Abstract

Three Arrows Capital’s aggressive investment strategies and poor risk management contributed to its failure to maintain short-term liquid assets to cover its liabilities. With over US$300 million of assets having been liquidated since mid-June, the hedge fund’s liquidity crisis has contributed to a domino effect, causing a cascade of liquidity problems among its investors.

Their collapse revealed underlying risks associated with the speculation of leveraged positions with major lending protocols. This unfortunate situation also shed light on the substantial risks from uncollateralized crypto loans, which currently stand at US$1billion.

With 3AC’s insolvency having caused a cascade of liquidity shortages in the market, the fallout would be worse if borrowers run out of liquidity to repay the US$1billion worth of uncollateralized loans, which are short-term in nature. More attention should be given to Amber Group and Wintermute Trading, the biggest borrowers in the uncollateralized lending market, with a total loan value of US$161.3 million and US$163.6, respectively.

1. The Domino Effect of Three Arrows Capital’s Liquidity Crisis

Following the liquidity crisis of Three Arrows Capital (3AC), investors were concerned that their funds in other protocols were also at risk as 3AC was one of the biggest funds in the industry. 3AC’s collapse had already triggered a domino effect, causing more firms to face liquidity problems.

Investors of 3AC, especially those who lent money to the hedge fund, suffered huge losses. On June 24, Finblox, an investment partner and lender of 3AC, reported that its multiple demands for 3AC’s full loan repayment were unsuccessful. Finblox continued to limit withdrawals as it was also mired in a liquidity crisis. BlockFi, a cryptocurrency lender as well as an investment partner of 3AC, liquidated some of 3AC’s positions, according to the Financial Times. Michael Moro, CEO of Genesis, tweeted on June 17 that the company liquidated a position with their large counterparty who failed to meet a margin call. The collateral was sold into the market without impacting their clients’ funds.

Celsius also blocked withdrawals on its platform as it had faced liquidity issues since June 16. Voyager Digital issued a loan default notice to 3AC on June 28 over a US$670 million debt. Many crypto firms were already dragged into the crisis. In the following sections we will explain how other institutions and protocols were affected by 3AC’s liquidity crisis, and look into two risky protocols offering uncollateralized loans.

2. Understanding how Three Arrows Capital was related to other institutions and decentralized protocols

Currently, AAVE, Compound and MakerDAO are the largest decentralized lending protocols in the crypto space. Together they hold billions of crypto assets for borrowing. As of October 2021, the three platforms held over US$60 billion of crypto assets. While these large crypto lenders played an important role in facilitating capital utilization, they also facilitated speculation on the other side by allowing big position leveraging on the back of abundant liquidity. They also offered attractive interest rates to encourage funds and institutions like 3AC to borrow for trading and investing.

Leverage on these decentralized protocols can be increased by cycled lending. This is particularly lucrative to aggressive fund managers like 3AC. As US$1 billion worth of ETH can be collateralized to take a US$800 million loan in any available stablecoin (maximum borrowing capacity of ETH on AAVE is 80%), which can then be used to purchase the equivalent value in ETH on exchanges. Aggressive traders tend to redeposit the purchased ETH and take out another loan to purchase more ETH. Cycled lending can increase leverage multiple times. It is commonly used for aggressive and big LONG positions.

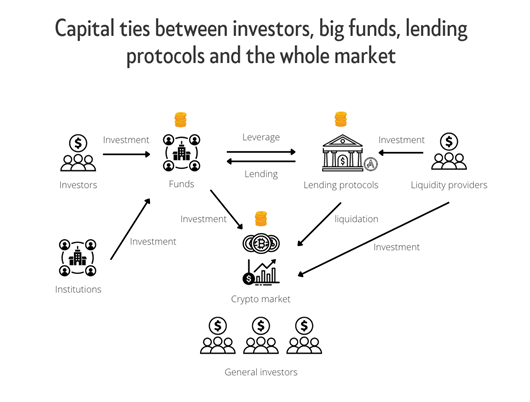

(Figure 1: Capital flow chart)

Large funds and lending protocols that raised funds from investors pooled capital and created gravity in the market. This resulted in significant selling pressure upon the liquidation of large positions.

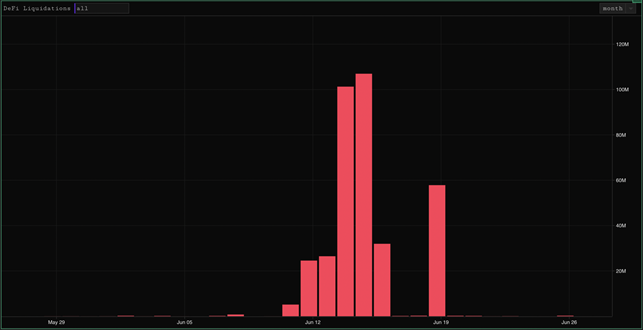

(Figure 2: Parsec Finance historical liquidation chart)

A cascade of liquidations took place between June 11 and June 19, clearing out risky leveraged positions on major decentralized lending protocols (see Figure 2). These positions, worth over US$400 million in total, likely belonged to 3AC and Celsius, which faced liquidity crises in that period. Currently, liquidation risks on AAVE, Compound and Maker remain low, as the market starts to consolidate at higher price levels.

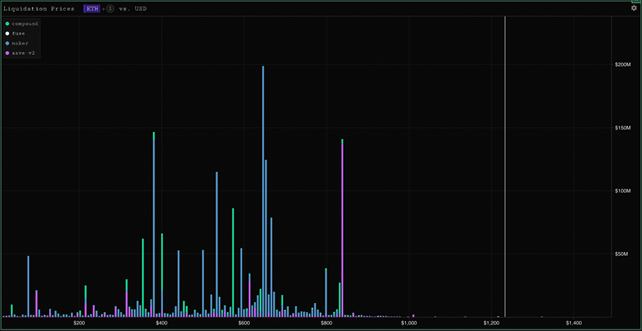

(Figure 3: Parsec Finance ETH liquidation prices)

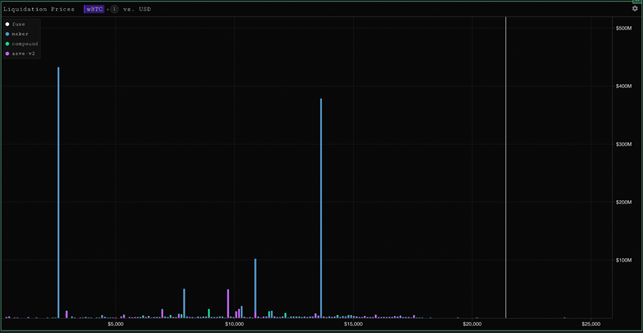

(Figure 4: Parsec Finance wBTC liquidation prices)

It is reasonable to surmise that firms which had close investment ties with 3AC already suffered from liquidity crises, and possibly executed some liquidations since mid-June (Figure 2).

The interconnected nature of fund managers and large lending protocols contributed to the domino effect triggered by 3AC’s liquidity crisis. As they borrowed heavily from each other, when one of them lacks liquidity the rest tend to face the same problem eventually. In Chapter 3.0, we will examine the risks associated with two other protocols offering uncollateralized loans – Maple Finance and True Finance.

3. Who will be Next? Risks from uncollateralized lending protocol

Maple Finance and True Finance are two lending protocols which offer uncollateralized institutional crypto loans. In other words, the two lending protocols allow institutional borrowers looking to leverage their reputations to borrow uncollateralized loans to fund operations and grow their business. The loans come from lenders that provide capital to various pools to earn interest from institutional borrowers, as well as any associated lending rewards. Uncollateralized loans are without doubt riskier than collateralized loans, because in the event of default investors get nothing.

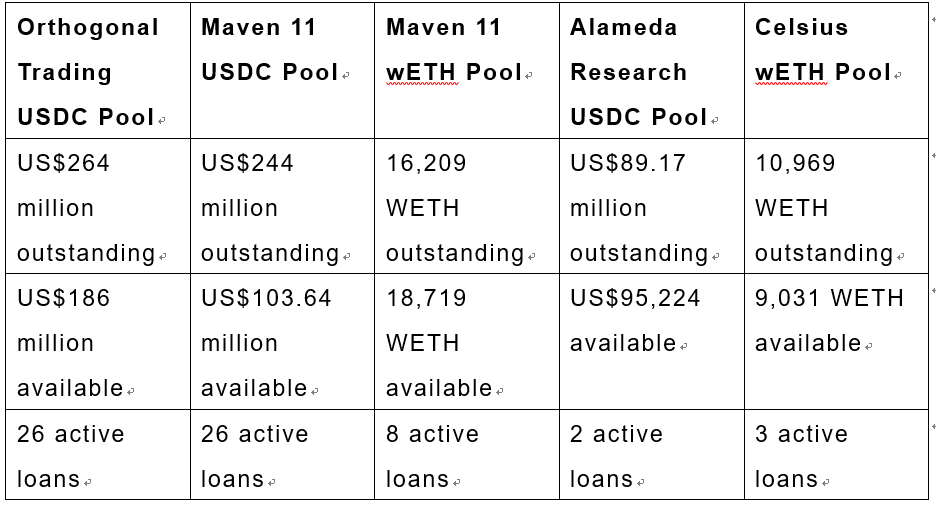

Currently, Maple Finance has total outstanding loans of approximately US$640 million in its Ethereum Pools, and US$113.9 million in its Solana Pools. There are five pools available for institutions to borrow on Ethereum and two pools on Solana. Lending Pools are established and managed by credit experts and asset managers, known as Pool Delegates. The latter participate by liaising with borrowers, assessing their credit worthiness and reaching an agreement on terms before lending from their actively managed Lending Pool. Once Pool Delegates create a Lending Pool, they are required to provide Pool Cover to their Lending Pool to serve as first-loss capital to the Pools, aligning their interests with Lenders. Statistics for the five Ethereum pools appear in the following table:

(Table 1: Maple Lending Pools Statistics)

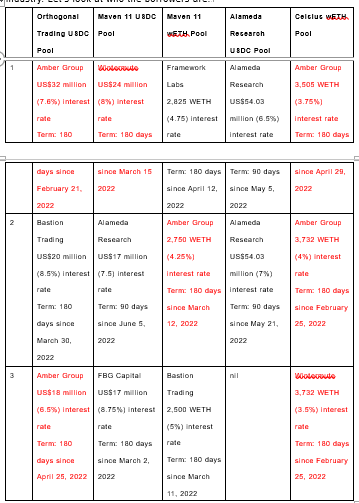

There were 65 borrowers who took out US$640 million in uncollateralized loans from these lenders in the bear market. The risk here speaks for itself as there has already been a cascade of liquidity crises across the crypto industry. Let’s look at who the borrowers are:

(Table 2: Maple Borrowers Statistics)

TrueFi has a Total Value Locked (TVL) of US$380 million across 4 different lending pools: BUSD, USDC, USDT and TUSD. The largest pools are USDC (US$147 million) and USDT (US$180 million).

(Figure 5: TrueFi Largest Borrowers Statistics)

The largest borrowers are Wintermute Trading, Alameda Research and Amber Group. Amber Group took a total of 10 uncollateralized loans totaling US$161.3 million on Maple and TrueFi:

1. $32 million in USDC maturing in August 2022 (Maple) ETH pool

2. $18 million in USDC maturing in October 2022 (Maple) ETH pool

3. 2,750 WETH (~US$3.18 million) maturing in September 2022 (Maple) ETH pool

4. 3,505 WETH (~US$4.05 million) maturing in October 2022 (Maple) ETH pool

5. 3,732 WETH (~US$4.31 million) maturing in August 2022 (Maple) ETH pool

6. $38.44 million in USDT maturing in August 2022 (TrueFi) ETH pool

7. $27.42 million in USDC maturing in August 2022 (TrueFi) ETH pool

8. $1.91 million in USDC maturing in August 2022 (Maple) Solona Pool

9. $7 million in USDC maturing in July 2022 (Maple) Solona Pool

10. $25 million in USDC maturing in September 2022 (Maple) Solona Pool

Wintermute Trading has 4 active uncollateralized loans totaling US$163.57 million on Maple and TrueFi:

1. $92.05 million in USDT maturing in October 2022 (TrueFi) ETH pool

2. $17 million in USDC maturing in September 2022 (Maple) ETH pool

3. 3,732 WETH (~US$4.52 million) maturing in August 2022 (Maple) ETH pool

4. $50 million USDC maturing in September 2022 (Maple) Solana Pool

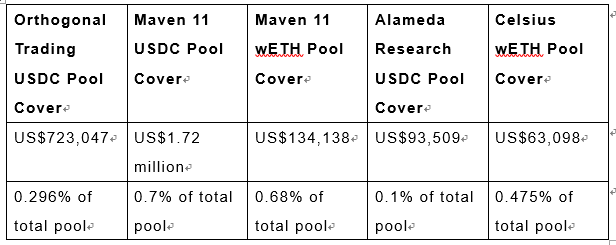

Amber Group and Wintermute Trading merit more attention when it comes to their current financial status. If they fail to repay their loans, investors who participated in the lending pools will have to bear the loss. There will be no assets to liquidate. In case of defaults, the Pool Delegate will provide a cover fund for compensation. Unfortunately, the size of the fund is insignificant compared with the pool size.

Cover amount in case of defaults on Maple Pools:

In fact, problems had already surfaced with borrowers defaulting on the uncollateralized loans. On June 20, Babel Finance halted withdrawals and acknowledged a liquidity problem. Babel had taken a US$10 million uncollateralized loan from the Orthogonal USDC pool on Maple, and is now unable to repay the loan.

(Figure 6: Tweeter @Maplefinance)

Two days after Babel’s notice, Maple announced that Orthogonal had been in daily contact with the borrower. However, there was still no update about Babel’s repayment arrangement nor any plan to handle the situation. With no collateral to sell, the incurred loss had to be shared among the lenders. Lending pool investors will get some protection from the small cover fund.

4. Reflection

Decentralized lending protocols played four major roles in the last bull run:

1) Enabled advanced investment strategies and higher capital utilization

2) Promoted institutional participation

3) Deepened liquidity

4) Facilitated speculation

This special financial product was a double-edged sword which nurtured and boosted growth in the space. On the other hand, it stepped up inorganic growth and caused speculative implosion at the end by enabling cycled lending. The failure of 3AC was an example which revealed the danger of poor risk management and aggressive investment strategies. (The speculative element took the form of highly leveraged investments without risk diversification, as reflected by its critical US$559.6 million loss from investing in Luna and Terra).

As the crypto market remains quiet in the bear market, more attention should be paid to uncollateralized lending such as Maple and TrueFi, as well as their borrowers. This is because uncollateralized loans are much riskier than collateralized loans, and there has already been a cascade of liquidity crises in the industry.

We should pay extra attention to uncollateralized borrowers’ financial status and their ability to overcome potential liquidity crises. If the market gets more bearish, more institutions will see a devaluation of their asset base and run out of liquidity to cover their liabilities. Eventually, they would prioritize their resources to secure their collateralized loans to reduce losses (where they could at least get their collateral back and sell their assets for more liquidity by clearing these debts). The uncollateralized loans would be in jeopardy, resulting in huge losses for the lending pool investors.

The contagion effect of the liquidity crises will be severe, and the aftermath is expected to be marked by a further market decline and more serious capitulations. Therefore, the ability of Amber Group and Wintermute Trading, the largest borrowers of all uncollateralized loans, to repay their uncollateralized loans maturing in the coming months will serve as a barometer of market sentiment. If the two show signs of their inability to pay back their loans (which can be conjectured if they took on more uncollateralized loans in August to cover their previous debts), we should expect a cascade of similar liquidity crises to take place.

About Huobi Research Institute

Huobi Blockchain Application Research Institute (referred to as "Huobi Research Institute") was established in April 2016. Since March 2018, it has been committed to comprehensively expanding the research and exploration of various fields of blockchain. As the research object, the research goal is to accelerate the research and development of blockchain technology, promote the application of blockchain industry, and promote the ecological optimization of the blockchain industry. The main research content includes industry trends, technology paths, application innovations in the blockchain field, Model exploration, etc. Based on the principles of public welfare, rigor and innovation, Huobi Research Institute will carry out extensive and in-depth cooperation with governments, enterprises, universities and other institutions through various forms to build a research platform covering the complete industrial chain of the blockchain. Industry professionals provide a solid theoretical basis and trend judgments to promote the healthy and sustainable development of the entire blockchain industry.

Official website:

https://research.huobi.com/

Consulting email:

research@huobi.com

Twitter: @Huobi_Research

https://twitter.com/Huobi_Research

Medium: Huobi Research

https://medium.com/huobi-research

Disclaimer

1. The author of this report and his organization do not have any relationship that affects the objectivity, independence, and fairness of the report with other third parties involved in this report.

2. The information and data cited in this report are from compliance channels. The sources of the information and data are considered reliable by the author, and necessary verifications have been made for their authenticity, accuracy and completeness, but the author makes no guarantee for their authenticity, accuracy or completeness.

3. The content of the report is for reference only, and the facts and opinions in the report do not constitute business, investment and other related recommendations. The author does not assume any responsibility for the losses caused by the use of the contents of this report, unless clearly stipulated by laws and regulations. Readers should not only make business and investment decisions based on this report, nor should they lose their ability to make independent judgments based on this report.

4. The information, opinions and inferences contained in this report only reflect the judgments of the researchers on the date of finalizing this report. In the future, based on industry changes and data and information updates, there is the possibility of updates of opinions and judgments.

5. The copyright of this report is only owned by Huobi Blockchain Research Institute. If you need to quote the content of this report, please indicate the source. If you need a large amount of reference, please inform in advance (see "About Huobi Blockchain Research Institute" for contact information) and use it within the allowed scope. Under no circumstances shall this report be quoted, deleted or modified contrary to the original intent.