Author: Hotcoin Research

Introduction

The TGE of Lighter on December 30, 2025, once again brought the Perp DEX track into the spotlight, marking the conclusion of the competition for on-chain perpetual contracts in 2025: at the beginning of the year, Hyperliquid dominated with over 70% market share; in the second half of the year, with the rise of new Perp DEXs with distinct features such as Aster, Lighter, and EdgeX, Hyperliquid's market share dropped to around 20%, entering a new stage of comprehensive competition involving technology, capital, incentives, and real demand.

This article will start from the background and development of the Perp DEX track, analyze the market landscape and key data in 2025, and review and analyze five representative Perp DEX protocols: Hyperliquid, Aster, Lighter, EdgeX, and Paradex, providing a comprehensive analysis from different dimensions such as background team, technical architecture and features, token economics, market data, and performance. It will further explore the risks and opportunities in the track and look ahead to the trends in 2026.

I. Background and Development of Perp DEXs

The early on-chain derivatives market was very small. Centralized exchanges (CEXs) long dominated derivatives trading, offering excellent user experience, deep liquidity, and one-stop services, but their centralization also harbored risks: the industry turmoil in 2022-2023, especially the successive blowups of giants like FTX, made users increasingly aware of custody risks and black-box operation hazards, prompting capital and traders to seek decentralized alternatives, which laid the demand foundation for the explosion of the Perp DEX track.

However, performance bottlenecks have always been a constraint on the development of on-chain perpetual contracts: on-chain matching and settlement are often limited by blockchain throughput and latency, leading to high slippage and insufficient depth. To overcome this, early projects explored various paths: for example, dYdX used an order book but relied on off-chain matching (now migrated to its own chain), while GMX adopted an on-chain multi-asset pool market-making model, offering perpetual trading but with liquidity constrained by pool size. Although these pioneers proved the feasibility of on-chain perpetuals, they did not truly challenge CEXs in terms of trading experience and scale.

In recent years, the development of Ethereum Layer2 and application chains has provided the foundation for high-performance contract exchanges, bringing latency and throughput to unprecedented levels. Hyperliquid built a dedicated Layer1 blockchain designed for derivatives, while EdgeX, Paradex, and others leveraged Layer2 technologies like StarkWare to achieve on-chain trading experiences of seconds or even sub-seconds. Coupled with incentive mechanisms like trading mining and airdrop points to attract users,

the Perp DEX track entered a period of rapid iteration in 2024-25. In 2024, Hyperliquid gained popularity first, with its HYPE token airdrop and buyback plan driving a surge in its locked value and trading volume, once capturing 80% of the on-chain perpetual market share. In 2025, with the launch of several new platforms and aggressive market strategies, the monopoly of Hyperliquid in the Perp DEX track was broken, officially entering a stage of fierce competition among various players.

II. Current State of the Track and Data Performance in 2025

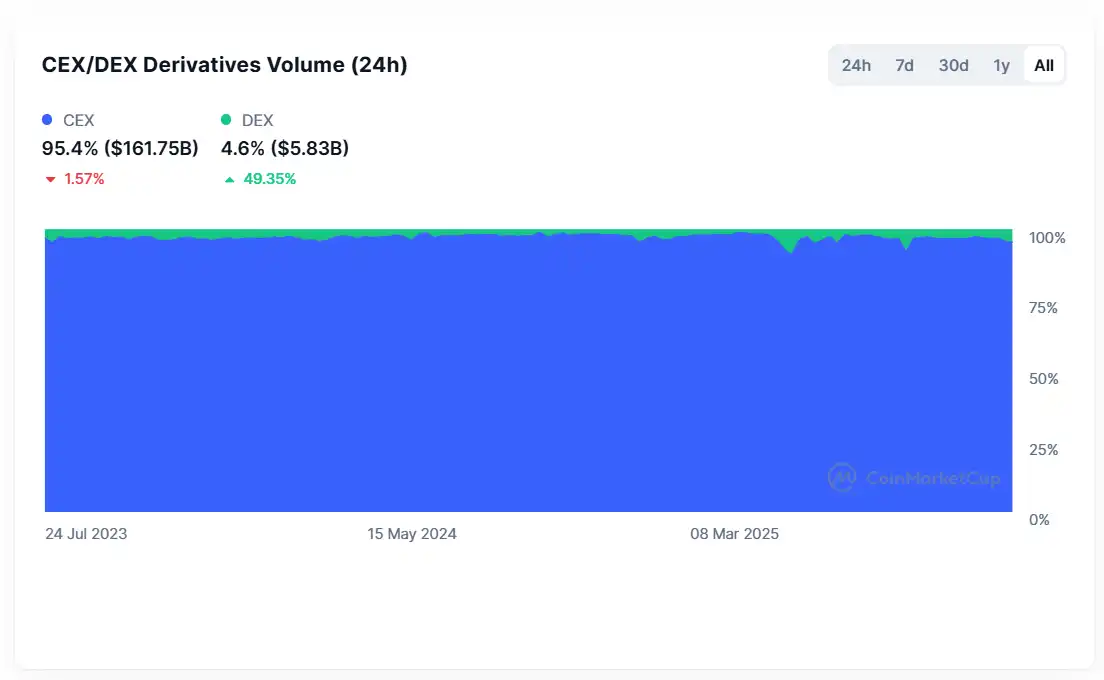

The overall scale of on-chain perpetual contract trading achieved a quantum leap in 2025. The monthly trading volume of perpetual contracts exceeded $1 trillion, and its proportion in the crypto derivatives market increased rapidly. The trading volume of on-chain perpetual contracts once reached 1/10 of that on centralized exchanges, beginning to pose a substantial challenge to the centralized giants. Particularly, during the extreme market conditions on October 11th, on-chain DEXs handled $19 billion in position liquidations within a short period while operating stably overall. These data indicate that Perp DEXs have grown from a niche testing ground to an indispensable part of the derivatives market.

Source: https://coinmarketcap.com/charts/derivatives-market/

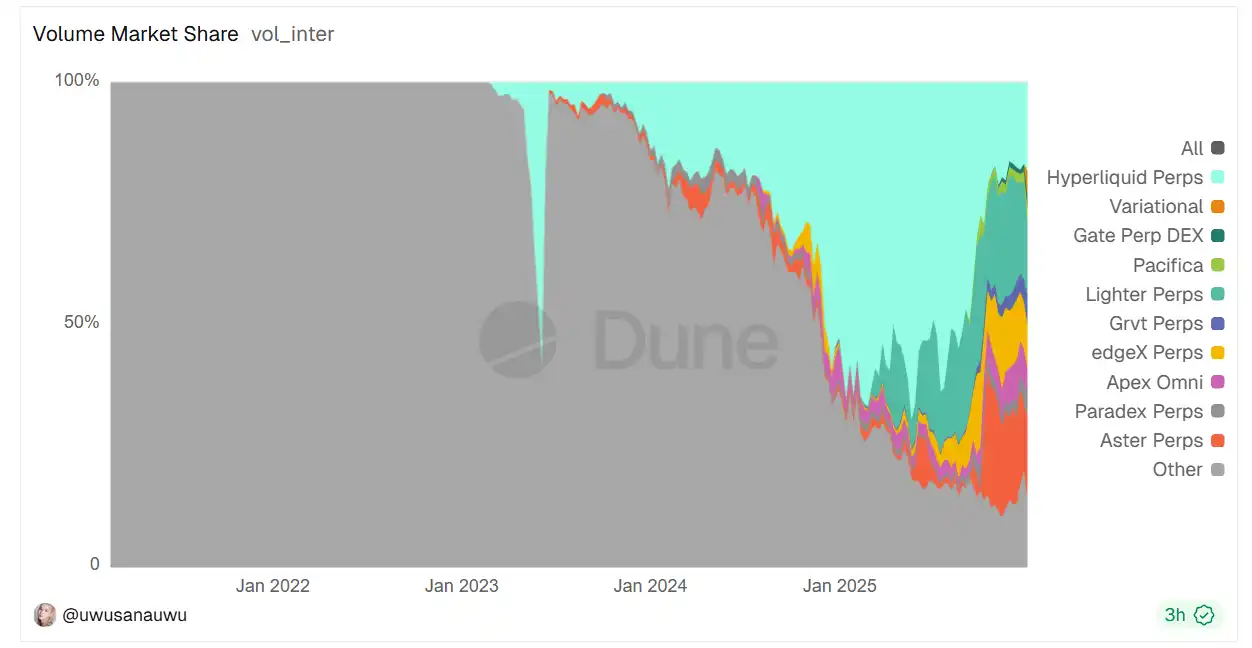

In terms of market structure, Hyperliquid steadily held the top position in the first half of the year, accounting for about 70% of on-chain perpetual volume. However, with the entry of newcomers in the second half, its share declined continuously. According to analytical data on Dune, Hyperliquid's trading volume share had dropped to 17% by the end of December. This was replaced by a new pattern of competition among several strong players: Lighter quickly attracted a large number of high-frequency traders with its zero-fee strategy, achieving a 20% volume share in December; Aster gained a 15% market share through continuous incentives and support from Binance; EdgeX, focusing on stability and professionalism, also captured about 10% of the share. Additionally, latecomers like Paradex, GRVT, and Pacifica divided the remaining share, further weakening the dominance of the leader. It can be said that in the second half of 2025, the competition for users and liquidity among new and old platforms in the Perp DEX track intensified.

Source: https://dune.com/uwusanauwu/perps

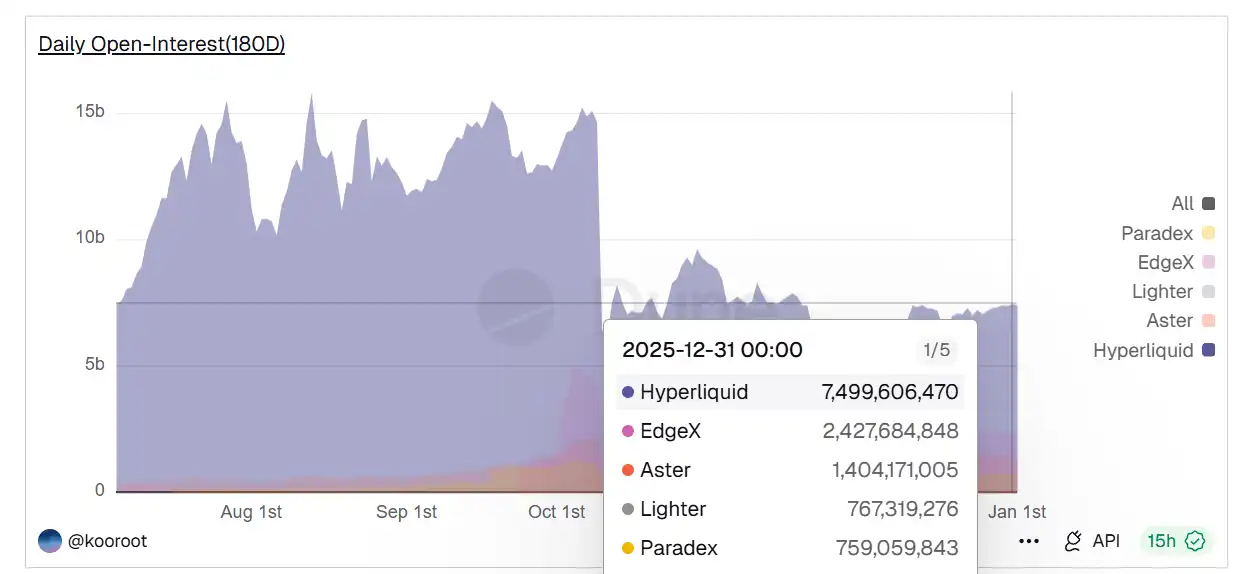

However, looking at the Open Interest (OI) indicator, data as of the end of December showed that Hyperliquid remained the undisputed leader in terms of OI, with an open interest size of about $7.5 billion, accounting for 49% of the total OI of the top four platforms, indicating that nearly half of the on-chain real positions remained on Hyperliquid. This shows that Hyperliquid still holds a structurally leading position in trading depth and capital沉淀, while the huge trading volumes of newcomers like Aster and Lighter were largely driven by frequent counter-trading for incentives rather than long-term capital investment.

Source: https://dune.com/kooroot/top5-perpdex-comparison

There is also a clear divergence in terms of revenue and profitability within the track. As many new platforms adopted zero-fee or significant rebate strategies, real fee income better reflects "hematopoietic" capability. Apart from Hyperliquid, EdgeX is one of the few projects that has achieved sustainable high revenue: its monthly fee income exceeded $20 million, with an annualized rate of about $250 million, second only to Hyperliquid. Platforms like Paradex and Extended also showed certain revenue potential. However, models like Lighter's zero-fee strategy to capture market share generated almost no fee income; its short-term trading volume topped the charts but protocol revenue was zero, and its profit model remains to be verified after the airdrop. Clearly, some new platforms are exchanging capital for market share, and whether they can truly establish commercial sustainability remains questionable.

III. Review of Representative Perp DEX Protocols

Based on trading volume and open interest rankings, the current Top 5 protocols in the Perp DEX track include Hyperliquid, Aster, Lighter, EdgeX, and Paradex. Below, we will analyze the performance of these five representative Perp DEX protocols from different dimensions such as background team, technical architecture and features, token economics, market data, and performance.

1. Hyperliquid — The King of On-Chain Derivatives

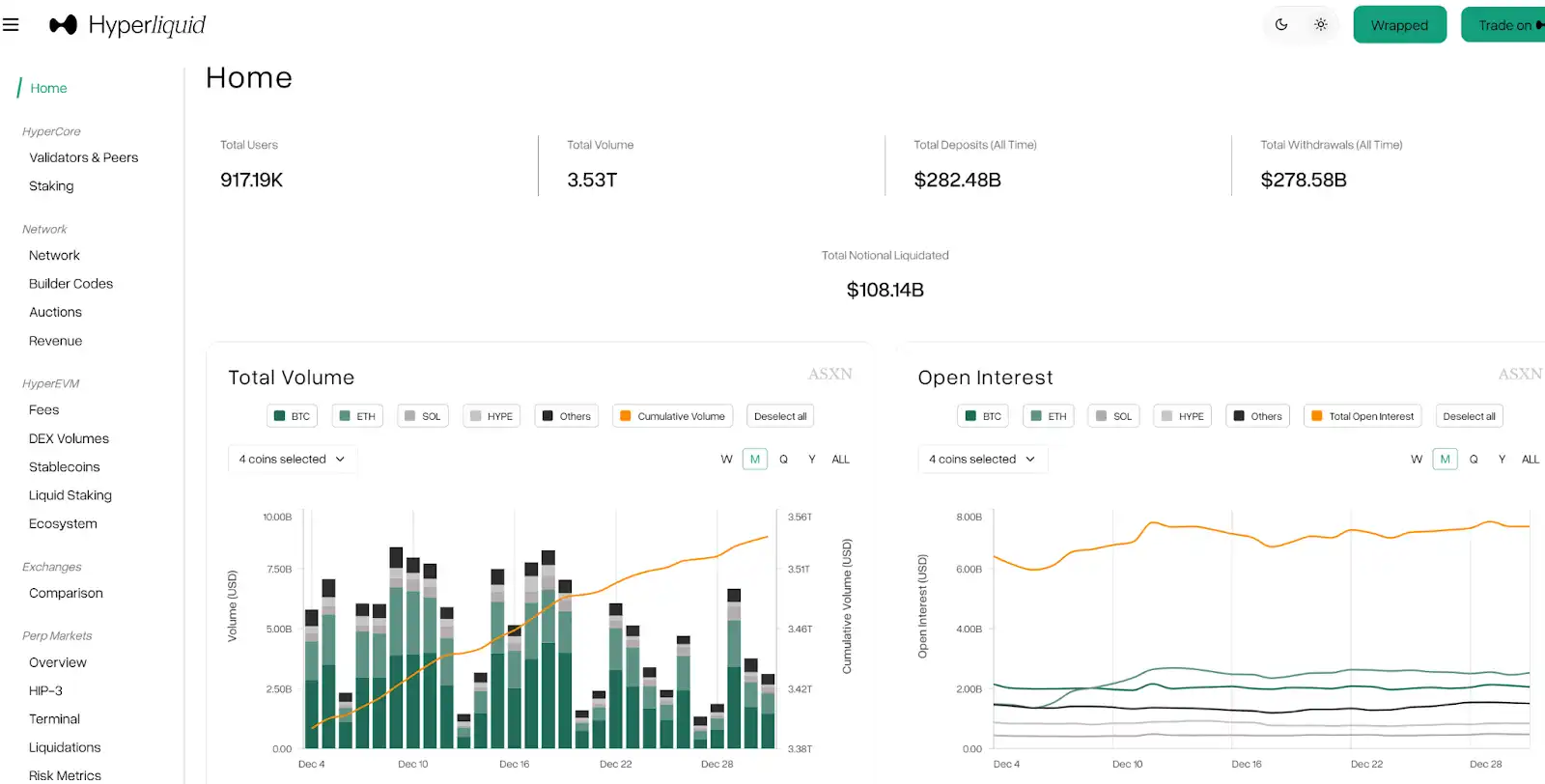

Source: https://wrapped.hyperscreener.asxn.xyz/summary

Background & Team: Hyperliquid was founded in 2023 by Jeff Yan. The initial team had only 11 members but built a "phenomenal" on-chain derivatives platform in less than two years. Hyperliquid was completely self-funded from the start, adhering to a community-driven path. This self-reliant development approach is rare in the crypto space but earned Hyperliquid a reputation for being "decentralization-native." The project did not engage in excessive market hype when it launched in July 2023; it only gradually entered the public eye in 2024 through large-scale airdrops and impressive data.

Product Features & Technology: Hyperliquid's biggest differentiation lies in its self-developed dedicated blockchain, with theoretical performance reaching 200,000 transactions per second and sub-second order confirmation latency. Hyperliquid deployed core modules like Central Limit Order Book (CLOB) matching and liquidation entirely on this high-performance chain. Users experience a front-end interface and matching efficiency similar to Binance, but the underlying settlement is fully decentralized and requires no KYC. Additionally, Hyperliquid plans to launch the HyperEVM, a universal smart contract platform, to host more applications. The officially promoted HLP Vault plays a market-making role for the platform: acting as the counterparty in a large number of transactions and earning a portion of the fees, funding rates, and liquidation profits. Its current TVL exceeds $390 million. This model effectively enhances platform liquidity and user stickiness, creating a win-win cycle for retail users and market-making capital.

Token Economics & Incentives: Hyperliquid's governance token HYPE, was introduced via an airdrop in early 2024. The allocation is highly tilted towards the community, with 70% of tokens reserved for the community (airdrops, mining, etc.). The platform also commits to using all fee revenue to repurchase and burn HYPE, directly converting protocol growth into token value support. This model led to a rapid expansion of HYPE's market cap after its launch. As of the end of 2025, the circulating market cap of HYPE token was approximately $8.2 billion, ranking 15th among cryptocurrencies.

Data & Performance: Although Hyperliquid faced challenges in trading volume share in the second half of 2025, it still firmly resides in the top tier based on key quality metrics. The platform's 24-hour trading volume consistently maintained between $3-10 billion; its open interest size long accounted for over half of the entire network. In terms of trading depth and liquidity, Hyperliquid's BTC perpetual could accommodate about $5 million in positions within a ±0.01% spread. Stability-wise, the Hyperliquid platform has not experienced any major technical incidents to date, operating without downtime even during the liquidation peak on October 11th. Overall, Hyperliquid demonstrated deep-rooted dominance in 2025: despite being overtaken in trading volume by newcomers, its solid technology, genuine liquidity, and healthy economic model keep its king status unshaken.

2. Aster — The Soaring Dark Horse and Trust Crisis

Source: https://www.asterdex.com/

Background & Team: Aster is a multi-chain perpetual contract exchange launched in early 2025, formed from the merger of Asterus and APX Finance. YZi Labs participated in early support, and CZ endorsed Aster multiple times on social media. This gave Aster a halo from birth. Its goal is to build a high-speed derivatives platform supporting deployment on multiple chains like BNB Chain, Ethereum, Arbitrum, and Solana, allowing users to trade assets from different chains without cumbersome cross-chain processes.

Product Features & Technology: Aster has commendable aspects in its product. First is its multi-chain deployment: it provides trading portals on chains like BNB Chain, Ethereum, Arbitrum, and Solana. Users can trade cross-chain through a unified account without tedious chain transfers. Secondly, Aster offers an astonishing leverage of up to 1001x, along with advanced features like hidden orders, catering to high-risk appetite users. Additionally, its planned Aster Chain is a dedicated chain based on zero-knowledge proofs, beneficial for enhancing transaction privacy and efficiency. Also, Aster allows users to earn yield on part of their collateral, and position margins can accrue interest, improving capital efficiency.

Token Economics & Incentives: The total supply of ASTER tokens is 8 billion, with airdrops accounting for a high 53.5%, ecosystem and community 30%, and team 5%. The original design involved monthly ecosystem unlocks, causing continuous selling pressure from the increasing circulating supply. In October, the Aster team announced modifications to the tokenomics, delaying a large portion of tokens originally scheduled for unlock in 2025 to summer 2026 or even 2035, but the market seemed unconvinced. Currently, the ASTER token price fluctuates around $0.7, significantly down from its peak.

Data Performance & Controversy: In September 2025, Aster launched its mainnet and the ASTER token. The token price surged from an issuance price of $0.08 to $2.42 within a week, a staggering increase of 2800%. The platform's daily trading volume also briefly climbed to $70 billion. From late September to early October, Aster,凭借疯狂的交易活动, briefly captured over 50% of the market share, becoming a veritable dark horse. Many investors saw Aster as the next Hyperliquid, hoping it would replicate the former's myth. However, on October 5th, the authoritative data aggregation platform DeFiLlama announced the delisting of Aster's data, citing "discovery that its trading volume was almost completely synchronized with Binance, indicating serious anomalies." Furthermore, Aster refused to provide backend trading data to DeFiLlama to prove its innocence. On-chain tracking revealed that 96% of ASTER tokens were concentrated in 6 wallets, and its trading volume/OI ratio was as high as 58, clearly indicating frequent wash trading to inflate volume. After the news broke, the ASTER price plunged over 10% that day, and its brand credibility was questioned.

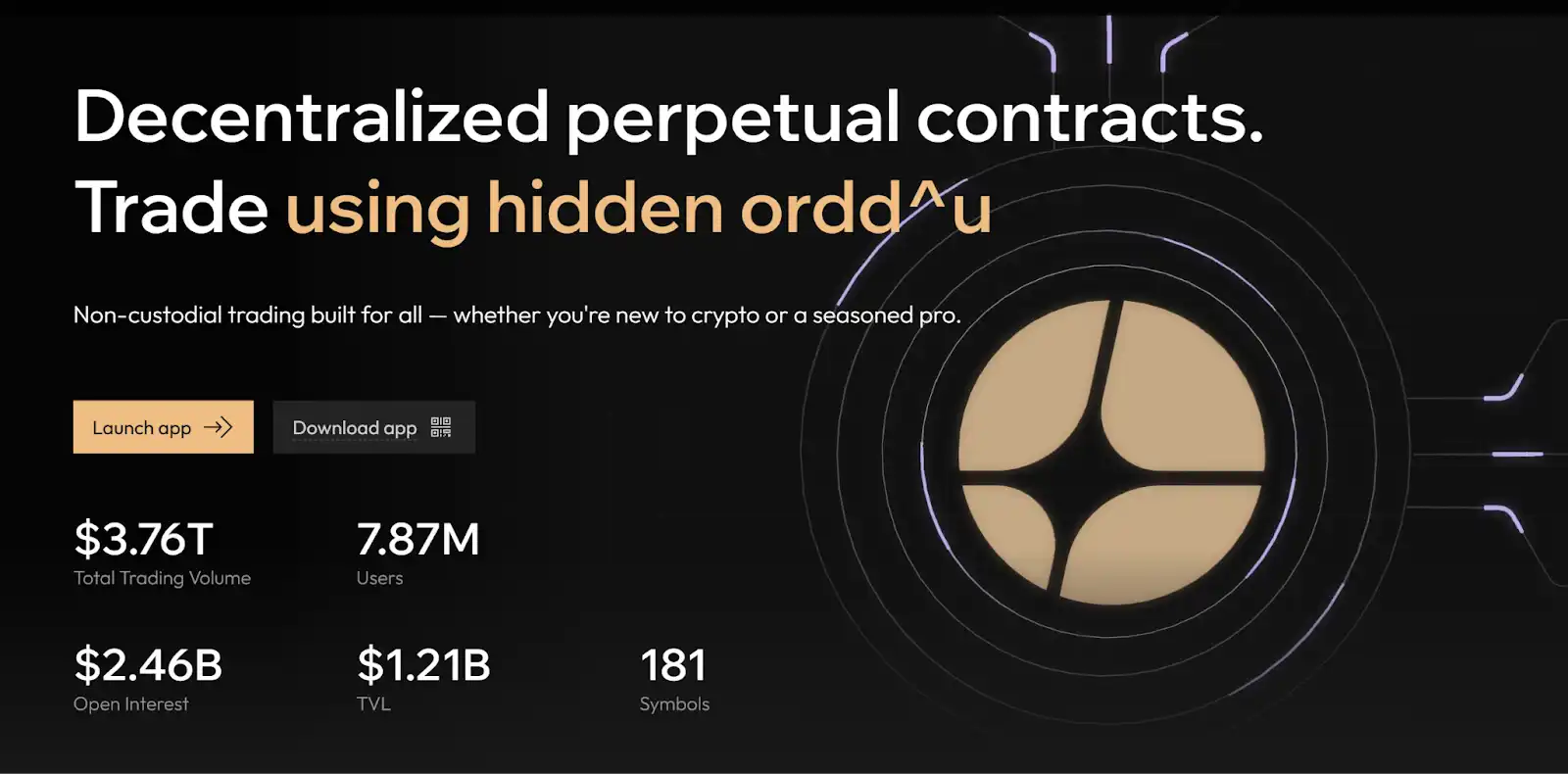

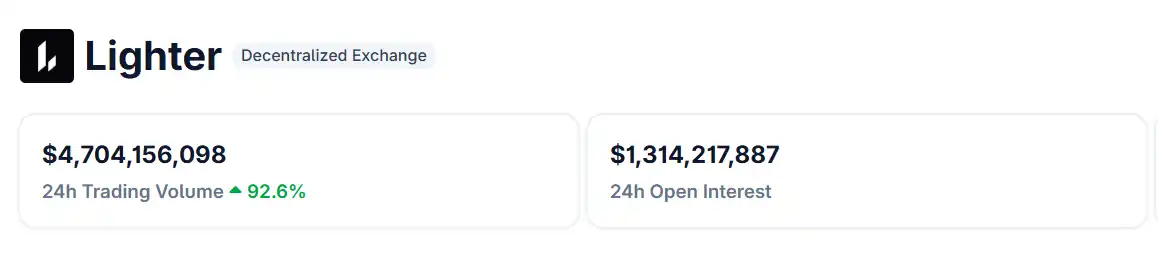

3. Lighter — The Zero-Fee Technology Disruptor

Source: https://www.coingecko.com/en/exchanges/lighter

Background & Funding: Lighter was a dark horse that entered the on-chain perpetual track in 2025. The core team was created by former Citadel hedge fund engineers, backed by top-tier investment institutions like Peter Thiel, a16z, and Lightspeed, raising $68 million in a seed round with a post-money valuation of $1.5 billion. Strong capital backing also gave Lighter ample development resources initially. Lighter officially launched on October 2, 2025. The name "Lighter" implies "lighter and faster trading experience," reflecting the team's technical strength and ambition.

Product Features & Technology: Lighter chose to build on a ZK Rollup, fully utilizing the security of the Ethereum mainnet while achieving scaling through Layer2. A key technical highlight is that each transaction uses zero-knowledge proofs for encrypted verification to ensure transaction data privacy and validity. A solution provided by StarkWare was used to accelerate proof generation, allowing the platform to achieve high-frequency matching while ensuring security. Additionally, Lighter designed a unique "escape hatch" mechanism: if the L2 platform itself fails, users can withdraw funds back to the mainnet through pre-deployed smart contracts, avoiding funds being trapped for extended periods. Overall, Lighter's technical route choice is very bold, aiming to achieve a great leap in performance without compromising security and decentralization.

Token Economics & Incentives: The token $LIT had its TGE on December 30, 2025. 50% is allocated to the ecosystem (of which 25% was directly airdropped, converted 1:20 from points), and the other 50% goes to the team and investors (with vesting lock-ups). Protocol revenue will be used to repurchase LIT or for ecosystem incentives, aiming to align community and project interests in the long term. The latest price on January 3, 2026, was $2.50, with a circulating market cap of $650 million and an FDV of $2.6 billion.

Market Performance & Controversy: Lighter adopted an aggressive zero-fee strategy to attract users externally, charging 0% transaction fees for both makers and takers, with protocol revenue coming entirely from HFTs and market makers. In terms of results, Lighter's zero-fee strategy worked. Within just weeks of launch, the number of users surged to 56,000+, and daily trading volume stabilized at $7-8 billion. A large number of arbitrageurs and quantitative teams flocked to trade, making it the top on-chain DEX by trading volume. However, Lighter's Vol/OI ratio once exceeded 8, meaning most capital was frequently used for opening and closing positions in cycles rather than holding long-term. Once the airdrop ends, this speculative flow could disappear instantly. The highly aggressive expansion also tested Lighter's system stability. In mid-October, the platform was down for about 4 hours, during which users could not place orders or withdraw. Lighter's LLP fund pool suffered a loss of about 10%, exposing shortcomings in Lighter's system stability and risk control under extreme market conditions. Additionally, the platform experienced UI lag and minor bug reports during peak hours, somewhat affecting the user experience.

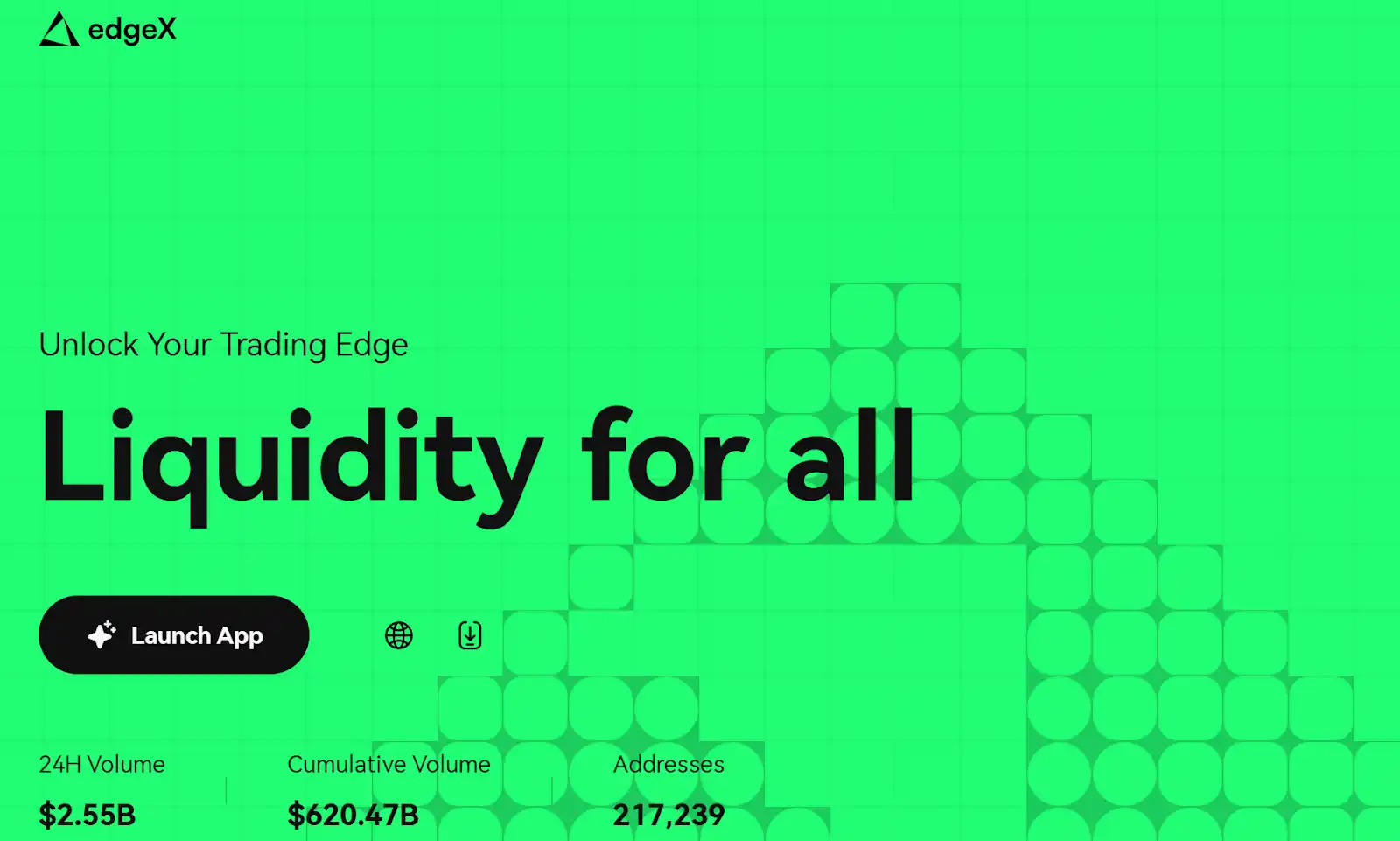

4. EdgeX — The Institutional-Grade Stable Exchange

Source: https://www.edgex.exchange/

Background & Team: EdgeX is a professional perpetual contract platform incubated by Amber Group, a top Asian crypto financial institution, launched in September 2024. EdgeX carries TradFi genes, built by a group of experts proficient in institutional services. Amber Group, as an established market maker managing around $5 billion, not only provided seed funding but also injected deep liquidity support and market operation capabilities into EdgeX, attracting attention in institutional circles and the Asian market upon launch.

Product Features & Technology: EdgeX is built on StarkWare's StarkEx engine, adopting a hybrid model of centralized matching + decentralized settlement: order matching is executed on StarkEx, and transaction results are batched on-chain. EdgeX promotes low fees + deep liquidity as its selling points, with fee rates slightly lower than Hyperliquid across the board: maker 0.012% (HL 0.015%), taker 0.038% (HL 0.045%). In terms of liquidity, thanks to Amber Group's support, the order book depth and spreads on the EdgeX platform are excellent. Data shows that within a ±0.01% range, EdgeX's BTC perpetual can accommodate $6 million in positions (better than HL's $5 million), and slippage for various mainstream trading pairs is generally smaller than competitors. Additionally, EdgeX places great importance on the mobile experience: it launched a comprehensive iOS/Android APP integrated with technologies like MPC wallets, allowing users to use it without remembering seed phrases, significantly lowering the barrier to entry.

Token Economics & Incentives: EdgeX has not yet issued a platform token, EGX. To compensate for the lack of a token, EdgeX also designed a transaction points reward mechanism, but it is relatively transparent and restrained. The source of points allocation is clear: 60% trading volume, 20% referral, 10% TVL/LP, 10% liquidation/OI, and it publicly states that it absolutely does not reward wash trading. User expectations for the future EGX token are also relatively rational. The community predicts that EdgeX will allocate about 20-35% of tokens to points holders during TGE.

Market Data & Performance: EdgeX's performance in 2025 was commendable, aptly described as "steady growth." According to CoinGecko data, EdgeX's 24H trading volume is about $2.5 billion, and OI is about $1.3 billion, ranking fourth among Perp DEX platforms. Although its trading volume market share is only 5-6%, EdgeX's annualized revenue is about $500 million, second only to Hyperliquid. In short, EdgeX wins with stability and professionalism, excelling in all aspects but without absolute standout features. Its late token issuance means it remains to be seen how it will attract attention after missing the airdrop frenzy.

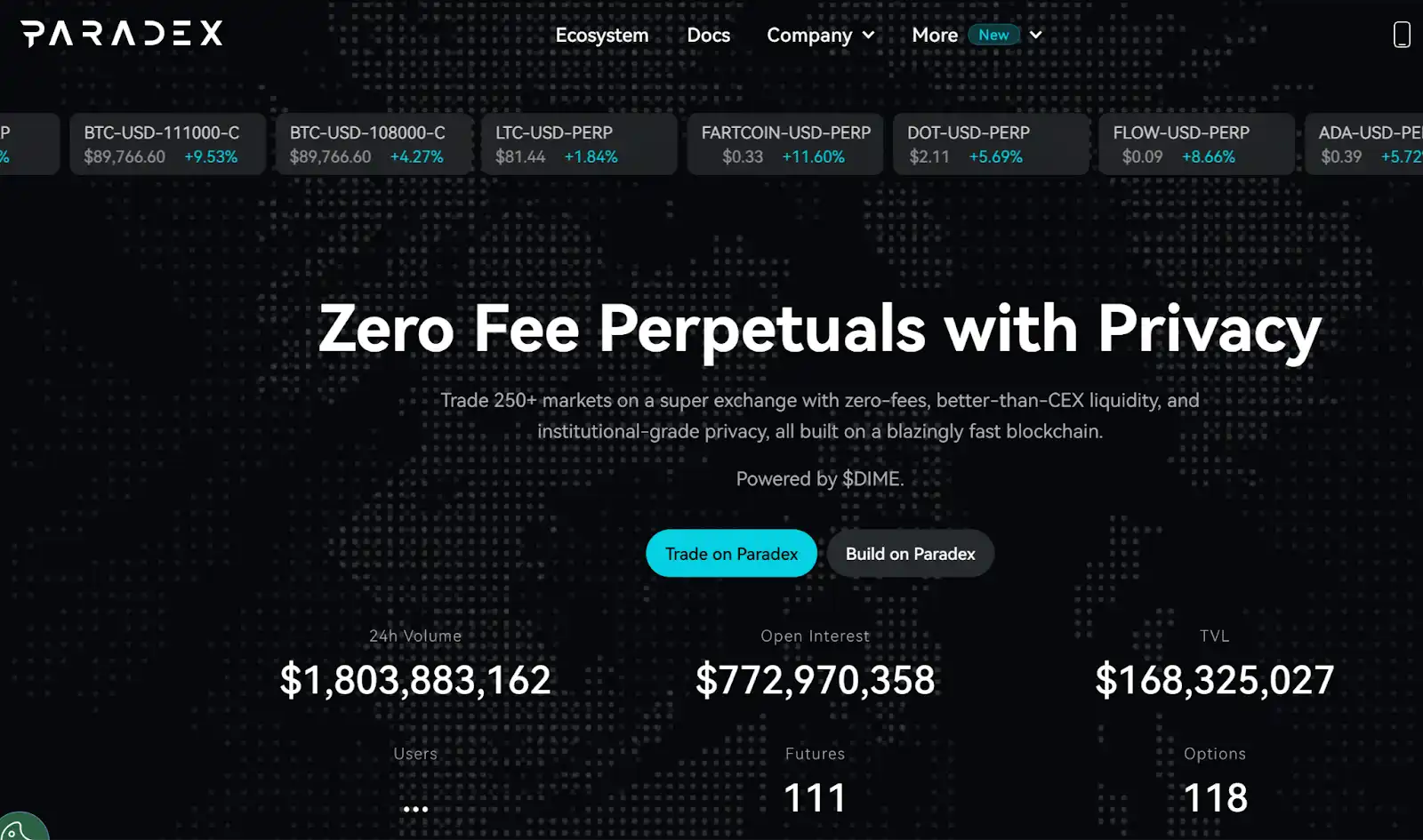

5. Paradex — The Full-Featured On-Chain Derivatives "Super DEX"

Source: https://www.paradex.trade/

Background & Team: Paradex was incubated by Paradigm, a crypto institutional trading network. Founded in 2019, it initially focused on serving institutions like hedge funds and market makers, providing OTC option matching services and once capturing 30% of the global crypto options market. In early 2025, Paradex launched its testnet, gradually opening public access mid-year, positioning itself as a high-performance decentralized trading and asset management comprehensive platform.

Product Features & Technology: Paradex built its dedicated Ethereum Layer2 blockchain, Paradex Network, based on the Starknet framework, supporting highly customized on-chain parameters. Paradex web trading is fee-free for all markets except BTC/ETH, and professional users accessing via API are charged only a 0.02% taker fee, with no maker fee. Paradex also plans to launch perpetual futures, perpetual options, and spot products in the future. All trades are settled through a unified account and support isolated margin, cross margin, and even portfolio margin modes. Paradex also embeds a series of DeFi asset management functions, supporting direct lending within the same account to improve capital efficiency. Furthermore, Paradex may introduce private trading modes in the future to meet the needs of some institutional users who do not want to disclose their positions. In short, while other perpetual DEXs compete on incentives and performance, Paradex takes a different path with product innovation, striving to form a fully functional, diversified on-chain exchange.

Token Plan & Incentives: Paradex has not yet issued a token, but the official has announced the token economics: 26.6% for continuous community rewards, 6% for foundation budget, 25.1% for core team, 3.8% for future contributors, 13.5% for Paradigm shareholders, etc. The platform token is named DIME and has multiple uses: as Gas fee for Paradex Chain, transaction fee discounts, staking rewards, liquidity mining, and governance voting, serving as the value carrier throughout the entire ecosystem. Paradex announced that it will launch DIME in 2025 and allocate 20% of tokens for a genesis airdrop. Paradex's points incentives are relatively moderate and transparent, with no outrageous wash trading现象 observed. Its Vol/OI ratio is typically around 1-2, close to normal levels like Hyperliquid. The official repeatedly emphasizes focusing on long-term value rather than short-term speculation.

Market Data & Performance: The Paradex platform TVL is approximately $170 million, with a daily trading volume of about $2 billion and OI of about $770 million. These figures are still relatively small compared to giants like Hyperliquid, but growth is steady without major fluctuations. Paradex has a good reputation among professional derivatives traders, especially favored by some users looking to explore on-chain options and advanced strategies. Its product line is still expanding rapidly: according to the official X account, spot trading will be launched in mid-to-late January 2026, followed by heavyweight developments like community-created meme token trading and the DIME token issuance. If its "unified account, all-in-one trading" model operates successfully, it will form a differentiated competitiveness in the track.

IV. Analysis of Opportunities and Risks in the Perp DEX Track

1. Opportunities Facing the Perp DEX Track

1) Large room for market penetration increase: Although on-chain perpetual trading volume surged in 2025, its proportion relative to the entire crypto derivatives market is still low, about 5-10%. The vast majority of contract trading still occurs on centralized platforms, like Binance's single-day futures volume in the trillions. As decentralized trading experience approaches CEXs, user demand for avoiding centralization risks and enjoying self-custody freedom will continue to grow. In the coming years, on-chain derivatives are expected to further capture market share. Even an increase to 20-30% would mean several-fold growth in trading volume for current DEXs.

2) New technology红利 empowers the track: Technologies like ZK proofs, sharding, and notary networks continue to mature, pushing on-chain performance to new levels, reducing usage costs, and expanding product boundaries. For example, the perpetual options planned by Paradex are made possible by underlying technological breakthroughs. It is reasonable to believe that the compound effect of technology will continue to help decentralized exchanges narrow the gap with centralized giants, even creating new product forms that the latter lack.

3) User education and habit changes: After experiencing events like FTX, the new generation of crypto users has a higher acceptance of DeFi products. Many users who previously only traded contracts on Binance and elsewhere tried Hyperliquid, EdgeX, etc., in 2025 and left positive reviews. As word spreads and KOLs drive adoption, on-chain trading is moving from a small circle to the masses. This means the user base for Perp DEXs is expanding, and DeFi-specific attractions like community governance and airdrop incentives will also translate into retention rates.

4) Capital and institutional entry: In 2025, several top-tier institutional funds began to venture into the Perp DEX field: 21Shares listed an ETP product for HYPE; traditional institutions like Amber directly incubated edgeX; Paradigm亲自下场做 Paradex. These signals indicate that compliant capital is optimistic about the future prospects of on-chain derivatives and is willing to provide liquidity and infrastructure support. As regulation becomes clearer, more Wall Street or crypto funds are likely to participate through DAO investments, liquidity market-making, etc., injecting new vitality into the track.

5) Ecological synergy effects: Perp DEXs have strong synergies with other areas of DeFi (lending, yield strategies, stablecoins, etc.). Paradex has begun exploring the combination of perpetual contracts with other DeFi legos to create new use cases. This预示着更丰富的跨协议合作和生态整合机会. For example, perpetual DEXs can provide hedging tools for on-chain assets, and interest rate derivatives from lending protocols can also be priced through perpetual markets.

2. Potential Risks in the Perp DEX Track

Beneath the surface prosperity of the Perp DEX track's explosion in 2025, multiple risks are hidden, worthy of investors' vigilance.

1) Wash trading造假 and excessive incentives: Aster's alleged data造假 leading to信用坍塌, and Lighter's excessive incentives埋下泡沫风险, remind us that short-term trading data can be packaged, but only open interest and revenue are hard indicators. Investors must not be fooled by exaggerated trading volumes.

2) Technical and security risks: New platforms often adopt complex architectures or self-developed chains to pursue high performance, increasing the probability of vulnerabilities and failures. Lighter's mainnet experienced a database crash and downtime just 10 days after launch. Self-developed chains like Hyperliquid have also been questioned for their consensus and security not being long-term tested. Additionally, technical risks like smart contract vulnerabilities, matching failures, and oracle failures cannot be ignored.

3) Token economic risks: Many Perp DEX platforms regard token price as the lifeline of the ecosystem, stimulating the price through buybacks, dividends, etc. But the secondary market is volatile; once the platform token plummets, it may打击用户积极性甚至引发挤兑. For example, if Lighter's LITER price falls short of expectations after listing, a large number of wash trading users may sell and leave.

4) Extreme market volatility risks: The current scale of the on-chain contract market is still small relative to CEXs. During extraordinary volatility, liquidity drying up and slippage soaring can still occur. Once an event like the "10.11 crash" in 2025 occurs, involving liquidations on the scale of tens of billions, platforms with poor risk resistance may collapse or even become insolvent.

5) Compliance policy risks: As on-chain derivatives trading volume surges, regulatory attention increases. Many countries and regions prohibit unauthorized platforms from providing high-leverage contract trading to their residents. Even decentralized platforms may face restrictive measures. Although decentralized protocols themselves are difficult to completely shut down, regulatory risks may打击用户信心 and affect the scale of capital inflow.

V. 2026 Outlook: Rise of Multiple Players, Continued Shakeout and Upgrade

Looking ahead to 2026, the on-chain perpetual contract market is expected to enter a more mature and also more intense new stage. Based on the current landscape and development trends, the following trends can be anticipated:

1. Evolving landscape, continued shakeout: Hyperliquid, as the seasoned霸主, is expected to continue consolidating its position in the first tier凭借深厚的OI and community foundation. Lighter, if it can maintain user activity, will be the most powerful challenger in terms of trading volume; Aster, with Binance's support, is expected to see its market share recover; EdgeX will likely capture the institutional and stable user market. Paradex attracts users with product differentiation and has the opportunity to rise from the second tier in 2026. The overall track pattern will be "one superpower, multiple strong players": Hyperliquid稳超, others各自拥细分领域, with the market share gap among top platforms narrowing. Meanwhile, the shakeout will continue, with intensified survival of the fittest among small and medium platforms.

2. Return to rationality, emphasizing quality growth: After the疯狂刷量军备竞赛 of 2025, all parties in the market will become more rational,开始意识到拼交易量排名意义不大,转而关注未平仓、收入、用户留存等更能反映真实健康度的指标. It is expected that the Vol/OI ratios of various platforms will overall fall back to reasonable intervals in 2026, new user growth will become more organic, and the恶性激励战 may come to an end. Of course, marketing will continue, such as various trading competitions, limited-time zero-fee promotions, etc., but this competition will focus more on improving user experience rather than simply inflating data. At the same time, as many airdrops are completed, the number of speculators will decrease, and the proportion of traders with real demand will increase. Quality first and stable operation will become the new consensus in the track.

3. Rise of product diversification models: In 2026, we may see Perp DEXs no longer limited to the single product of "perpetual contracts" but expanding into full exchange product lines. Paradex's planned perpetual options and spot trading will be a test case: if successful, other platforms will inevitably follow suit in developing new contract types like options, futures (dated futures), providing richer derivative tools. Additionally, real-world asset (RWA) contracts may emerge, allowing users to trade contracts for traditional market assets like gold and stock indices on-chain. Meanwhile, features like social trading and algorithmic strategies will be integrated into platforms, deepening the trend of exchange + wealth management integration.

4. Regulatory and compliance试探: 2026 may become the year when the regulatory framework for DeFi derivatives gradually takes shape. Some major jurisdictions may issue guidelines or regulations targeting decentralized derivatives. There are rumors that EdgeX is considering launching a regulated version for institutional access, similar to dYdX's custodial version back in the day. If Hyperliquid wants to further open up the US market, it might also evaluate the possibility of registering as a Swap Execution Facility (SEF). Overall, the gray areas in the DeFi field will gradually be standardized in 2026, which is both a challenge and an opportunity for the Perp DEX track dominated by retail anonymous users. Standardization有助于更多主流资金进场, but may also conflict with the philosophy of decentralization. Platforms will likely adopt a "two-pronged approach": retaining anonymous open access while setting up separate compliant windows to meet regulatory requirements.

5. Collision of old and new forces: 2026 may also witness head-on confrontations between traditional giants and链上新贵. On the one hand, established centralized exchanges are unlikely to sit back and watch their份额被抢; entering the DeFi derivatives field will be a natural strategy. Binance, OKX, etc., are already deploying decentralized products. Binance's previous investment in Aster might just be the beginning; it's not impossible for them to launch their own decentralized contract trading features in the future, linking with their CEX to provide "centralized + decentralized" dual-track services. Similarly, rising platforms like Bitget may also incubate their own DEXs. The entry of centralized platforms will bring more resources and user traffic to the track, but also意味着竞争更白热化. On the other hand, new链上原生 projects will continue to emerge, attempting to challenge existing leaders with newer concepts or mechanisms.

Conclusion: In 2025, the Perp DEX track went from Hyperliquid's solo lead to fierce competition among various players, with thrilling climaxes attracting much attention. The Perp DEX track in 2026 will enter a stage transitioning from "wild growth" to "intensive cultivation." The overall market will become more mature and stable,告别粗放刷量转向高质量竞争; product forms will become more diverse, evolving towards comprehensive derivatives platforms. Looking ahead, the battle for on-chain derivatives will continue to be exciting, and we await the birth of new格局和传奇.

About Us

Hotcoin Research, as the core investment research institution of Hotcoin Exchange, is dedicated to transforming professional analysis into your practical tool. We analyze market trends through "Weekly Insights" and "In-Depth Research Reports"; with the exclusive column "Hotcoin Select" (dual screening by AI + experts), we help you identify potential assets and reduce trial-and-error costs. Every week, our researchers also engage with you face-to-face through live streams, interpreting hot topics and predicting trends. We believe that warm companionship and professional guidance can help more investors navigate cycles and seize the value opportunities of Web3.

Risk Disclaimer

The cryptocurrency market is highly volatile, and investment itself carries risks. We strongly advise investors to invest based on a full understanding of these risks and within a strict risk management framework to ensure fund safety.

Website: https://lite.hotcoingex.cc/r/Hotcoinresearch

X: x.com/Hotcoin_Academy

Mail: [email protected]