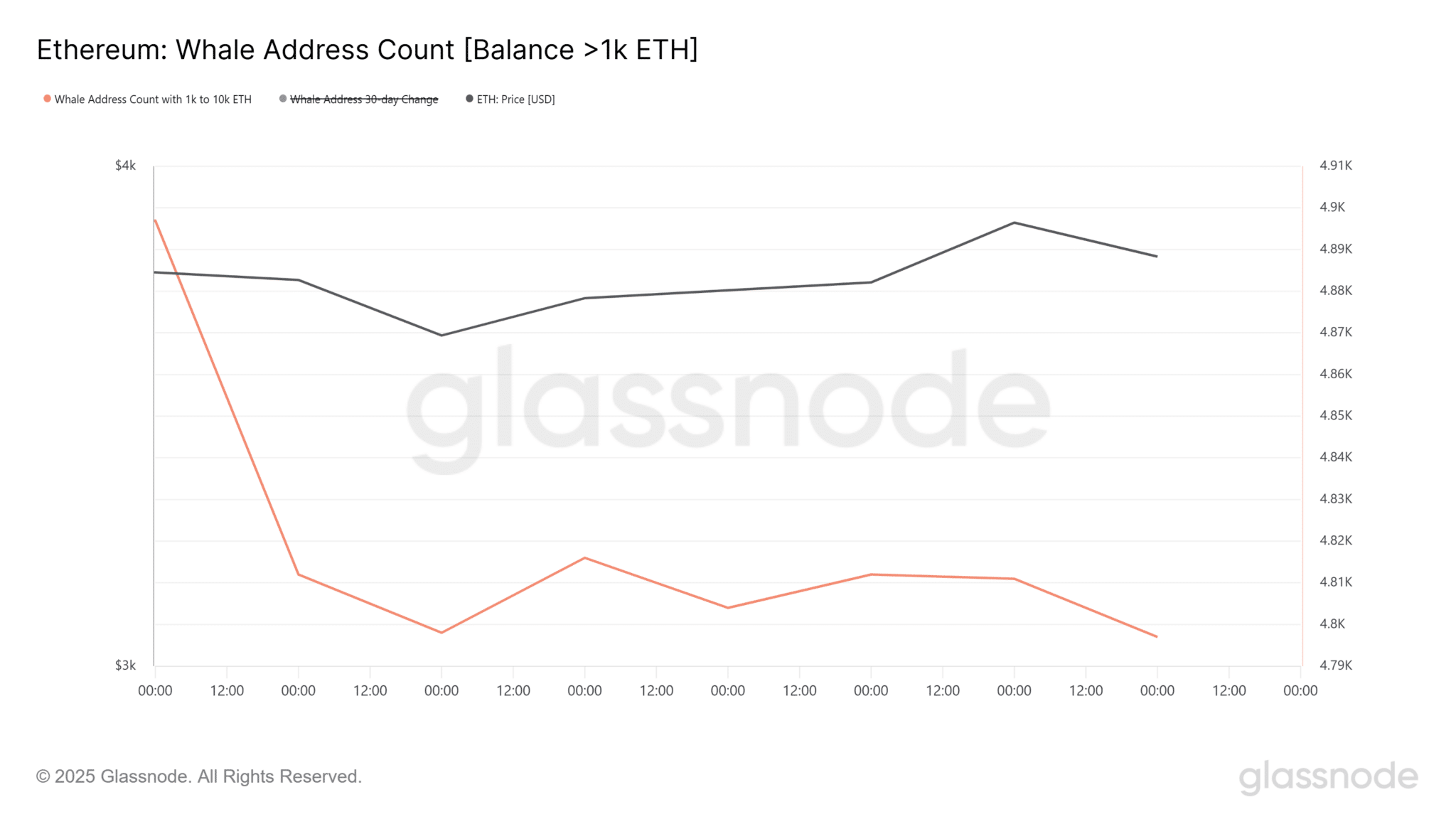

此外,持有 1000 枚以上 ETH 的巨头钱包数量从 4897 个降至 4797 个,过去七天净减少 100 个高净值持有者。

来源:Glassnode

再加上币安平台 - 0.21% 的周资金费率,各种信号开始相互印证。巨头逢高减持,而永续合约净空头持仓增加?这是一场协同进行的平仓行动。

随之而来的是 “收获时刻”。短短 24 小时内,超过 1 亿美元的以太坊多头头寸被平仓,引发的连锁反应让激进的空头轻松获利。

简而言之,在高位派发筹码会困住追高的多头。价格加速下跌,而精明资金则收割利润。结果就是,以太坊陷入流动性争夺与突破失败的循环中。

以太坊徘徊于宏观波动性边缘

以太坊目前仅比 4000 美元突破区间低 3.3%,随着美联储准备公布下半年政策,宏观催化剂再度发力。

以太坊多头正提前布局轮动行情,尤其是 ETH/BTC 日内上涨 1.4% 的情况下。比特币 dominance(BTC.D)在本周触及 62% 以上后回落至 61.25%,这进一步为以太坊添力。

再加上不断上升的现货需求和稳定的机构资金流入,市场结构似乎已为突破做好准备。但突破 4000 美元与站稳该价位是两码事。

来源:TradingView(ETH/USDT)

如果精明资金故技重施(逢高派发并在高位加空),4000 美元附近的局部高点可能引发又一轮多头清算潮。

从表面上看,以太坊似乎在搭建起飞的平台。但深入来看,巨头们并未增持。如果这种买盘迟迟不出现,以太坊可能会在阻力位遭遇第三次 rejection。