Author: Nico

Compiled by: Jiahuan, ChainCatcher

Stablecoin digital banking is the next major growth frontier for retail adoption, with foreign exchange (FX) becoming a core component.

Tether and Circle have spent over a decade building liquidity, distribution channels, and network effects around USDT and USDC, which is extremely difficult for new forex stablecoin issuers to replicate.

Instead of competing by issuing spot forex stablecoins, a better path forward is synthetic forex: users continue to hold USDT/USDC as the underlying asset while their account balances are denominated in their preferred local currency.

Stablecoin digital banking is moving beyond crypto-native circles, disrupting how global consumers and businesses transact. Over the past year, approximately $6 billion in venture capital has flowed into this frontier.

However, given the current state of on-chain forex infrastructure, stablecoin digital banks essentially function as banks with US dollar accounts. This limitation presents a massive opportunity, as 95% to 99% of global bookkeeping is not denominated in US dollars.

24x Growth in Under a Year

A clever friend from Tether once told me that diversifying its holder base is one of the company's top three North Star metrics. A holder structure dominated by whales introduces unnecessary volatility to USDT's Total Value Locked (TVL).

All stablecoin issuers want to win over retail and corporate users who use stablecoins for daily transactions and banking, not attract more traders and whales.

In short, one billion people each holding 10 USDT is far better than one whale holding 10 billion.

Stablecoin digital banking presents an excellent opportunity for stablecoins to reach everyday retail and corporate users. Beyond trading, the mass market will experience the convenience and superiority of stablecoins as currencies for payments, savings, and investments, moving beyond the trading use case that currently dominates stablecoin volumes.

A snapshot of the take-off speed for stablecoin digital banking: crypto card spending surged 525% in 2025, jumping from $14.6 million to $91.3 million, with EtherFi leading the way at $55.4 million.

Yesterday, daily spending on the @ether_fi card just surpassed $3.7 million. This translates to an annualized stablecoin spending rate of $1.35 billion, representing a 24x growth from last year.

When something grows 24x in less than a year, you have to pay attention. Also, @ether_fi launched its Euro product last week. I'll elaborate on this later.

The digital bank stablecoin is a new battleground, with no clear leader yet. From 2018 to now, stablecoins with fiat on/off-ramp liquidity and widespread acceptance by centralized exchanges were seen as the best and captured the greatest growth.

How do you win this new battle? What kind of stablecoin is truly suited for digital banking?

Why Forex Stablecoins Matter

Historically, single-currency digital banks have invariably failed to gain market acceptance. Major fintech giants like @Wise, @Revolut, and @airwallex all started out as forex companies. When PayPal went public in 2002, forex accounted for over 40% of its revenue.

International money transfers are much more difficult than domestic ones, which gives these successful digital banks a chance to shine in forex and establish market dominance in specific payment corridors or consumer/business segments.

Therefore, stablecoin digital banks with only US dollar accounts face significant hurdles in growth and differentiation, let alone competing with existing fiat digital banks. 95% to 99% of the world operates in non-USD currencies.

Currently, stablecoin digital banks cannot serve any businesses or consumers among them.

$6 Billion vs. $400 Billion

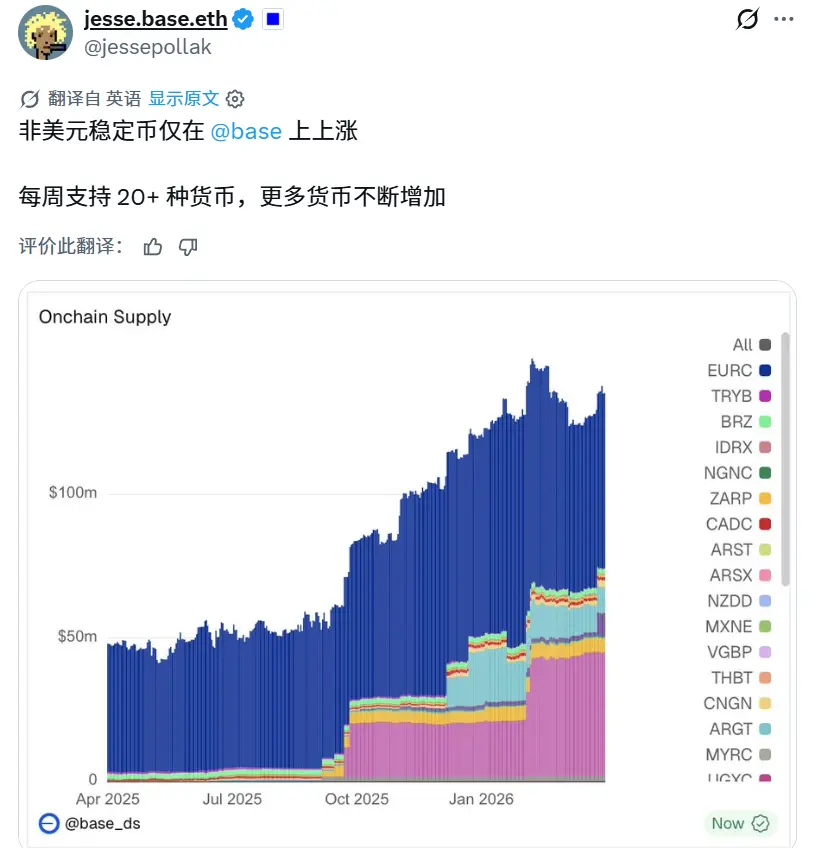

Despite many excellent teams and public chain ecosystems (especially @base and @CodexFX) eyeing the opportunity in forex, the harsh reality is that the total value of all forex stablecoins constitutes an extremely small fraction of the US dollar stablecoin market. Roughly $6 billion versus $400 billion, representing a staggering 700x gap.

If @tether's success has taught us anything, it's that stablecoins are a business with extreme network effects. @Tether's status as the highest-quality stablecoin is due to the vast network built around it.

Given the limited TVL of forex stablecoins, unfortunately, most face the following dilemma:

- Limited liquidity leads to fragile pegs (e.g., the Paxos Gold depegging event on Oct 10 could happen to any forex stablecoin with limited liquidity and TVL; PAXG had a $1.2B TVL, almost triple the size of EURC, the largest forex stablecoin)

- Lack of acceptance by fintech platforms or centralized exchanges

- Even if accepted, fiat on/off-ramp liquidity is very limited

- Limited liquidity against major trading pairs (including vs USDT/USDC)

- Almost no yield opportunities

- Compliance and licensing issues are highly complex across different regions

- Most importantly, due to untested peg mechanisms, stablecoin digital banks and the broader fintech space hesitate to adopt them before they reach a certain scale. This is a chicken-and-egg problem that could take a long time and significant resources to solve.

What Makes a High-Quality Stablecoin?

A great digital bank stablecoin must excel in all the following aspects:

- Fiat on/off-ramp liquidity

- Strong peg stability independent of overall market liquidity

- Yield opportunities

- Liquidity against major trading pairs

- Broad acceptance in CeFi, TradFi, and payments

- Strong presence on low-Gas chains

- Brand and token name recognition

The TradFi Answer

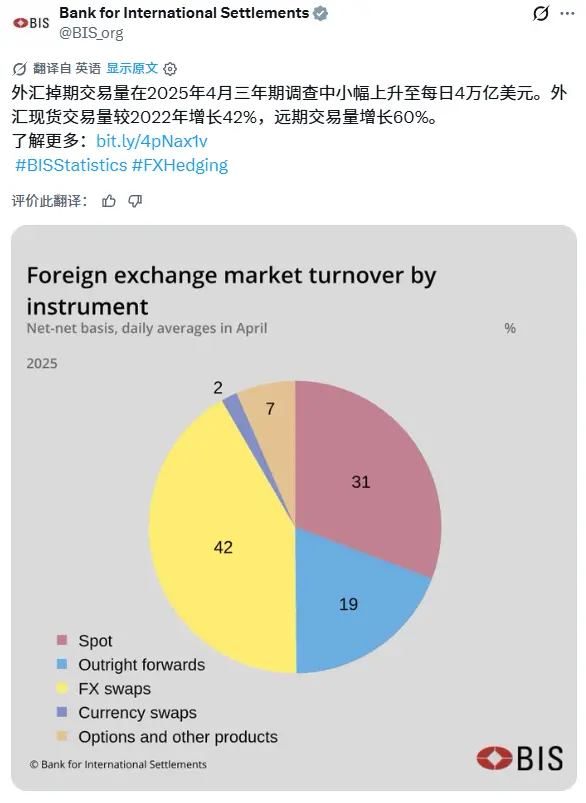

According to the Bank for International Settlements (BIS), only about 31% of global forex trading volume comes from spot transactions, while about 69% comes from derivatives markets. This indicates that modern forex is driven primarily by synthetic exposure, hedging, and financing activity, not physical currency conversion.

Thus, forex swaps settle a notional amount of $4 trillion daily.

One of the most important non-spot forex instruments is the Non-Deliverable Forward (NDF): a cash-settled forex forward contract where no physical currency is delivered. The counterparties do not exchange the underlying currency but settle only the profit or loss difference, typically in US dollars.

NDFs are particularly common where currency convertibility is restricted, offshore access is fragmented, or offshore liquidity is insufficient for efficient physical delivery, making synthetic exposure settled in dollars operationally easier than sourcing and settling local currency directly.

Example:

- A company wants exposure to Swiss Francs (CHF) over the next 3 months.

- Instead of sourcing and settling physical francs, it enters into a CHF NDF, effectively denominating its account in francs while holding dollars.

- At maturity, only the profit/loss difference, denominated in dollars, relative to the agreed exchange rate is exchanged.

Many modern NDF structures are also Mark-to-Market (MtM), meaning unrealized profits and losses are regularly collateralized or settled throughout the contract's life, reducing counterparty risk and improving capital efficiency.

A Mark-to-Market NDF can effectively keep an account's underlying funding in dollars while economically denominating balances and profits/losses in another currency.

The Optimal On-Chain Forex Solution: NDFs, Not Spot

For currencies lacking deep or efficient spot liquidity, Mark-to-Market NDFs are a robust solution already widely used in TradFi for pairs like USD/CHF, USD/KRW, USD/INR, USD/BRL, and USD/TWD.

Corporates, banks, and offshore investors typically use them to gain synthetic forex exposure without physically delivering local currency.

The crypto space faces similar structural issues:

- Not all currency pairs have deep spot liquidity

- Maintaining fully collateralized local fiat stablecoins is operationally very difficult

Therefore, Mark-to-Market NDF structures are well-suited for crypto-native forex systems.

Users can:

- Keep their funds entirely in USDT/USDC

- Simultaneously synthetically short the USD and long a foreign currency via a Mark-to-Market NDF structure

- Effectively convert account value and P&L to be denominated in the target currency without leaving the dollar settlement network

Advantages include:

- Oracle-based strong peg: Exposure tracks a reliable forex reference rate, not reliant on fragmented local spot liquidity.

- Retain USD stablecoin networks and yield: Users continue holding USDT/USDC, enabling access to the deepest on-chain liquidity and yield opportunities.

- Superior liquidity and access: USDT/USDC have the strongest global fiat on/off-ramps, exchange integrations, and trading liquidity across the entire crypto market.

- Cross-currency scalability: Any currency with a reliable USD oracle can be synthetically supported, without building local banking infrastructure, local custody, or sovereign bond reserves like traditional fiat stablecoin issuers.

- Capital efficiency: Only forex profit/loss differences need to be settled or collateralized periodically, not full spot conversions.

This perfectly mirrors how today's institutional forex market operates off-chain: layering synthetic exposure and cash-settled risk transfer on top of a dominant dollar funding and collateral system.

On-Chain NDF Forex, Who Will Use It?

Simply having a narrative or believing "forex is obviously the next step" won't work. Details matter, and building a forex stablecoin with TVL reaching ten to twelve figures (i.e., hundreds of millions to hundreds of billions of dollars) is no easy task.

Teams working in this direction cannot expect holders to flock automatically upon product launch. At @SupernovaLabs_, we are extremely clear on three simple questions:

- Who are your holders?

- Why do they hold?

- How do you distribute to them?

1. Digital Banks, Custodians, Wallets: Multi-Currency Accounts Are a Must-Have

Total deposits are one of the most important metrics for digital banks and stablecoin-hosting public chains. Without native forex infrastructure, multinational corporations cannot comfortably hold operational funds on-chain and are forced to move funds back to local banking systems.

Thus, many stablecoin digital banks and public chains risk becoming mere pass-through conduits for funds rather than true financial operating systems.

Mark-to-Market NDF infrastructure changes this.

Stablecoin digital banks, custodians, wallets, and payment platforms can integrate @SupernovaLabs_'s APIs to offer synthetic forex denomination directly on top of the USD stablecoin network. For end-users, the experience becomes a simple toggle:

- Switch an account's denomination from USD to EUR, CHF, SGD, HKD, etc.

- Or hold balances denominated in multiple currencies within one account

- While the underlying settlement, collateral, and liquidity infrastructure remains USDT/USDC

Stablecoin digital banks, custodians, and wallets have highly aligned incentives with Mark-to-Market NDFs:

- Unlock international user acquisition channels

- Increase deposits and retained balances

- Reduce funds flowing back to traditional banking systems

- Support multi-currency accounts for competitive differentiation

Thus, multinational corporations or individual users can:

- Keep funds entirely on-chain

- Maintain access to deep USD stablecoin liquidity and yield

- Simultaneously hold foreign currency exposure economically via synthetic forex markets

This product benefits from a macro tailwind: the US dollar has depreciated about 10-12% against the Euro over the past year, increasing demand for non-USD denomination while users can still keep funds on USD stablecoin rails.

2. Forex Carry Yield: Scale and Stability Far Exceeding Ethena

Forex derivatives are also widely used for carry trades, one of the largest macro strategies globally. The classic example is the Yen carry trade:

- Borrow low-yielding Yen

- Go long high-yielding currencies like the Brazilian Real (BRL)

- Earn the interest rate differential, known as the "carry"

The Brazilian Real often trades in double-digit interest rate territory, making it one of the most favored carry currencies for hedge funds and macro investors. These trades are typically executed via NDFs, forwards, and forex swaps, not spot conversion.

Compared to crypto basis trade products like @ethena:

- Forex carry is linked to sovereign interest rate differentials, not crypto market funding rates

- The market is significantly larger and more institutionalized

- Capacity is much deeper due to the sheer size of the global forex derivatives market

- Yields are typically lower than crypto basis trade peaks but historically more stable and scalable

This creates an excellent opportunity for on-chain forex carry vaults:

- Users deposit USDT/USDC as collateral

- Gain synthetic exposure to foreign currencies via Mark-to-Market NDFs

- Earn sovereign forex carry yield on-chain without leaving USD stablecoin rails

3. Corporate Global Payments: Stripe Has Already Validated This Path

Over the past year, @Stripe has enabled business customers to receive fiat in EUR, MXN, BRL, COP, GBP and automatically convert funds to USDC.

However, forex can only be received, not held, on-chain currently. For businesses managing or accounting in currencies like CHF or SGD, this means they still need to withdraw funds to local banking networks.

This limitation is particularly acute when serving global businesses, which is an area @Stripe is actively driving adoption and expansion.

Stripe offers NDF-style forex hedging support for its fiat global payments. If a merchant wants to settle in currency A and a customer pays in currency B, the merchant can hedge the forex exposure over a defined period and offer the customer a stable, locked, locally denominated price.

Stripe's NDF Forex API for Fiat Payments

Stablecoin payments can apply a similar model on-chain: users continue to hold and transact with USD stablecoins, while merchants or wallets can synthetically hedge to preferred local currency denomination, without relying on spot forex liquidity or local stablecoin issuance.

I want to highlight how astonishing the profit margin for Stripe's forex product is. Despite serving primarily non-speculative, highly predictable corporate and retail payment flows, it charges around 20 basis points per transaction.

Annualized, this translates to roughly a 73% cost for hedging, an extremely high take rate for forex risk transfer.

This not only speaks to the business's profitability but also shows how price-insensitive users are when faced with seamless global payments and exchange rate certainty.

Without Interest Rate Stability, The On-Chain Economy Cannot Function

At @SupernovaLabs_, we are focused on bringing interest rate stability on-chain, pushing DeFi into its next institutional phase, building financial infrastructure at the operating system layer not just for crypto natives, traders, and whales, but for everyday businesses and retail users.

We started with Interest Rate Swaps, settling over $5 billion in notional volume, serving top-tier full-stack prime brokers and institutional borrowers.

NDF forex is an area we are deeply excited about because we strongly believe it will unlock the next phase of on-chain financial transaction volume and global stablecoin adoption.

Just as centralized exchanges shaped the current stablecoin landscape, digital banks will create new waves and push adoption to the multi-trillion dollar level.

Five years from now, today's roughly $3.5 trillion stablecoin market might seem insignificant compared to the multi-trillion dollar scale possible with stablecoin digital banking and global on-chain financial accounts.

Forex will be a central part of this expansion, and our goal is to build the infrastructure layer that fully captures this growth.