Original | Odaily Planet Daily (@OdailyChina)

Author | Golem (@web3_golem)

This week, I wrote an article reviewing the absurd event contracts on Polymarket, pointing out that betting on some seemingly outrageous contracts at this time would be profitable.

This made me wonder: who is going against "common sense" to provide "free money" for the market?

Bets that oppose our smart choices aren't completely without a chance of happening; there are certainly some people who firmly believe in their judgments (for example, some still believe the Earth is flat). But prediction markets aren't a "greater fool market." I believe that when players use real money to predict whether an event will occur, they will do their best to think as a "rational person," meaning their decisions are the most economical and profitable. Therefore, from this perspective, those users betting "Yes" on seemingly impossible event contracts must also have some kind of profit strategy; they aren't fools providing us with "high-certainty" financial opportunities for free.

After thinking and discussing, I believe that those providing counterparty liquidity in these absurd event markets likely fall into the following three categories (this article is meant to spark discussion, welcome feedback and corrections, X@web3_golem):

Lottery Players

The logic of lottery players is simple: they focus only on the odds, aiming for a small stake to win big.

Sometimes, real life is far more surreal than we imagine; even events that seem outrageous can happen. Moreover, although prediction markets settle based on the real world, settlement results can sometimes be distorted due to settlement conditions, system failures, and other factors. Polymarket has had instances where settlement results did not match reality due to issues with UMA's dispute resolution mechanism. A recent example is Polymarket ruling that the US military action in Venezuela did not constitute an "invasion."

Therefore, long-tail odds偏差 (bias) appear. Even for events with a very small probability of occurring, the Yes side still has a price of 1%-3%. As long as the odds are high enough, "lottery players" will buy, becoming one of the firm bottom buy supports.

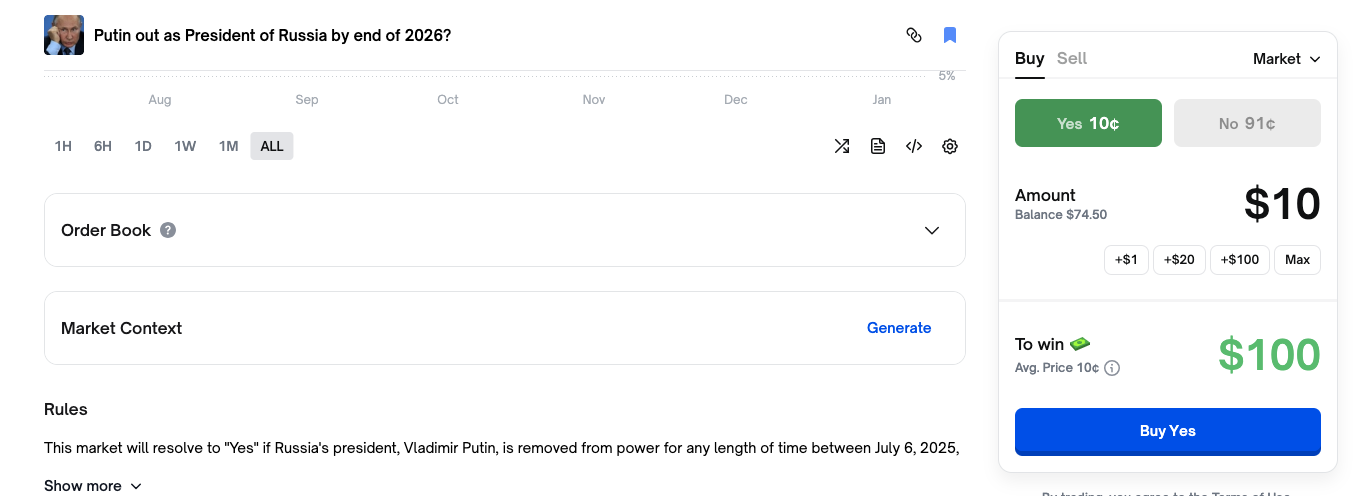

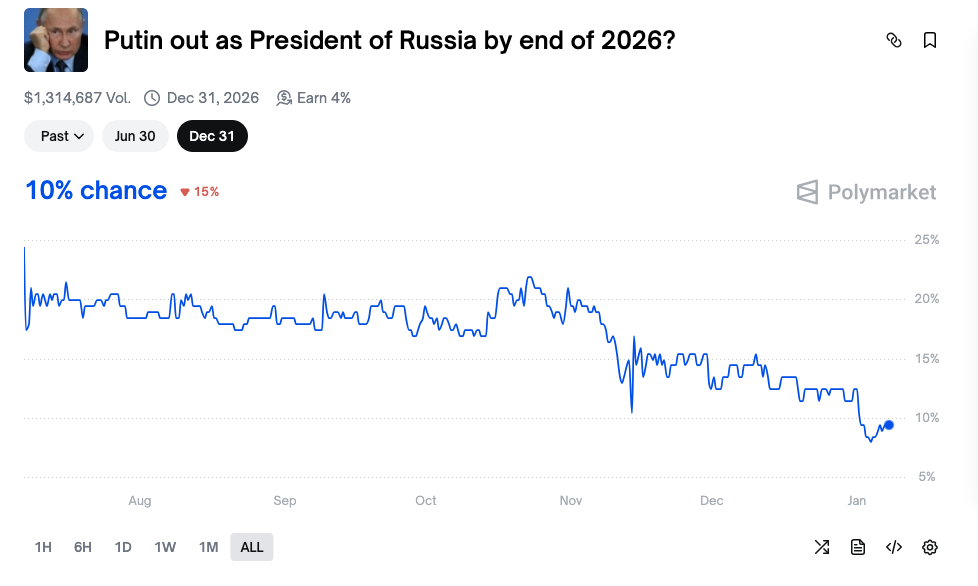

But actually, this psychology of "lottery players" is also rational. For example, in the event contract "Will Putin step down before the end of 2026?", driven by common sense, most people will buy "No," and the probability already shows people's attitude. But the Yes side still has a 10% probability, meaning if you bet $10, you could get $100 back if Putin really steps down before the end of 2026—a 10x return. So, why not gamble?

Furthermore, lottery players don't necessarily place heavy bets on a single market. Since prediction markets are不缺 (not short of) such high-odds events, by casting a wide net and hitting the jackpot a few times, there's still a chance to recoup costs and even profit.

They anticipate black swan events more than normal people. Therefore, they are happy to provide buy-side liquidity on the Yes side of "counterintuitive" markets (In some markets, Polymarket provides placing rewards and holding rewards, but this is not the main factor driving lottery players).

Bots

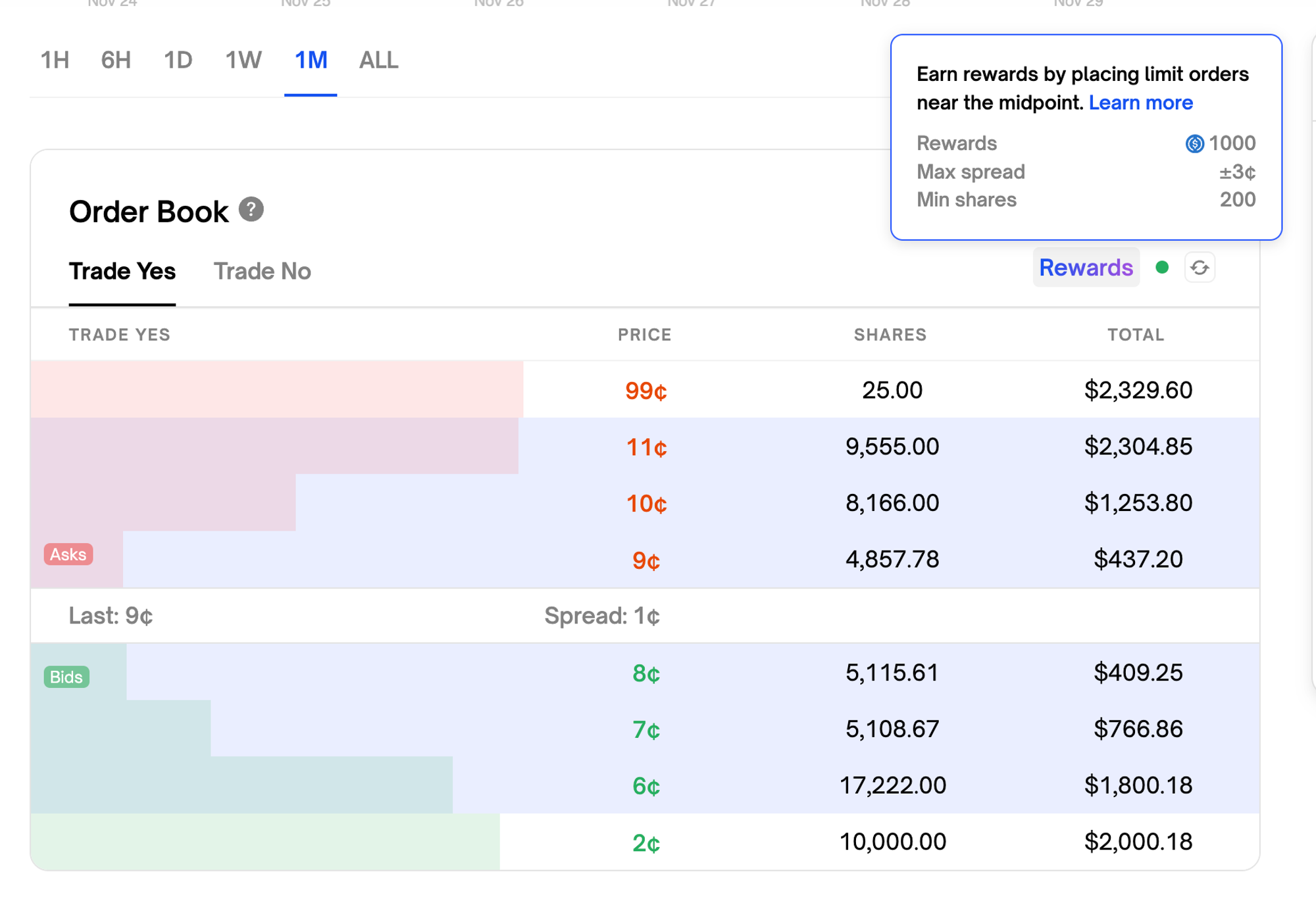

If an event contract itself has strong certainty, the intervention of players sweeping the尾盘 (end-of-market) will push the probability on one side to 99%-100% before settlement. The existence of "lottery players" can partially explain why these "counterintuitive" markets still have players taking the Yes sell orders (Odaily Note: Because Polymarket uses a shared order book, meaning when the No side has a buy order for 1 share at $0.99, the Yes side will correspondingly have a sell order for 1 share at $0.01), but they are always a minority group and cannot explain why these markets still have large trading volumes and good depth.

So, who else is injecting large amounts of liquidity into these markets? The answer is bots.

Market-making bots on Polymarket have developed very rapidly. Bots that trade automatically through the Polymarket API actively monitor all newly created markets and are often among the first participants. These bots can profit by actively trading in these markets.

In these "counterintuitive" markets, when the No side price is $0.99, due to the shared order book, the Yes side will have sell orders listed at $0.01. Market-making bots, like "lottery players," will also eat these $0.01 sell orders. But immediately after, they will list sell orders on the Yes side at $0.02, $0.03, or even higher, waiting for "lottery players" or other bots to成交 (execute the trade). The No side will also see buy orders at $0.98, $0.97, or even lower (Odaily Note: again due to the shared order book). Thus, the order book gains significant depth.

However, after communicating with the crypto VC Jsquare team (they invested in prediction market aggregator Rocket), they believe there aren't many bots executing this strategy on the market. In these "counterintuitive" markets, the speculative psychology of "lottery players" or regular players is enough to support most of the opposing orders.

The existence of some wash trading bots also provides market liquidity and trading volume for these "counterintuitive" and somewhat niche markets (compared to events like the US election). A wash trading bot places a buy order on the Yes side at $0.02, and another wash trading bot places a buy order on the No side at $0.98 to execute the trade.

This behavior is mainly to qualify for future prediction market airdrops. In high-frequency markets, orders might be matched by other players, so these "counterintuitive" event contracts are the ideal tools for wash trading.

Prediction Platforms

In addition to the above "lottery players" and bots, the prediction platforms themselves also contribute greatly to the liquidity of these markets.

Polymarket's mechanism includes two liquidity incentives: placing rewards and holding rewards. Placing rewards mean that in some specific markets, players can get rewards simply by placing orders within the maximum stipulated spread. Holding rewards mean that in some specific markets, players holding shares, whether Yes or No, can receive a 4% annualized holding reward.

The highlighted part indicates the maximum spread range for placing rewards

According to statistics, Polymarket has invested about $10 million in market maker incentives, paying over $50,000 daily at its peak to maintain order book liquidity. These incentives have now decreased to just $0.025 per $100 traded.

These investments have indeed been effective, driving trading in many "counterintuitive" markets. For example, the event contract "Will Putin step down before the end of 2026?" has already seen over $1.3 million in trading volume. Holding shares in this contract yields a 4% annualized return. For players holding Yes shares, this equates to an ultimate annualized return of 14% (10% tail-end收益 (profit) + 4% platform reward), which is hugely attractive. For players holding No shares, the placing rewards and holding rewards also hedge some of the risk.

There is also speculation that, in addition to openly providing liquidity incentives, prediction markets themselves act as market makers, providing liquidity for these "counterintuitive" and niche markets to achieve advertising and marketing effects. But this is pure speculation, open for discussion.