地缘政治紧张局势于周末进一步升级,美军轰炸机对伊朗境内三座深层核设施发动迅速且精确的打击。美方报告称,设施损毁严重,惟尚未得到官方证实核材料是否已被摧毁或事先撤离。

市场本能地抛售风险资产,而加密货币作为唯一周末持续交易的资产类别,自然首当其冲,攻击刚开始时 BTC 自 102 k 以上回落约 4% 至 99 k 左右。须留意的是,在传统金融投资者眼中,加密货币仍持续被视为前沿/高风险资产。

由于局势升级,市场原本担忧周一开盘将出现剧烈风险反应,惟此类疑虑在亚洲早盘已快速消散,市场上逐渐浮现一种观点,认为此番行动或许代表一次成功的「以升级换降温」(escalate to de-escalate),即透过关键的武力展现来推动谈判进展。此外,封锁荷莫兹海峡的实际困难(伊朗石油与天然气出口大多流向中国)也让市场对油价失控飙升的担忧有所缓解。

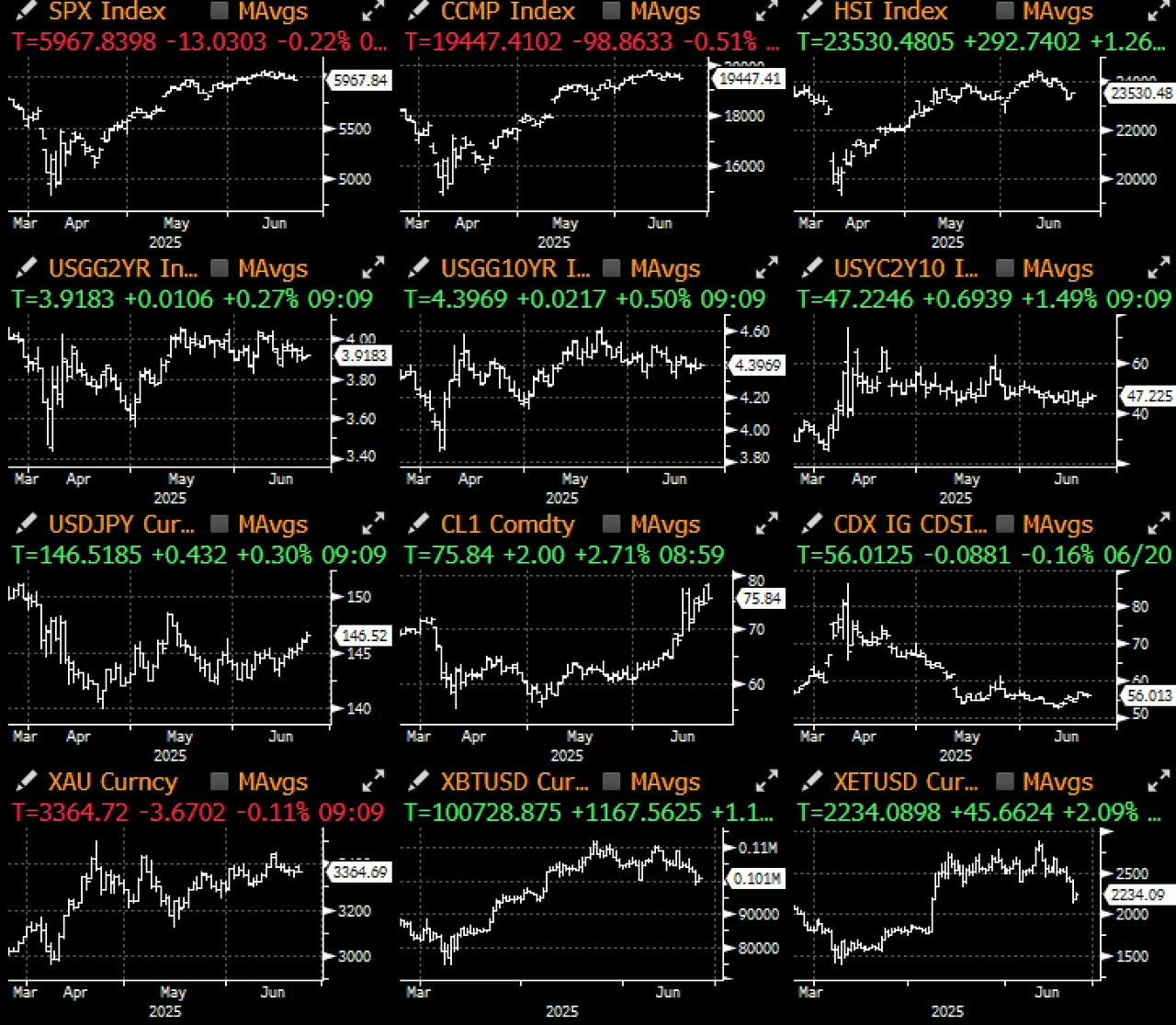

周一早盘的价格表现似乎也印证此观点,美股期货几乎已回升至上周五的水平,油价稳定在每桶约 75 美元,现货黄金回吐了此前涨幅,美元兑以色列新谢克尔也已回落至冲突前低点。

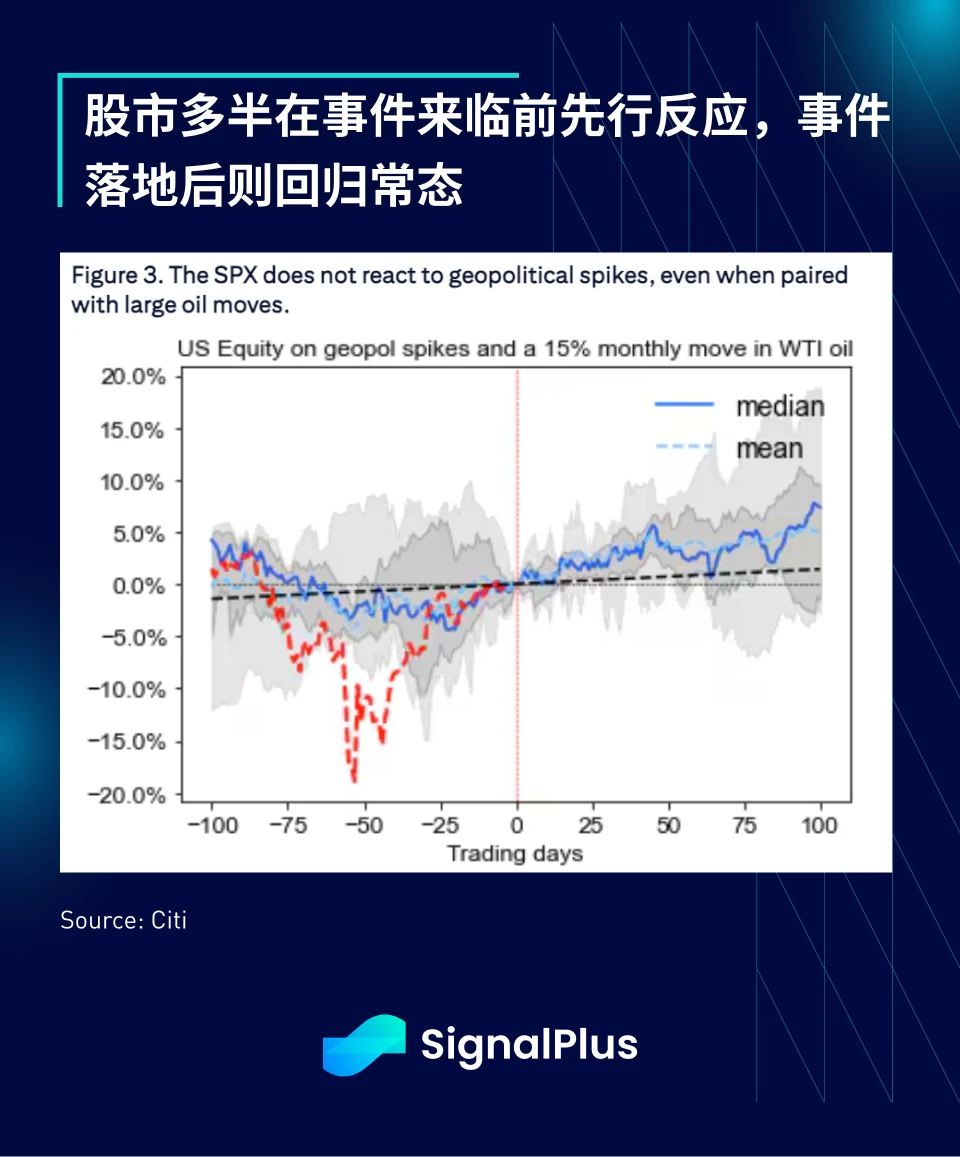

一般而言,地缘政治压力往往是短暂的,对股市也只有暂时性的影响。花旗近期一项研究显示,SPX 指数往往会在地缘政治事件风险升温前出现负面反应,但一旦事件实际发生,表现通常不差。若我们相信股市具有一定效率,且能够前瞻性地反映已知与可预见的未知风险,这样的结论便合情合理。除非出现难以想像的大规模毁灭性武器攻击或其他极端突发事件,否则我们预期风险市场将逐渐适应此轮冲突,并重新聚焦于正在进行的关税谈判与经济发展上。

在利率市场方面,尽管市场对美国巨额利息支出与潜在通胀风险的讨论不断,但利率隐含波动率已回落至中期低点,显示市场并不预期已开发国家央行将有实质行动,整体远期利率轨迹亦维持稳定,债券交易员已重回常态操作。

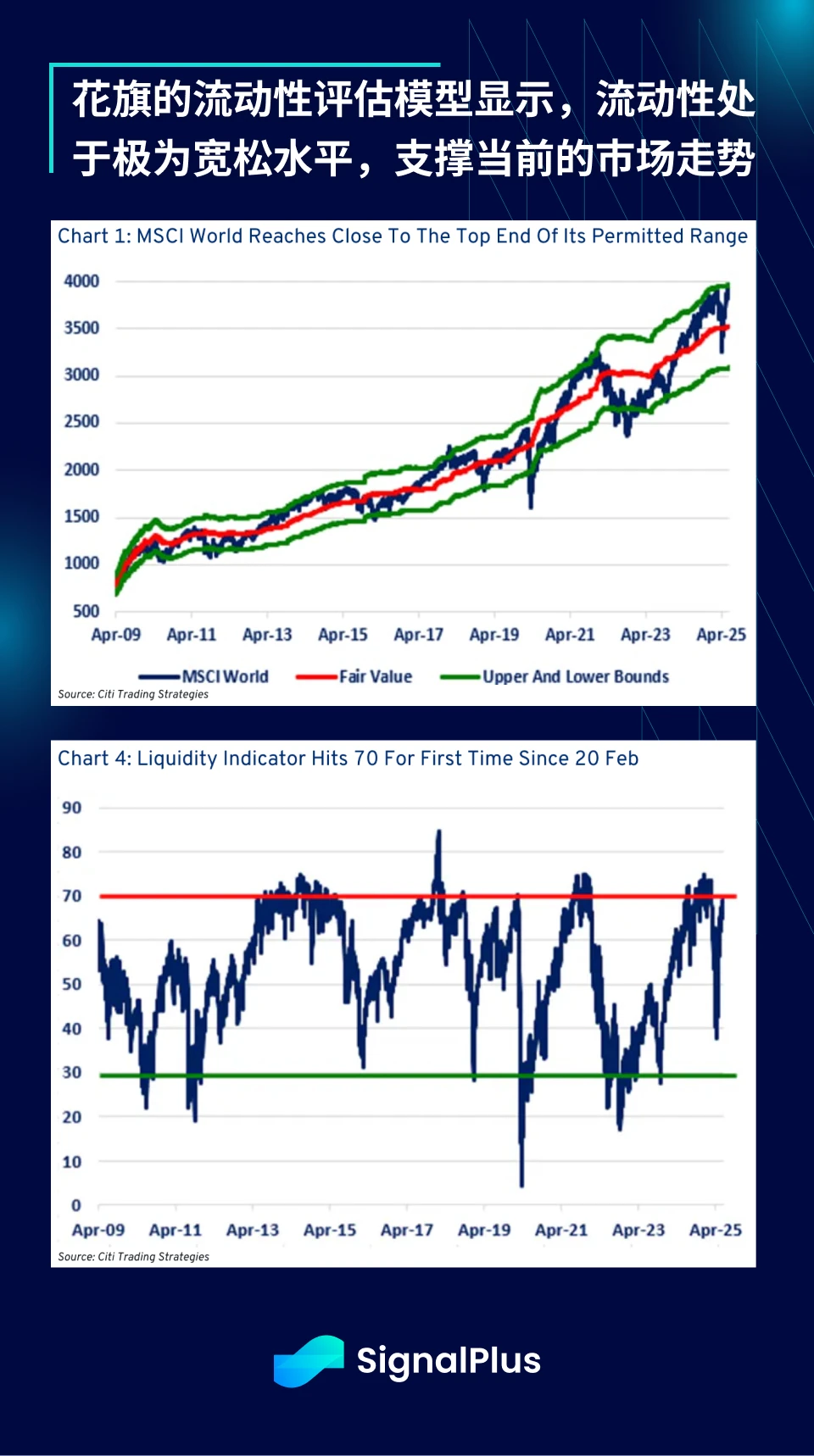

与此同时,根据华尔街多数观点,目前市场流动性(即金融形势)仍相当充裕,使得风险资产(例如股票)得以持续攀升「忧虑之墙」,即便经历了解放日、持续的俄乌冲突与以伊紧张局势,SPX 指数仍能强劲回升。

尽管宏观观察人士可能仍长期抱持悲观立场,投资者却以实际资金投票,在各种预警声中,风险情绪仍明显偏多,整体经济亦持续运转,企业盈利稳步上升。

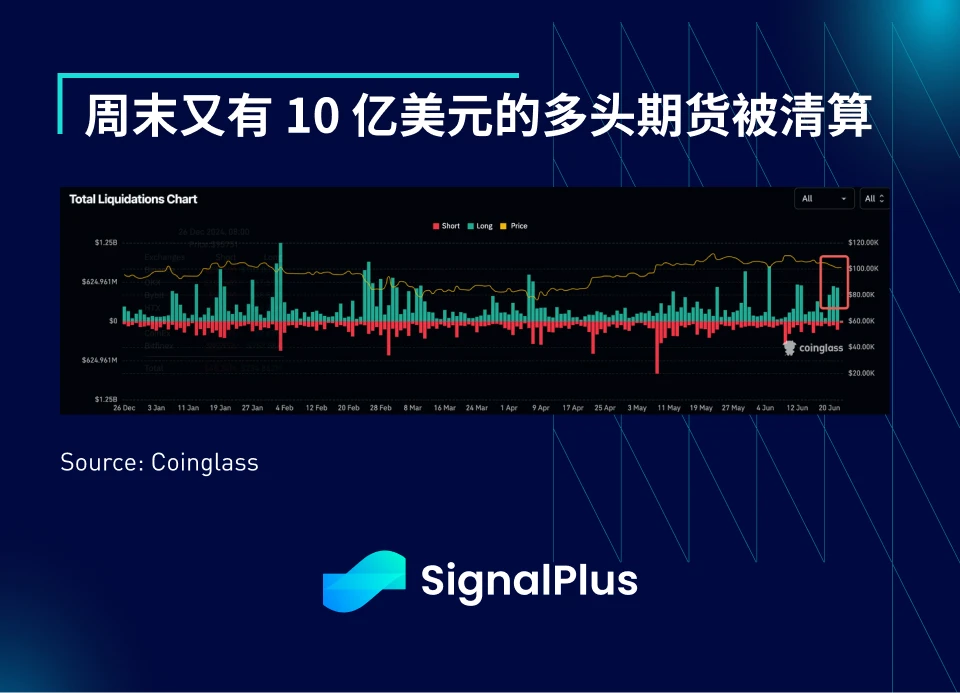

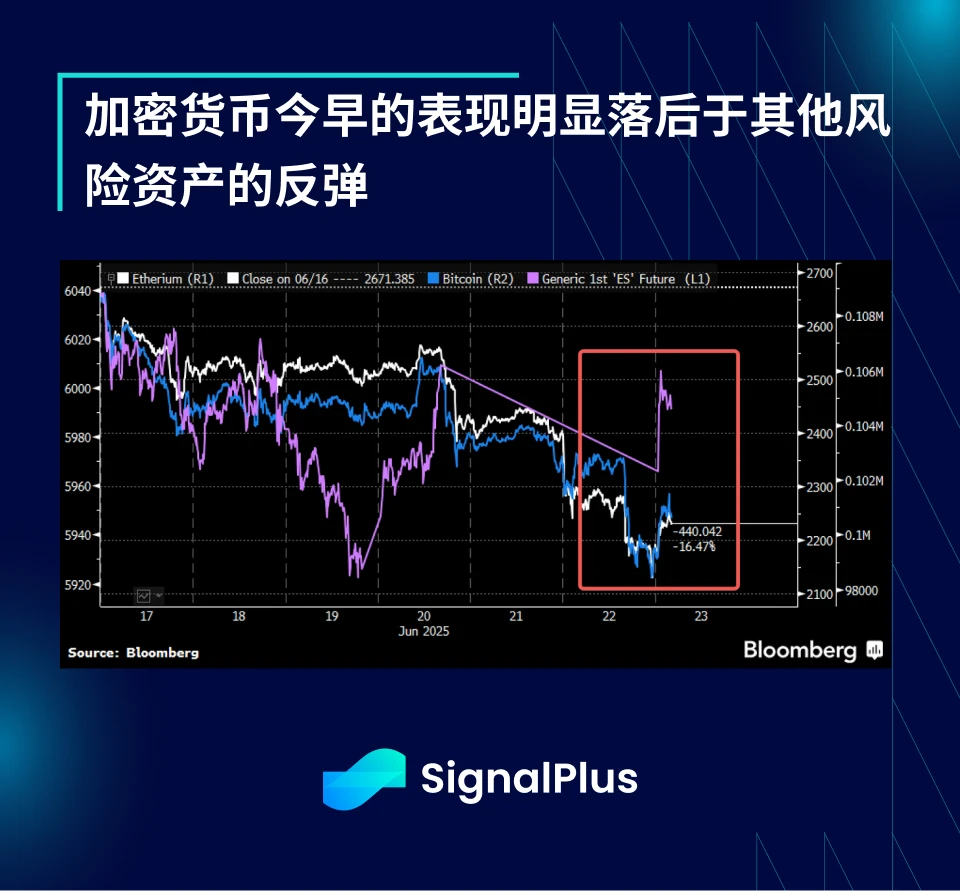

可惜的是,加密货币市场并非如此。BTC 下跌 4% ,触及 98.9 k 美元附近,而 ETH 则大跌约 10% 至 2, 150 美元,创下自 5 月初以来最低的盘中价位。随著伊朗空袭消息传出,加密货币作为唯一仍在交易的资产,自然遭到抛售,周末期间有超过 10 亿美元的期货部位遭到清算。

尽管股票、原油与黄金价格在早盘已扭转周末走势,加密货币价格却难以同步反弹,投资者在冲突发生时仍处于多头部位,且过去一个月帐面波动剧烈,而加密货币价格自第一季度以来始终无法有效突破,BTC 也难以突破 2 月份的高点。

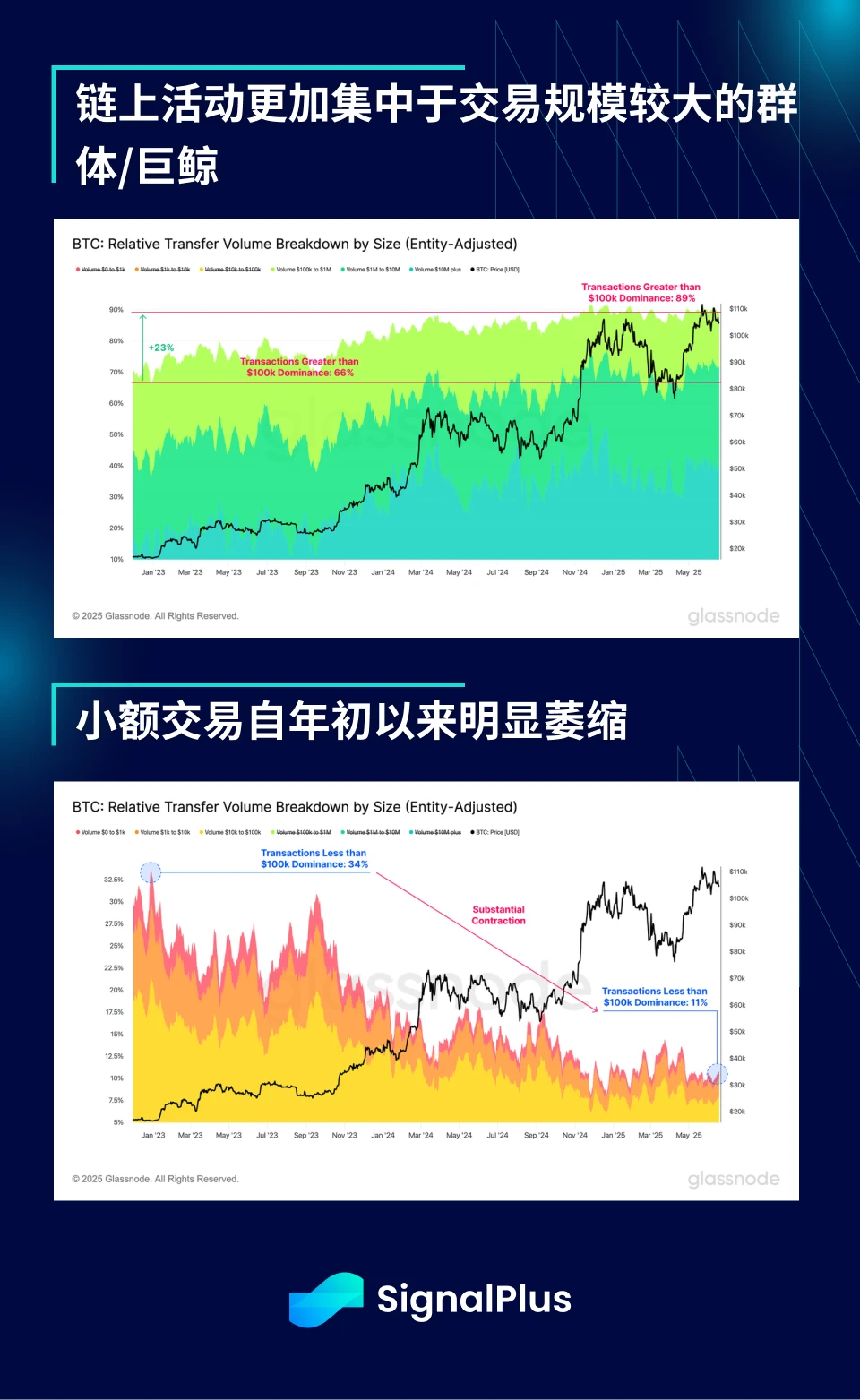

Glassnode 上周进行了一项出色的分析,显示尽管 TradFi 社群对 BTC 表现出浓厚兴趣,链上交易活动却已显著放缓。简言之,由于主流投资者试图透过传统工具(例如 ETF、期货)获取 BTC 敞口,链下场外(OTC)交易活跃,然而自 FTX 以来,链上活动并未恢复,这从 DeFi 与 Altcoin 表现低迷以及新叙事(除稳定币/RWA 外)乏善可陈的现象中可见一斑。

同样地,幂律分布现象在加密货币领域也愈发普遍,一方面,BTC 的市值主导地位持续上升,另一方面,其自身的链上转帐活动也愈发集中于大型钱包。根据 Glassnode 的数据,单笔金额超过 10 万美元的交易占比已从 2022 年的 66% 上升至今日的 89% ,进一步证实了「巨鲸」主导市场的观点,而小型帐户在市场上的影响力与参与感也越来越低。

不幸的是,随著加密货币行业日益成熟并加速机构化,这一趋势很可能会持续下去,这或许是无可避免的结果。

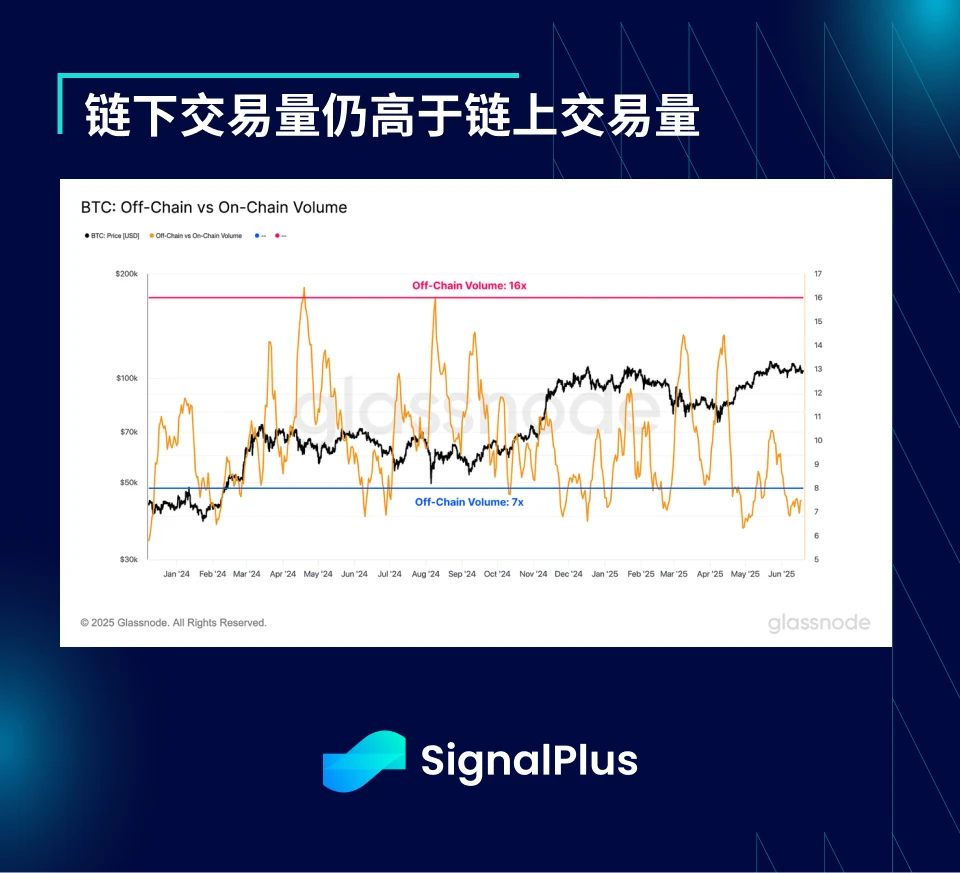

此外,随著 BTC 成为主流资产类别,自然也必须遵循其他宏观资产的运作规则,也就是由资金体量最大的参与者所主导,链下交易远比链上交易活跃。长期观察者指出,本轮周期与过往不同,缺乏 altcoin 热度或新叙事的崛起,但这其实早就在预料之中,TradFi 参与者更倾向透过他们熟悉的工具(链下)参与市场,自主托管与链上叙事对此族群而言吸引力有限,然而,由于他们拥有的资金规模远大于原生用户,他们的行为与偏好将越来越主导价格走势。

这种宏观相关性的变化,可以通过 BTC 期货未平仓量的大幅增加来观察,自 2024 年第四季度以来,BTC 期货未平仓量的急剧变动正是我们更频繁看到清算缺口(如上周末)的主因。链下活动与期货驱动的价格变动意味著更高的宏观相关性,加密货币原生动能的影响更加薄弱。

与此同时,本轮周期中加密货币期权交易活跃度也显著上升。整体市场每日交易量从 2024 年的 15 亿美元攀升至近期高点 50 亿美元,显示日益成熟的市场参与者采用更多期权策略来管理风险。欢迎持续与 SignalPlus 团队联系,我们将竭诚协助您探索更多期权策略应用!

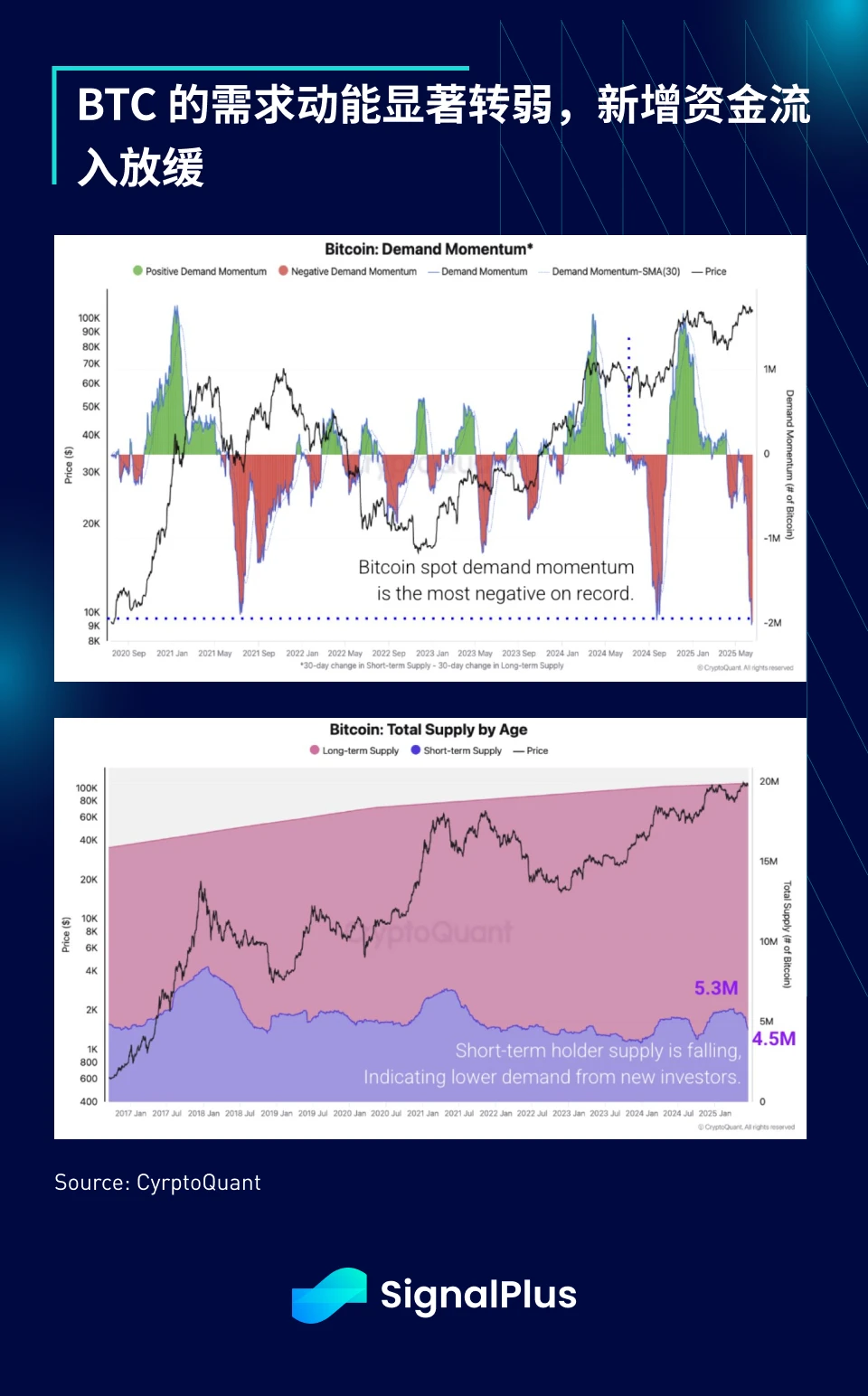

回到当前时点,BTC 的需求动能似乎显得疲弱。根据 CryptoQuant 的数据,其需求动能指数创下历史低点,即使市场拥有一连串利多政策(如 Genius Act、香港稳定币政策等),价格依旧无法有效突破先前高点,短期持币者(即新资金)供给似乎正在放缓。

波动率市场方面,价格变化显示交易员对这次波动措手不及,隐含波动率自此前单边下行趋势中突然飙升。看跌期权出现显著买盘,尤其是 ETH,显示市场参与者在持有多头 delta 的情况下寻求下行保护,短期内市场可能还有进一步下行压力。

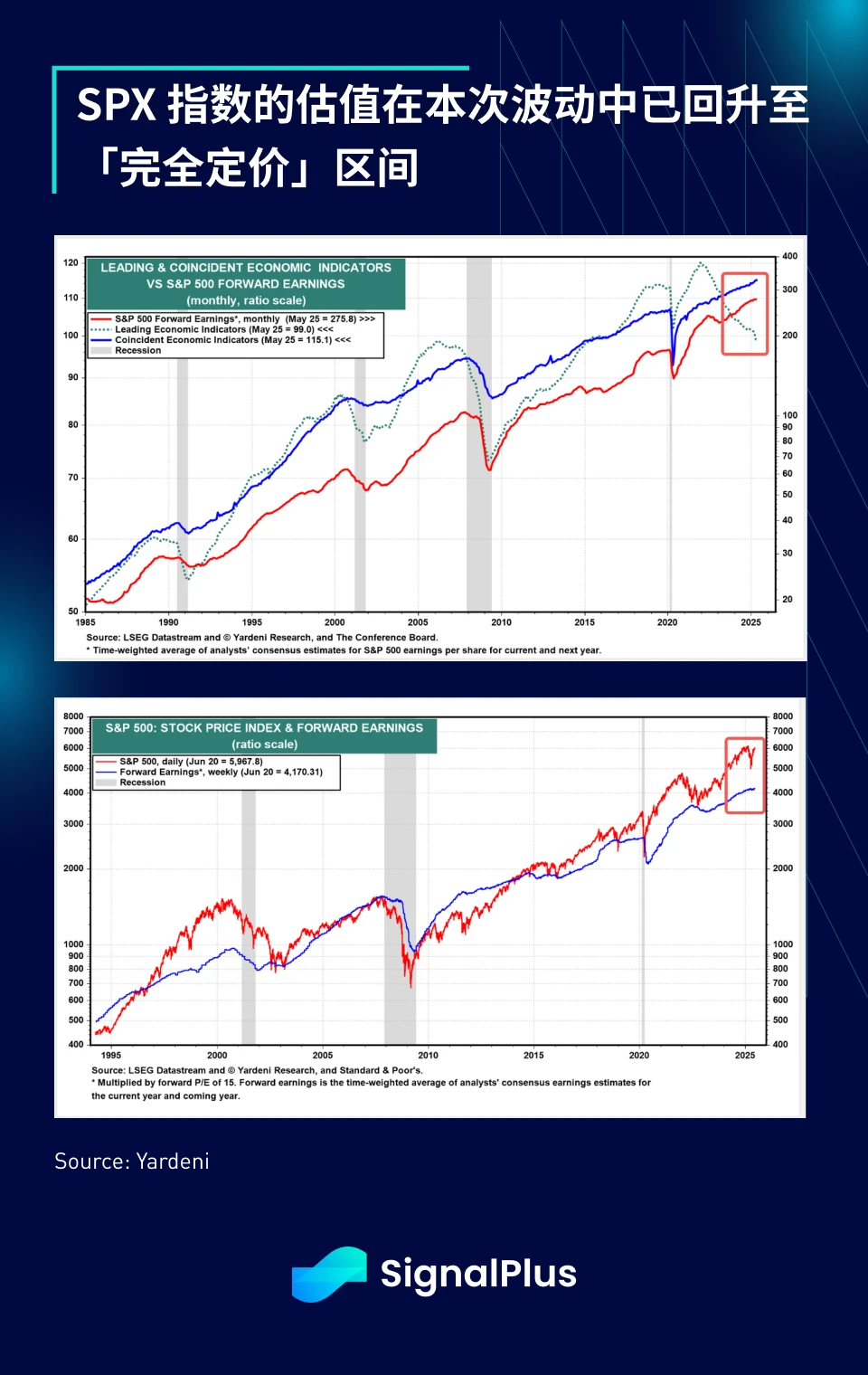

展望未来,我们认为市场将很快消化并走出此次地缘政治事件,甚至可能看到俄罗斯与伊朗局势都出现某种和平突破,以及关税谈判的实质进展。市场自然会因这些进展而上涨,但届时焦点也将重新回到高估值问题上,目前 SPX 指数已经反映 + 12% 的盈利增长预期至 296 美元(相当于 20 倍远期市盈率),然而美国经济实际上似乎正在放缓(就业指标、CEO 裁员预期等)。

如我们一直以来的立场,不建议逆势做空当前股市上涨趋势,但相信此波反弹行情已接近尾声,现阶段更应聚焦于降低风险。在加密货币市场方面,鉴于近期价格表现,我们更担忧市场可能出现更大幅度的调整,清洗近期进场的追高资金与浮动筹码。我们亦对众多上市公司纷纷将 BTC 纳入公司持币的「财务工程」操作感到警惕,这可能反而是一种负面 FOMO 信号。

保持冷静,控制风险,愿冷静的头脑战胜当前局势。祝各位好运。

您可免费使用 SignalPlus 交易风向标功能 t.signalplus.com/crypto-news/all,通过 AI 整合市场信息,市场情绪一目了然。

如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlusCN,或者加入我们的微信群(添加小助手微信,请删除英文和数字中间的空格:SignalPlus 666)、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。

SignalPlus Official Website:https://www.signalplus.com