Author: Insightful Commentary

The US-Iran dispute has reignited, with crude oil and precious metal assets surging strongly. The recent rise in oil prices mainly reflects geopolitical risk premiums rather than actual tightness in physical supply.

Market signals are diverging: futures prices, freight rates, and risk reversal option prices are rising due to risk concerns, while futures contract spreads (calendar spreads) and physical crude oil differentials, which reflect spot supply and demand, are weakening. MS analyzed four potential scenarios.

Scenario Analysis

· Base Scenario: Ruled out the sustained closure of the Strait of Hormuz as a core scenario, as the threshold is extremely high and the probability is very low. The analytical framework focuses on a range of possibilities from de-escalation to limited friction.

· Scenario 1 (No Supply Disruption): Situation de-escalates, risk premium fades. An estimated risk premium of about $7-9/bbl is expected to disappear quickly, with Brent crude potentially falling back to the mid-to-low $60s/bbl.

· Scenario 2 (Limited Strikes & Short-term Logistics Friction): Targeted military action occurs but avoids energy infrastructure. Could lead to supply disruptions of 0-0.5 million barrels per day (mb/d), lasting 1-3 weeks. Oil prices might briefly spike to the mid-to-high $70s/bbl, but China slowing its strategic reserve accumulation will be a key balancing mechanism, after which prices are expected to return to the mid-to-low $60s/bbl.

· Scenario 3 (Partial Iranian Export Disruption): Broader strikes cause partial disruption to Iran's export chain but do not affect Strait of Hormuz shipping. Could lead to supply disruptions of 0.8-1.5 mb/d, lasting 4-10 weeks. Price movement would be between Scenario 2 and Scenario 4.

· Scenario 4 (Fleet Efficiency Shock & Shipping Impairment): Tail risk. Iran retaliates through maritime means such as harassing vessels, leading to reduced shipping efficiency and increased delays. This equates to an "effective supply tightness" of 2-3 mb/d for several weeks. Price action could resemble the spike in early 2022, but the duration is expected to be shorter.

· Scenario 1 (No Supply Disruption): Situation de-escalates, risk premium fades. An estimated risk premium of about $7-9/bbl is expected to disappear quickly, with Brent crude potentially falling back to the mid-to-low $60s/bbl. (Significant Probability)

The first scenario, "No Supply Disruption: De-escalation and Risk Premium Fading," is set as a reference scenario with considerable probability. Its core assumption is that the current significant US military deployment in the Middle East, combined with diplomatic pressure, is sufficient to prompt Iran to make negotiating adjustments on the nuclear issue, thereby avoiding direct military conflict. In this case, the military threat primarily acts as leverage rather than a prelude to actual action; sanctions enforcement may remain strict but will not impose additional restrictions that substantially alter current Iranian export flows.

Consequently, this scenario has no impact on physical crude supply: Iran's exports remain roughly at recent levels, and regional transportation through the Strait of Hormuz remains unimpeded. Its main impact on the market is that the geopolitical risk premium currently embedded in the front-end oil price will disappear. The report, based on regression analysis of OECD commercial inventories versus the Brent M1-M4 calendar spread (the spread between near-term and longer-dated contracts) over more than 25 years, points out that current inventory levels should correspond to a flat or slightly contango market structure, not the actual backwardation present. The current Brent M1-M4 spread is about $1.75/bbl; if the market clearly realizes no physical supply disruption will occur, this spread could revert towards the level implied by the regression analysis (close to zero).

This implies that if the front end of the crude futures curve shifts into contango while the back-end prices remain stable, the front-month (spot) Brent price could drop from the current level around $70/bbl to the mid-to-low $60s/bbl. Based on this, it is estimated that a geopolitical risk premium of about $7 to $9 per barrel could fade relatively quickly in a de-escalation scenario. Most of the price adjustment could happen within days to weeks, rather than months, especially when market participants are confident that regional supply and transportation flows will remain uninterrupted.

The report cites the market performance after the Iran-Israel conflict in June 2025 as a precedent, noting that oil prices, which had spiked due to escalation fears, quickly fell back to pre-conflict levels within weeks after it was confirmed that energy infrastructure and transportation were not substantially affected. This confirms that when physical supply remains intact, risk premiums can be built and dissipated very rapidly. Ultimately, volatility would compress, and the dominant pricing factor for the market would shift back from geopolitical risk to physical supply and demand fundamentals.

· Scenario 2 (Limited Strikes & Short-term Logistics Friction): Targeted military action occurs but avoids energy infrastructure. Could lead to supply disruptions of 0-0.5 million barrels per day (mb/d), lasting 1-3 weeks. Oil prices might briefly spike to the mid-to-high $70s/bbl, but China slowing its strategic reserve accumulation will be a key balancing mechanism, after which prices are expected to return to the mid-to-low $60s/bbl. (Significant Probability)

The second scenario, "Limited Strikes and Short-term Logistics Friction," describes a development path with significant probability. This scenario assumes the US launches a targeted military strike, deliberately avoiding energy infrastructure. In response, Iran adopts a calibrated countermeasure aimed at demonstrating deterrence domestically but avoiding triggering broader escalation; other regional actors also avoid direct involvement. Under these conditions, maritime transport through the Strait of Hormuz continues without sustained interruption.

Therefore, any impact on physical supply would most likely stem from secondary logistics friction rather than infrastructure damage. This friction could include: several days of cautious tanker movement and delays, a temporary rise in insurance premiums, tighter sanctions enforcement, and limited self-restraint by traders. Based on this, the report assesses the potential supply disruption as relatively modest, around 0 to 0.5 mb/d, and temporary, expected to last 1 to 3 weeks. There is even a possibility, as seen in the June 2025 event, that regional strikes do not translate into sustained export losses.

Even with temporary shortages of this scale, the available spare capacity in Saudi Arabia and the UAE would be sufficient to offset them, limiting the risk of long-term physical imbalance. However, the initial market reaction would still focus on the front-end price. Brent prices could be pushed into the $75-$80/bbl range due to short-term risk premium, and the spread between near-month and longer-dated contracts (M1-M4) would widen from current levels.

But the more critical balancing mechanism in this scenario would manifest on the demand side, particularly through inventory behavior adjustment rather than final consumption. Over the past six months, China's implied crude inventory build has averaged around 0.8 mb/d. In an environment of rising oil prices, especially if the front-end futures curve steepens into deeper backwardation, the pace of this autonomous strategic reserve accumulation is likely to slow.

The report expects that inventory accumulation willingness will weaken when oil prices enter the mid-to-high $70s/bbl. Merely a slowdown in China's inventory build pace from recent highs to a more normal level (e.g., around 0.3 mb/d) would be enough to offset a temporary disruption of 0.5 mb/d in Iranian exports.

In the second scenario, the market's price reaction would be "high first, low later." There would be an initial spike due to risk pricing, but as logistics friction eases, OPEC spare capacity reassures the market, and Chinese inventory demand slows – these three balancing mechanisms take effect, and in the absence of evidence of sustained supply damage, the crude futures curve and prices are expected to compress again, eventually returning to the mid-to-low $60s/bbl level. This normalization process might last longer than in Scenario 1, potentially extending from weeks to months, but it would not trigger a sustained, substantial sharp rise in prices.

· Scenario 3 (Partial Iranian Export Disruption): Broader strikes cause partial disruption to Iran's export chain but do not affect Strait of Hormuz shipping. Could lead to supply disruptions of 0.8-1.5 mb/d, lasting 4-10 weeks. Price movement would be between Scenario 2 and Scenario 4. (Low Probability)

The third scenario, "Partial Iranian Export Disruption: Broader Strikes but No Shipping Impairment," is seen as a low-probability escalation path. This scenario assumes the US launches broader military actions targeting a wider range of strategic assets within Iran, but other regional actors still refrain from direct involvement, and the crucial Strait of Hormuz shipping lane does not suffer sustained damage—meaning no sustained convoy mechanism or systemic shipping shock occurs. The primary targets are not energy infrastructure, but the scale is sufficient to cause substantial, localized disruption to Iran's export chain.

The core impact channel is operational, not structural. Specific possibilities include: intermittent disruptions to loading operations at key export terminals (like Kharg Island), temporary power or communication failures affecting terminal operations, and short-term constraints in logistics from fields to terminals. Simultaneously, persistently tighter sanctions enforcement and commercial self-restraint could keep actual volumes below normal levels even after the military action period.

Under these conditions, a reasonable outcome is a significant and prolonged drop in Iranian exports—larger than in Scenario 2, yet not reaching the regional shipping efficiency shock described in Scenario 4. The report assesses the effective supply loss at approximately 0.8 to 1.5 mb/d, lasting about 4 to 10 weeks, depending on the nature of the operational disruptions and the speed of export logistics normalization.

From a market reaction perspective, price volatility would concentrate on the front end of the futures curve. The spread between near-month and longer-dated contracts (the prompt spread) is expected to widen and maintain upward pressure for a longer duration than in Scenario 2, reflecting more persistent physical supply tightness. However, since Strait shipping is not persistently impaired, the likelihood of the acute mismatch described in Scenario 4 is lower. In this scenario, balancing mechanisms would be more prominent than in Scenario 2 but still effective: Saudi and UAE spare capacity has room to offset a large portion of shortages exceeding 1 mb/d, but the response speed and market confidence in it would be key to price dynamics; on the demand side, higher oil prices and a deepening backwardation structure are expected to dampen autonomous inventory demand, particularly in China, providing an additional buffer.

Consequently, price movement would be between the short-term spike of Scenario 2 and the sharp surge of Scenario 4. As evidence accumulates that the disruptions are operational and reversible, the futures curve would begin to compress; but given the longer duration of export interruptions and the time needed for the market to verify the sustained recovery of Iranian export volumes, the price normalization process would be slower than in Scenario 2.

· Scenario 4 (Fleet Efficiency Shock & Shipping Impairment): Tail risk. Iran retaliates through maritime means such as harassing vessels, leading to reduced shipping efficiency and increased delays. This equates to an "effective supply tightness" of 2-3 mb/d for several weeks. Price action could resemble the spike in early 2022, but the duration is expected to be shorter. (Tail Risk)

The fourth scenario, "Fleet Efficiency Shock: Regional Maritime Leverage and Shipping Impairment," is defined as a "tail risk" event with a very low probability of occurrence but potentially massive impact. This scenario assumes that after a large-scale US strike, Iran adopts a significant countermeasure, leveraging its maritime influence in the Gulf region without attempting a complete blockade of the Strait of Hormuz. Such actions could include repeated fast-boat harassment, selective seizure of tankers, drone flyovers, missile demonstrations, etc., aimed at significantly increasing navigation risk and uncertainty. Commercial shipping would continue but would be forced to slow down, insurance premiums would soar, some shipowners might temporarily withdraw capacity, and naval convoys or formation sailing patterns might reemerge, all effectively prolonging vessel transit times.

The primary impact mechanism in this scenario stems not from oil field production disruption but from a decline in the productivity of the global shipping fleet. The report illustrates through quantitative simulation: currently, approximately 11 billion ton-miles per day of crude oil transportation originates from locations behind the Strait of Hormuz. If enhanced security procedures, convoy operations, and route delays increase the average voyage time for these routes (e.g., by 5 days), the effective productivity of vessels operating on these routes would decline by about 17%. This would translate to a near loss of 2 billion ton-miles per day in effective capacity, equivalent to 6% of global crude oil shipping capacity. Based on the current seaborne crude flow of about 50 mb/d, this equates to the market suffering an "effective supply tightness" on the scale of 2 to 3 mb/d for several weeks.

From a market balance perspective, a disturbance of this magnitude would likely exceed the buffer provided merely by China slowing its strategic reserve accumulation and would also test the practical limits of Saudi and UAE spare capacity call-up. Therefore, the reaction in prices and futures curve structure could begin to resemble the dynamics of early 2022, when the market doubted its ability to absorb a multi-million barrel supply shortfall and drastically revalued front-month prices. The market reaction would be intensely concentrated on the curve's front end: Brent prices could spike sharply, and the spread between near-month and longer-dated contracts (the prompt spread) would widen significantly as refiners and traders scramble for immediately available crude.

However, unlike 2022, the primary balancing mechanism need not require sustained reduction in final consumption: higher oil prices and a steeper backwardation are expected to suppress autonomous inventory demand (especially in China) and accelerate adaptive adjustments in shipping and operations, which would help limit the duration of the market mismatch.

Simultaneously, shipping freight would spike in sync. As operational adjustments take effect, and as long as shipping continues under high risk, this effective tightness would gradually ease. But during the period of shipping impairment, oil prices could be significantly higher than the levels described in Scenario 2, and the normalization process would depend on when confidence in Gulf shipping security is restored.

MS: Iran Situation Scenario Analysis

Oil prices rise on risk, not supply tightness: Physical signals ease, option skew surges. We outline four Iran scenarios from risk premium fading to shipping impairment and maintain our base forecast that Brent will gradually slide towards around $60/bbl as risk premiums fade and the supply-demand balance shifts looser.

Key Points

· This week, futures prices, freight rates, and risk reversal options all rose, while futures spreads and physical differentials weakened—the market is pricing geopolitical risk, not immediate supply tightness.

· We rule out sustained closure of the Strait of Hormuz as a core scenario; instead, we list four scenarios from de-escalation to shipping impairment.

· For moderate shocks, Chinese inventory building is the primary buffer: Autonomous stockbuilding is likely to slow as prices rise and backwardation deepens.

· The biggest shock channel is logistics: Convoy/delay risks reduce fleet efficiency—equivalent to an effective supply tightness of ~2-3 mb/d in the short term.

· The base forecast remains anchored on the no-significant-disruption scenario: A $7-9/bbl risk premium could fade, and Brent could slide to $60/bbl as surplus re-emerges.

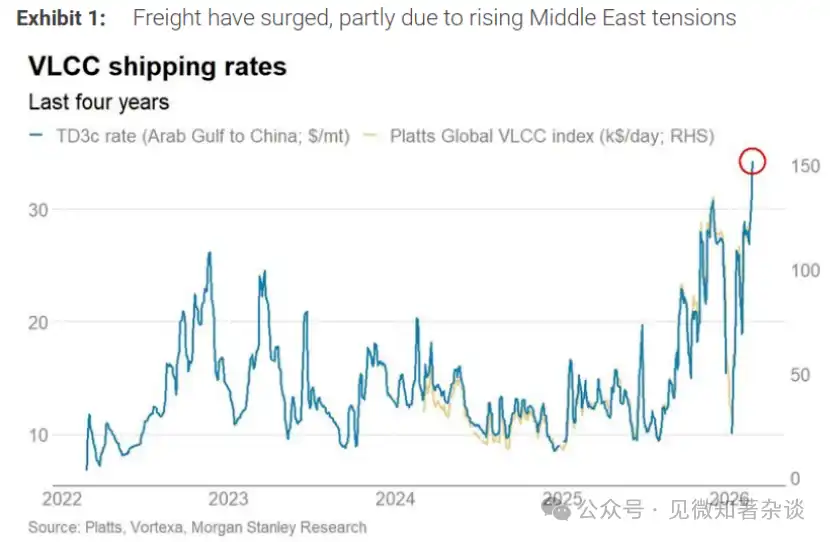

Figure 1: Shipping rates surge, partly due to heightened Middle East tensions

Figure 2: Near-term Brent price forecast raised as geopolitical risk premium may persist for a while, but still expect prices to fall back to $60/bbl later this year

Four Scenarios for the Crude Oil Market

Market Signals: Risk Repricing vs. Physical Supply Tightness

This week, the crude oil market sent a striking signal: paper risk was repriced higher, while signals of physical supply tightness eased.

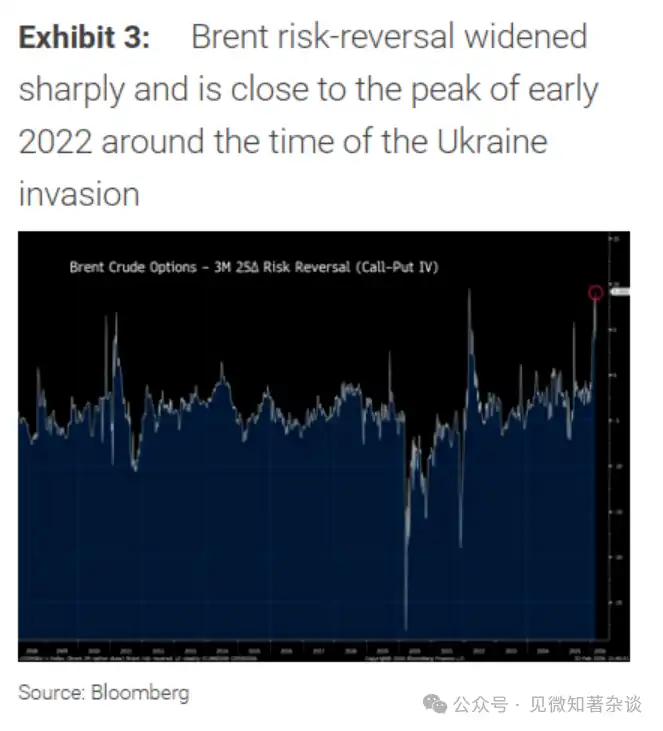

Near-month futures prices for the three major benchmarks all strengthened (Brent up ~$3.1/bbl to ~$71.8/bbl, WTI up ~$3.5/bbl to ~$66.4/bbl, Dubai up ~$3.7/bbl to ~$70.7/bbl, all week-on-week), and shipping indicators moved higher in sync. In the options market, the Brent 3-month 25Delta risk reversal spread widened sharply, approaching levels seen during periods of severe uncertainty like early 2022.

Figure 3: Brent risk reversal spread widens sharply, nearing peak levels around Ukraine invasion in early 2022

However, several indicators that typically track the immediate physical situation moved in the opposite direction: The Brent M1-M2 spread narrowed (from ~$0.7/bbl to ~$0.5/bbl), the Brent DFL实质 declined (from ~$0.9/bbl to ~$0.3/bbl), and the Brent CFD spread compressed sharply (first week from ~$3.0/bbl to ~$0.7/bbl).

Differentials for Atlantic Basin long-haul crudes also eased, including West African and other arbitrage crudes—again a pattern typically consistent with the spot supply turning looser, not tighter.

Taken together, rising futures prices, freight, and risk reversal skew, coexisting with softening prompt spreads and physical differentials, are classic features of the market pricing geopolitical risk premiums and tail-risk hedging demand, not a reaction to immediate scarcity.

Figure 4: Contradictory signals: Brent front-month contract rises...

Figure 5: ...while the M1-M2 calendar spread weakens

Nonetheless, geopolitical risks are real; we outline four scenarios

In recent weeks, public reports have noted a significant buildup of US military assets in and around the Middle East, including additional tactical aircraft squadrons (F-15, F-35, and F-22), tankers, and early warning radar systems, as well as enhanced naval deployments.

According to multiple news agencies, the USS Abraham Lincoln carrier has arrived in the Gulf, and a second carrier strike group centered on the USS Gerald R. Ford is en route. A recent BBC News report called this the largest US air and naval buildup in the region since the 2003 invasion of Iraq.

Against this backdrop, we set the following scenario framework.

Before delving in, a clarification: While an overt and sustained closure of the Strait of Hormuz is not impossible, we do not list it as a core scenario. The threshold for such an outcome is high, and the probability appears very low.

The US Fifth Fleet, headquartered in Bahrain, has a long-standing mandate to protect freedom of navigation, and the US and its allies possess extensive air and naval capabilities (including mine countermeasures) that would make sustained closure difficult to maintain. Attempting closure would also cause economic self-harm for Iran, as its exports also rely on these waters and would directly jeopardize supplies to key customers like China—factors likely to trigger a broad international response.

Therefore, consistent with historical experience, we focus on a spectrum of scenarios ranging from de-escalation to limited friction, partial Iranian export chain disruption, and transportation impairment via operational and shipping constraints rather than sustained closure.

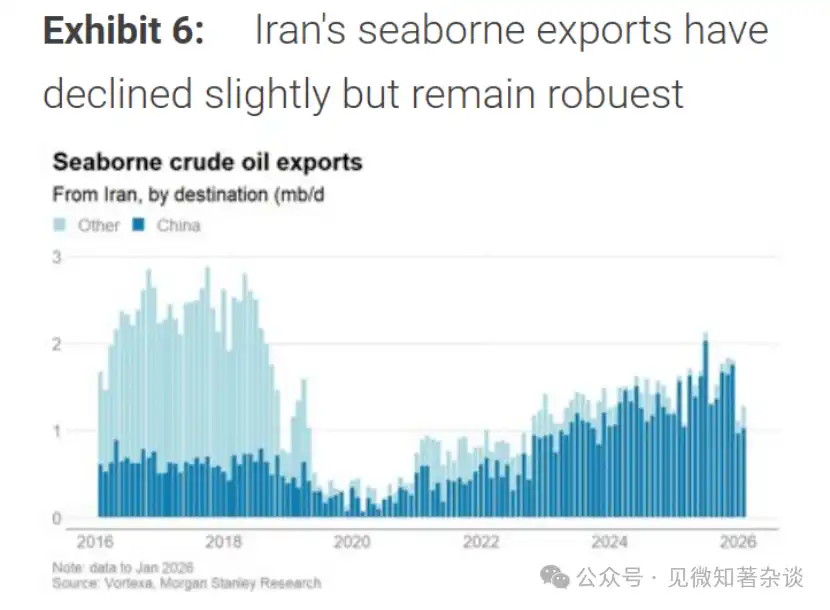

Figure 6: Iran's seaborne exports have declined slightly but remain strong

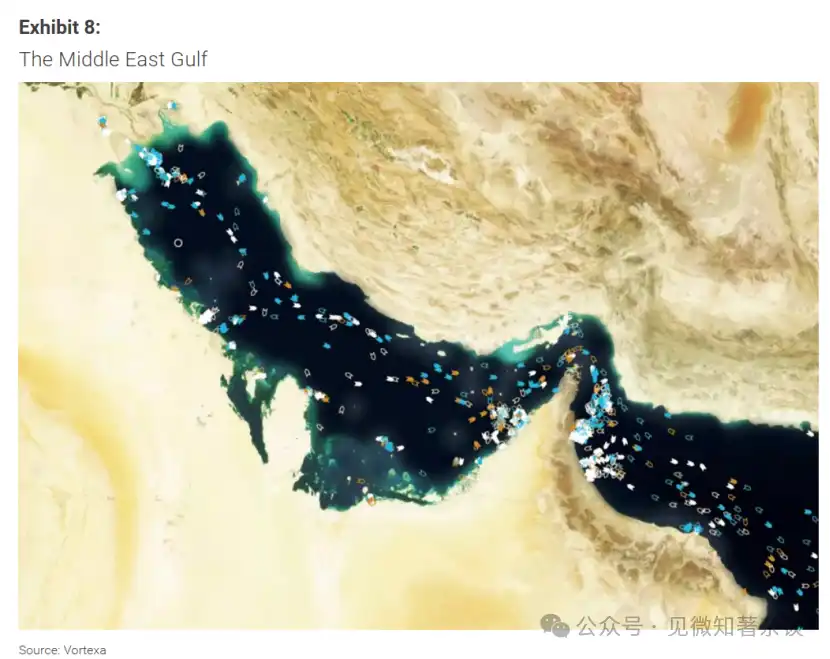

Figure 7: Approximately 15 mb/d of crude and 5 mb/d of products are shipped out through the Strait of Hormuz

Figure 8: Middle East Gulf Region

Scenario 1 - No Supply Disruption: De-escalation and Risk Premium Fading

· Reference scenario; Significant probability

· No impact on production or exports

· $7-9/bbl risk premium消散: Brent falls back to mid-to-low $60s/bbl

In this scenario, diplomatic pressure combined with the visible US military deployment proves sufficient to prompt Iran towards negotiated adjustments on its nuclear posture, avoiding direct military confrontation. Negotiations may still be lengthy and incremental, but the threat of force acts primarily as leverage, not a prelude to actual action. Sanctions enforcement may remain strict but does not impose additional restrictions that materially alter current export flows.

Under this outcome, physical oil supply remains largely unchanged. Iranian exports continue around recent levels, and regional transportation via the Strait of Hormuz is unaffected. The primary market effect will be the elimination of the geopolitical risk premium currently embedded in front-end prices.

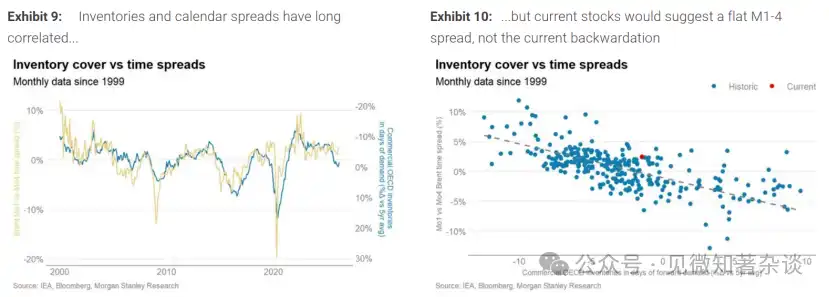

Based on our regression analysis of OECD commercial inventories versus the Brent M1-M4 calendar spread over more than 25 years (see attached chart), current inventory levels should correspond to a flat-to-slight-contango structure, not the prevailing backwardation.

The Brent M1-M4 spread is currently trading around $1.75/bbl; in the scenario where it becomes clear no physical disruption will occur, this spread could reconnect to the level implied by the regression analysis, near zero. If the curve front shifts into contango while farther-dated Brent prices remain broadly stable, this would imply a front-month Brent price in the mid-to-low $60s/bbl, versus current levels in the low $70s.

This suggests that in a de-escalation scenario, a geopolitical risk premium of roughly $7-9/bbl could fade relatively quickly. Most of the adjustment could occur within days to weeks, not months, particularly if market participants become confident that regional supply and transportation flows will remain uninterrupted.

A recent precedent illustrates the speed of such premium decay. In June 2025, following Iran-Israel clashes, Brent oil prices rebounded sharply from the mid-$60s to near $80/bbl on fears of broader regional escalation and potential Gulf export disruptions. However, as it became clear that energy infrastructure and transport flows were not substantially affected, prices fell back to pre-conflict levels within weeks.

This episode underscores that when physical supply remains intact, geopolitical premiums can form and dissipate rapidly. Volatility would likely compress, the curve front could shift into contango, and supply-demand fundamentals (rather than geopolitics) would re-emerge as the dominant pricing driver.

Figure 9: Long-term correlation between inventories and calendar spread...

Figure 10: ...but current inventory levels suggest M1-4 spread should be flat, not the current backwardationScenario 2 - Limited Strikes & Short-term Logistics Friction

· Significant Probability

· Potential for 0-0.5 mb/d supply disruption lasting 1-3 weeks

· Brent temporarily rises to mid-to-high $70s/bbl, then normalizes to mid-to-low $60s/bbl

· Slowing Chinese inventory demand is key balancing mechanism

This scenario assumes targeted US military action, deliberately avoiding energy infrastructure. Iran responds in a calibrated manner, aimed at showing domestic deterrence but not provoking broader escalation. Regional actors avoid direct participation, and maritime transit through the Strait of Hormuz continues without sustained interruption.

Under this outcome, any physical supply impact would most likely come from secondary logistics friction, not infrastructure damage. This friction could include brief shipping caution (e.g., tanker delays for days), temporarily higher insurance premiums, tighter sanctions enforcement, and limited self-restraint by traders. Thus, a reasonable disruption range is modest, around 0 to 0.5 mb/d, and likely temporary, lasting roughly 1-3 weeks. It is also possible that no measurable disruption occurs, as demonstrated by the June 2025 event where regional strikes did not translate into sustained export losses.

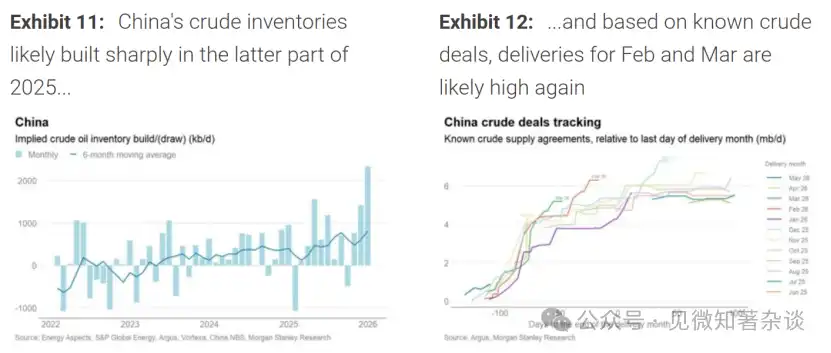

Even within this range, any temporary shortfall could be offset by available spare capacity in Saudi Arabia and the UAE if utilized, limiting the risk of longer-term physical imbalance. Furthermore, the primary margin of adjustment would likely occur on the demand side, via inventory behavior rather than end-user consumption. Over the past six months, China's implied crude inventory build has averaged around 0.8 mb/d (see chart), though such estimates are themselves subject to revision.

In a higher price environment—particularly if the front-end backwardation deepens—autonomous inventory accumulation would likely slow. While the exact price threshold is uncertain, we expect inventory accumulation to become less responsive to price as oil reaches the mid-to-high $70s/bbl. A slowdown in Chinese inventory accumulation from recent elevated levels to a more normal pace (e.g., down to around 0.3 mb/d) alone could offset a temporary 0.5 mb/d interruption in Iranian exports.

From a market structure perspective, this scenario could produce a front-loaded reaction. Brent prices could spike into the $75-80/bbl range, and the M1-M4 spread would widen from current levels as near-term risk is priced.

However, in the absence of evidence of sustained supply damage, the curve is expected to compress again as logistics friction eases, OPEC spare capacity reassures the market, and Chinese inventory demand slows.

While normalization could take longer than in Scenario 1—potentially extending from weeks to months if uncertainty is intermittent—sustained, materially higher prices would likely require a larger or more persistent disruption than assumed here.

Figure 11: China's crude inventories likely built substantially in H2 2025...

Figure 12: ...and based on known crude deals, February and March deliveries could be high again

Scenario 3 - Partial Iranian Export Disruption: Broader Strikes but No Shipping Impairment

· Low probability escalation

· 0.8-1.5 mb/d disruption lasting 4-10 weeks

· Price action between Scenario 2 and 4

In this scenario, the US launches broader military action targeting a wider range of strategic assets within Iran, while regional actors avoid direct participation, and transit through the Strait of Hormuz continues without sustained impairment (i.e., no sustained convoying and systemic shipping shock). Energy infrastructure is not the primary target, but the scale of action causes substantial, localized disruption to Iran's export chain.

The relevant transmission channels would be operational, not structural: intermittent disruption to loading operations at key export terminals (including safety shutdowns), temporary power or communications outages affecting terminal operations, and short-term constraints in logistics from fields to terminals. Concurrently, persistently tighter sanctions enforcement and commercial self-restraint could reduce loadings beyond the immediate period of military activity.

A reasonable outcome here is a material reduction in Iranian exports—larger in scale and duration than Scenario 2, but not incorporating the regional shipping efficiency shock embedded in Scenario 4. A reasonable range is around 0.8-1.5 mb/d of effective loss, lasting roughly 4-10 weeks, depending on the nature of the disruption and the speed of export logistics normalization.

Market reaction would likely concentrate on the curve front: Prompt spreads are expected to widen and remain supported for longer than in Scenario 2, reflecting more persistent physical tightness. However, with no sustained transport impairment, the potential for the acute mismatch described in Scenario 4 is lower.

The balancing channels in this scenario would be more relevant than in Scenario 2, but still material. Saudi Arabia and the UAE have room to offset a large portion of shortages above 1 mb/d, though the speed of any response and market confidence in it would be crucial for price dynamics.

On the demand side, higher prices and a steeper backwardation would likely curb autonomous inventory demand, particularly in China, providing an additional buffer. The curve is expected to begin compressing as evidence accumulates that disruptions are operational and reversible; however, given the longer duration of export interruptions and the time needed for the market to verify sustained recovery in Iranian loadings, normalization could be slower than in Scenario 2.

Scenario 4 - Fleet Efficiency Shock: Regional Maritime Leverage and Shipping Impairment

· Tail risk

· Primary mechanism is tanker delays, reducing effective shipping capacity, thus global crude exports

· This translates to a supply loss of 2-3 mb/d for several weeks

· Price action similar to early 2022, though duration likely significantly shorter

This scenario assumes that following a large-scale US strike, Iran undertakes significant retaliation, leveraging its maritime influence in the Gulf without attempting a full closure of the Strait of Hormuz. Such actions could include repeated fast-boat harassment, selective seizure of tankers, drone overflights, missile demonstrations, and other measures aimed at raising risk and uncertainty. Commercial traffic would likely continue, but at slowed pace. Insurance premiums would rise, some shipowners might temporarily withdraw capacity, naval convoys or formation-style operations could re-emerge, lengthening effective transit times.

The primary impact here is not from field shutdowns but from reduced fleet efficiency. By way of illustration, global seaborne crude and condensate volumes are currently ~32 billion ton-miles per day, with ~11 billion ton-miles per day originating from locations behind the Strait of Hormuz. The average voyage time for these flows is ~29 days. If enhanced security procedures, convoying, and route delays increase the average voyage time by, say, 5 days, the effective productivity of vessels operating on these routes would decline by ~5/29, or ~17%.

Applied to flows originating from Hormuz, this implies a near reduction in effective transport capacity of ~2 billion ton-miles per day, equivalent to ~6% of global crude shipping capacity. On a current seaborne crude flow of ~50 mb/d, this equates to an effective supply tightness of 2-3 mb/d for a period of several weeks. While the shipping market would gradually adapt through higher freight, capacity reallocation, and operational adjustments, the initial impact could be significant relative to available spare capacity.

From a supply-demand balance perspective, a disruption of this magnitude could exceed what could be offset merely by pausing Chinese autonomous inventory accumulation and would test the practical limits of Saudi and UAE spare capacity. In this regard, price and curve reaction could begin to resemble early-2022 dynamics, where the market questioned whether available buffers were sufficient to absorb a multi-million b/d shortfall and repriced the curve front accordingly. Market reaction would likely concentrate on the curve front, with Brent prices rising sharply and prompt spreads widening significantly as refiners and traders scramble for prompt spot.

However, unlike 2022, the primary balancing margin need not require sustained reduction in end-user consumption: higher prices and a steeper backwardation are expected to curb autonomous inventory demand (especially in China) and accelerate shipping and operational adjustments, helping to limit the duration of the mismatch.

Freight rates are expected to rise in sync. As operational adjustments take effect and if transport continues under high risk, the effective tightness would gradually ease. However, during the period of shipping impairment, prices could be well above levels described in Scenario 2, with normalization dependent on the restoration of confidence in Gulf shipping security.

Price forecast adjusted but still anchored to Scenarios 1 and 2

The scenario framework above reflects the近期 uncertainty around geopolitically driven supply risks. Nonetheless, our core view remains anchored to Scenarios 1 and 2, i.e., ultimately little or no disruption to physical supply.

If such an outcome materializes in the coming weeks, our regression framework (linking OECD commercial inventories to the Brent M1-M4 calendar spread) suggests that the ~$7-9/bbl geopolitical risk premium in the front-month Brent price could fade, the curve flattens to the level implied by current inventory conditions, and spot prices fall back to the low $60s.

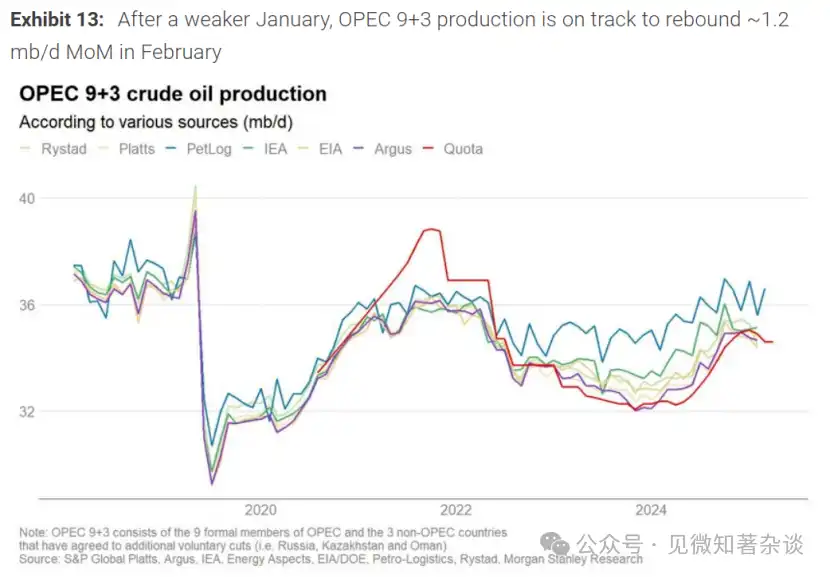

However, looking beyond the very near term, our fundamentals remain weak. The January supply-demand balance was tighter than we expected due to temporary disruptions (including in Kazakhstan and the US), but these appear to be reversing. Furthermore, early tracking from Petro-Logistics suggests OPEC+ production is on track for a ~1.2 mb/d month-on-month rebound in February.

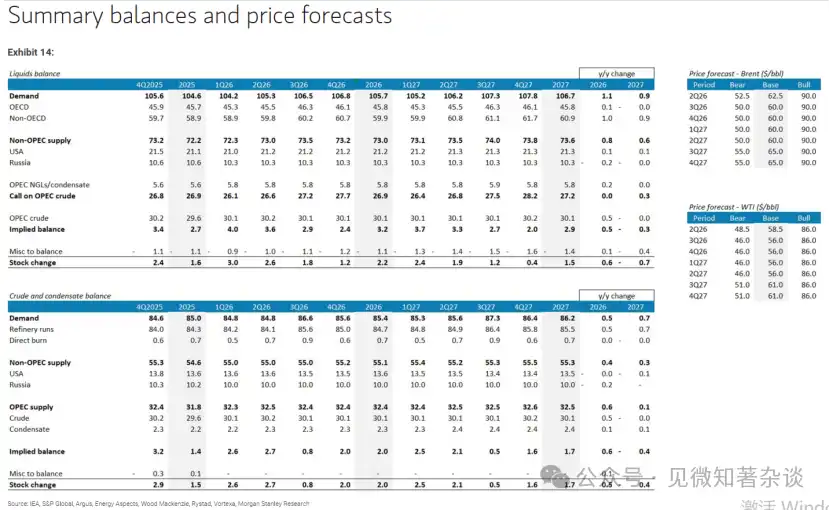

Thus, our crude balance still points to a surplus of ~2.5 mb/d in H1 2026 and ~1.4 mb/d in H2 2026.

We assume that ~0.8 mb/d of the surplus will be absorbed by inventory building in China, but we do not assume a repeat of the large increase in floating storage seen in 2025 for 2026. This implies that an estimated 0.6-1.7 mb/d surplus would need to be absorbed in onshore inventories outside China, including a material portion in commercial stocks at the OECD/Atlantic Basin pricing centers.

Historically, inventory absorption of this magnitude would likely require the Brent curve front to return to a slight contango later in the year. Applying our regression relationship to our forecast inventory trajectory suggests that while near-term de-escalation could pull Brent back into the low $60s, the accumulation of OECD commercial stocks in H2, under purely fundamental conditions, could be consistent with deeper contango and front-month prices closer to the high $50s.

In practice, however, prices are unlikely to be determined by pure fundamentals alone. Recent weeks have again highlighted that geopolitical risk premiums can provide material support to the front end, particularly on price softness, creating a negative feedback loop when prices fall.

On this basis, our base expectation is for the front-month Brent price to gradually slide towards around $60/bbl as 2026 progresses, but we see limited room for prices to sustain materially below that level unless geopolitical risks see clearer and more lasting relief.

Figure 13: After a weak January, OPEC 9+3 production is on track for a ~1.2 mb/d m/m rebound in February

Câu hỏi Liên quan

QWhat are the four scenarios analyzed by MS regarding the Iranian situation and its impact on the crude oil market?![]()

AThe four scenarios are: 1) No supply disruption: De-escalation and risk premium fade; 2) Limited strikes and short-term logistical friction; 3) Localized Iranian export disruption: Broader strikes but no shipping damage; 4) Fleet efficiency shock and shipping damage (tail risk).

QWhat is the estimated risk premium embedded in the current Brent crude oil price according to the 'No supply disruption' scenario?![]()

AThe estimated risk premium embedded in the current Brent crude oil price is approximately $7-9 per barrel.

QIn the 'Limited strikes and short-term logistical friction' scenario, what is identified as the key balancing mechanism for the oil market?![]()

AThe key balancing mechanism identified is the slowing of China's strategic inventory accumulation in response to higher prices and a deepening backwardation.

QWhat is the primary mechanism of supply disruption in the 'Fleet efficiency shock' tail risk scenario, and what is its estimated impact?![]()

AThe primary mechanism is a reduction in tanker fleet efficiency due to shipping delays and increased risk, which is estimated to create an effective supply tightness equivalent to 2-3 million barrels per day for several weeks.

QWhat is MS's base case forecast for the Brent crude oil price once the current geopolitical risk premium fades, and what is the fundamental reason for this forecast?![]()

AMS's base case forecast is for Brent crude oil to gradually slide toward approximately $60 per barrel. The fundamental reason is an expected supply surplus, with their balance pointing to a surplus of about 2.5 million barrels per day in H1 2026 and 1.4 million barrels per day in H2 2026, leading to inventory builds and a potential shift to a contango market structure.