For most Bitcoin OGs in the space, the main crypto investment strategy has always been ‘HODL,’ which has been enough to outperform most assets in certain periods.

Early asset managers who entered the sector also adopted a similar passive strategy for their respective crypto ETFs (exchange-traded funds). They have been holding the crypto assets in the hope that, in three, six, or 12 months, their value would appreciate.

According to 21Shares president Duncan Moir, however, crypto ETFs are transitioning from passive management to active strategies. Moir noted that the sector was a ‘nascent’ and ‘growing asset class’ that fits perfectly with active management.

At the core of this new strategy is scaling yield streams and extra earning opportunities beyond just holding the crypto assets. From a regional crypto ETF demand, Moir said,

The interest is still concentrated in the larger coins in the US. In Europe, institutional clients are more interested in newer assets and the application layer beyond the Layer-1.

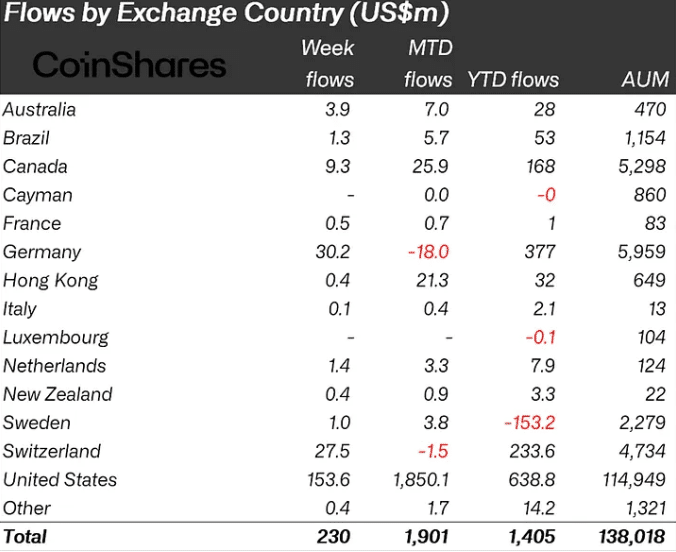

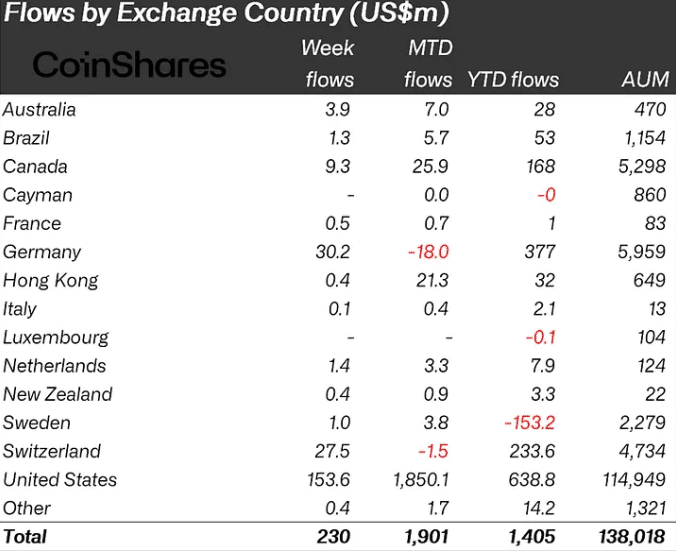

In fact, on a year-to-date (YTD) basis, the U.S. leads with $638 million in crypto inflows, followed closely by Germany at $377 million and Switzerland at $233 million.

Crypto ETFs evolution and diversification

For Moir, the mature investor base in Europe, who already hold Bitcoin and Ethereum, is looking to expand their crypto allocation with better offerings.

This led to 21Shares launching an ETP tied to Strategy’s preferred stock, Stretch (STRC), which offers an annual dividend yield of up to 11.5% payable monthly. This is one of the Strategy’s ways of raising capital for Bitcoin buys.

Moir noted that the product has been an instant success across several regions, underscoring a strong appetite for yield-bearing assets that are feasibly accessible via traditional platforms.

Additionally, crypto ETF staking rewards have become another active strategy to maximize investors’ returns.

Grayscale and BlackRock’s push for staking rewards in their respective Spot ETH ETFs is one example of asset managers seeking more opportunities for investors.

Finally, Moir said they also look for major thematic trends or future shifts that can be maximized. The approach informed the launch of 21Shares’ Bitcoin-and-gold ETP, based on the rising demand for safe havens amid debasement trade and rising U.S. fiscal debt.

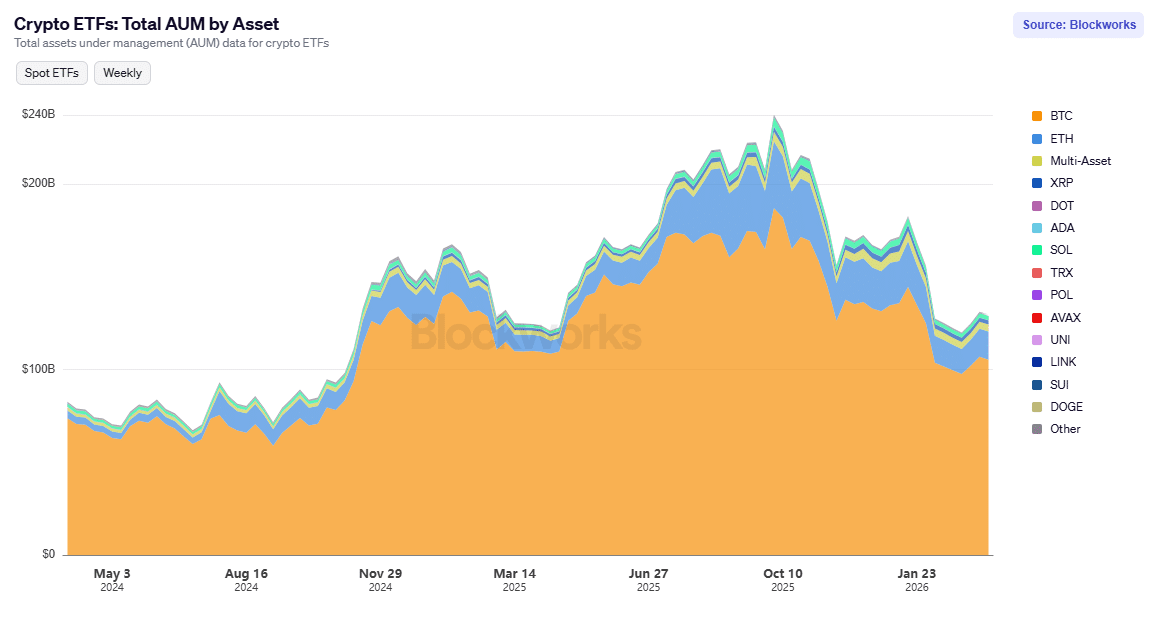

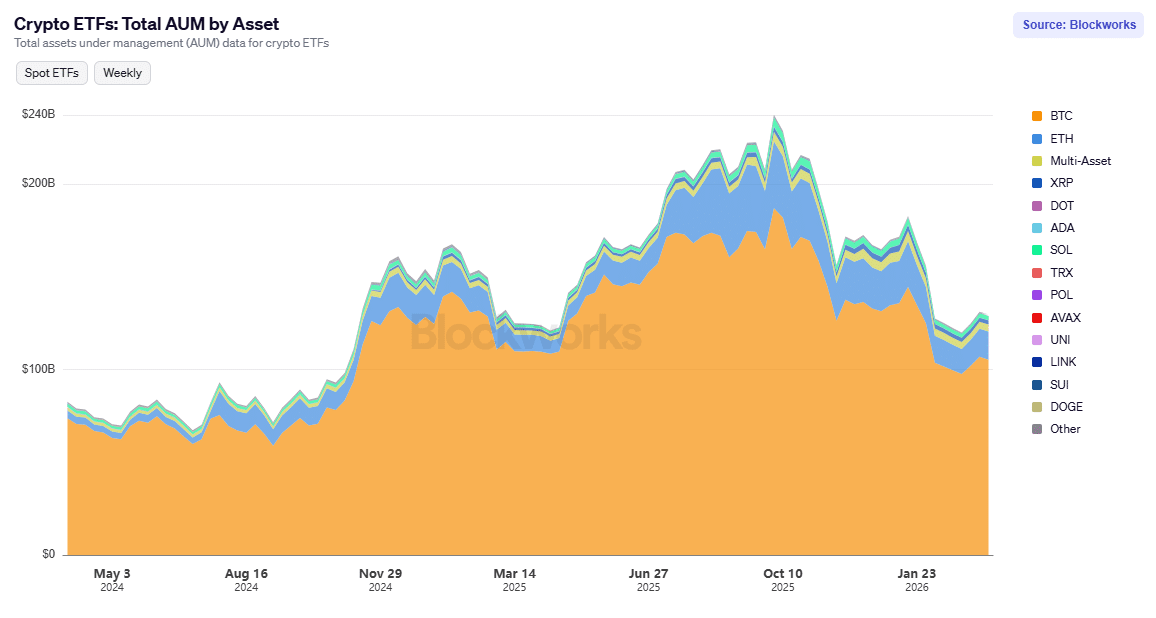

It remains to be seen how the new active strategy will drive demand into crypto ETFs. As of writing, the total crypto ETF assets under management (AUM) were about $130 billion, down from nearly $240 billion at the peak of 2025.

Final Summary

- 21Shares’ Duncan Moir said that active strategies will be at the center of the next crypto ETF management.

- Yield-focused wrappers and staking rewards are some active strategies asset managers are deploying for investors.