Author: Zhao Ying

Source: Wall Street News

Trump will personally preside over the swearing-in ceremony of the new Fed Chairman, Kevin Warsh. This arrangement, which breaks recent conventions, once again thrusts the decades-long power game between the White House and the Federal Reserve into the spotlight. History shows that every Fed Chair has had to seek a balance between political pressure and policy independence, and Warsh is no exception—but the situation he faces is far more complex than outsiders imagine.

According to the Wall Street Journal, citing White House officials, Trump will preside over Warsh's swearing-in ceremony at the White House this Friday. This move breaks with recent practice—inauguration ceremonies are typically held internally at the Fed, with the president rarely attending in person. The last time a Fed Chair's swearing-in ceremony was held at the White House dates back nearly forty years to Alan Greenspan's inauguration in 1987.

The Fixed Income team at Caitong Securities (Sun Binbin, Sui Xiuping, Lu Xingchen) pointed out in their latest research report that although Warsh is not a "dovish chair," it cannot be ruled out that there will be no rate cuts this year—the relationship between the Fed Chair and the U.S. President is not static but evolves over time.

However, Warsh is not inheriting a unified and ready Federal Reserve. At the late April FOMC meeting, Governors Hammack (Cleveland), Kashkari (Minneapolis), and Logan (Dallas) cast the most unusual dissenting votes since October 1992—they did not oppose the idea of rate cuts themselves but argued against even hinting at them. This means Warsh inherits a central bank already showing internal fractures, precisely as Trump expects him to deliver rate cuts.

White House Inauguration: An Arrangement Full of Political Signals

The arrangement of the inauguration ceremony itself sends a strong signal. When Jerome Powell was inaugurated in 2018, the ceremony was held internally at the Fed, and Trump did not attend. The most recent sitting president to attend an inauguration was George W. Bush, who attended Ben Bernanke's swearing-in in 2006. Trump's personal hosting this time directly underscores his close attention to this Fed appointment.

At the procedural level, this transition process has also been unusually lengthy. Warsh was confirmed by the Senate last week, receiving a four-year term. Powell's term as Chair ended last weekend, but he stated he would remain on the Fed Board as a Governor, a term that lasts until January 2028. Warsh also agreed to divest some personal investments before formally taking office, which delayed the transition to some extent. During the interim, Fed Vice Chair Philip Jefferson represented the central bank at the G7 finance ministers and central bank governors meeting in Paris this Monday.

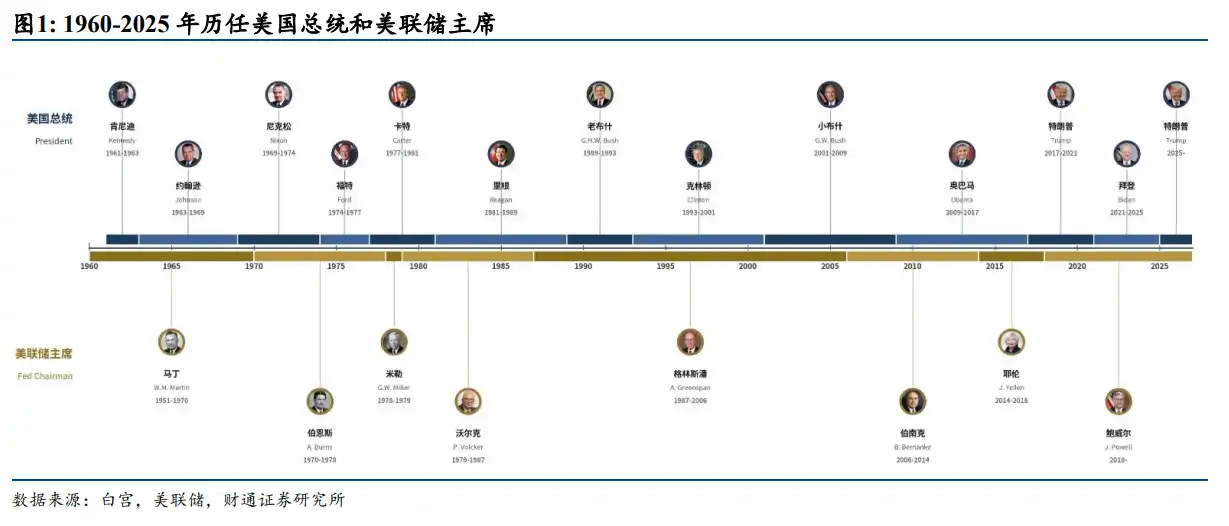

70 Years of Rivalry: From Martin to Powell

Caitong Securities' report systematically reviews the history of the relationships between each Fed Chair and the President since 1960, outlining a clear evolutionary path.

William Martin, facing a lack of institutional moats, could only rely on personal credibility to guard independence. After taking office, he refused to act as the Treasury's agent, shifted the Fed's decision-making center from New York to Washington, and expanded decision-making authority to the entire FOMC. When Truman saw him on a New York street, he just threw out the word "Traitor" and walked away.

Arthur Burns's failure stemmed from his own disbelief that monetary policy could end inflation, which opened the door to Nixon's political pressure. Nixon applied pressure through private letters, intervened in Board personnel composition, and even sent senior advisors to directly lecture Fed staff. Burns preserved institutional independence in form but made significant compromises on substantive policy direction, ultimately destroying the Fed's credibility.

William Miller represents the most direct political coordination model—deliberately chosen to align with Carter's political goals, but backfired in the face of external crises. By the summer of 1979, inflation had become Carter's biggest political crisis. Miller was moved to Treasury Secretary, making way for appointing a true inflation hawk.

Paul Volcker elevated independence from "personal credibility defense" to a triple moat of "personal credibility + institutional framework + market credibility." Carter, knowing appointing Volcker would come at a political cost, still made the choice—as his policy advisor Eizenstat said, it "ultimately squeezed him out of a second term, at the cost of high unemployment, while squeezing out inflation." Though Reagan "ordered" Volcker not to raise rates before the 1984 election and launched an "FOMC ambush" through appointed governors in 1986, he ultimately failed to substantively change policy direction.

Alan Greenspan used technocratic rhetoric to push the struggle below the surface, clashing fiercely with George H. W. Bush, reaching a "Washington-style peace" with Clinton, but overstepping to support tax cuts under George W. Bush, becoming the first Fed Chair in history to actively "invade" the realm of fiscal policy.

Ben Bernanke embodied a model of natural convergence between the White House and the Fed under crisis conditions, with his main pressures coming from Congress and within the Fed, not the White House. Janet Yellen countered Trump's attacks with "non-political language + strict self-restraint," becoming the first Fed Chair to be replaced by an incoming president since Carter did not reappoint Burns.

Jerome Powell faced presidential pressure more severe than any Chair since Burns. During Trump's first term, under combined external political pressure and internal economic judgment, Powell cut rates three times consecutively in 2019 and stopped balance sheet reduction. In Trump's second term, facing investigations launched by Trump over cost overruns in the Fed's Washington headquarters renovation and hints of dismissal, Powell's response significantly hardened, elevating the defense of Fed independence to a historically new level of legalization, documentation, and publicity. In his final meeting as Chair, the FOMC held rates steady with an unusually split 8-4 vote.

Warsh's Dilemma: A New Chair Caught in Internal and External Troubles

The situation Warsh inherits is quite rare in history—he simultaneously faces rate cut pressure from the White House and hawkish resistance from within the FOMC.

Warsh is not a traditional dove. Appointed as a Fed Governor by George W. Bush in 2006 at age 35, he was one of the youngest governors in Fed history. After QE2 was formally launched in 2010, he became the only Governor in the FOMC to publicly question its expansionary direction and resigned early in 2011, widely interpreted by the market as a silent protest against the Fed's excessive easing. His background as a Morgan Stanley investment banker, Executive Secretary of the White House NEC, and close ties to Republican core circles suggest his policy independence expectations are no lower than those of historically similar chairs.

Caitong Securities' report outlines four key points from Warsh's recent speeches and Q&A sessions:

- First, his definition of Fed independence is more nuanced than his predecessors'. He believes politicians' comments on monetary policy do not affect Fed independence. This is both a desensitization tactic towards Trump's pressure and leaves room to maintain policy independence in the future without open conflict.

- Second, he holds a negative view of forward guidance. Markets may need to adapt to a more "silent" Fed.

- Third, he takes inflation very seriously, directly refuting Trump's view that rising oil prices represent "fake inflation."

- Fourth, he believes productivity gains from artificial intelligence will make rate cuts possible, sharing a similar logical structure to Greenspan's insights during the late 1990s productivity boom.

Rate Cuts and Balance Sheet Reduction: Direction Certain, Pace Cautious

Caitong Securities believes that monetary policy under Warsh will likely feature "certain direction but cautious pace."

Regarding the pace of rate cuts, with inflation exceeding the target for five consecutive years, the priority of stabilizing inflation expectations is higher. Warsh's serious attitude towards inflation, especially his denial of "fake inflation," indicates he will not easily cut rates before inflation clearly returns to the target range. In the short term, demand growth driven by data center investment may further offset room for rate cuts, causing the pace of cuts to be constrained by data and slow down. The report notes that if Trump shows Warsh more respect, rate cuts may come earlier; if Trump continues high-intensity pressure, to defend Fed independence, Warsh would instead lean towards cutting later.

Regarding the pace of balance sheet reduction, Warsh believes the expanded balance sheet has effectively extended the Fed's monetary policy boundary into the fiscal domain, making reduction logically necessary. But he also acknowledges that it took the Fed 18 years to accumulate the balance sheet to this extent, and reducing it is not an overnight task; it's expected to proceed slowly and methodically. Furthermore, starting balance sheet reduction without having cut rates could almost be seen as proactively picking a fight with the White House—this also dictates that reduction will proceed at a pace that avoids a direct confrontation before the rate-cutting cycle begins.

Caitong Securities' core conclusion is: Recreating Greenspan-style management and returning to a scarce reserve model first require winning support within the Fed itself; moving too hastily will only backfire. Judging Warsh's future policy path should not rely solely on his personal stance or his current relationship with the White House but should return to macro trends—the position of inflation, growth elasticity, oil price direction, financial condition tightness—to deduce his most likely choices under different scenarios.