"As long as you don't invest in Crypto, you can make money in everything else."

Recently, the crypto market and other global markets seem to be worlds apart.

In 2025, gold rose over 60%, silver surged 210.9%, and the U.S. Russell 2000 index increased by 12.8%. Bitcoin, however, ended the year in the red after a brief new high.

Entering 2026, the divergence is intensifying. On January 20, gold and silver hit new highs again, the U.S. Russell 2000 index outperformed the S&P 500 for 11 consecutive days, and China's STAR 50 index gained over 15% in a single month. Bitcoin, on the other hand, fell for five consecutive days on January 20, dropping from $98,000 to $91,000 without looking back.

Funds seem to have decisively left the crypto market after 10/11. BTC has been oscillating below the $100,000 mark for over three months, and the market has entered a period of "the lowest volatility in history."

Disappointment is spreading among crypto investors. When asked about investors who left Crypto and made money in other markets, they even shared the "ABC" secret—"Anything But Crypto"—meaning as long as you don't invest in Crypto, you can make money anywhere else.

The "Mass Adoption" everyone anticipated in the last cycle has indeed arrived, but not in the form of decentralized application普及 everyone hoped for. Instead, it's a complete "assetization" led by Wall Street.

This round has seen the U.S. establishment and Wall Street embrace Crypto with unprecedented enthusiasm. The SEC approved Bitcoin spot ETFs from BlackRock, Fidelity, and others; BlackRock and JPMorgan have allocated assets to Ethereum; the U.S. government passed legislation to establish a national strategic Bitcoin reserve; pension funds in several states have invested in Bitcoin; the SEC chairman publicly stated that U.S. stocks would be on-chain within two years; and even the New York Stock Exchange (NYSE) announced plans to launch its own cryptocurrency trading platform.

So the question arises: Why, after gaining so much political and capital backing, is Bitcoin's price performance so disappointing when precious metals and stock markets are hitting new highs?

When crypto investors have become accustomed to checking pre-market U.S. stock prices to gauge crypto market movements, why is Bitcoin not rising along with them?

Why Is Bitcoin So Weak?

Leading Indicator

Bitcoin is a "leading indicator" for global risk assets, as Real Vision founder Raoul Pal has repeatedly mentioned in his articles. Because Bitcoin's price is purely driven by global liquidity and is not directly affected by national earnings reports or interest rates, its fluctuations often lead those of mainstream risk assets like the Nasdaq index.

According to MacroMicro data, Bitcoin's price turning points have repeatedly领先 the S&P 500 index in recent years. Therefore, once Bitcoin, as a leading indicator, stalls in its upward momentum and fails to make new highs, it serves as a strong warning signal that the upward momentum of other assets may also be nearing exhaustion.

Liquidity Tightening

Secondly, Bitcoin's price, to this day, remains highly correlated with global net dollar liquidity. Although the Fed cut interest rates in 2024 and 2025, the quantitative tightening (QT) that began in 2022 is still continuously draining liquidity from the market.

Bitcoin hitting new highs in 2025 was more due to new funds brought by ETF approvals, but this did not change the fundamental landscape of tight global macro liquidity. Bitcoin's sideways movement is a direct reaction to this macro reality. In an environment short on money, it's difficult for it to start a super bull market.

The world's second-largest source of liquidity—the yen—is also tightening. The Bank of Japan raised its short-term policy rate to 0.75% in December 2025, the highest level in nearly 30 years. This directly impacts a crucial source of funding for global risk assets over the past decades: the yen carry trade. Historical data shows that since 2024, all three rate hikes by the Bank of Japan were accompanied by Bitcoin price drops of over 20%. Synchronized tightening by the Fed and the Bank of Japan has made the global liquidity environment even worse.

Geopolitical Conflict

Finally, potential geopolitical "black swans" are keeping market nerves on edge, and Trump's series of domestic and international actions in early 2026 have pushed this uncertainty to new heights.

Internationally, the actions of the Trump administration are full of unpredictability. From military intervention in Venezuela and capturing its president (unprecedented in modern international relations) to war with Iran again being on the brink; from attempting to forcibly purchase Greenland to issuing new tariff threats against the EU. This series of aggressive unilateral actions is comprehensively intensifying major power矛盾.

Domestically in the U.S., his measures have sparked deep public concern about a constitutional crisis. He not only proposed renaming the "Department of Defense" to the "Department of War" but has also ordered active-duty troops to prepare for potential domestic deployment.

These actions, combined with his past暗示 of regretting not using military force and unwillingness to accept midterm election losses, have made public担忧 increasingly clear: Would he refuse to accept a midterm election loss and use force to stay in power? This speculation and high pressure are already intensifying internal U.S. conflicts, with protests currently showing signs of expanding.

The normalization of such conflicts is dragging the world into a "gray zone" between localized war and a new Cold War. Traditional full-scale hot war had relatively clear paths, market expectations, and was even accompanied by stimulus "bailouts."

The destructive power of these localized conflicts lies in their extreme uncertainty, full of "unknown unknowns." For risk capital markets that highly rely on stable expectations, this uncertainty is fatal, as it significantly increases market risk premiums. When large capitals cannot predict the future, the most rational choice is to increase cash holdings and wait on the sidelines, rather than allocating funds to high-risk, high-volatility assets.

Why Aren't Other Assets Falling?

In stark contrast to the crypto market's stagnation, since 2025, markets like precious metals, U.S. stocks, and A-shares have taken turns rising. However, the rise in these markets is not due to a普遍 improvement in macro and liquidity fundamentals, but rather structural rallies driven by sovereign will and industrial policy against the backdrop of great power competition.

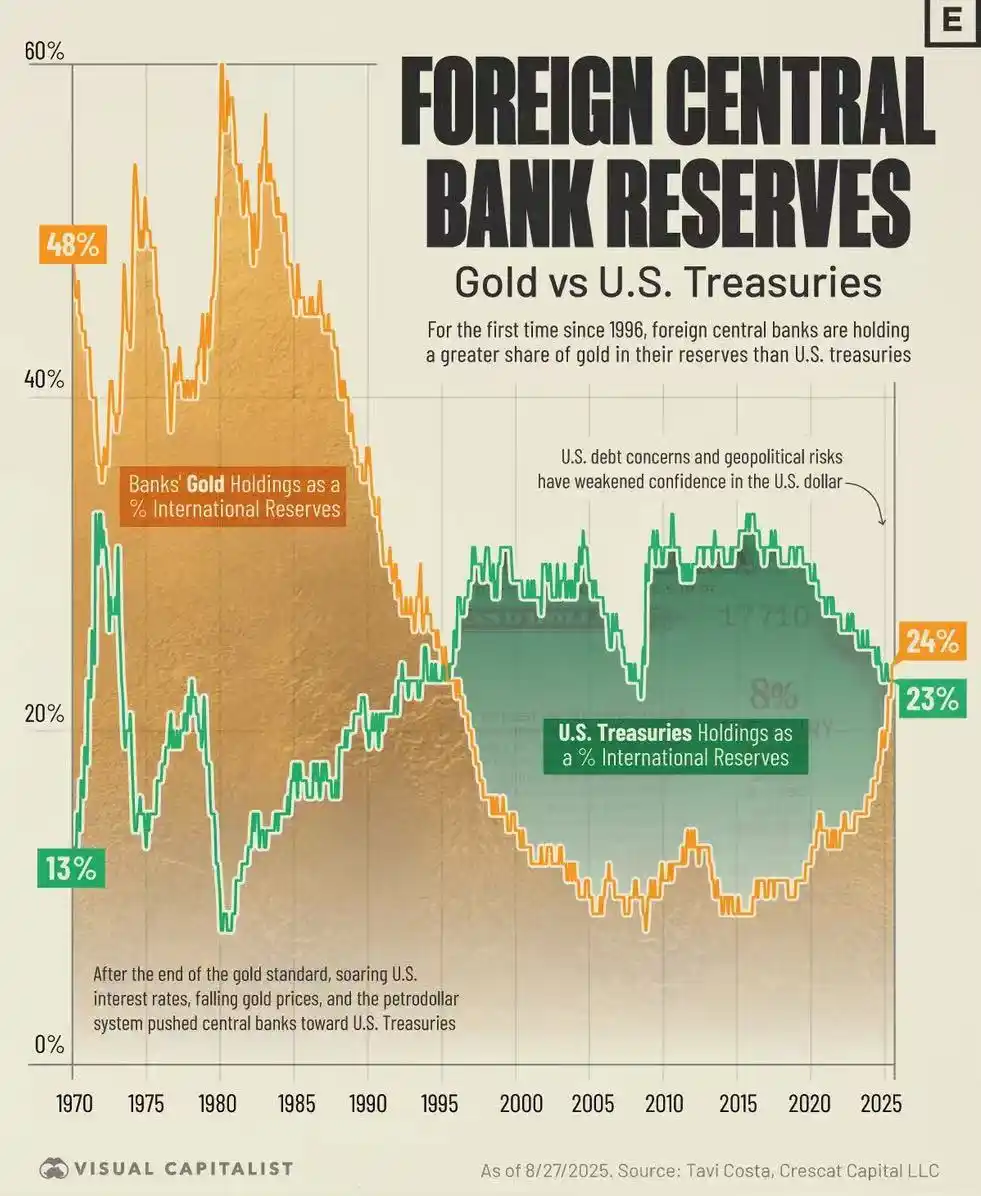

Gold's rise is a reaction by sovereign states to the existing international order, rooted in the credibility cracks of the dollar system. The 2008 global financial tsunami and the 2022 freezing of Russia's foreign exchange reserves彻底 shattered the "risk-free" myth of the U.S. dollar and Treasury bonds as the world's ultimate reserve assets. In this context, global central banks have become "price-insensitive buyers." They buy gold not for short-term profits, but to find an ultimate store of value that does not rely on any single sovereign credit.

Data from the World Gold Council shows that in 2022 and 2023, global central banks' net gold purchases exceeded 1,000 tons for two consecutive years, setting historical records. The main driver of this gold rally is official power, not market speculation.

The stock market's rise, on the other hand, is a reflection of national industrial policies. Whether it's the U.S. "AI Nationalization" strategy or China's "Industrial Self-Reliance" policy, state power is deeply介入 and directing capital flows.

Take the U.S., for example. Through the CHIPS and Science Act, the AI industry has been elevated to a national security战略 priority. Funds are明显 flowing out of large tech stocks and into more growth-oriented small and mid-cap stocks that align with policy directions.

In China's A-share market, funds are also highly concentrated in areas closely related to national security and industrial upgrading, such as "信创" (IT application innovation) and "国防军工" (national defense and military industry). This type of government-driven rally has a pricing logic that naturally存在 a hard-to-bridge gap with Bitcoin, which relies on purely market-driven liquidity.

Will History Repeat Itself?

Historically, it's not the first time Bitcoin's performance has diverged from other assets. And each time, the divergence ended with a strong rebound in Bitcoin.

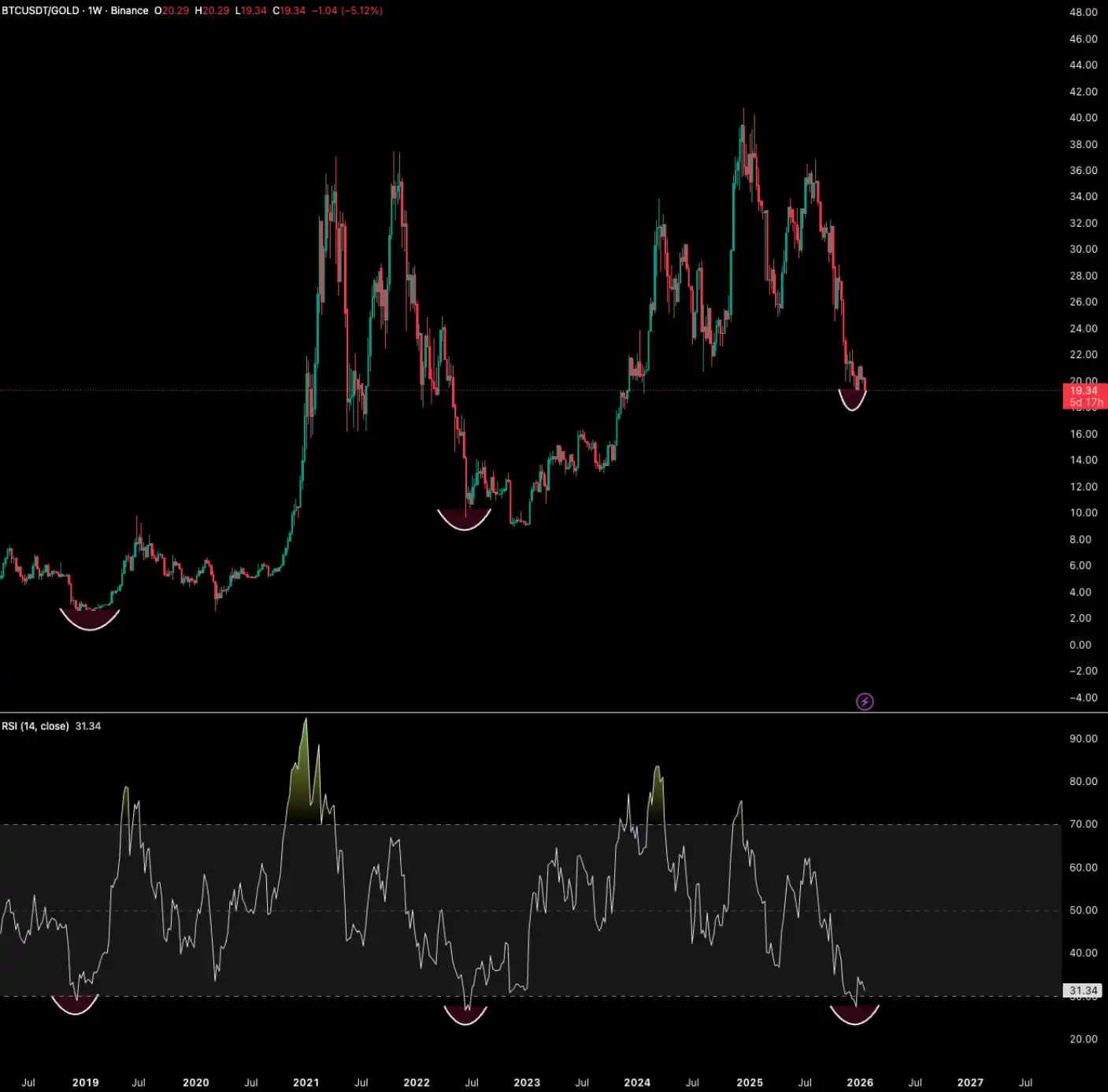

Historically, there have been four instances where Bitcoin's RSI (Relative Strength Index) against gold fell below 30, indicating extreme oversold conditions: in 2015, 2018, 2022, and 2025. Each time, when Bitcoin was极度 undervalued relative to gold, it预示 a subsequent significant rebound.

In 2015, at the end of the bear market, Bitcoin's RSI against gold fell below 30, subsequently launching the 2016-2017 super bull market.

In 2018, during the bear market, Bitcoin fell over 40%, while gold rose nearly 6%. After the RSI fell below 30, Bitcoin反弹 over 770% from its 2020 low.

In 2022, during the bear market, Bitcoin fell nearly 60%. After the RSI fell below 30, Bitcoin recovered strongly in 2024 and early 2025, outperforming gold again.

From late 2025 to now, we are witnessing this historic oversold signal for the fourth time. Gold surged 64% in 2025, and Bitcoin's RSI against gold has once again fallen into oversold territory.

Is It Still Time to Chase Other Rising Assets?

Amid the "ABC" noise,轻易 selling crypto assets to chase other currently booming markets might be a dangerous decision.

When U.S. small-cap stocks start leading gains, it has historically often been the final狂欢 before liquidity dries up at the end of a bull market. The Russell 2000 index has risen over 45% from its 2025 low, but most of its components have relatively poor profitability and are very sensitive to interest rate changes. Once the Fed's monetary policy falls short of expectations, the fragility of these companies will be immediately exposed.

Secondly, the AI sector's狂热 is showing typical bubble characteristics. Whether it's Deutsche Bank's survey or warnings from Bridgewater founder Ray Dalio, the AI bubble is listed as the biggest market risk for 2026. Valuations of star companies like Nvidia and Palantir have reached historical highs, and whether their profit growth can support such high valuations is being questioned more and more. A deeper risk is that AI's enormous energy consumption could trigger a new round of inflationary pressure, forcing central banks to tighten monetary policy and burst the asset bubble.

According to Bank of America's fund manager survey in January, global investor optimism hit a new high since July 2021, and global growth expectations soared. Cash holdings fell to a record low of 3.2%, and protection measures against market corrections are at their lowest level since January 2018.

On one side are疯狂 rising sovereign assets and普遍 optimistic investor sentiment; on the other are escalating geopolitical conflicts.

Against this backdrop, Bitcoin's "stagnation" is not simply "underperforming." It is more like a sobering signal, an early warning of greater risks ahead, and also an accumulation of strength for a grander narrative shift.

For true long-termists, this is precisely the moment to test convictions, resist temptation, and prepare for the coming crises and opportunities.