Strong cash flow foundation, billions poured into AI, the market seems to applaud the "splurge," but will this time be different from the metaverse?

Written by: Frank, M Tong MSX

$135 billion—this is the amount Meta (META.M) plans to spend in 2026.

The Q4 2025 earnings and Q1 2026 guidance, both exceeding expectations, let many who were anxious about "falling behind" breathe a sigh of relief. But at the same time, the full-year 2026 capital expenditure (CapEx) soaring to $135 billion, nearly double last year's, is hard not to worry about—could this be another aggressive gamble?

Surprisingly, the market seemed to choose to buy, with Meta's stock surging over 10% after hours and continuing to rise overnight.

Meta Stock Price Data Source: Yahoo Finance

The answer lies hidden in this earnings report: at least at this stage, it shows the market that AI investment isn't just a future vision but is already tangibly improving the current core cash cow—advertising business. So Wall Street started betting on Meta's narrative reversal and is willing to buy into this super spending plan.

Ultimately, "daring to spend, daring to bet" has always been the底色 of Meta and Zuckerberg. This also means that winning could be a huge narrative reversal; losing, at least under the current financial structure, is unlikely to turn into an uncontrollable disaster.

I. Earnings Quick Read: Earnings & Guidance "Double Beat"

From the results, this is an earnings report足以改变市场情绪.

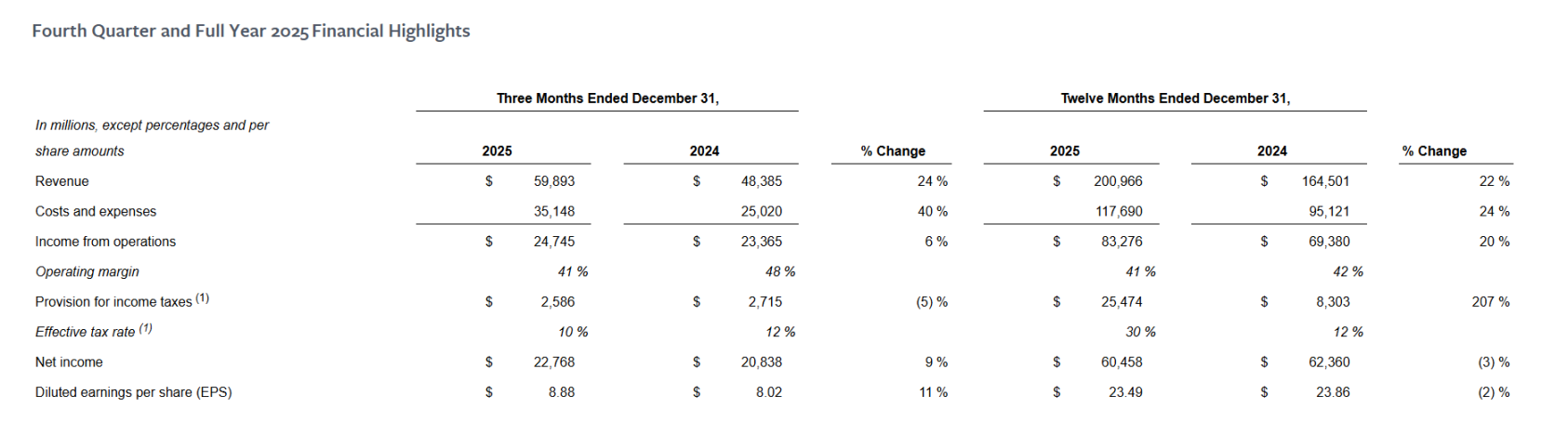

Among them, Q4 2025 core financial indicators almost all exceeded expectations across the board: revenue of $59.893 billion, up 24% YoY, above market expectations of $586 billion; net profit of $22.768 billion, up 9% YoY; diluted earnings per share (EPS) of $8.88, up 11% YoY, above market expectations of $8.23.

It can be said that whether in terms of growth resilience on the revenue side or profit release节奏 on the profit side, Meta delivered a solid, stable Q4 report card.

Extending the perspective to the full year, the growth logic同样成立: 2025 full-year revenue of $200.966 billion, up 22% YoY; operating profit of $83.276 billion, up 20% YoY, core indicators still maintaining double-digit expansion.

The only seemingly "against the trend" was the full-year net profit recording $60.458 billion, down 3% YoY, but this change wasn't due to恶化 of main business but mainly from a one-time tax factor—affected by the "Big and Beautiful Act," the company recognized about $16 billion in one-time non-cash income tax expense.

Excluding this factor, full-year net profit and EPS would still achieve可观增长, also explaining the surface contradiction between the full-year data and the quarter's strong performance.

Source: Meta

At the same time, operational metrics also showed typical "volume and price rising together" characteristics:

-

Family app daily active users (DAP) reached 3.58 billion, up 7% YoY, meeting market expectations;

-

Ad impressions up 18% YoY; average price per ad up 6% YoY;

-

Average revenue per user (ARPU) was $16.73, up 16% YoY;

This set of data points to one conclusion: Meta's advertising moat not only hasn't slowed down but is continuously evolving in efficiency and monetization capability.

Furthermore, what further stimulated market sentiment turning wasn't just the realized超预期业绩, but also management's optimistic guidance for the future: Meta expects Q1 2026 revenue to reach $535-565 billion, corresponding to YoY growth of 26%-34%, significantly higher than the previous market expectation of about 21% growth. This pricing implies management's judgment that Reels' high growth momentum will continue, and Threads' commercialization progress is better than the market's previous cautious expectations.

With the advertising base盘稳固, this guidance directly strengthened market confidence in AI-driven advertising efficiency improvement having sustainability.

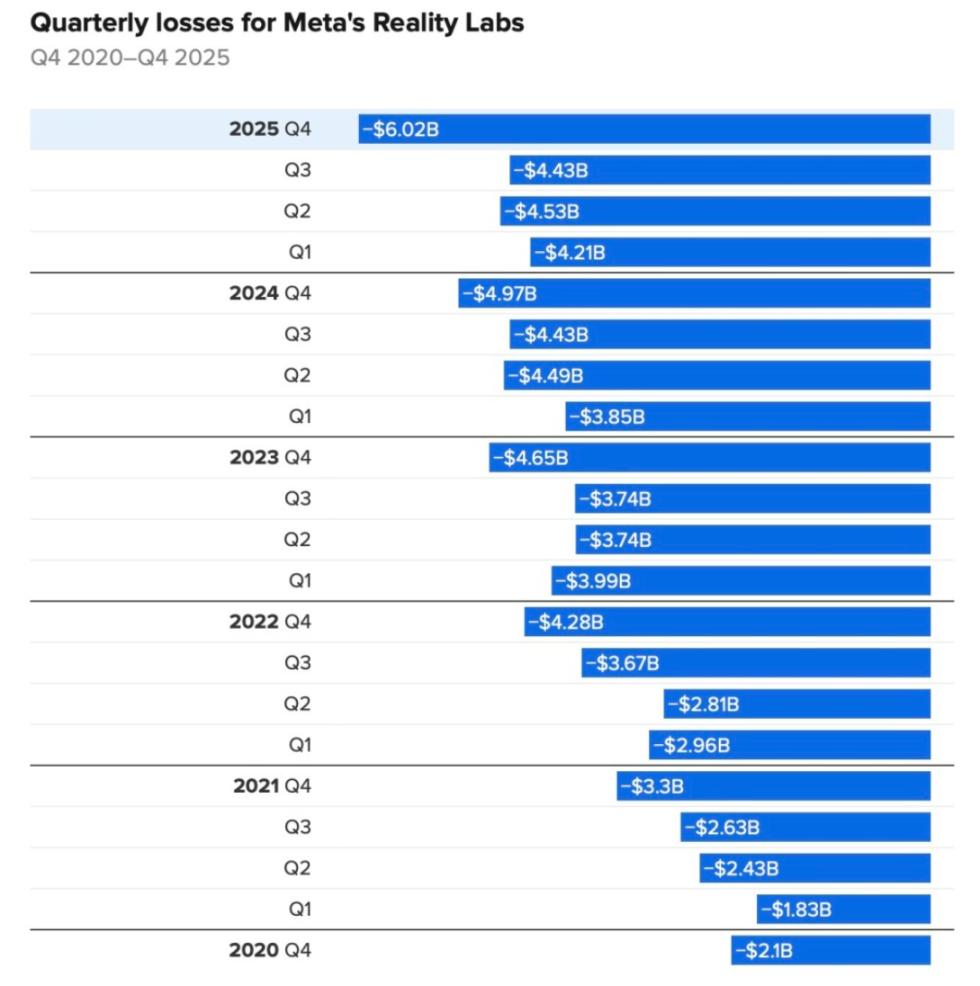

Reality Labs Five-Year Loss Details

Of course, it's worth mentioning that the "metaverse" is still Meta's bleeding edge, with its元宇宙部门 Reality Labs recording an operating loss of $6.02 billion in Q4, expanding 21% YoY. Revenue was $955 million, up 13% YoY. Since late 2020, this department's cumulative operating loss has approached $80 billion.

But different from the past, Reality Labs' role in the current earnings report is no longer the core variable左右公司整体叙事, but is gradually being marginalized.

II. Social Base盘稳固, AI Deepens the "Moat"

At least at the main business level, AI has indeed started creating value for Meta's (META.M)商业化真金白银.

It can be said that to some extent, unlike Google (GOOGL.M) or Microsoft (MSFT.M), Meta is currently the most direct and already earnings-reported player with "AI investment directly feeding back to main business cash flow".

First体现在广告效率的系统性提升上, this benefits from AI directly嵌入推荐系统与广告投放系统, making Meta's Q4 average ad price up 6% YoY, with impressions大增 18%. Management has also多次强调, AI recommendation algorithms and投放系统的升级, significantly improved ad conversion rates and投放效率.

Among them, Instagram Reels' watch time in the US market grew over 30% YoY, becoming the core engine driving ad inventory and monetization capability.

Second is the accelerated推进 of WhatsApp commercialization. Meta plans to fully introduce ads into WhatsApp Status this year, seen as the company's next potential billion-dollar revenue growth point, also a key step for AI recommendation and ad systems to expand to more traffic scenarios.

Overall, against the backdrop of ongoing external competition like TikTok, Meta's social base盘 hasn't loosened; instead, through deep AI embedding into recommendation and ad systems, it has further deepened its moat.

Source: Meta

Looking back over the past year, Meta's actions in the AI direction can be described as激进—from spending billions to acquire Scale AI equity, inviting Alexandr Wang to lead the "Meta Superintelligence Lab (MSL)", to continuously high-salary poaching, restructuring AI organizational structure, then investing tens of billions to acquire Manus, and launching Meta Compute, planning to build tens of GW-level computing and power infrastructure within this decade...

This series of actions reminds many of that familiar script: aggressive investment, grand narrative, long payback period. In other words, we seem to see the "Zuckerberg of the metaverse era" again.

But different from the metaverse period, management this time gave a clear bottom expectation, stating that even with大幅提升基础设施投入, 2026 operating profit will still be higher than 2025, and the cost growth path for the huge 2026 investment is highly transparent, mainly concentrated on computing power, depreciation, third-party cloud services, and high-end technical personnel.

In short, in Meta's strategic framework, AI isn't just a technological narrative押注未来, but a real tool持续改善主营现金流, its logic isn't complicated: when AI is deeply embedded into recommendation systems and ad systems, even marginal improvements, like making 3.6 billion users stay几十秒 longer daily, or improving ad conversion rate by 1%, on Meta's current traffic scale and ad base, will be rapidly放大为可观、可重复的现金流增量.

It is under this high-leverage structure that the efficiency improvement brought by AI is实实在在地对冲甚至覆盖高达 135 billion annual capital expenditure. In other words, Wall Street is no longer afraid of Meta burning money, to some extent because it has seen the real silver brought by AI.

Interestingly, from a more macro perspective, in Silicon Valley's AI arms race, besides the mainstream path of忙着向外输出算力、模型与工具, "selling shovels and tools" to the world, another is the Meta model—internalizing AI as the heart of its own commercial system, directly amplifying existing traffic and monetization engines.

It is this model of not relying on external sales of new products, but improving self-monetization efficiency to achieve回报, that makes Meta's AI investment path明显区别于其他大型科技公司以大模型或云服务为核心的变现逻辑, also because of this, the market began重新审视 Meta's pricing basis:

AI here isn't a long-term story waiting to be realized, but can already through the advertising system,持续、量化地反馈到主营现金流中的现实变量.

This或许也正是市场愿意重新给 Meta 定价的根本原因.

III. Violent Betting, an Unloseable War?

"Superintelligence" has become one of the highest frequency keywords in Zuckerberg and Meta management's mouths.

Zuckerberg on this earnings call also didn't hide his ambition: "I look forward to promoting superintelligence for global users", this也成为一场涵盖人才、算力与基础设施的 Meta 长期战略.

First from capital expenditure numbers, as mentioned above, Meta started an uncompromising violent betting, 2026 full-year operating expenses will reach $162-169 billion, up 37%-44% YoY,明显高于市场买方此前约 1500-1600 billion expectation range.

At the same time, Meta is also using actions to release "abandonment signals" to the market. This month, media revealed its plan to cut about 10% of Reality Labs employees again, involving about 1,500 people, meaning元宇宙相关业务正被进一步压缩,为 AI 与核心业务腾挪资源.

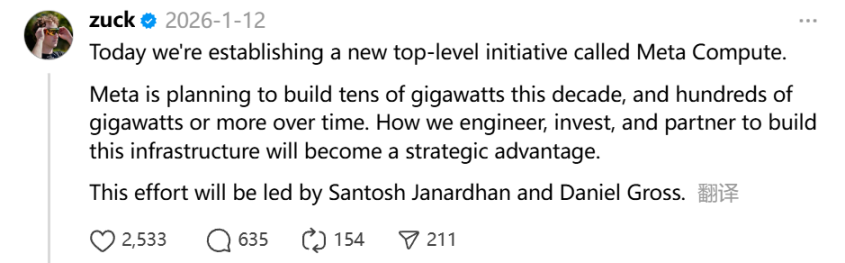

More strategically significant is Meta's redefinition of computing power and infrastructure. Zuckerberg personally posted on January 12,表示 "started a new top-level strategic project named Meta Compute". According to disclosed information, Meta plans to cumulatively invest at least $600 billion in US data centers and related infrastructure by 2028.

However, Meta CFO Susan Li later clarified this number, saying this investment isn't solely for AI server procurement but covers US本土数据中心建设、算力与电力设施, as well as supporting new employees and配套成本 needed for US business operations.

Objectively, whether from talent density, computing scale, or infrastructure intensity, Meta's investment in AI direction已经不逊于、甚至某些维度上超过了主要竞争对手.

Of course, this path is also naturally a double-edged sword. Once revenue growth, advertising efficiency, or new model progress cannot持续跑在成本扩张之前, the market's tolerance will rapidly decline, valuation and profit expectations都可能面临反噬.

In other words, this isn't an experiment that can be tried repeatedly, but a strategic war once the bow is drawn, it's hard to turn back.

Written at the End

As early as a blog program in September 2025, Zuckerberg直言, if ultimately几千亿美元浪费掉, that would be very unfortunate, but on the other hand,假设在 AI 浪潮中掉队, the risk for Meta might be higher.

"For Meta, the real risk isn't whether the investment is too aggressive, but whether it will hesitate at key moments", this remark, in today's context, can almost be seen as the footnote for all Meta's strategic actions over the past year.

Of course, history isn't easily forgotten. In the last metaverse narrative, Zuckerberg同样选择了提前下注、全力推进, but the final result didn't meet the market's initial expectations.

The difference is that this time Meta holds the world's densest, most commercializable user traffic entrance; and AI is正在以前所未有的方式, directly重塑人与内容、人与商业之间的连接效率.

As for 135 billion, whether it's a historic strategic sprint or another costly lesson, the answer still needs time to tell.