“In an era of stress and anxiety, when the present seems unstable and the future unlikely, the natural response is to retreat and withdraw from reality, taking recourse either in fantasies of the future or in modified visions of a half-imagined past.” – Alan Moore, Watchmen

Everyone is looking for scapegoats. We instead need to look in the mirror.

For the wages of sin were visible everywhere.

In every euphoria-engulfed conference hall, in every sensationalist YouTube video, in every smirk on the faces of insiders and their apologists, in every helpless, naive speculator being brought into this madness, in every pump and dump on the latest casino chain, and in every hysterical tweet: an influencer, once ethical, cashing in their reputation, their followers scammed once again; an industrious investor rewarded for years of deep research by the sudden, tragic insolvency of a trusted exchange; the bulls’ beloved heroes blown into eternity by their own greed; the others turned fraudulent and awaiting imprisonment. It was a moment of appalling revelations and discoveries, of which these were not the worst.

It was never about being fearful, it was about being prepared.

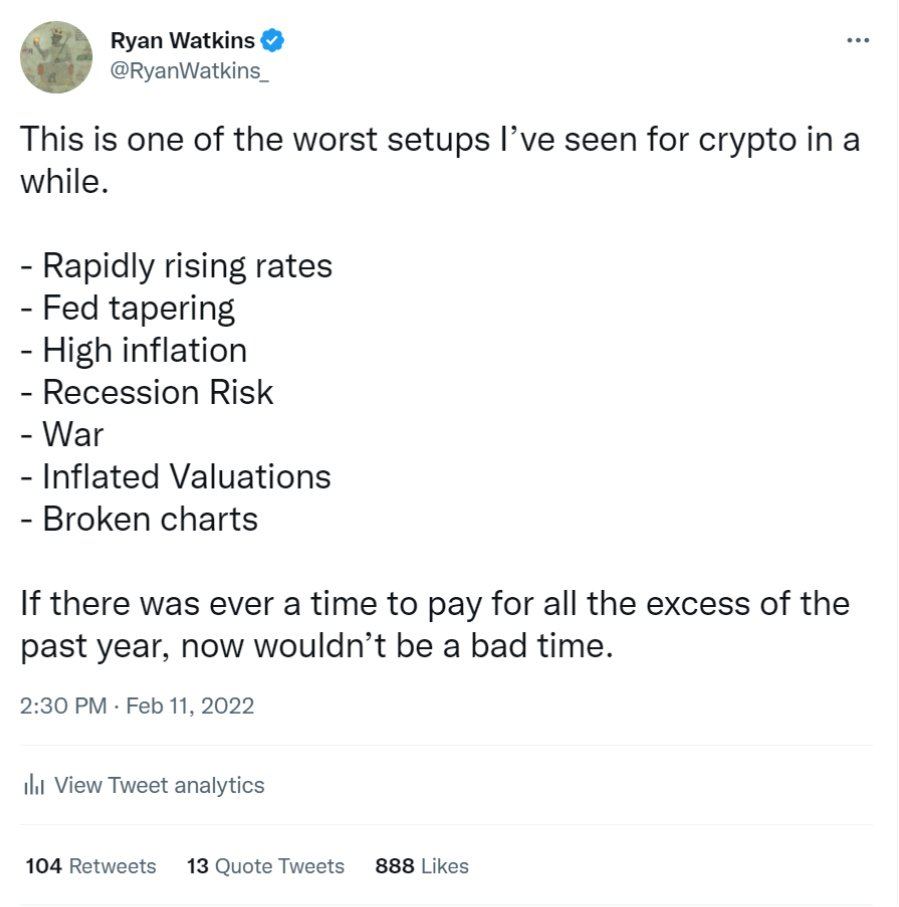

Heading into 2022 I felt troubled by the state of the industry for the first time in my career. The industry had become culturally impoverished after nearly 2 years of relentless speculation and the market was standing on increasingly fragile footing as economic risks mounted in the waning weeks of 2021. By the time February came around, I suspected it may be time to pay for all the excess of this bull market.

Setup was all that mattered. The word that defined the year was kurtosis – a measure of the “fatness” of the tails found in probability distributions. Today’s environment is the first in crypto’s history amidst the birth of a new global market regime. Decades of secular trends in global financial markets and geopolitical relations reached a turning point, setting the stage for shocks in the core engines of markets. These shocks created a ripple across the financial system, causing highly unexpected, highly impactful events to dominate crypto markets.

Kurtosis is what the market underestimated heading into 2022. Kurtosis was ultimately the basis of Syncracy’s intuition to position itself extremely defensively throughout the year.

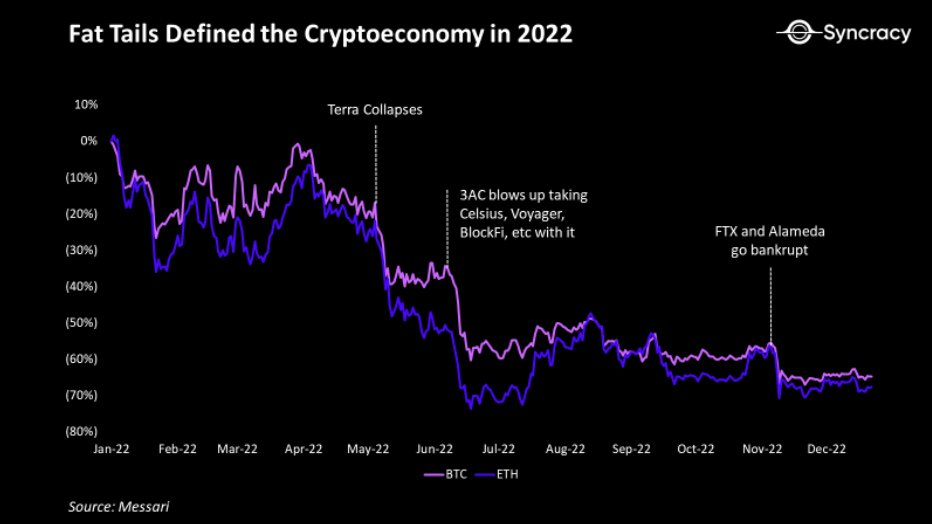

Fast forward to the end of this year and the only succint way to describe what happened is a nuclear bomb hitting the cryptoeconomy. Sweeping bankruptcies, spectacular protocol failures, nauseating hacks, and shocking levels of fraud; the scale and scope of destruction has surpassed anything experienced in prior crypto cycles. What we’re left with is an industry at a crossroads and a feeling of unease in the industry as strong as it's ever been.

I know this all sounds pessimistic, but bear with me. All I can do is keep it real. We must address our past first before we can discuss the light at the end of the tunnel.

The casino era is over and the beginning of a new era is upon us. The choices we make today and values we live by will shape this industry for decades to come.

The Psychology of The Crypto Speculator

“Nothing is easier than self-deceit. For what every man wishes, that he also believes to be true.”

– Demosthenes

There is no single idea that shattered more dreams during the past 18 months than Supercycle. To be clear, everyone believed it, whether explicitly through their words or implicitly through their actions. The thesis was seductive. It suggested the cryptoeconomy had reached a new paradigm where growth was unstoppable and mainstream adoption was inevitable. It promised an unprecedented run of “up only” returns that only the timid and close-minded dared question.

The average speculator was defenseless against this thesis. Already they viewed their tokens as chips in a decentralized casino rather than economic ownership in decentralized networks. Valuations were arbitrary. Intrinsic value was a meme. Every token was a lottery ticket – a chance at life changing riches and financial freedom. The phenomenon came to exist due to:

Excessive religious fervor

Lack of reliable educational resources

Lack of common valuation frameworks

Unprecedented retail access to early stage opportunities

Countless stories of generational wealth creation from nothing

Over a decade of central bank fueled up only returns that reinforced FOMO mentality

The supercycle thesis was rocket fuel to this lottery ticket belief. It not only caused speculators to never sell and double down on every dip, but also take out enormous amounts of leverage to juice their returns. The path to higher prices was preordained, so why not get as long as possible? There was no risk too great to take. Every financial instrument, every strategy on-chain or off-chain to enhance returns was par for the course. This widely shared psychology provided ripe conditions for excess. Even founders weren’t immune as they unleashed a torrent of useless tokens and NFTs on the market to monetize speculators’ greed.

The Great Unwind

Bubbles typically pop due to four common factors: leverage, overly-optimistic projections, heightened fraud and unsustainable business practices, and shifting macroeconomic and interest rate conditions. The crypto bubble was a victim of all four.

Leverage – Like the broader global macroeconomy, the cryptoeconomy was on a leverage binge fueled by easy money. This was the first bull market with a bonafide crypto credit industry. As the bull market raged on, lenders extended credit on increasingly looser terms and credit quality deteriorated. At the peak in November 2021, CeFi loans outstanding reached ~$35 billion, DeFi loans outstanding reached ~$30 billion, and futures open interest reached ~$40 billion, for a combined $105 billion of leverage in the system. Today, this combined number is down over 75% and the entire CeFi lending complex is nearly wiped.

Overly-Optimistic Projections – Look no further than the countless calls for $10,000 ETH, $100,000 BTC, and mass adoption predictions by year-end 2022. To be clear, those price estimates imply $1.2 trillion and $1.9 trillion market capitalizations for ETH and BTC, respectively. That is an enormous amount of credit given the entire asset class has just a 4% retail and 2% institutional holder penetration rate — a statistic that is even less impressive when you consider that the percentage of total wealth both retail and institutions store in cryptocurrencies is a rounding error. And it’s not just that people barely store wealth in these assets either. Daily usage is inherently limited with Bitcoin and Ethereum only being capable of processing a combined ~2 million transactions per day. For this reason, Bitcoin and Ethereum only have a couple million daily active users at best.

Heightened Fraud and Unsustainable Business Practices – These factors have dominated mainstream headlines throughout the year. Light regulation, easy money, and uneducated users provided the prime conditions for these practices. FTX, a once $32 billion institutional darling, ended up being the biggest fraud since Bernie Maddoff. Terra, a once $70 billion ecosystem, propelled to enormous heights by unsustainable mechanism design and incentives, was incinerated in the biggest protocol collapse in the industry’s history. And these two, despite being the largest, were just the tip of the iceberg. With each passing month, even more fraud and unsustainable practices are being uncovered.

Shifting Macroeconomic and Interest Rate Conditions – This was the nail in the coffin. We went from trillions of dollars in fiscal and monetary stimulus and zero percent interest rates to the most hawkish central banks in decades. We now live in a world of aggressive quantitative tightening and 5%+ terminal rate expectations. The 40-year secular decline in interest rates that fueled economic growth and asset price appreciation is over. A new financial reality is setting in.

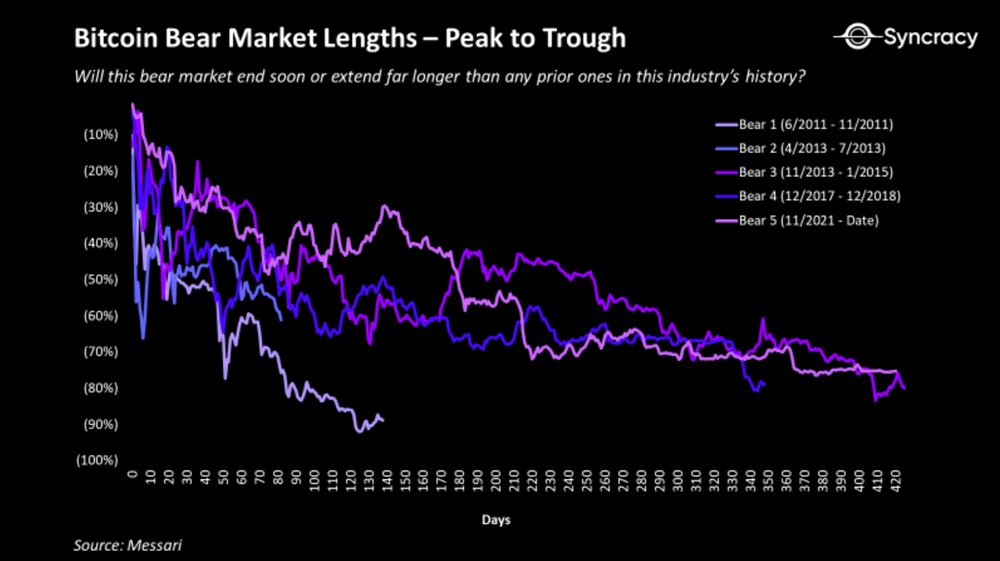

Unwinding is a process, not an event. While we are likely ~90% through the unwinding of crypto’s first credit cycle (can’t be too sure it’s over given there’s no lender of last resort in the cryptoeconomy to prevent further contagion), we are at the precipice of a potential protracted global economic recession and fighting the most hawkish central banks in decades. The direction of the global economy in the coming quarters will likely determine whether this bear market ends soon or extends far longer than any prior ones in this industry’s history. The smartest capital allocators I know are anxious heading into 2023 — the nastiest leg of bear markets is typically the last when the economy finally contracts, businesses go bankrupt, liquidations escalate, and liquidity evaporates. The chances crypto would decouple in this environment are slim. It's all still one trade.

Many people would argue that there’s very little to break in this industry following all the bankruptcies, protocol collapses, and hacks. I agree that most of the forced selling is done with the exception of distributions related to Mt Gox, Silk Road, and Bitfinex totaling ~278,000 BTC (~$4.9 billion) and potential further contagion from FTX. However, I’ve also learned from prior cycles to never underestimate the apathy that follows each bubble popping — people sell when they give up.

If you want to find what’s at risk of breaking next in this cycle, I’d encourage you to take a long look in the mirror.

The Aftermath – Sobriety

Waymond: “You’ve been feeling it too, haven’t you? Something is off. Your clothes never wear as well the next day. Your hair never falls in quite the same way. Even your coffee tastes wrong. Our institutions are crumbling. Nobody trusts their neighbor anymore. And you stay up at night wondering to yourself…”

Evelyn: “How can we get back?”

- Everything Everywhere All At Once

One of my favorite conceptualizations of blockchains is as Single Source of Truth Systems. At their core, blockchains are public digital infrastructure that maintain consistent and truthful views of economic, financial, and social state – society’s remembered information that forms the basis of nearly all our institutions. The big idea is that through managing this state and the conditions for how this state may change, blockchains could underpin a new world governed by transparent, impartial, autonomous code. This code could govern a variety of activities surrounding:

Property rights

Contracts

Identity and reputation

Provenance

Voting

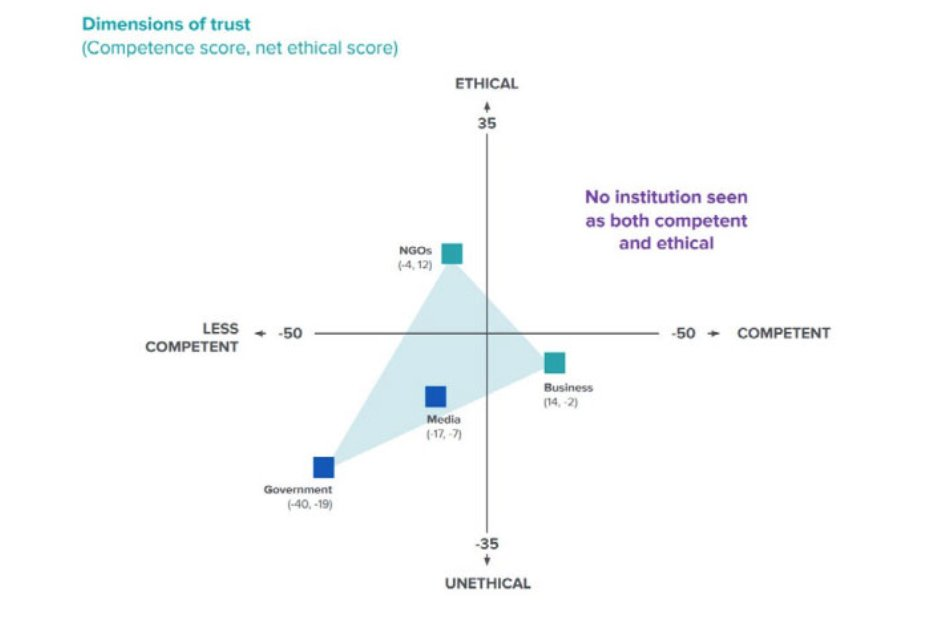

The rise of transparent, impartial, autonomous code in these mission critical areas is incredibly important as trust in institutions continues decling globally. Stability — the backbone of economic growth — is in jeopardy following decades of rising inequality and several critical system shocks including the 2008 financial crisis, 2016 political election cycle, and 2020 Covid pandemic. Fragility in the core institutions of money, finance, technology, and government is threatening a global rise in coordination costs. Blockchains, which may usher in a new paradigm of algorithmic authority, enforced by tens of thousands of independent, open-source, user-run nodes around the world, have the potential to counteract these forces. Blockchains could provide every smartphone user in the world with more trustworthy digitally native institutions.

Rising distrust in institutions isn’t just an abstract societal megatrend either. This “counterparty” risk has very tangible effects on individuals, businesses, and governments worldwide and manifests itself both politically and economically. This year Canadian banks froze the accounts of people protesting vaccine mandates and Russia's central bank reserves were seized by Western governments following its invasion of Ukraine. In years past, Facebook infamously cut the cord on Zynga as their interests grew misaligned and Twitter closed off API access to third party developers to better control the user experience and Twitter’s ability to monetize. The list goes on. Rule of law and property rights in the digital domain are unreliable with powerful centralized intermediaries at the helm and there are serious political and economic consequences.

Source: Edelman Trust Barometer 2020

Initially I thought all the collapses, bankruptcies, hacks, and scams would set this industry back years. It's undeniable that confidence in the industry has been hit hard and there is now greater risk of draconian regulatory blowback. However, the more I thought about it, the more I realized that I was only focusing on the bad.

In reality, it is much easier for this industry to move forward confidently now that the greedy, reckless, and fraudulent went bust. It's also a good thing that there is finally urgency for governments to figure out how to regulate this industry. There are a large number of people and institutions on the sidelines waiting for the green light to dip their toes into the cryptoeconomy. Regulatory clarity will accelerate their arrival.

But perhaps more important than either of these developments is the fact that all these events may have provided the biggest catalyst ever for users, businesses, and governments to embrace the on-chain economy – the economy natively built on this new foundation of trust.

The crux of it is that there was nuance in all the cryptoeconomy’s chaos in 2022. The off-chain economy was littered with principal agent problems. Centralized intermediaries misappropriated assets, behaved recklessly, and committed fraud. In contrast, the on-chain economy was largely secured by transparent, impartial, autonomous code. Smart contact based intermediaries protected users’ rights. Promises made off-chain, enforced by governments, were broken. Promises made on-chain, enforced by smart contracts, were upheld. Simply put, protocols were more reliable counterparties. The difference between the off-chain and on-chain economy was and continues to be that: Companies make promises. Protocols make guarantees.

Moving forward I believe it's inevitable decentralized protocols will eat market share from their centralized counterparts within the cryptoeconomy as users place a higher premium on trust and transparency. If you’re already dealing with blockchain based assets, why rely on government based legal systems to protect your rights, when protocols can protect them with far greater assurances? That’s the point of this all anyway right? “Not your keys, not your coins.”

These assurances and guarantees will become increasingly hard for users and developers to ignore when paired with capital efficiency (lower transaction costs), compounding composability (accelerating innovation), and borderless accessibility (greater scale). The structural reasons for the cryptoeconomy to win have never been more clear. With time the cryptoeconomy will ultimately expand the pareto-frontier of the global economy and enable coordination at unprecedented scale and efficiency.

Of course these applications are still in their early days. Not only are many decentralized applications slow, clunky, and difficult to use, but many are also prone to hacks and unsustainably built. The latter attributes were heavily discounted in the bull market where deploying unaudited code and pumping usage through unsustainable incentives was in fashion. At a certain point during this period, the original design goals of this industry – to build reliable decentralized economic infrastructure – became an afterthought as bull market protocol architects sought returns.

As the industry sobers up following the collapse of Terra and similarly unsustainably designed protocols, I expect sustainable protocol design to once again command a premium. The coming years will be a much less forgiving environment than the past, and protocols that organically bootstrap demand and are designed thoughtfully to become critical infrastructure are positioned to win moving forward. Bet on boring.

The Future – Scalability, Usability, Commercialization

Blockchains sell block space – space on a blockchain that can be used to store information and run code. That space provides assurances that information stored in it is incorruptible and code written to it runs as designed. All economic activity on blockchains settles on block space. However today secure block space is scarce and expensive, limiting the ability of the cryptoeconomy to scale.

Over the next 6 – 18 months the state of blockchain scalability will change dramatically as leading blockchains roll out core protocol upgrades, scalability improvements, and interoperability solutions. I expect the rollout of sufficiently secure, connected, and abundant block space to be a broadband moment for the industry that powers the next generation of applications.

Alongside this expansion of secure block space, I expect the usability of blockchain applications to improve significantly. Technology giants such as Meta are embedding blockchains into their core products and investing upwards of $25 billion per year into the metaverse. Wallet infrastructure is evolving rapidly, especially in the realm of mobile, with key features like multiparty computation, social key recovery, and direct fiat on-ramps soon to become the standard. Account abstraction — an upcoming Ethereum protocol level upgrade — will be a key accelerant to this trend through making user owned accounts programmable and providing wallets with enhanced functionality and customizability. Traditional fintech’s are jumping in on this opportunity as well with some beginning to offer in-app access to on-chain protocols. Protocols like Superfluid and Sablier are making it easier to get paid from smart contracts, providing the infrastructure to support working on-chain. Payments protocols are making it easier for merchants to transact in stablecoins. Data providers are shining a light on the rich data of the cryptoeconomy, empowering stakeholders to make better decisions. The list goes on. Blockchains are about to become orders of magnitude more usable as both retail and institutional infrastructure rapidly matures.

With faster, more scalable blockchains and smoother and safer user experiences, the wave of new talent and capital that entered the industry over the past two years will finally be able to develop blockchain applications ready for mass adoption. Already today we see the green shoots of the mainstream applications of tomorrow that are achieving impressive feats relative to their centralized counterparts. We also see the early signs of scalability making a difference with Ethereum L2s now handling more transactions than Ethereum main chain. And we continue to see cryptocurrencies being adopted on the margins in developing economies that lack reliable monetary and financial infrastructure. Non-sovereign digital money and stablecoins are already making a difference in these markets despite the UX hurdles.

All in all, the setup to onboard new users to the cryptoeconomy has never been stronger.

Source: Ryan Selkis

The Path Ahead – Controlled Aggression

“The way to build superior long-term returns is through preservation of capital and home runs” - Stanley Druckenmiller

I came into 2022 disgusted at the state of the cryptoeconomy. Today I am no longer disgusted and believe the risk reward favors controlled accumulation in the coming quarters. However, while the time to sell everything has long passed, this is still a market that favors patience over bravery. Regime change can be brutal as global markets rapidly reprice every asset class for a new financial reality. Staying nimble and adaptive in this environment still is the highest priority. The last thing you want to do is make a fatal mistake before the next big dance. Now is the time to begin thinking long-term, cautiously.

2023 will likely be a very favorable environment for convicted, long-term buyers. Syncracy’s expectation is that markets will be choppy for the next 6 - 12 months with directional bias still leaning to the downside. Idiosyncratic risk in the cryptoeconomy has decreased substantially following all the major bankruptcies, creating an opportunity for this bear market to begin its apathy phase. With clarity closer in sight, we may finally have the conditions for a firm bottom. Contagion risk from FTX still looms, however further dominoes are likely to be footnotes unless DCG, Tether, or Binance blows up.

DCG is at highest risk of bankruptcy as has been publicly revealed following the collapse of FTX while Tether and Binance appear to be fine at this moment. I’m not betting on either Tether or Binance running into any serious issues, but I do expect both will come under pressure in 2023. Tether has notoriously managed their reserves aggressively throughout its history and continues to see outflows as yields in TradFi rise and the desirability of holding yield-less stablecoins dwindles. If there was ever a time for their aggressive reserve management practices to bite them in the ass it would be during the climax of this bear market in the broader global economy. I’m the least concerned about solvency issues with Binance, despite their questionable transparency. However, Binance is notorious for being a renegade offshore exchange and I expect that governments will be far more aggressive towards it post-FTX, especially given its dominance.

Nevertheless, idiosyncratic risk in the cryptoeconomy is no longer the primary worry regarding market direction. Broader financial markets will provide a massive overhang as global recession risk rises and the world comes to terms with structurally higher interest rates and tighter liquidity. This overhang will largely be driven by shifting monetary policy and will continue to pressure crypto valuations which have not yet fully rationalized — lazy percentage down from ATH and relative valuation analyses aren’t enough justification given we were so far removed from reality in 2021. There’s still over 50 projects trading north of $1 billion valuations and that figure doesn’t even include private markets. I’m as optimistic long-term on this industry as anyone, but I personally find it incredibly difficult to believe the cryptoeconomy has produced that many unicorns. This is an industry that still struggles to provide tangible, widely discernible proof points of its value after all. Remember it’s all one trade, and if broader financial markets still have their nastiest leg down ahead of them, crypto will not be spared.

That said, the beauty of this environment is that it provides a ton of time to build conviction and accumulate high quality assets. As explained previously, the structural advantages of blockchain based applications have never been more clear. With valuations having come down so low there is little need to assume unnecessary illiquidity or be contrarian when the most sure-fire, category leading protocols are trading publicly at bargain prices. This is a generational environment for fundamentally oriented asset pickers. The next generation of globally dominant platforms are scaling.

For additional perspective, after Bitcoin bottomed at $3,156 last cycle in December 2018, investors had 111 days to buy it under $4,000. This came after 355 days of unrewarded dip buying as Bitcoin trended lower and lower with each passing month – and this was in a significantly more favorable macro regime. Remember, the goal is to make it to the next big dance, not to be a hero. The most money is made in catching the meat of the move, not buying the bottom or selling the top. Pacing is essential.

Prices and Crises – The Light at the End of the Tunnel

Financial markets are a peculiar thing. On the surface, it can often appear as if they’re a sideshow – a zero sum game veiled over the real economy. After all, traders don’t build anything, builders do. Yet in reality the idea that financial markets are a zero sum sideshow couldn't be further from the truth.

At its core, finance structures uncertainty and gives form to the open ended system of promises we make to each other about the future. These relationships aren’t mediating something else on the “real” side of the economy; they are the constitutive relationships of the economic system. Financial markets don’t matter to the cryptoeconomy just because they can make you rich or poor, they matter because they reflect the perceived confidence in the promises made between its stakeholders.

In 2021, financial markets provided the cryptoeconomy with an enormous amount of new attention, users, capital, and talent. However, confidence eventually stretched too far beyond reality and eventually sowed the seeds of fraud, grift, and opportunism. In 2022, this confidence reached its peak and financial markets violently reversed, catalyzing a nasty reset of all the cryptoeconomy’s businesses and infrastructure that couldn’t live up to their lofty promises. As confidence collapsed, the industry was jolted with a much needed reminder of what matters. In 2023, financial markets will likely continue to be an overhang on the industry causing attention, users, capital, and believers to dry up. But the overhang will likely also provide the conditions ripe for the ecosystem to refocus on itself and on driving tangible adoption — the path to restoring that confidence once again. It should be clear then that financial markets aren’t just a sideshow, they are an intrinsic part of the game we’re all playing.

If you survived all the bankruptcies, collapses, hacks, and scams this year you deserve all the glory on the other side of this. I firmly believe that one day we will look back on this period as the end of the beginning – the defining moment where this industry made a choice whether to die in its cradle as a niche technology or grow up and reach the masses. The path to mainstream adoption won’t be smooth and is certainly not guaranteed, but I’m confident there are enough intelligent and committed people in the industry to make it happen. Despite growing pains, the vision of the cryptoeconomy has never been more clear.

Stay happy, healthy, and engaged as we settle into winter. The hardest part over the next 6 - 12 months will be keeping a level head as we grind through this challenging period. I hope you're all prepared for what comes next. I know Syncracy is. Bear markets are where legends are made.