Author: Alan | Biteye Content Team

On June 17th, WeChat's official account "微信派" announced that WeChat Pay has officially launched the AI-exclusive card. According to the official description, users can propose consumption needs in conversations with Workbuddy and complete related payments through the AI-exclusive card.

This sounds quite interesting: in the future, to order a milk tea, purchase a service, or subscribe to a tool, you could just let the AI handle the entire process seamlessly.

However, after practical testing, we found that the WeChat AI-exclusive card currently does not support "fully automated AI consumption." A more accurate understanding is: it is a layer of payment capability opened by WeChat Pay for AI Agents, but each transaction still requires user confirmation. Moreover, whether a purchase can actually be completed depends on the Agent, Skills, third-party platform authorization, and product fulfillment processes.

This article will explore two questions and one hands-on test:

-

What exactly is the WeChat AI-exclusive card?

-

What can it do now, and what can't it do?

-

A practical test: using it to order a cup of milk tea to see how many pitfalls we can encounter.

1. Conclusion First: The WeChat AI-exclusive Card is Not a Card for "AI to Spend Freely"

From a product mechanism perspective, the WeChat AI-exclusive card is more like a "small wallet" isolated from the main WeChat wallet.

Users first need to bind the AI-exclusive card and then transfer funds from their WeChat wallet to this card. Subsequently, relevant consumption by AI Agents will be deducted from this independent balance first, rather than directly from the user's daily WeChat wallet funds.

Simply put, it primarily addresses three questions:

First, where does the money for AI consumption come from.

The AI-exclusive card has an independent balance, making financial boundaries clearer.

Second, whether AI consumption can be controlled.

Each payment still essentially requires user confirmation on the mobile device after scanning a QR code; it's not automatic deduction by the AI.

Third, how AI consumption records are managed.

AI-related expenses are separated from ordinary WeChat Pay transactions, making them easier to view and manage.

2. How to Activate: Entry Point is in the Workbuddy Conversation

WorkBuddy is a desktop office efficiency agent launched by Tencent, closer to an Agent workbench, with an interface similar to CodeX. It can understand user goals in conversation and then use different "expert" Agents or Skills to call external capabilities to complete tasks, such as office processing, information queries, and local life services.

This time, WeChat Pay's AI-exclusive card was first integrated into WorkBuddy, which also implies that WeChat Pay is not directly opening up to all AI applications. Instead, it is first testing the complete process of "AI initiating payment, user confirming deduction" within a relatively controlled Agent scenario.

The actual activation process is not complicated:

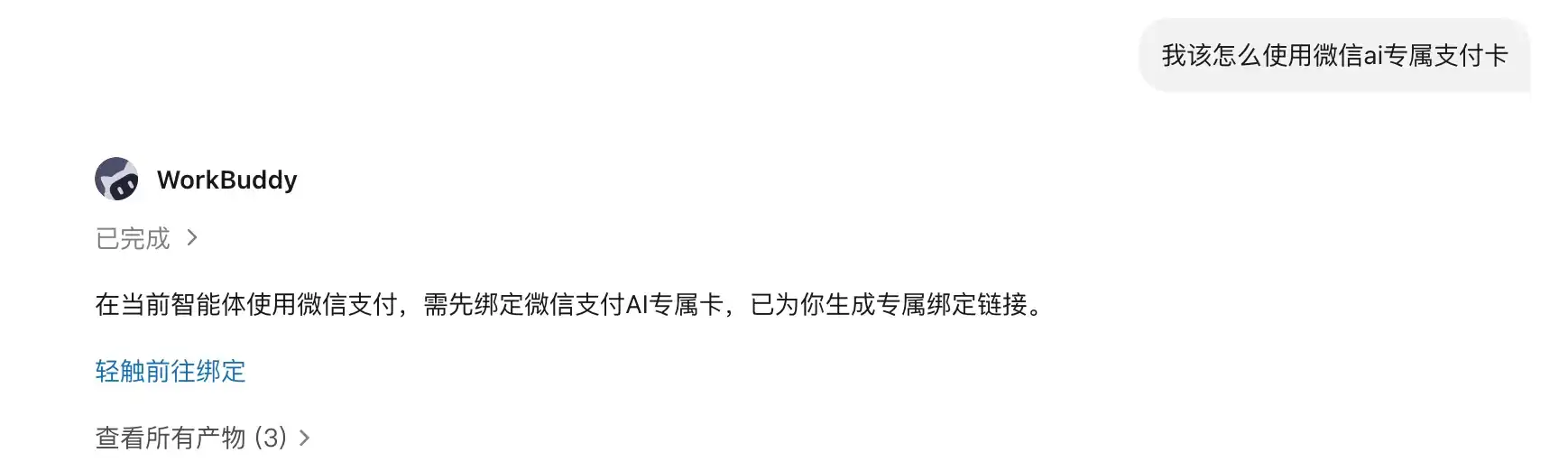

Step One, ask in the Workbuddy dialog:

"How do I use the WeChat AI-exclusive payment card?"

The Agent will return a jump link ⬇️

Step Two, after clicking the link, you need to scan a QR code with WeChat to complete the binding.

A small detail here: the binding link is only valid for 5 minutes after generation, so you need to scan the code promptly.

Step Three, read and agree to the relevant agreements, and after entering your payment password, you can complete the binding.

Step Four, after binding is complete, users can transfer funds from their original WeChat wallet to the AI-exclusive card.

The activation and top-up experience is quite smooth. However, the real challenge with AI payment doesn't lie in "how to get the card," but in what happens after you get it—can the AI actually help users complete purchases smoothly?

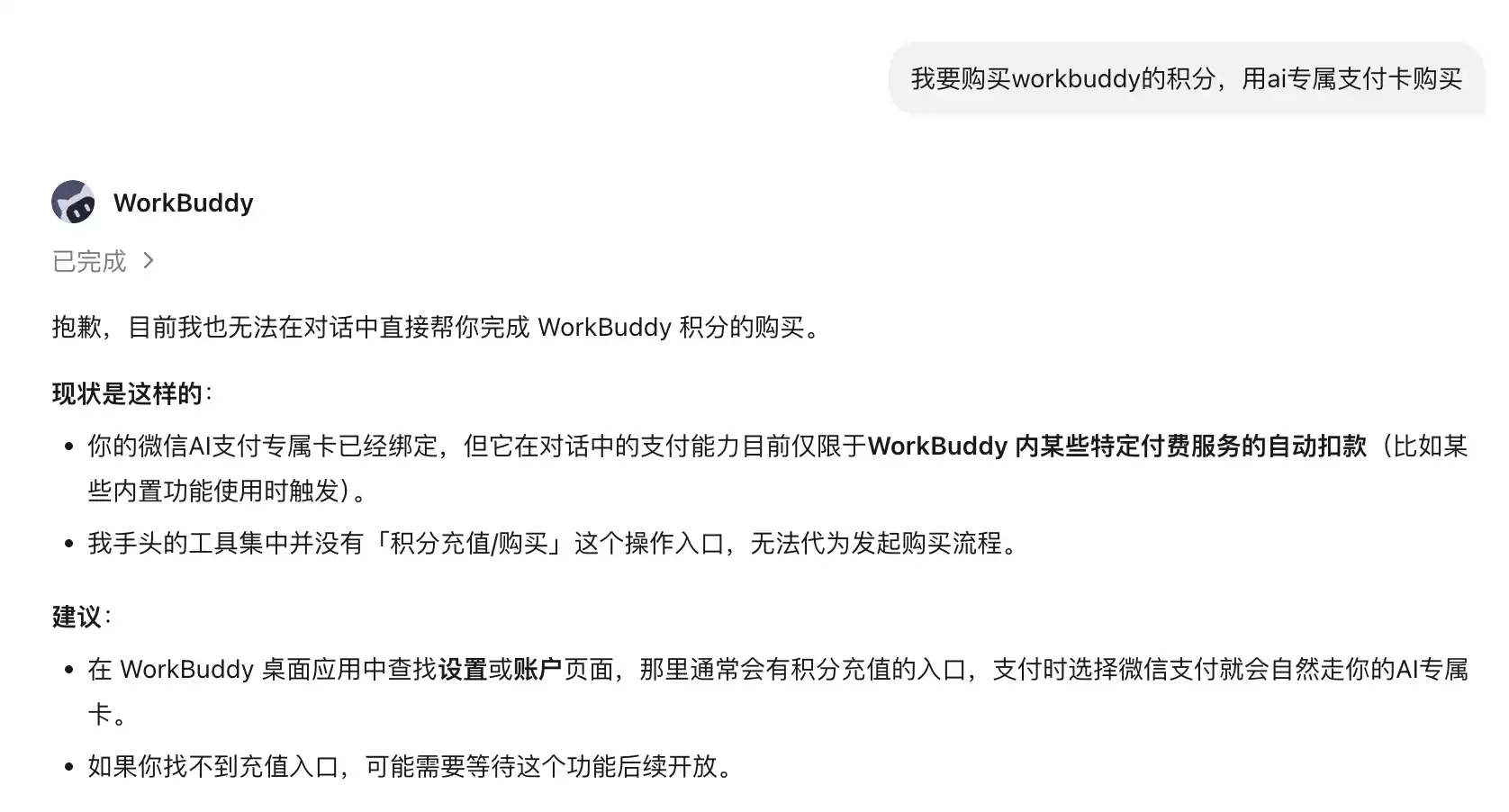

3. What Scenarios Is It Currently Suitable For?

According to Workbuddy's explanation, the AI-exclusive card is mainly intended for several types of AI consumption scenarios:

1️⃣ Purchasing Paid Content

Such as reports, data, professional analysis services, etc.

2️⃣ Calling Paid APIs or Tools

Such as certain online plugins, professional database queries, tool capabilities charged per use.

3️⃣ Subscribing to or Renewing Services

Such as in-platform value-added features, membership services, etc.

These scenarios share a common point: the payment objects are relatively standardized, the consumption chain is short, and the fulfillment method is quite clear.

However, unfortunately, so far, our tests have not identified any of these three types of applications within Workbuddy that can directly trigger payment using the AI-exclusive card. According to Workbuddy, it needs to trigger certain specific built-in paid features ⬇️

4. Hands-on Test: Asking Workbuddy to Order a Heytea for Me—Failed

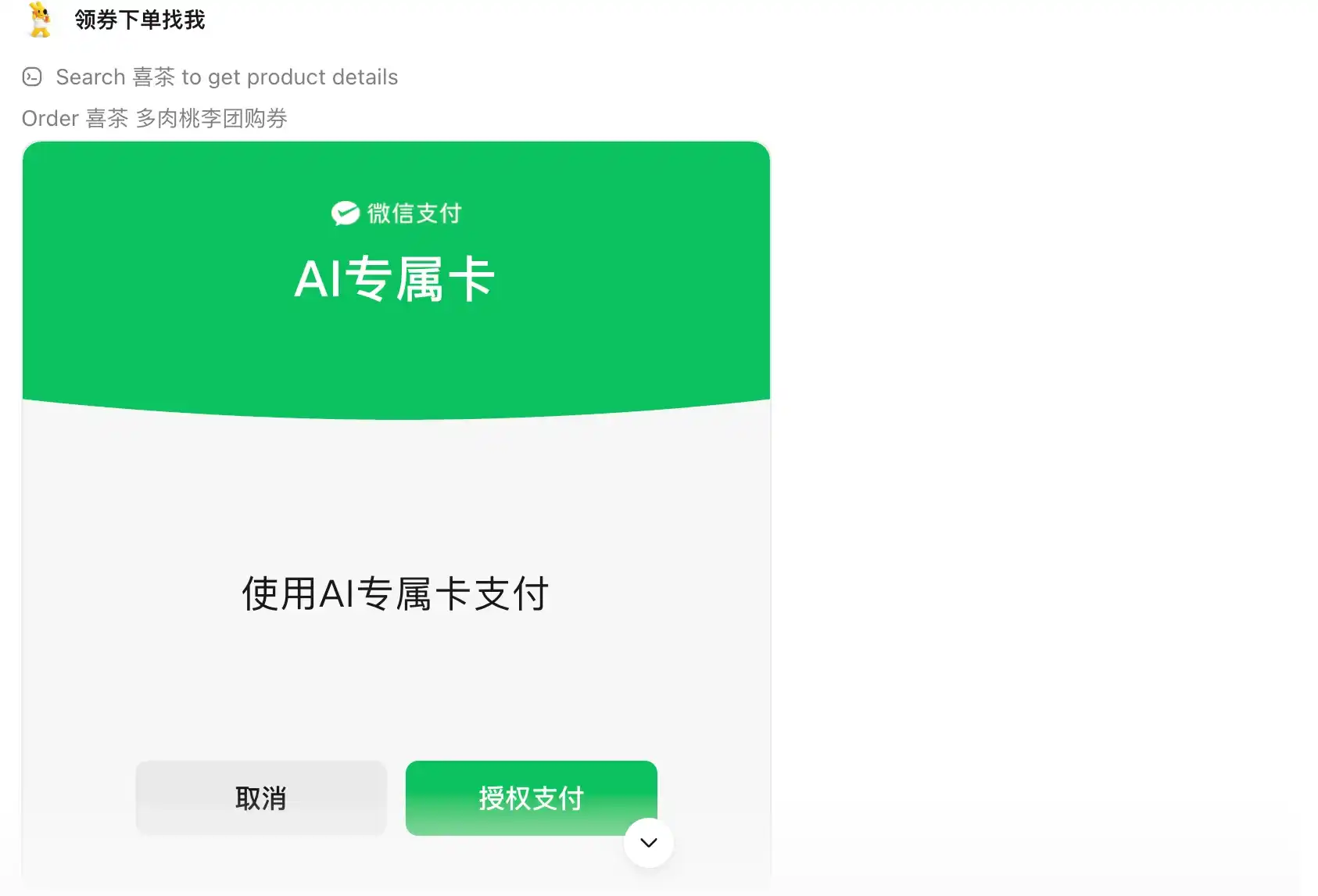

🥤 We tried one of the most intuitive life scenarios: asking Workbuddy to order a cup of Heytea for me.

The first step encountered a limitation. Workbuddy itself cannot directly fulfill such takeout or beverage ordering needs; it requires calling the corresponding life service Skill.

Therefore, following WeChat's official demonstration, we selected the "Meituan Life Assistant" Skill.

This step introduced a new cost issue: just generating the QR code to log into the Meituan account consumed 185.37 points. In comparison, Workbuddy awards 150 points daily upon login.

This means that before even starting the actual order, the step of just authorizing the login had already exceeded the daily free point allowance.

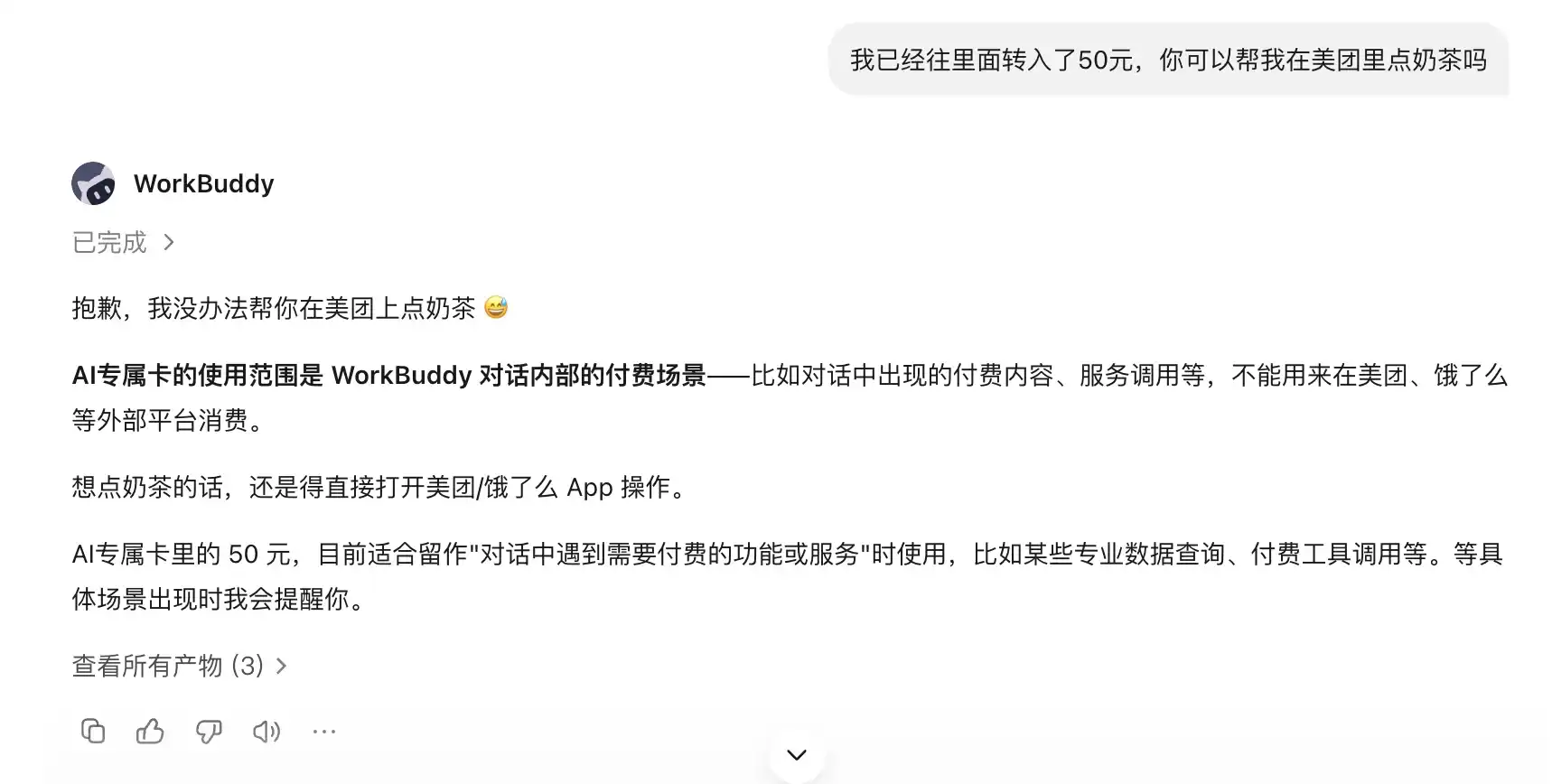

After completing the account login authorization, we continued to ask it to order milk tea. When the AI-exclusive card payment link popped up, the experience did indeed feel close to "AI buying something for me."

However, after payment, we discovered that what Workbuddy actually purchased was not the specific cup of milk tea we wanted, but a Meituan group-buying coupon that didn't match our needs.

The payment action was completed, but the purchase result did not align with the user's needs.

5. Reasons for Failure: The Problem Isn't with Payment, but with the Agent Execution Chain

In fact, this failure cannot be simply attributed to the AI-exclusive card being "not useful." More accurately, the AI-exclusive card is responsible for the payment capability, not the complete purchasing capability.

What really got stuck was the Agent execution chain.

A task like "help me order a cup of milk tea" involves at least the following steps:

Identifying user needs, calling a third-party platform, completing account authorization, selecting the correct product, confirming the fulfillment method, initiating payment, user confirming payment, completing subsequent fulfillment...

The AI-exclusive card only covers the "payment" part. As for the preceding steps like product identification, platform redirection, account authorization, product matching, and the subsequent delivery or verification, they all deeply rely on the capabilities of the Agent and third-party Skills.

Therefore, in this test, the AI did trigger the payment, but it did not complete the "correct purchase."

This is a common issue many AI Agents currently face: they can call tools, but they are not yet guaranteed to reliably complete complex real-world tasks.

6. Current Mechanism: Users Still Hold Final Payment Confirmation Authority

From a security perspective, the AI-exclusive card does not allow the AI to bypass the user and make payments directly.

The current mechanism can be roughly summarized as:

| Aspect |

Current Mechanism |

| Source of Funds |

Only uses the independent balance in the AI-exclusive card |

| Payment Confirmation |

Every payment requires user confirmation on the mobile device |

| Main Account |

Does not directly deduct funds from the main WeChat account |

| In-Store Goods |

After payment is completed, the user still needs to go to the store for verification/redemption |

This design is relatively restrained and aligns with the current realistic state of AI consumption scenarios.

If the AI could directly and autonomously make payments, the risks would actually be very high: buying the wrong product, duplicate orders, accidental subscriptions, or induced consumption could all become real problems.

Therefore, the WeChat AI-exclusive card currently functions more like a small WeChat wallet with controllable limits, confirmation for each transaction, and isolation from the main account.

Final Thoughts

If you just want to experience the WeChat AI-exclusive payment card, you can try activating it. However, it is recommended to start with low-amount, low-risk, digital service scenarios first. But please keep the following three points in mind:

1️⃣ Top up with a small amount first; don't deposit too much at once.

2️⃣ Carefully check the product name, amount, and fulfillment method before paying.

3️⃣ Do not assume that the AI Agent has understood your real needs, especially when it involves specific stores, delivery, group-buying coupons, or packages.