Author: Jim, MSX Matong

During this round of US stock 13F disclosures, one of the most watched funds was not Bridgewater or Berkshire Hathaway, but a fund with a very distinctive name—Situational Awareness LP.

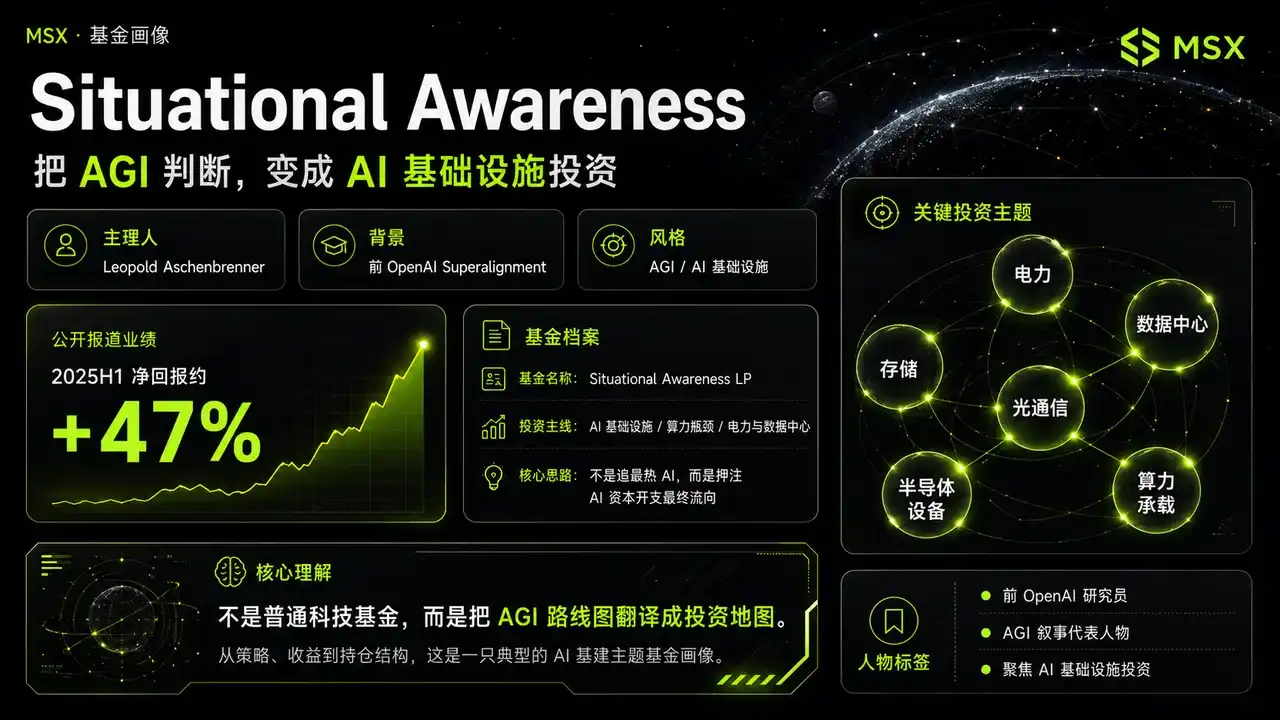

Its manager, Leopold Aschenbrenner, is not a traditional Wall Street veteran. He was a former member of OpenAI's Superalignment team. In 2024, he published a lengthy essay titled "Situational Awareness: The Decade Ahead". Its core thesis was very radical, stating that AGI might arrive sooner than most people think, and that what will be truly scarce in the future is not just the model capabilities themselves, but compute power, electricity, data centers, chips, storage, and the national-level resource competition surrounding the AI arms race.

Two years later, the facts have proven him right.

Leopold internalized a set of judgments about AGI in the coming decade and then mapped those judgments to the capital markets. Precisely because of this, Situational Awareness, from its inception, has not resembled a typical tech fund, but rather has been like directly translating the AGI roadmap into an AI infrastructure investment map.

This is also why its every move is closely watched in the AI investment space. The latest 13F filing shows that this most knowledgeable AI bull seems to be quietly building a large-scale position in put options.

I. SALP: A Product That Turns AGI Belief into a Fund

Public information shows that Leopold founded an investment company focused on AGI, backed by heavyweight Silicon Valley figures such as Patrick Collison, John Collison, Nat Friedman, and Daniel Gross.

According to market reports, Situational Awareness achieved approximately +47% net returns after fees in the first half of 2025, significantly outperforming the S&P 500 and the tech hedge fund index during the same period. Its uniqueness lies in the fact that it is not simply bullish on "tech stocks," but highly focused on AI infrastructure, betting on where AI capital expenditures will ultimately flow.

As stated at the beginning, his underlying logic is: if AGI truly arrives faster, the first to be revalued might not necessarily be application-layer companies, but rather those controlling compute power, electricity, data centers, storage, optical communications, semiconductor equipment, and energy resources. Therefore, its high returns are not simply from buying the index, but from a basket of high-beta AI infrastructure stocks widening the gap: such as Bloom Energy, Sandisk, Lumentum, CoreWeave, Core Scientific, etc.

It's necessary to explain first what 13F is.

13F is a quarterly holdings disclosure filing that US institutional investment managers submit to the SEC, typically used to observe the quarterly holdings changes of large funds in US stocks, ETFs, and related options. However, it is essentially just a snapshot at the end of a quarter, telling the market only "what was disclosed at a certain point in time." It cannot fully reconstruct a fund's entire trading strategy, especially regarding options. 13F does not show strike prices, expiration dates, whether positions are paired with others, and cannot directly deduce the fund's true net exposure.

This is also the part most prone to misinterpretation when reading such filings.

The reporting date for this Q1 13F was March 31. Last10K shows the file was submitted on the evening of May 15 (ET), but the SEC acceptance time was May 18. That is to say, it wasn't simply "not filed," but there was a time lag between submission and the market actually seeing the disclosed results. Hence, discussions like "waiting for Leopold's 13F" appeared on social media.

More critically, the disclosed results of this 13F are not entirely as the market imagined. Many initially thought Leopold would continue aggressively adding to core AI assets like NVIDIA, Broadcom, AMD, TSMC, and ASML. But the reality is, SALP established large new PUT option positions covering a batch of AI and semiconductor core holdings, including the SMH semiconductor ETF, NVIDIA, Oracle, Broadcom, AMD, Micron, TSMC, ASML, Intel, and others.

This has prompted the market to reconsider a question: Why is the person who most believes in the accelerated arrival of AGI starting to buy insurance for AI leaders?

If simply chalked up to "being bearish on AI," that's too simplistic. What truly deserves analysis is under what macro backdrop he made this move, and what changes in AI trade structure this reflects.

II. Understanding SALP's Latest 13F: From Betting on AI to Managing AI Volatility

The most striking action revealed in this 13F is undoubtedly SALP's establishment of large put option positions:

- The largest is a PUT on the SMH semiconductor ETF, with a disclosed value of approximately $2.043 billion;

- Next is an NVDA PUT, about $1.568 billion;

- Then an ORCL PUT, about $1.073 billion;

- An AVGO PUT, about $1.006 billion;

- And an AMD PUT, about $969 million;

- In addition, it also established new MU PUT, TSM PUT, ASML PUT, INTC PUT positions, among others;

On the surface, this looks a lot like being bearish on AI leaders. But the issue is, PUTs do not necessarily represent outright shorting — after all, the option amounts in 13F are more of a nominal value disclosed based on the underlying security size, not equal to the fund's actual premium cost. More importantly, 13F doesn't show strike prices, expiration dates, whether positions are paired, or the true net exposure within the portfolio.

Therefore, directly stating Leopold is "completely bearish on NVIDIA and semiconductors" is not rigorous. A more reasonable understanding is that he is buying "insurance" for his AI infrastructure long portfolio. Because many of the holdings in SALP's original portfolio are themselves high-beta, high-volatility, rate-sensitive companies, like the aforementioned Bloom Energy, CoreWeave, Core Scientific, IREN, Applied Digital, Sandisk, etc. The long-term thesis for these assets is related to AI infrastructure, but short-term stock prices often heavily depend on risk appetite and the valuation environment.

Once the market starts de-risking due to rising oil prices, recurring inflation, higher interest rates, or geopolitical conflicts, these high-beta assets are often sold first. This also relates to the macro backdrop around late March: on one hand, Middle East tensions and US-Iran conflict risks were pushing up oil price expectations; on the other hand, rising oil prices could exacerbate inflation stickiness, weakening market confidence in rate cuts.

For high-valuation growth stocks, this equals "double pressure": oil prices push inflation, inflation suppresses rate cuts, rates don't come down, and the valuation of high-duration tech assets gets compressed.

Placed within this context, Leopold's establishment of numerous PUT positions becomes easier to understand. It's not about rejecting AI, but about acknowledging that no matter how strong the long-term AI logic is, it cannot completely ignore macro headwinds.

Especially for a fund like SALP, many holdings in its portfolio are high-beta assets. If it only held offensive positions, once a systemic market pullback occurred, portfolio NAV volatility would be very high. By buying PUTs on liquidity-rich, representative AI core assets like SMH, NVDA, AVGO, AMD, ORCL, it can use relatively standardized instruments to hedge systemic pullback risks for the entire AI trade.

The true meaning behind this is that Leopold has not changed from an AI bull to an AI bear, but has shifted from "unilaterally aggressively long AI" to "continuing to bet on AI infrastructure, but starting to manage the path volatility."

This is a more mature portfolio management approach.

III. So, Where is Leopold's Offensive Direction?

If establishing PUTs solves the "defense problem," then the list of additions, reductions, and liquidations truly tells us where Leopold's offensive direction lies.

From the disclosures, SALP still retains and has added to a batch of AI infrastructure-related stocks. For example, it slightly added to its common stock position in Sandisk; common stock in CoreWeave, IREN, Applied Digital, Riot Platforms, CleanSpark, Bitfarms, Bitdeer are also on the addition list. Currently retained important long positions also include Bloom Energy, Sandisk, CoreWeave, IREN, Core Scientific, Applied Digital, etc.

This indicates it has not abandoned AI. On the contrary, it is still betting on the same long-term logic: AI capital expenditures will continue to flow downstream, and the true beneficiaries are those companies controlling electricity, data centers, storage, compute hosting, and infrastructure bottlenecks.

This is very close to MSX's Q2 thematic judgment. In "AI Infrastructure Rallied Throughout Q1; in Q2, Who Can Still Justify the 'High Valuation'?" we emphasized that the focus of AI trading has shifted from just GPUs to networks, storage, and power. The market is now more concerned about whose orders, revenues, and profits the continuously expanding capital expenditures of major firms will ultimately flow into. The reason why segments like equipment, networks, storage, and power are more advantageous is not because they are sexier, but because they better fit the current market's taste for earnings realization.

From this perspective, SALP's long positions are quite representative: Bloom Energy corresponds to power and independent energy supply; CoreWeave, Applied Digital, Core Scientific, IREN correspond to data centers, compute hosting, and infrastructure capacity; Sandisk, Micron, TSM-related positions correspond to storage, semiconductor manufacturing, and hardware supply.

In other words, Leopold is not avoiding buying AI; he is more concerned about where the AI money ultimately goes and who can turn that money into revenue on their financial statements.

Looking at reductions and liquidations, they are equally informative. SALP liquidated INTC CALL, Lumentum, Cipher Mining, and reduced positions in CoreWeave CALL, Bloom Energy, Core Scientific, among others. Notably, this is not simply an exit from a certain direction, but a reduction of some positions that have already rallied significantly, are highly volatile, or have stronger leverage attributes.

For example, with CoreWeave, it reduced CALLs but still holds common stock, indicating it's not abandoning CoreWeave entirely, but switching from a more aggressive option expression to a relatively more controlled common stock expression. Similarly, reductions in Bloom Energy and Core Scientific don't equate to thesis invalidation, but are more likely portfolio-level risk control and profit-taking.

The liquidation of Lumentum is even more intriguing. In MSX's Q1 review, AI hardware and optical communications were among the strongest-performing themes, with AXTI, AAOI, LITE, and LWLG achieving multi-fold gains. The strength of optical communications essentially stemmed from the explosion in demand for optical interconnect, optical modules, and network links from AI data centers. However, the issue is, the more a theme rallies in Q1, the more likely it faces crowded trades and diminishing risk-reward in Q2.

Therefore, Leopold's liquidation of LITE and reduction of some high-beta AI infrastructure positions may not necessarily represent a bearish view on the direction, but a more realistic acknowledgment: The most successful trade in Q1 may not be the trade with the best risk-reward in Q2.

This is the most important takeaway from this rebalancing. It's not about rejecting AI, but actively switching structure—from buying anything in the AI chain to retaining only those assets that can better absorb long-term capital expenditures, possess stronger infrastructure attributes, and are more resilient through macro volatility.

He's not giving up on AI; he's giving up on the linear fantasy that "all AI will rise together."

This 13F is essentially only a snapshot as of March 31 and does not represent the exact same positions Leopold still held by May. Yet, it still offers strong inspiration for the current market.

First, the long-term AI theme is not over, but the trade structure has changed. In the future, not everything AI will rise; the premium will go to those who can deliver, while crowded trades will require hedging.

Second, in a high-oil-price, high-interest-rate, high-volatility environment, the truly effective strategy is not simple all-out offense nor comprehensive defense, but playing offense with defense in place—core positions betting on certainty, marginal positions betting on upside, while using hedging tools to control portfolio drawdowns. Leopold's move essentially demonstrates this logic with real positions.

Third, this also confirms a major change in US stocks in 2026: index Beta weakens, while structural Alpha strengthens. In the past, simply buying the "Magnificent Seven" or NVIDIA might have been enough to win. But now the market is more discerning; it questions every company: Can your AI story ultimately turn into orders? Into revenue? Into profits? If not, valuations will compress no matter how high.

This is also why AI Infrastructure 2.0 becomes important. Future capital won't just look at GPUs, but will search down the chain of compute → interconnect → storage → power → data center infrastructure for segments that can truly deliver.

In Conclusion

If viewed superficially, the most eye-catching part of this 13F is that string of massive PUTs.

But if you truly go through the entire portfolio, you'll find that what Leopold did is not a "turn from AI bull to bear," but a more mature upgrade: long-term still betting on AI infrastructure, short-term starting to face the volatility risks of high-valuation, high-beta assets.

This is the most important takeaway from this 13F. It tells us that the direction of AI might still be right, but the path to that destination will certainly not be a straight line.

For true fund managers, what's important is not just betting on the correct end point, but also surviving and navigating the volatility along the way.

For ordinary investors, the biggest takeaway from this 13F is also clear: the AI trade in 2026 has shifted from "buying the story" to "buying the delivery"; from "buying the leaders" to "finding the bottlenecks"; from "unilateral offense" to "playing offense with defense."

This is the most interesting, and absolutely should not be ignored, signal.