原文作者:Jake Pahor

原文编译:Frank,Foresight News

鲜为人知的是,Aave、Gyrscope 和 Beethoven X 有一个共同点:它们都有利用 Balancer 的技术堆栈,随着即将推出 V3 版本,Balancer 也可能要迎来出一些真正改变游戏规则的变量。

本文就是加密研究员 Jake Pahor 关于 Balancer 的最新报告,对 Balancer 做了详细的研究,并从使用案例、大规模采用、项目收入、代币经济学等多个角度对 Balancer 进行了深入的探究,Foresight News 对全文进行了编译。

1.概述

Balancer 的核心是一个去中心化的 AMM 协议,然而当深入研究该协议时,我们会发现 Balancer 团队正在构建一个强大的技术堆栈,以成为一个流动性中心:

正在开发新的 AMM/DEX;

收益性资产;

DAO 治理;

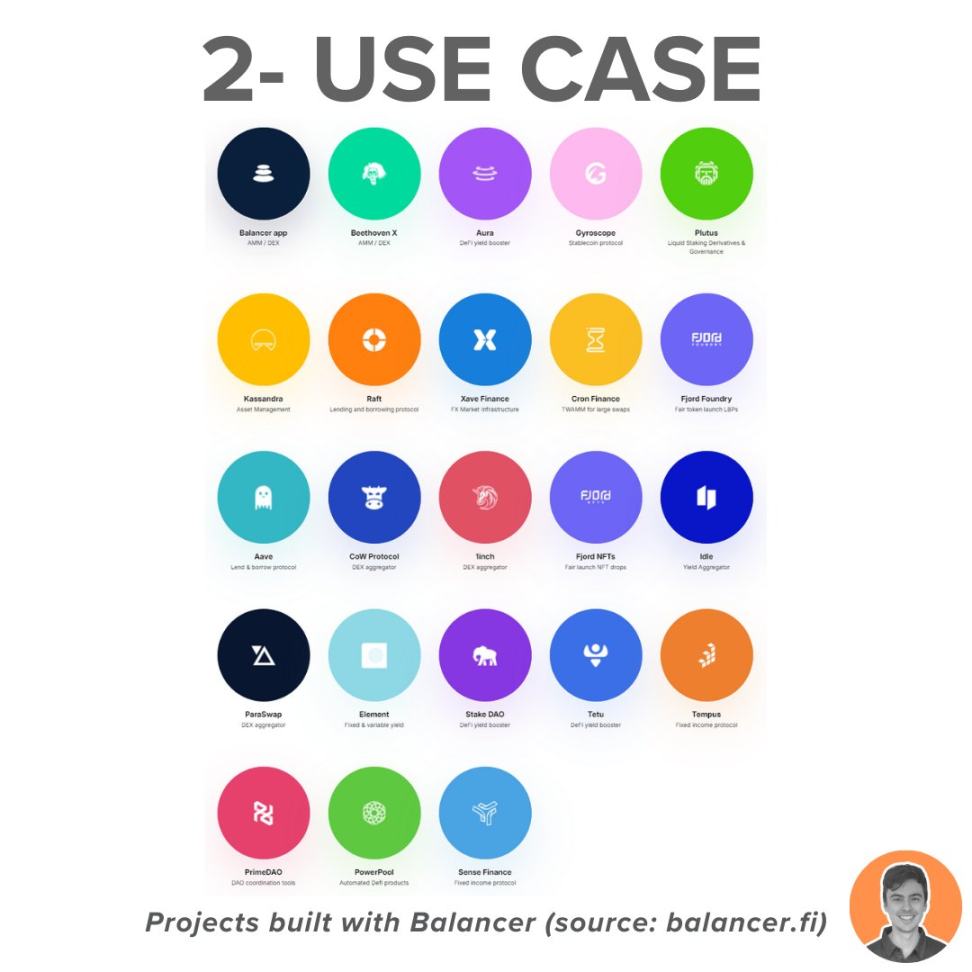

2.使用案例

Balancer 不仅是一个具有前瞻性的 DEX,也是培育未来 DeFi 创新的基础技术,其独特的架构简化了向市场提供独特金融服务的流程。

其中 Aave、Beethoven X、Radiant 和 Fjord 目前都在使用其技术堆栈。

关于 Balancer 我最兴奋的是预计今年(2024 年第 2 季度)发布的 V3 版本,它承诺以 V2 的创新为基础,推动 Balancer 成为:

DeFi 的收益承载枢纽;

创新 AMM 部署的 Launchpad;

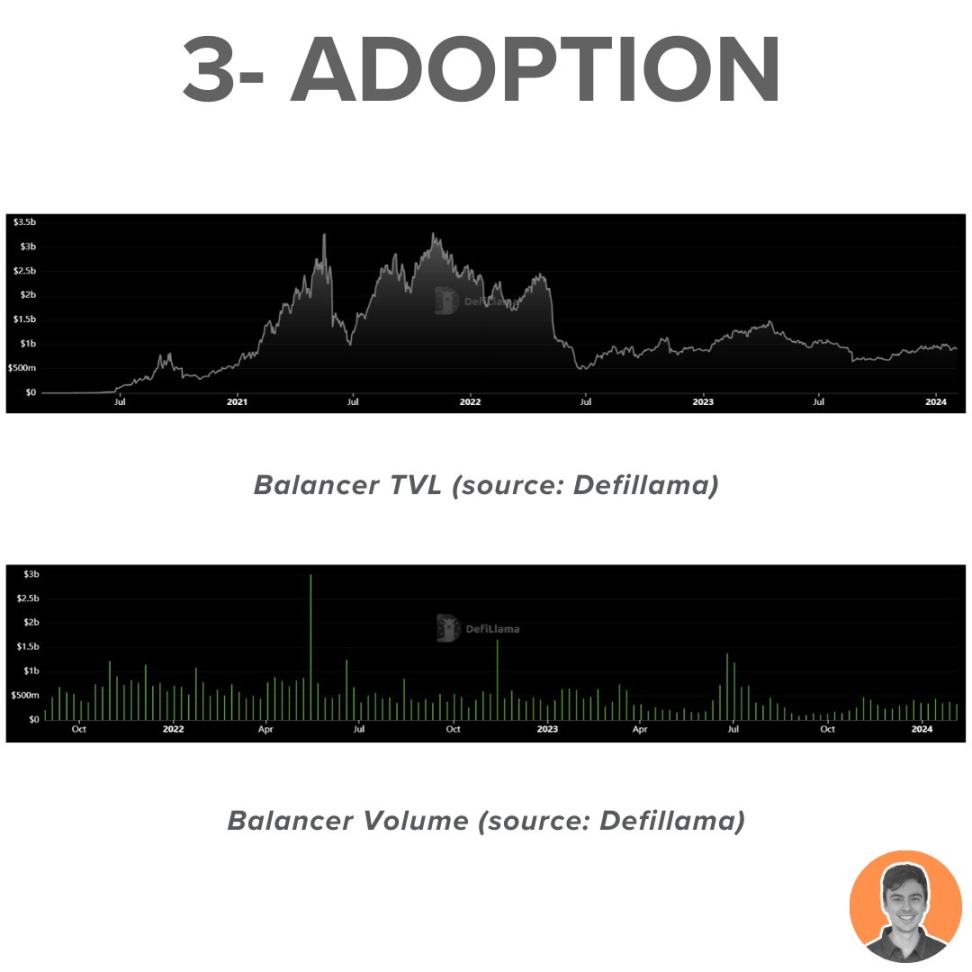

3.大规模采用

Balancer TVL 目前是 9.15 亿美元,在所有 DeFi 协议中排名第 23 位,在其他 DEX 协议中排名第 4 位。

虽然仍比 ATH(2021 年 11 月的 33.1 亿美元)低 72% ,但其 TVL 自 2022 年 7 月以来一直呈缓慢走高趋势,整体锁仓规模有着坚实的基础。

4.项目收入

在过去的 30 天里,Balancer 系统累计产生了:

150 万美元的费用;

64.9 万美元的收入;

根据 DefiLlama 的说法,它在总体 DeFi 应用中排名是第 35 ,在 DEX 中排名第 6 。截至 2023 年 8 月,该协议对非豁免池收取 50% 的 Swap 费用和 50% 的封装代币收益费用。

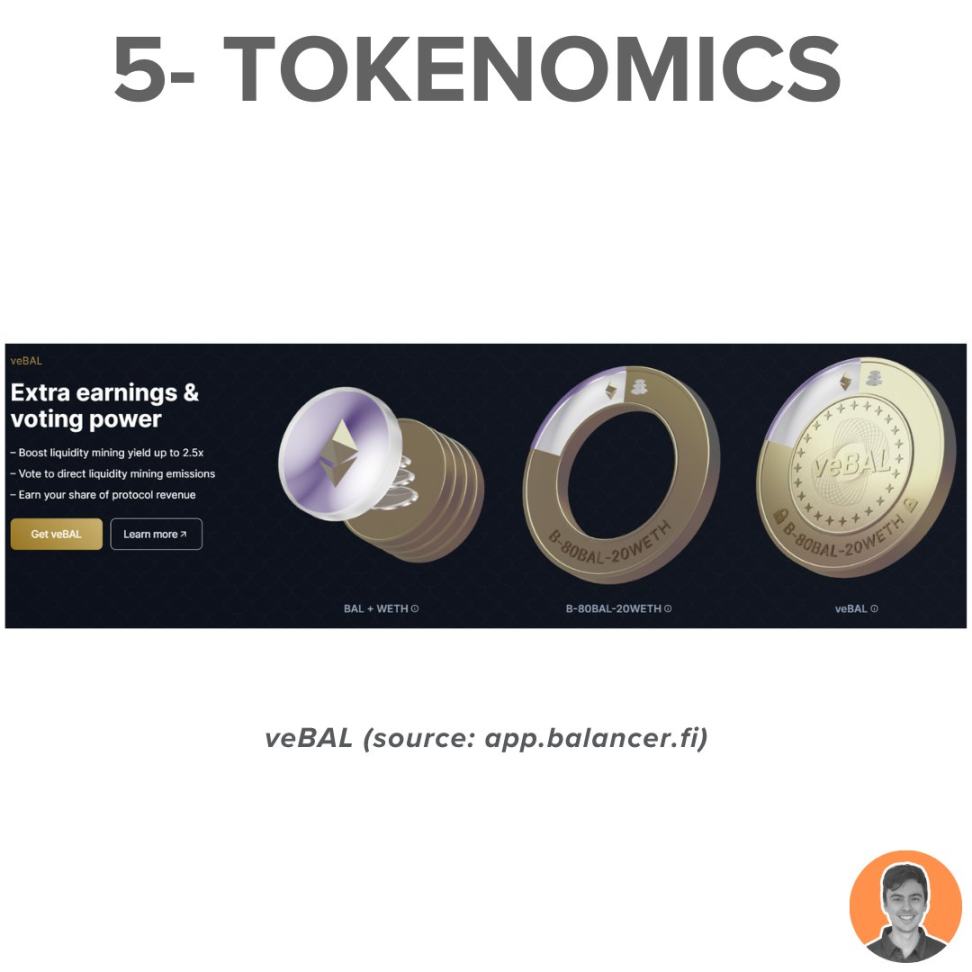

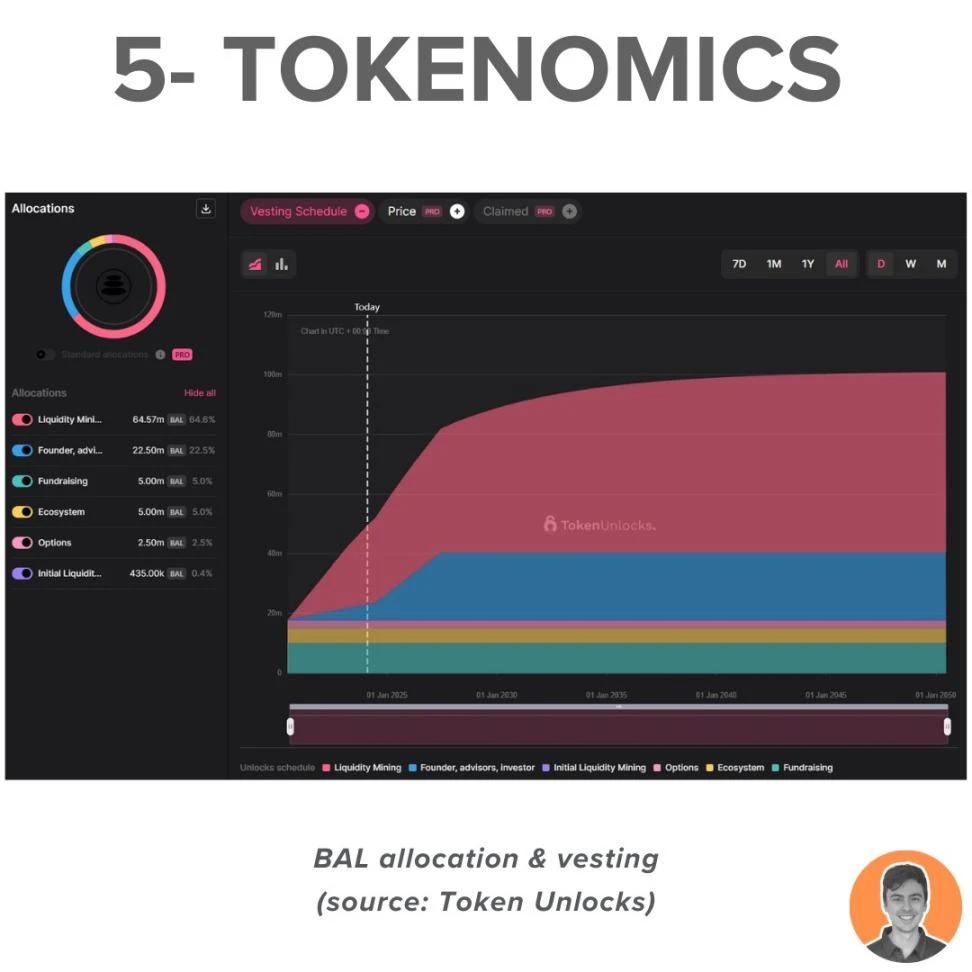

5.代币经济学

生态系统中有两种主要代币:

BAL,即生态治理代币;

veBAL,即锁定一定期限的 BAL(以 80: 20 的比例锁定 BAL/WETH);

Balancer 提出的 80: 20 比例的 ve 模式是一种创新,旨在解决单方质押给 DAO 治理代币经济(例如 Curve)带来的一些问题。

让我们来看看一些关键的区别:

用户通过锁定 80/20 比例的 BAL/WETH Balancer 池代币而不是纯 BAL 来获得 veBAL,即使大部分 BAL 代币被锁定,也能确保深度流动性;

最长锁定期限为 1 年,比 veCRV 的最长 4 年期限有所缩短;

当前供应统计:

循环供应量: 5478 万枚;

最大供应量: 9615 万枚;

市值: 1.95 亿美元;

FDV: 3.42 亿美元;

市值 /FDV: 57% ;

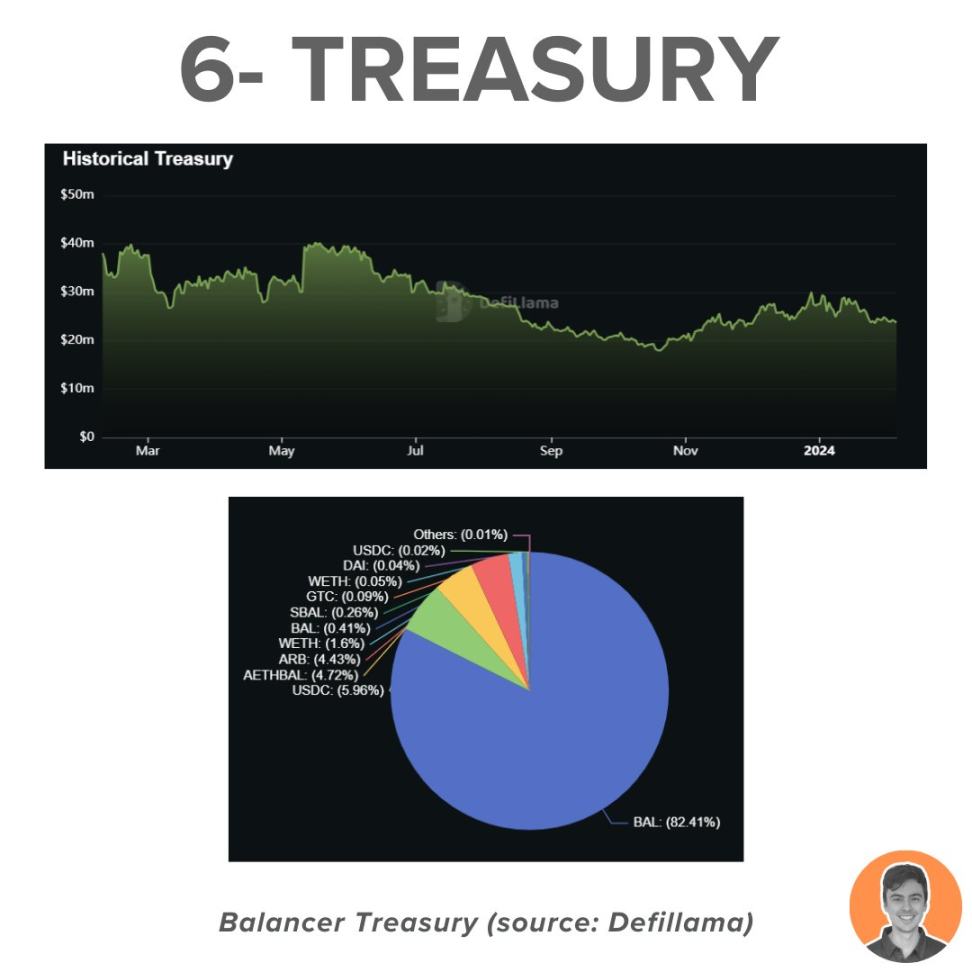

6.金库

Balancer 金库目前价值 2377 万美元,它由以下部分组成:

价值 1959 万美元的 BAL;

其他价值约 236 万美元的代币(ARB、AETHBAL);

143 万美元的稳定币;

价值 39 万美元的主流代币(BTC 和 ETH);

这些资金目前由 DAO 多重签名钱包持有。

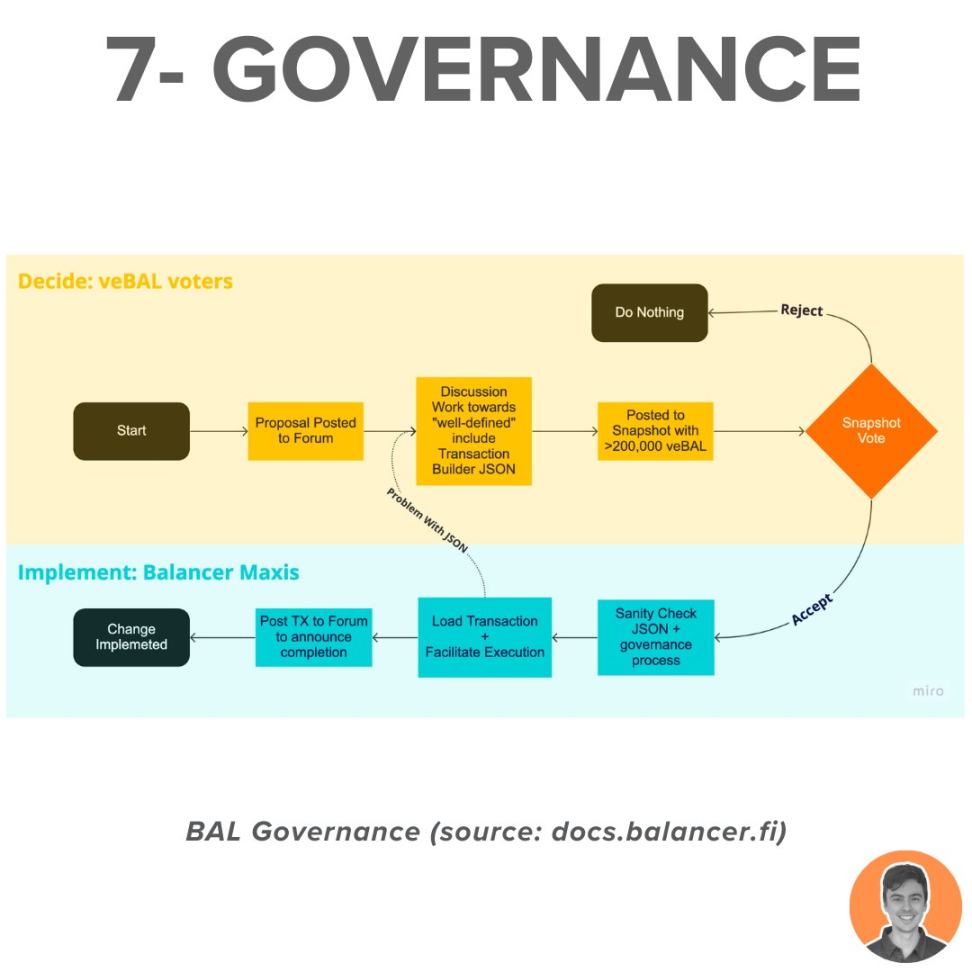

7.治理

Balancer 实施了强大的去中心化治理流程,并且已经运行了相当长的一段时间。

此外,他们还推出了 ve(80/20)计划,旨在显着增强传统 DAO 治理的代币经济学设计。

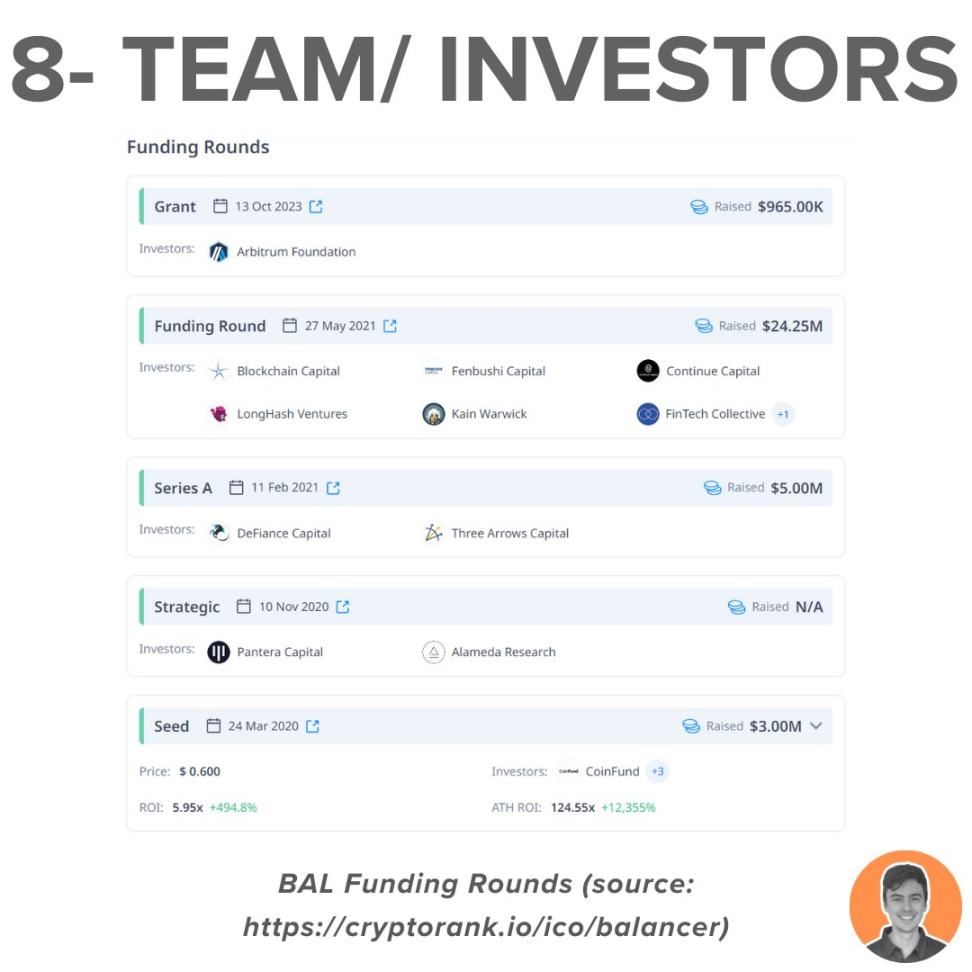

8.团队及投资者

Balancer 由 Fernando Martinelli 和 Mike McDonald 于 2018 年创立,自成立以来,Balancer 已成功筹集 3925 万美元资金。

著名投资者包括 Pantera Capital、Blockchain Capital、CoinFund、Fenbushi Capital 和 Arbitrum 基金会。

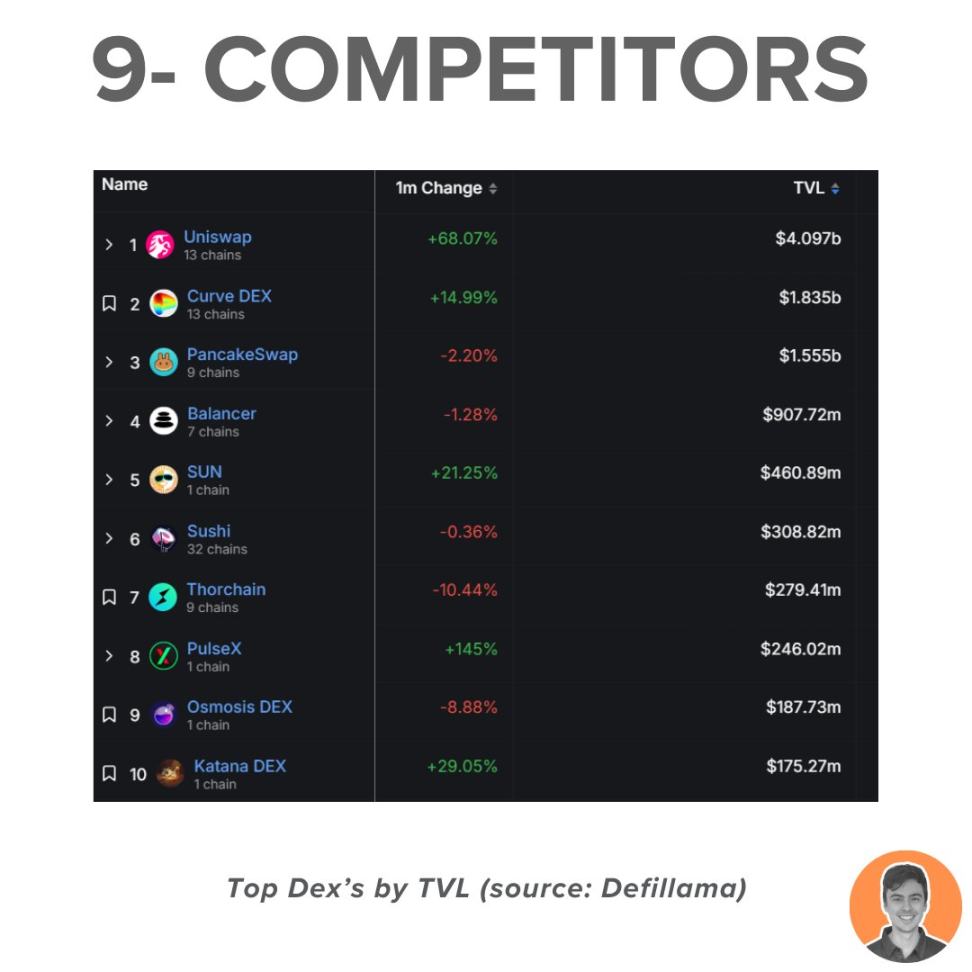

9.竞争对手

Balancer 是一个著名的 DEX,与其他几个平台竞争,包括 Uniswap、Curve、PancakeSwap、Sushi 和 Thorchain。

然而,Balancer 将自己定位为新项目的最佳 AMM 和技术堆栈,可用于快速扩展和构建。

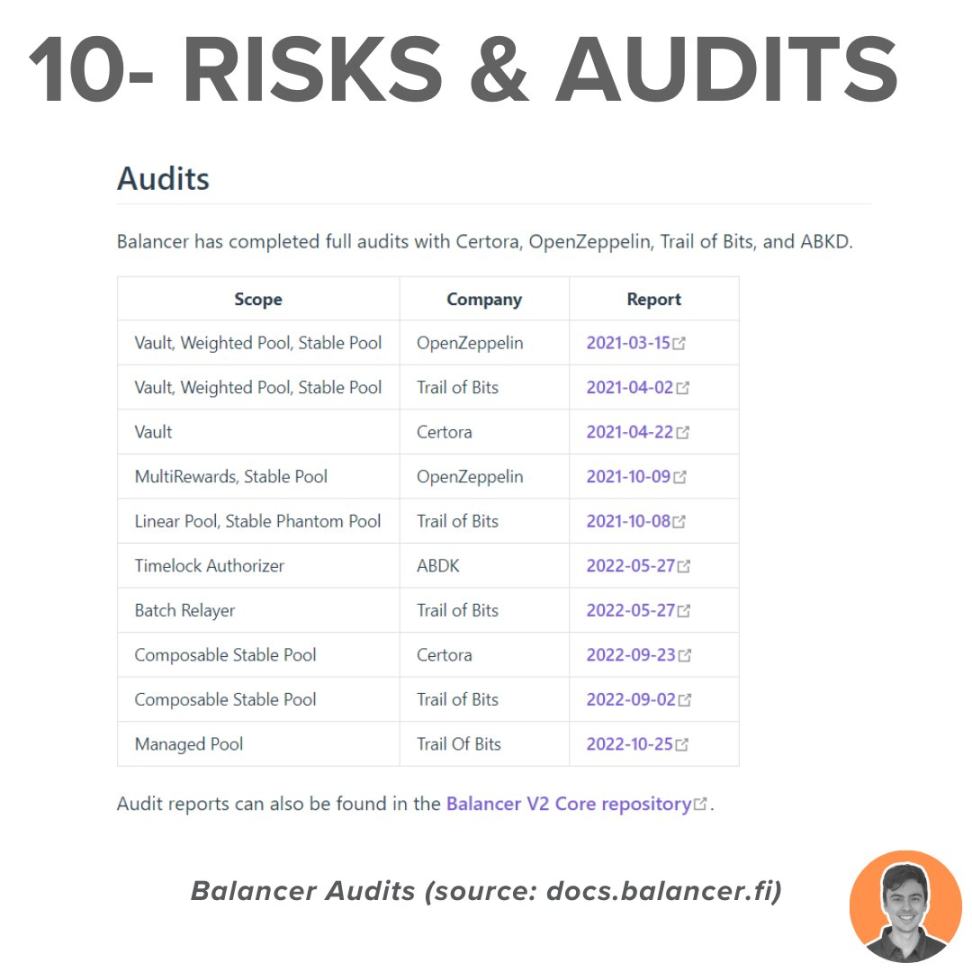

10.风险与审计

2023 年,Balancer 经历了两次重大漏洞,其中一个影响了 V2 池,而另一个则涉及前端攻击。

值得注意的是,Balancer 经过了多次审计,并推出了大额漏洞赏金计划(最高 100 万美元)。

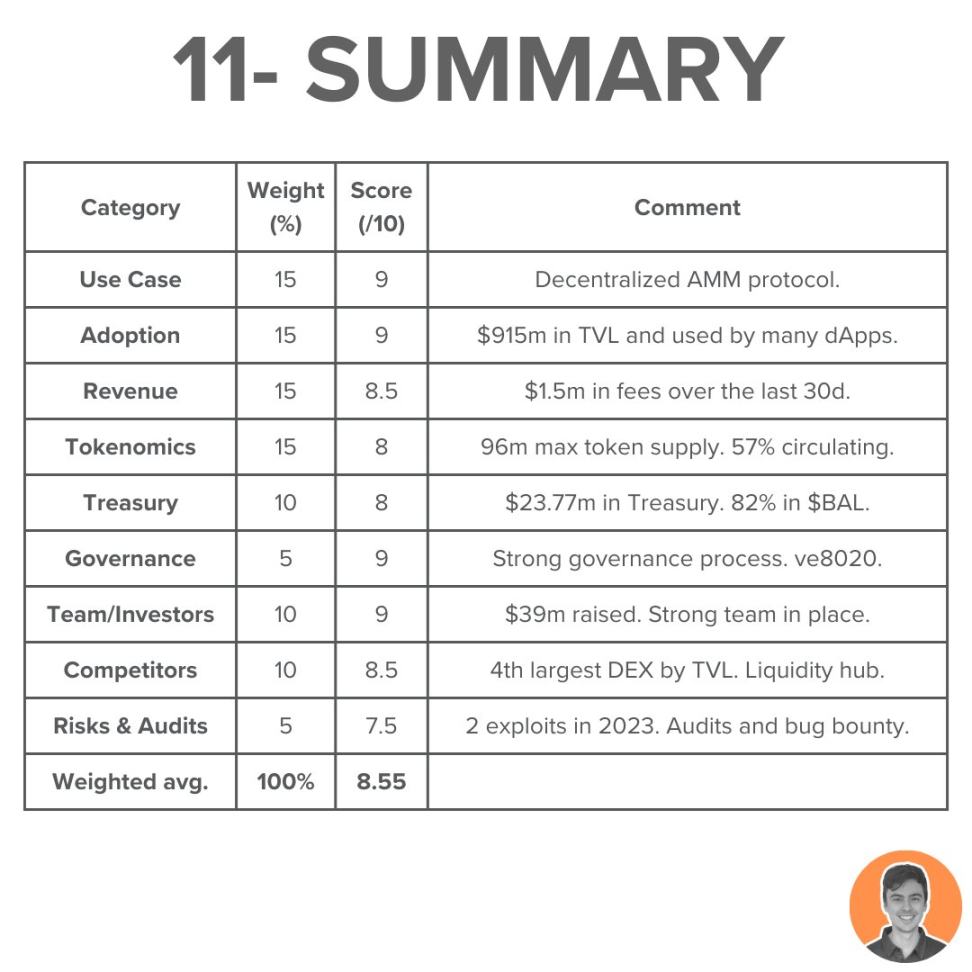

11.总结

Balancer 正在低调发展,该团队不断开发创新且实用的产品,即将到来的催化剂包括:

Balancer V3 升级;

LST 和稳定币收益的增长;

治理代币经济学——ve 80/20 流动性池;

总加权分数= 8.55