Падение суточного числа транзакций в сети первой криптовалюты во многом связано с обвалом нефинансовых операций и ростом доминирования крупных игроков. К таким выводам пришли аналитики Glassnode.

Despite #Bitcoin’s elevated price, a clear divergence has emerged between market valuation and network activity. In this report, we explore activity across both on and off-chain markets, and examine how network metrics have changed this cycle.

— glassnode (@glassnode) June 19, 2025

Discover more in the latest Week… pic.twitter.com/vLhL7sllKK

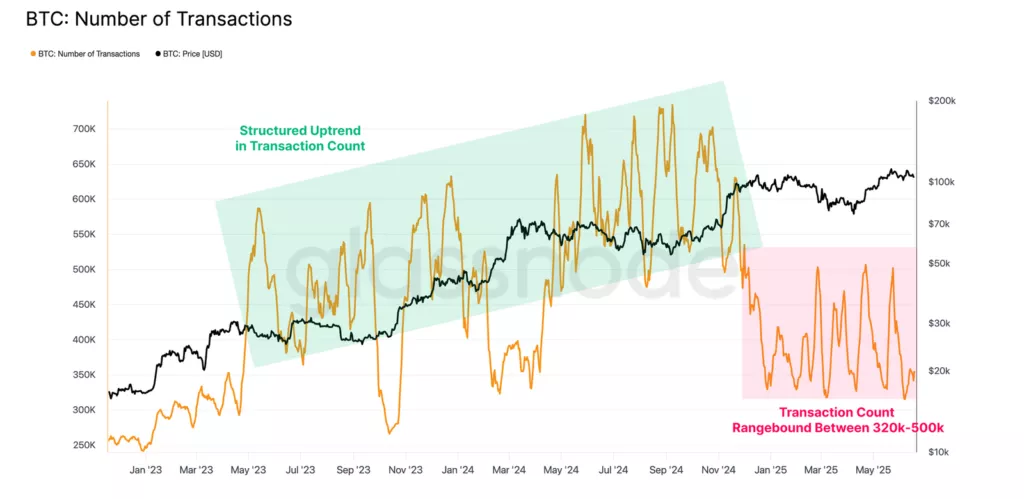

На протяжении 2023-2024 годов количество ончейн-операций в сутки демонстрировало восходящий тренд, достигнув пика в 734 000 в ноябре. После начала 2025 года показатель обвалился до значений 320 000-500 000, приблизившись к минимумам с октября 2023 года.

При этом объем ежедневно перемещаемой стоимости остается на исторически высоком уровне — $7,5 млрд в среднем.

По оценке экспертов, это свидетельствует о том, что падение числа транзакций на блокчейне связано с прекращением ажиотажа вокруг активов, выпущенных с помощью свидетельских данных Taproot (Ordinals) и полей OP_Return (Runes).

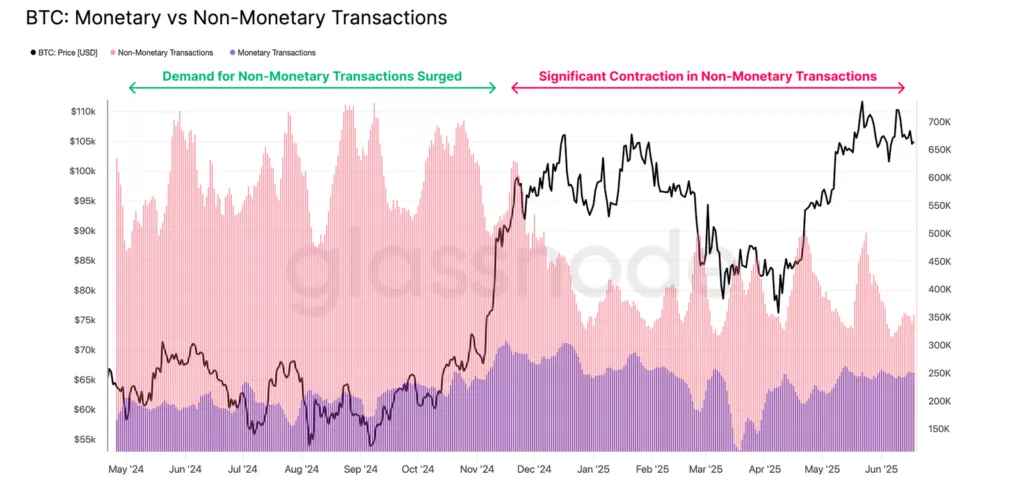

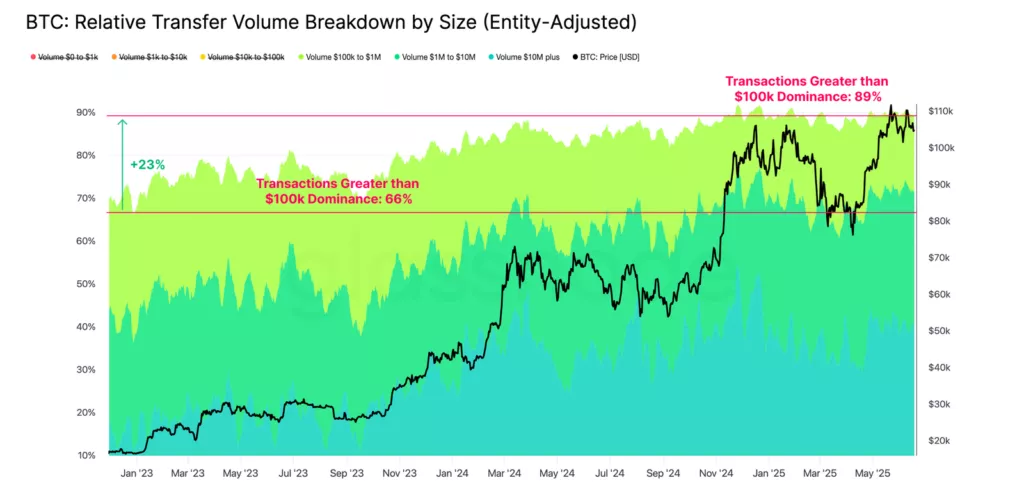

В Glassnode также отметили, что количество финансовых транзакций остается примерно неизменным, но их средняя долларовая стоимость достигла $36 200. Доля операций на сумму от $100 000 увеличилась с 66% в ноябре 2022 года до 80% на текущий момент.

Для сравнения, в декабре 2022 года на сделки до $100 000 приходилось 34% от общего количества, сейчас значение упало до 11%.

«Эта тенденция подтверждает мнение о том, что участники с высокой стоимостью становятся все более доминирующими в ончейн-активности», — подчеркнули аналитики.

Значительная часть экономики биткоина переместилась в офчейн, констатировали в Glassnode. В сегменте спотовой торговли это обеспечивают централизованные биржи. За последний год среднесуточный объем торгов на CEX составлял около $10 млрд с пиком $23 млрд в ноябре, но подобные операции чаще всего не подразумевают передачи активов в сети.

Также в текущем цикле резко выросла торговая активность по фьючерсным контрактам и опционам, а также использование кредитного плеча.

По данным аналитиков, объем офчейн-рынка биткоина регулярно превышает суммарный показатель операций на блокчейне в 7-16 раз.

Эксперты Glassnode признали, что все перечисленные тренды оказали давление на комиссионные доходы майнеров. Доля сетевых сборов в выручке уже упала ниже 1%. В июне средний показатель составил $530 000 в сутки.

Напомним, после очередного перерасчета сложность сети биткоина скорректировалась от ATH всего на 0,45%, продолжая оказывать давление на рентабельность добытчиков.