This month in South Korea, if you are neither an SK Hynix employee nor hold SK Hynix stock, you are most likely 'having a tough time.'

As soon as the massive Q1 profits were announced, investment banks—never shy about fanning the flames—not only actively revised up their profit forecasts for Hynix this year but also raised the bonus expectations of Hynix employees. Leveraging the company's principle of allocating 10% of annual operating profit as a bonus pool, they calculated year-end bonuses amounting to millions of RMB per capita. In doing so, they conveniently placed the capitalists at rival Samsung in a rather unflattering and awkward position.

Since then, anything even remotely associated with Hynix's IP has been met with frenzied追捧.

Hynix work uniforms have become a priority pass in the Korean相亲market; real estate agents in Icheon City, where its headquarters is located, experienced a dream-like quarter, with housing prices and transaction volumes rising in multiple areas along the Hynix commuter bus routes; even the tangentially related China-South Korea semiconductor ETFs were driven to premium rates of around 30%, frequently triggering temporary trading halts.

Even the Hong Kong stock market, long criticized for lacking tech substance, managed to perk up.

As of May 13, 2026, the Hong Kong-listed CSOP SK Hynix Daily 2x Leveraged ETF (07709.HK) (hereinafter referred to as the 2x Long Hynix ETF) saw its asset规模approach HK$60 billion, surpassing the long-time leader in the US market, the 2x Long Tesla ETF (TSLL.NASDAQ), to become the world's largest single-stock leveraged derivative product by size.

No matter how niche an investment product is, when the market rallies to this extent, anyone surfing the web—even if just following tech and digital influencers—can't help but occasionally encounter enthusiastic netizens' in-your-face question in the comments section: 'Why didn't you buy 2x Long SK Hynix?'

The Fatal Leverage

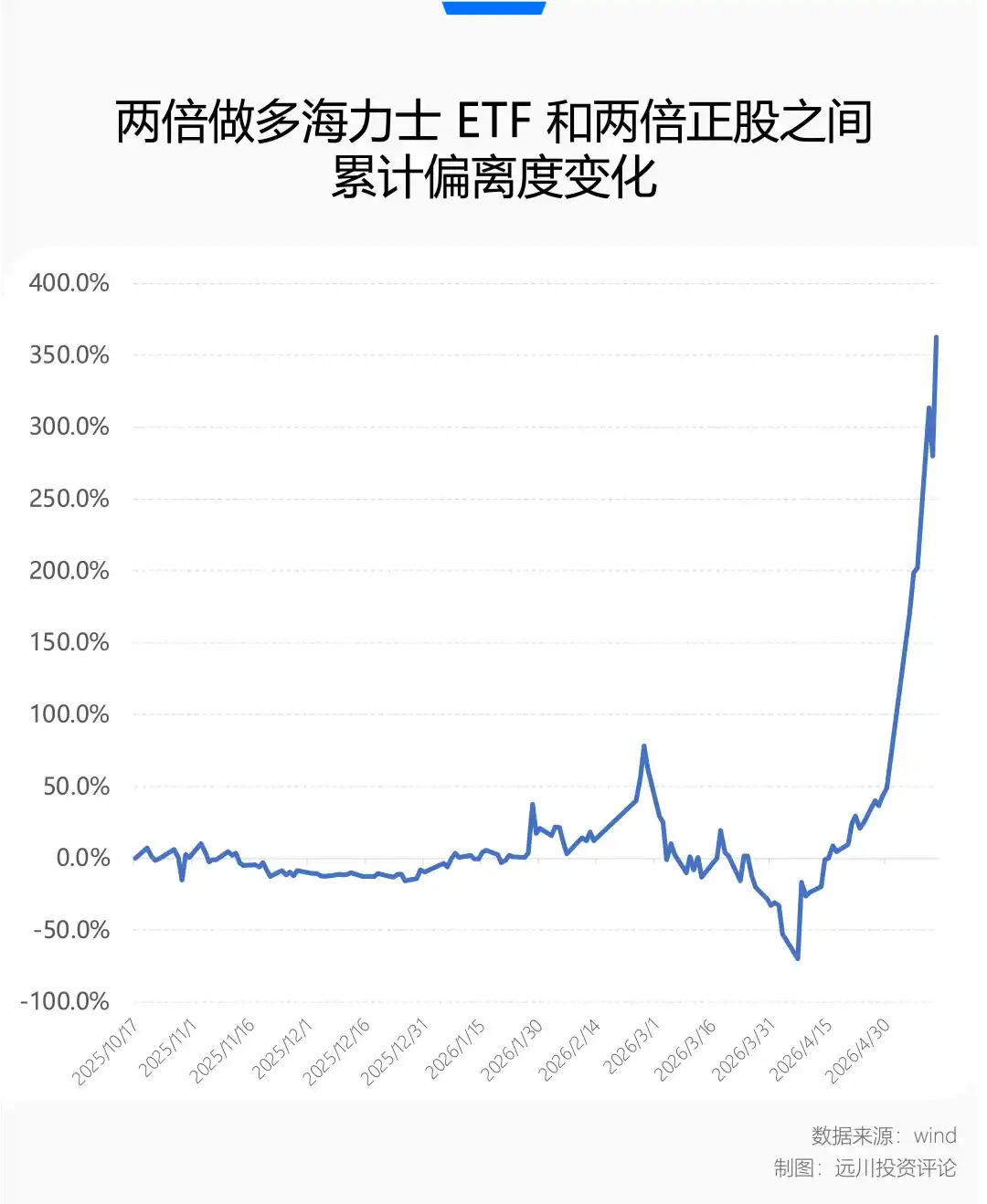

When the 2x Long Hynix ETF was first listed on the Hong Kong Exchange on October 16, 2025, its issuance size was less than HK$5 billion. Calculating based on the closing price on May 13, 2026, over these 7 months, this leveraged ETF's net asset value has surged by 1011.58%, while its规模ballooned more than 13-fold.

云迹科技, which debuted on the same day in Hong Kong as the so-called 'first hotel robot stock' and has seen its股价rise steeply, only achieved a market cap less than 4 times its IPO valuation.

If you think this demonstrates the terrifying efficiency of 2x leverage, consider that SK Hynix's underlying stock in the Korean market gained 'only' 324.49% cumulatively from October 17 last year to May 13 this year. Bolstered by a sustained upward rally, this leveraged ETF even generated an excess return of 362% beyond its theoretical 2倍收益. Faced with such a暴力撒币spectacle, labeling it a 'triple leverage' product seems more appropriate.

However, zooming out over the past 7 months, this paper-thin excess is temporary.

Just two months ago, the Strait of Hormuz陷入薛定谔的封锁, and global markets panicked amidst an abrupt oil and gas supply disruption. In the seesawing and rapidly shifting situation, the market did not experience a traditional one-sided decline. Instead, it became schizophrenic in this atypical geopolitical conflict.

During the day, it might trade on the避险logic of 'World War III erupting, supply chains breaking,' only to swiftly switch to the 'de-escalation, return to the tech主线' FOMO狂欢 at night based on ambiguous statements from the White House spokesperson. This模糊性and uncertainty in the evolution path were amplified by the rapid spread on social media, translating into wild sell-offs targeting tech stocks or frantic bottom-fishing on every dip. The传导was extreme.

While common sense tells us wars eventually end, and daily AI industry token consumption keeps accelerating, when market volatility becomes too intense, the曲折过程cannot be entirely ignored.

It was during this period that more people felt the波动损耗inherent in this leveraged ETF product.

Looking at actual trading data from March to April 2026, Hynix's stock price declined amidst剧烈震荡. A decline is problematic in itself, but the multiple violent rebounds exceeding 10% during the period were the real salt in the wound.

For the 2x Long Hynix ETF, which rebalances its leverage daily, a one-sided decline might be somewhat tolerable; a high-volatility,震荡下行trend is the real meat grinder. During the most agonizing phase, it跌超过50% more than twice the underlying stock's decline.

In theory, without considering other transaction fees and management expenses, the product's daily rebalancing mechanism means that in a one-sided bull market, yesterday's profits automatically become today's 'principal,' on which an additional 2x leverage is applied, generating magnified超额正收益. Conversely, in a one-sided暴跌, because the daily calculation基数shrinks, its actual losses would be less than the theoretical 2x.

However, once it enters a '涨跌交替' volatile, range-bound market, the leveraged ETF reveals its狰狞的一面.

The 2x Long Hynix ETF repeatedly experienced '多空双杀'—after a big gain yesterday and rebalancing, a drop today would inflict heavier losses; then, after rebalancing again, another rebound tomorrow would incur losses once more due to the reduced基数.

The反复摩擦from alternating gains and losses causes the product's actual net value drawdown to far exceed twice the decline of the underlying stock, creating significant negative波动损耗that erodes investors'本金.

However, now the market has returned to the AI主线,狂热资金is once again rallying and pouring in, bringing about one-sided暴涨and皆大欢喜.

As Hynix's market cap repeatedly hits new highs, and as this hundred-billion-scale leveraged ETF product ignites狂热交投, the market inevitably returns to that age-old question: In this round of industrial revolution, do cycles truly not exist?

The Silicon-Based Cyclical Stock

One must admit that, judging by its listing timing, the 2x Long Hynix ETF was practically叠加满了with the加持of 'destiny, luck, and风水.'

For a considerable period before, memory was not the absolute focal point for going long on the AI主线in secondary markets. After all, since humanity boarded the information age express in the 90s, memory has often been the sector littered with casualties after periods of烈火烹油, where the terror of cycles far outweighs the梦幻of growth.

Memory chips (especially traditional DRAM and NAND) are highly standardized大宗商品. The memory sticks produced by different manufacturers, aside from the brand贴纸, have almost no differences in physical performance, akin to silicon-based猪肉股. The entire industry has long been trapped in a brutal cyclical loop:

Shortage → Price surge → Giants疯狂扩产→产能过剩→价格雪崩→ Losses & production cuts → Shortage again.

Each upcycle is冠以'super cycle' under超级乐观expectations. Each downcycle is marked by惨烈price wars and billions in losses, leaving累累尸骨.

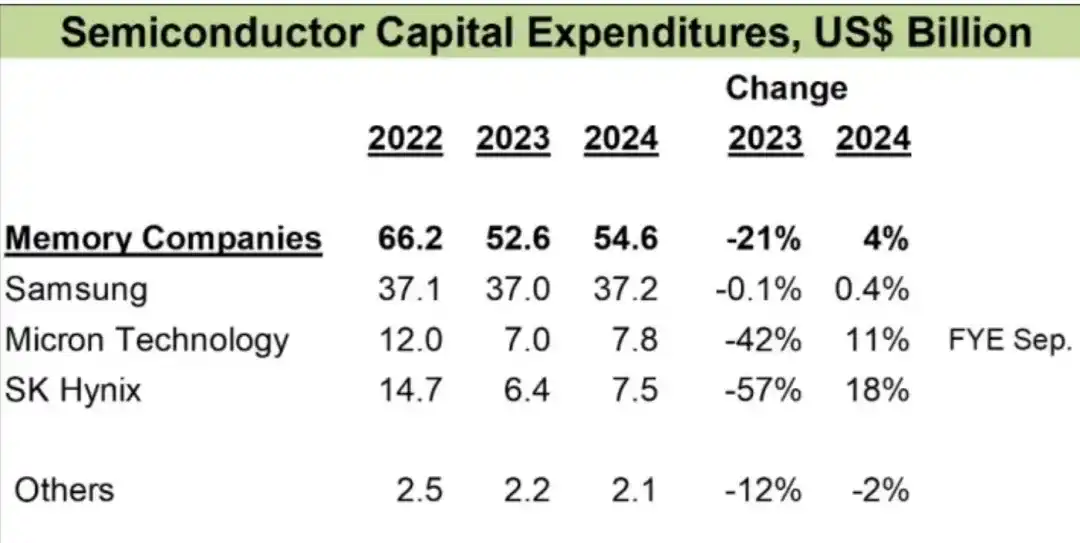

After enduring the半导体寒冬of 2022-2023, the surviving memory triumvirate—Micron, Samsung, Hynix—tacitly cut capital expenditures, abandoning the strategy of恶意扩产that hurts the enemy a thousand while自损八百.

Image Source: IC Insights

Then the AI narrative arrived, replaying the shortage-and-price-hike script, essentially installing money-printing machines for everyone.

Especially starting from the second half of last year, as the competitive focus in the AI industry端shifted from 'training' to 'inference,' demand重心for infrastructure shifted from 'computing power' to 'storage power,' and supply bottlenecks moved from bandwidth to capacity, widespread memory shortages became the hottest trading narrative.

At this point, anyone still mentioning 'wasn't the end of AI supposed to be electricity?' is most likely someone who missed the rally.

Post-Q3 2025, AI industry news was almost exclusively about memory chip shortages—sometimes reports that巨头们had HBM orders booked through 2027 and beyond; other times notifications to clients that DDR5 was also in short supply, apologizing that now, whether高端or低端, it's about across-the-board price hikes.

Hynix, as NVIDIA's primary supplier for HBM, captured极高的先发优势and market share. The timely上市of the 2x Long Hynix ETF practically coincided perfectly with the golden days when memory sticks' price per gram surpassed黄金and one box could trade for an apartment in Shanghai.

So, does hopping on the AI express allow escape from周期引力? The important thing isn't to draw a conclusion now, but to identify where changes might occur.

Hynix has established a dominant,一家独大position behind the yield壁垒of HBM. In Q1 2026, SK Hynix's quarterly毛利率reached a historical peak of around 79%, even surpassing NVIDIA's profitability during the same period.

Human nature tells us that极致超额利润will inevitably attract蜂拥而上的产能扩张欲. The tacit understanding seemingly reached among memory giants through 'production cuts' is untrustworthy in the face of absolute暴利.

Therefore, whether Samsung or Micron's yields will breakthrough at some future point, potentially discounting the scarcity narrative of HBM and increasing分歧between bulls and bears leading to sector震荡, is a variable requiring持续跟踪.

Beyond changes on the supply side,争议on the demand side hasn't completely烟消云散just because of accelerating Agent adoption and increasing token consumption.

Ultimately, Hynix's疯狂is built upon NVIDIA's疯狂; and NVIDIA's疯狂is built upon downstream tech giants'每年上千亿美金的 AI capital expenditures.

Capex边际变化remains the greatest引力in secondary markets for all AI-related anxiety and pride.

Epilogue

Whether you buy the 2x Long Hynix ETF or not, it will become a微妙注脚when we look back on this era in the future.

In this era, bulls and bears are often talking about two different things: bulls on AI industry信仰, bears on macro地缘担忧.

People habitually翻开历史书, trying to find parallels in the internet狂飙of the millennium or earlier macro upheavals. But each round of technological revolution unfolds differently. This time, the '不一样' lies in: the颠覆速度of this industrial revolution is史无前例.

AI is reshaping global productivity and生产关系的at an unprecedented acceleration. This extreme '快' has broken the漫长的渗透与发酵过程of traditional tech cycles. It doesn't give the market much time to slowly digest valuations, nor does it offer much轮动机会for 'old-school stocks' to get a bit of眷顾from泛滥的流动性.

Whether industry giants or secondary market capital, all are forced to complete their站队与定价within an extremely short time window. Hence, stock price gains are measured in multiples; hence, seasoned AI practitioners have already默认that in this era, six months counts as a长期.

However, the storm over the Strait of Hormuz once again placed this round of tech revolution under the commonality shared by all past tech cycles: industry determines the终局and收益率, while macro influences the路径and波动率. What caused the巨大负向偏离in the 2x Long Hynix ETF was not an中断in the AI进程, but the极度摇摆of global macro expectations during that one-plus month.

And the软肋of the real world isn't confined to just that 33-kilometer narrowest point of the Strait of Hormuz.