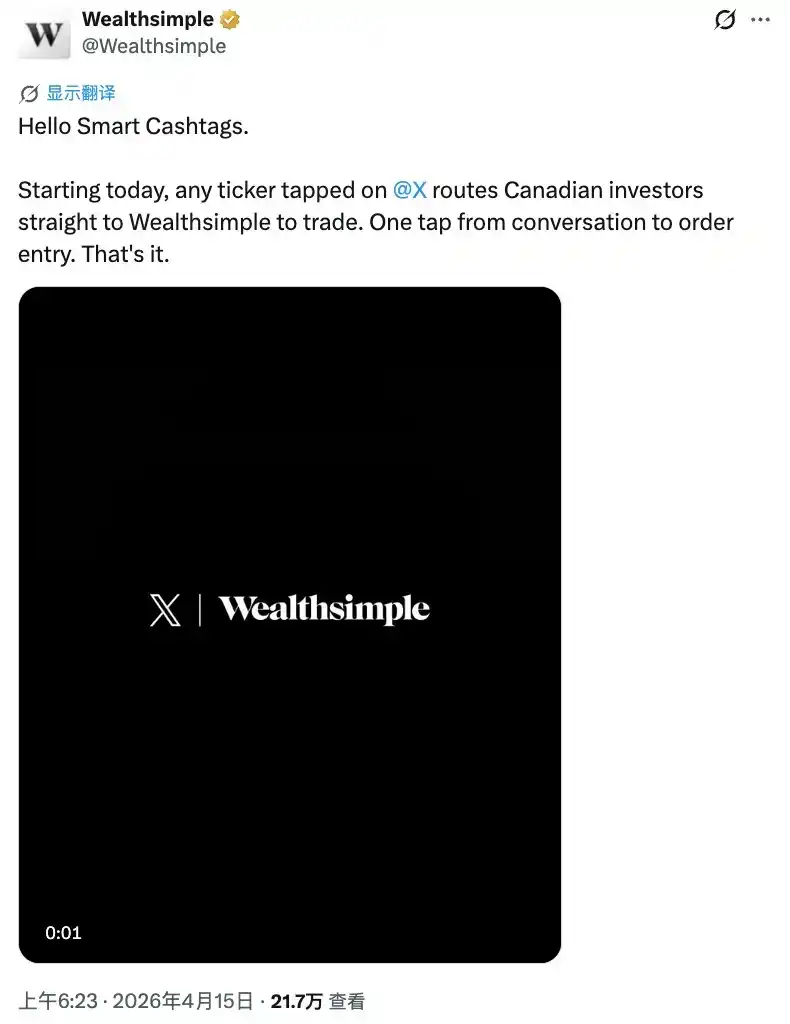

On April 14, the X platform launched the Cashtag feature on the iPhone in the United States and Canada. The usage is very simple: type $AAPL in a tweet, and this string of characters becomes a blue clickable link. Click on it, and you will see Apple's real-time stock price chart, price trends over a period of time, and all discussions on X with $AAPL. If you are in Canada, you will also see a button that directly jumps to Wealthsimple to complete the transaction.

What Can Cashtag Do?

It's not just stocks. X's Cashtag also supports cryptocurrencies. You can search for $BTC, $ETH, or directly input the contract address of a token on the Solana chain to find its on-chain data. In other words, this system aims to cover everything from mainstream blue-chip stocks to long-tail meme coins.

X's product lead, Nikita Bier, specifically emphasized at the feature launch: X will not act as a broker and will not directly execute trades. X's positioning is the "data and discovery layer"; it is responsible for presenting information, aggregating discussions, and guiding users. The actual order placement is handed over to third-party brokers to complete.

This positioning is crucial. If X were to directly act as a broker, it would need to face the SEC's broker license review, FINRA's compliance requirements, and a series of complex regulatory procedures. By defining itself as a "data layer," X only provides information display, while trade execution happens elsewhere, making the regulatory boundaries much blurrier.

But in terms of user experience, the entire path from seeing a tweet to completing a transaction has been compressed to just a few clicks. This is the first time on the X platform that there is no friction between discussion and action.

Its Origin Is Somewhat Ironic

The term "Cashtag" was not invented by X.

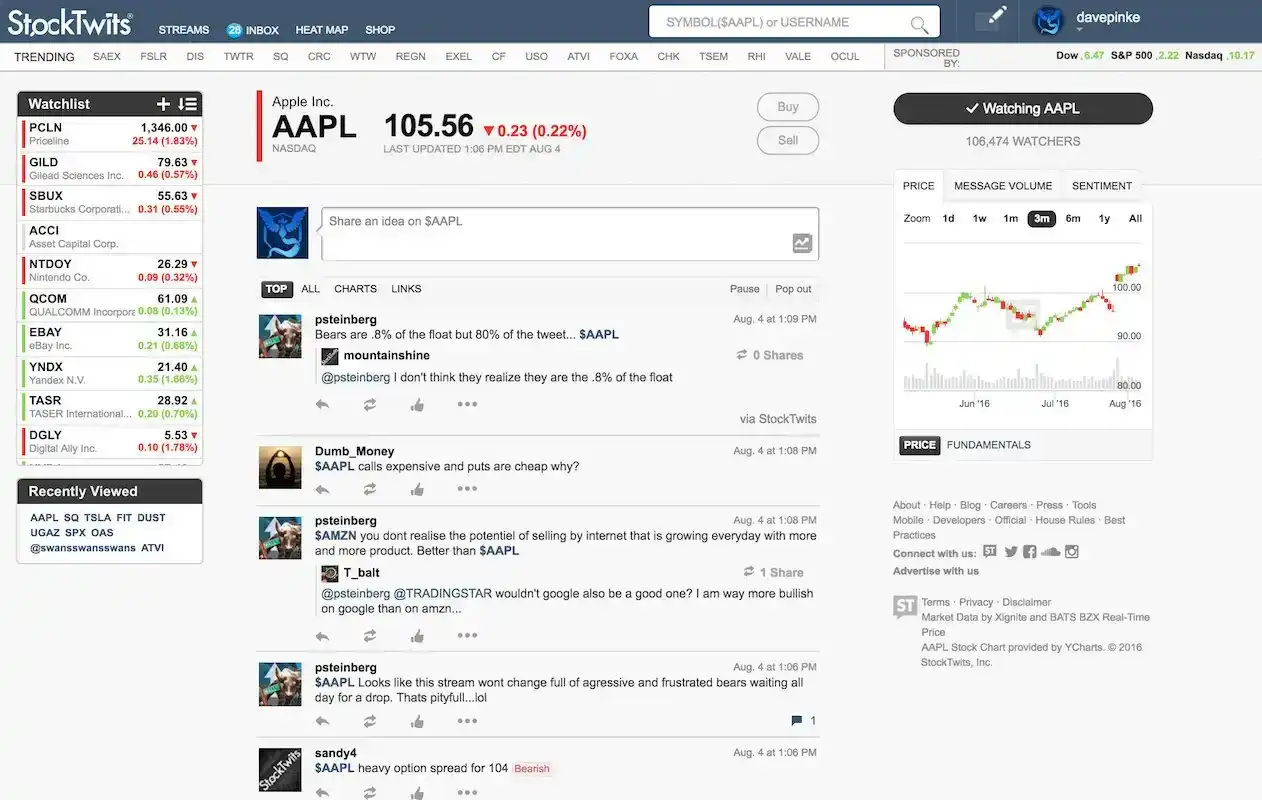

In 2008, a financial analyst and angel investor named Howard Lindzon created StockTwits, a social platform specifically for investors. He introduced symbols like $AAPL on it, using the $ prefix to turn stock tickers into clickable hashtags, allowing retail investors to discuss specific assets and track market sentiment. He named this design: cashtag.

This idea circulated in small circles for four years.

In July 2012, Twitter announced official support for cashtag; $AAPL on Twitter became a blue clickable link. Lindzon publicly expressed "disappointment," saying Twitter had "hijacked" his idea. But he was powerless; cashtag had no copyright, the $ symbol belongs to everyone, and Twitter owed him no explanation.

Over the next dozen years, the two reached a strange balance: StockTwits lived off cashtag, but its traffic was far less than Twitter's. Twitter had the cashtag feature, but on Twitter, it was more like a hashtag than a real financial tool. Clicking on it only led to a topic page—no data, no prices, nothing actionable.

On April 14, 2026, Lindzon posted a tweet on his X homepage advertising the 2026 Cashtag Awards that StockTwits was about to host at the New York Stock Exchange.

On the same day, the X platform made cashtag truly usable for the first time. Cashtag was invented, appropriated, shelved for over a decade, and then weaponized right under the nose of its inventor, who was still advertising on the opponent's platform.

Why Wealthsimple?

The Cashtag feature was first launched in the US and Canada, but only Canadian users can click on a Cashtag to directly jump to a broker to place an order. The reason is simple: Wealthsimple is a Canadian company, so it's available in Canada. The trading partner for the US market has not yet been announced. But the interesting question is: Why Wealthsimple, and not other Canadian financial institutions?

Wealthsimple is Canada's largest online broker—this is its most direct identity. Founded in 2014, it now manages over CAD 50 billion in assets and has extremely high penetration among young investor demographic in Canada. It holds both traditional securities licenses and digital asset trading permits (Wealthsimple Digital Assets), allowing it to handle both stocks and cryptocurrencies—a condition that X's Cashtag needs to support. This is not something just any institution in Canada can meet.

At the same time, Wealthsimple is also a partner with "a history."

In March 2026, just one month before the partnership with X was announced, the Quebec Superior Court approved a class-action lawsuit settlement against Wealthsimple's crypto business. The cause was its promotion of "zero-commission" trading without clearly explaining to users that it profits from the bid-ask spread. The final settlement was CAD 750,000, averaging about CAD 3.34 per investor. Wealthsimple did not admit any wrongdoing, but the information disclosure issue was already publicly disputed.

Earlier, in 2025, Wealthsimple experienced a data breach. A software package from a trusted third-party supplier was attacked, leading to unauthorized access to some customers' Social Insurance Numbers and account information. Wealthsimple controlled the situation within hours, completing full notification and emergency response. From a crisis management perspective, it did not collapse.

To summarize Wealthsimple's status in one sentence: It has stumbled, but it has gotten back up. It knows where the regulatory boundaries are and has real crisis management experience. For X's new feature, which aims to connect social discussion with trading entry, such a partner, compared to one that hasn't been tested, actually presents more predictable risks.

The real suspense lies in the US market. Robinhood is testing its own social trading feature (Robinhood Social); Coinbase has deeper crypto compliance experience but also more friction with the SEC. Whom X chooses in the US will be the real test of whether this model can succeed.

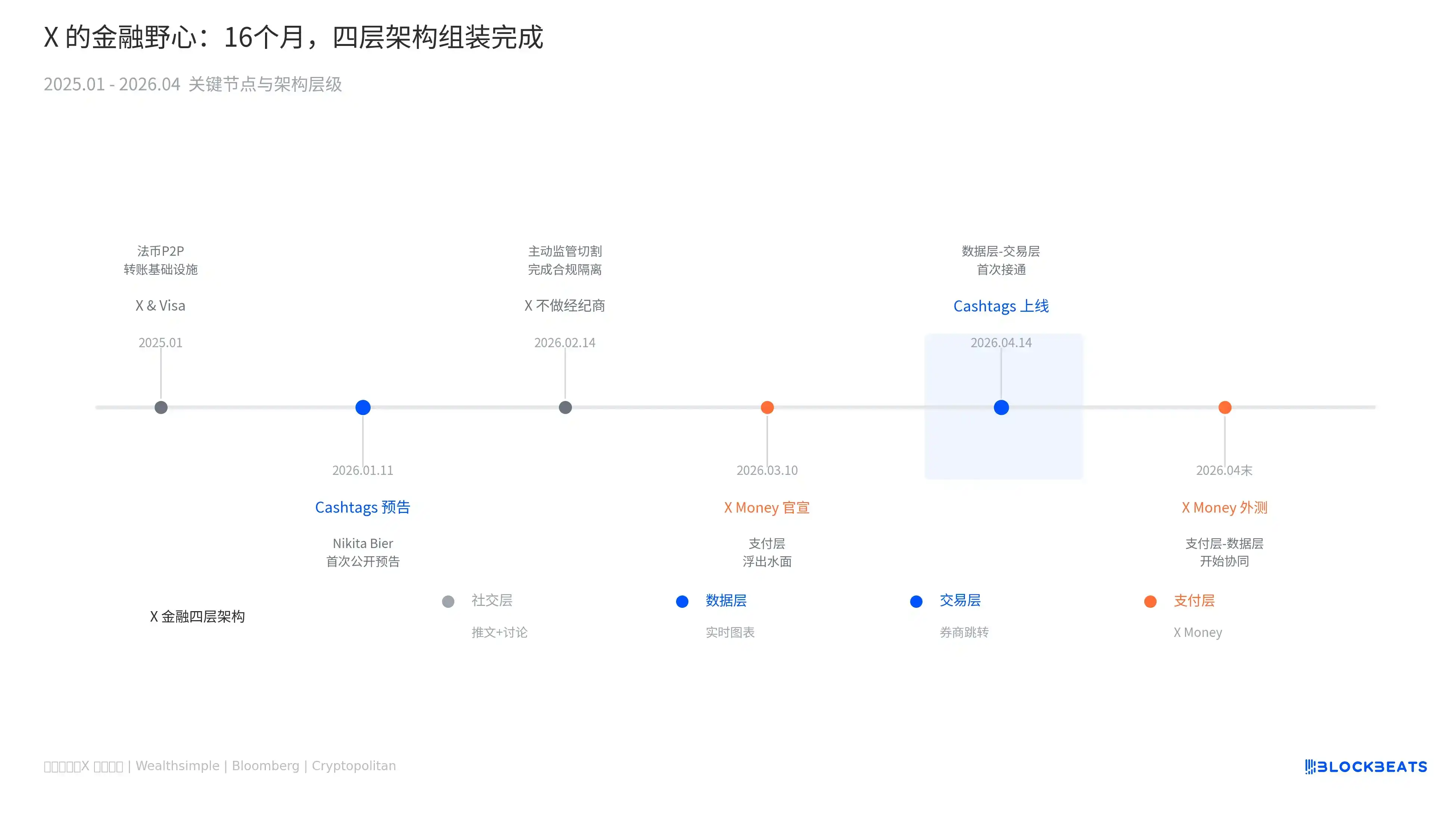

X's Financial Ambitions, A Timeline Explained in One Chart

The launch of the Cashtag feature marks the assembly of a layered architecture. Looking back at X's actions over the past 16 months, each step falls into a precise position:

January 2025: Partnered with Visa, obtaining the infrastructure for fiat peer-to-peer transfers;

January 2026: Nikita Bier previewed Smart Cashtags, the outline of the financial data layer began to emerge;

February: Proactively clarified "X is not a broker," completing the regulatory separation;

March: X Money officially announced public beta plans, the payment layer surfaced;

April 14: Cashtags launched, simultaneously announcing the Wealthsimple partnership—the data layer and trading layer connected for the first time.

Stack the four layers together: Social layer (tweets + discussions), Data layer (real-time charts), Trading layer (broker jump), Payment layer (X Money P2P transfers + 6% APY yield account). Each layer individually has mature competitors, but combined, no platform has done this before.

This is the most concrete landing of the "everything app" that Elon Musk has been talking about. Starting from attention, it first captures all discussions about money, then step by step transforms these discussions into real capital flows. From Howard Lindzon typing the first $AAPL on StockTwits in 2008 to the X platform today allowing hundreds of millions of users to click this symbol and directly buy stocks, cashtag took 18 years to fulfill its destiny.