Original Title: What happened to Ethereum?

Original Author: @paramonoww

Original Compilation: Peggy, BlockBeats

Editor's Note: Recently, Vitalik Buterin published a long article pointing out that as Ethereum L1 scaling capabilities have significantly improved and the progression of L2 towards 'Stage 2' has long lagged, the past vision of treating L2 as 'Ethereum-branded shards' is no longer tenable. He emphasized that L1 is accelerating its return to the core focus of scaling, no longer needing L2 as a 'crutch' for performance expansion.

This rewriting of L2's positioning has sparked widespread discussion in the community. Beyond price, this article shifts the focus back to Ethereum itself: from the fading of the 'ultrasound money' narrative, the repeated wavering of the Rollup roadmap, to the lack of financial incentives and the loss of core talent, the problems do not stem from external competition but from unclear direction and structural internal friction.

With Vitalik reflecting on the existing roadmap and the Ethereum Foundation promoting internal reforms, Ethereum stands at a critical turning point. Whether it can shift from ideology back to clear goals and execution efficiency will determine if it regains vitality or continues to test the market's patience.

Against this backdrop, Vitalik suggested that L2s reposition their value proposition, turning towards differentiated directions such as privacy enhancement, deep optimization for specific applications, extreme scalability, non-financial use cases, ultra-low latency architecture, or built-in oracles; if they continue to handle ETH-related assets, they should at least reach Stage 1 and strengthen interoperability with the Ethereum mainnet as much as possible.

The following is the original text:

This article is primarily inspired by a recent tweet from Vitalik about changes and the current state of the market. Against the backdrop of a declining market, it's actually difficult to blame any single individual, and I have no intention of making such accusations.

I write this article from the perspective of someone who has collaborated with many Ethereum teams, represented a venture capital fund investing in multiple protocols built on Ethereum, and was once a staunch supporter and advocate of Ethereum and its EVM ecosystem.

But unfortunately, I can hardly say the same anymore. Because I feel that Ethereum is losing its direction (and I'm not the only one who feels this way).

I don't want to discuss ETH's price action, but I also cannot ignore the fact that as the world's second-largest cryptocurrency by market cap, ETH's performance is full of uncertainty. No matter how the global market moves, ETH behaves more like a stablecoin that is 'de-pegging'.

This article aims to discuss: what exactly has happened to Ethereum over the past few years, and why more and more people are losing confidence, or have already completely lost it. Ethereum is not losing to Solana or some other project; Ethereum is losing to itself.

Rollup-Centric Roadmap

When Ethereum proposed the 'Rollup-centric roadmap', almost everyone was excited. The vision it painted was: Rollups (and Validiums) handle scaling, end-user transactions primarily occur on Rollups, and Ethereum exists as a validation layer—that is, prioritizing being the L1 for Rollups rather than directly serving users as an L1.

Compared to developing a brand new L1, developing a Rollup is faster and cheaper, so a future with 'thousands of Rollups coexisting' seemed both realistic and optimistic.

What could possibly go wrong?

As it turns out, everything could go wrong, and almost everything did: meaningless debates, prioritizing ideology over real needs, long-term internal friction within the community, identity crises, and hesitation and delayed abandonment of the Rollup-centric vision.

Everything that could go wrong, did. Most people in the community once viewed Max Resnick as an incompetent and 'evil' figure, only to later realize that he was right on almost all key issues.

During his tenure at Consensys, Max repeatedly pointed out the changes Ethereum needed to make to move forward, but he was met almost exclusively with criticism, with little real support.

The most absurd moment was when the entire industry began seriously discussing questions like: whether a particular L2 is considered part of Ethereum or not, for example:

Viewpoint A: 'Base is an extension of Ethereum, we contribute greatly to the Ethereum ecosystem.'

Viewpoint B: 'Base is not an extension of Ethereum, it is an independent system.'

What on earth are we even discussing?

How does this kind of discussion help Ethereum and its ecosystem move towards a better future? Why are we so seriously debating 'what is Ethereum' and 'what is not Ethereum'? Don't we have more important problems to solve?

If we decide: because Rollups use ETH for gas, they are extensions of Ethereum—that sounds plausible; if we decide: Rollups are not extensions of Ethereum, but applications built on top of Ethereum that benefit from it—that also seems plausible.

Right? Actually, completely wrong.

This so-called 'ideological discussion' is not a discussion at all; it's two self-absorbed cliques yelling at each other, trying to prove they are correct. We don't need PvP (Player vs. Player), we need PvE (Player vs. Environment). The problem is not 'us versus each other', but 'us together facing problems and the future'.

But unfortunately, many people prefer psychological stimulation over even slightly considering that maybe their viewpoint isn't entirely correct.

Technical Ideology Prioritized Over User Needs

Based Rollup, Booster Rollup, Native Rollup, Gigagas Rollup, Keystore Rollup.

Which one is better? Which one is the future? How should they connect?

'This one is the future.' 'No, that one is the future.' 'There's no reason not to develop Based Rollup.' 'Native Rollup is more Ethereum-aligned, they will replace the entire ecosystem.'

All these debates... the end result is that Arbitrum and Base continue to win.

Technical superiority does bring advantages, but not when you're over-differentiating between apples and pears, or oranges and oranges. These solutions are similar enough that users simply don't care. Outside the bubble, nobody cares about these minutiae. One more precompile, one less precompile, doesn't decide the winner.

'Oh, we are the Ethereum-aligned ones, we are closer to Ethereum, embody its core values, users will definitely choose us.'

Let me ask: which values exactly? And which group of users will choose you because of that?

@0xFacet became the first Stage 2 Rollup, a paragon of 'Ethereum alignment'.

But where is it now? Where are its users? Where are the developers? Where are the technical KOLs? Where are those supporters who shouted the narrative of Ethereum ecosystem and alignment? How many people have even heard of Facet? How many applications are on Facet?

I personally have nothing against Facet. I've spoken with its founder multiple times and respect him greatly; he's a great person. But where are all those people who once shouted 'We need more Stage 2 Rollups'? I don't know, and you don't either.

Financial incentives are far stronger than technical incentives. I was a devoted supporter of Taiko, especially admiring their research around Based Rollup: stronger censorship resistance, neutrality, no sequencer downtime risk, L1 validators could even earn more money.

So what's the problem?

The problem is that the economics behind this model don't add up. You can't force people to give up their revenue for the sake of so-called 'alignment'.

Arbitrum promised decentralized sequencers; Scroll promised; Linea, zkSync, Optimism all promised. Where are they now? Where are those sequencers?

Almost every Rollup's documentation has a line like: 'We currently use a centralized sequencer, but have strong intentions to decentralize in the future.' But almost none have delivered on that promise. Metis did it, but whether fortunately or unfortunately, hardly anyone cares about Metis.

Do I think they over-promised initially to please influential ETH maximalists? Yes.

Do I think they genuinely want to decentralize the sequencer internally? Also yes. But it doesn't make economic sense.

Coinbase (Base) has a legal obligation to generate as much profit as possible for the company, and so do other teams. Why actively cut off your own revenue stream? It makes no sense at all.

Only about 5% of Base's revenue flows to Ethereum. Rollups were never extensions of Ethereum.

Taiko had days where it paid more in sequencing fees to Ethereum than it collected in user transaction fees. And companies like Taiko have significant operational costs beyond just paying Ethereum.

The vision of a Based Rollup or 'Ethereum-aligned' Rollup only holds if the team is willing to forgo its own revenue.

I'm not denying the importance of decentralization, security, and permissionlessness. But if your sole goal is to be 'ideologically correct' rather than user-centric, then it's all meaningless.

It is also precisely because of this fragility and the promise of 'Ethereum alignment' that it has attracted a large number of speculators and scammers into this space.

Consequences of the Rollup-Centric Roadmap

Eclipse, Movement, Blast, Gasp (Mangata), Mantra: these protocols were not designed for the long-term future from the start. They easily cloaked themselves in terms like 'Ethereum aligned', 'making Ethereum better', 'bringing SVM to Ethereum'.

Without exception, they all 'rugged' in different forms. All Rollups eventually realized: their tokens are almost useless because fees are paid in ETH, and their tokens have little actual utility. Speculators also realized that by generating enough hype around the Rollup centralization narrative, they could dump almost worthless tokens on retail investors at high prices.

Ethereum never truly acknowledged Polygon as an L2, even though it played a significant role in locking and carrying value for ETH. If you believe Rollups are 'cultural extensions' of Ethereum, then why not acknowledge a project highly tied to Ethereum in terms of security and usage?

Polygon was crucial to Ethereum during the 2021 bull market, contributing significantly to the growth of ETH as an asset. But because it 'doesn't count as an L2', it didn't deserve recognition from the Ethereum community. If Polygon were an L1, its valuation would likely be much higher.

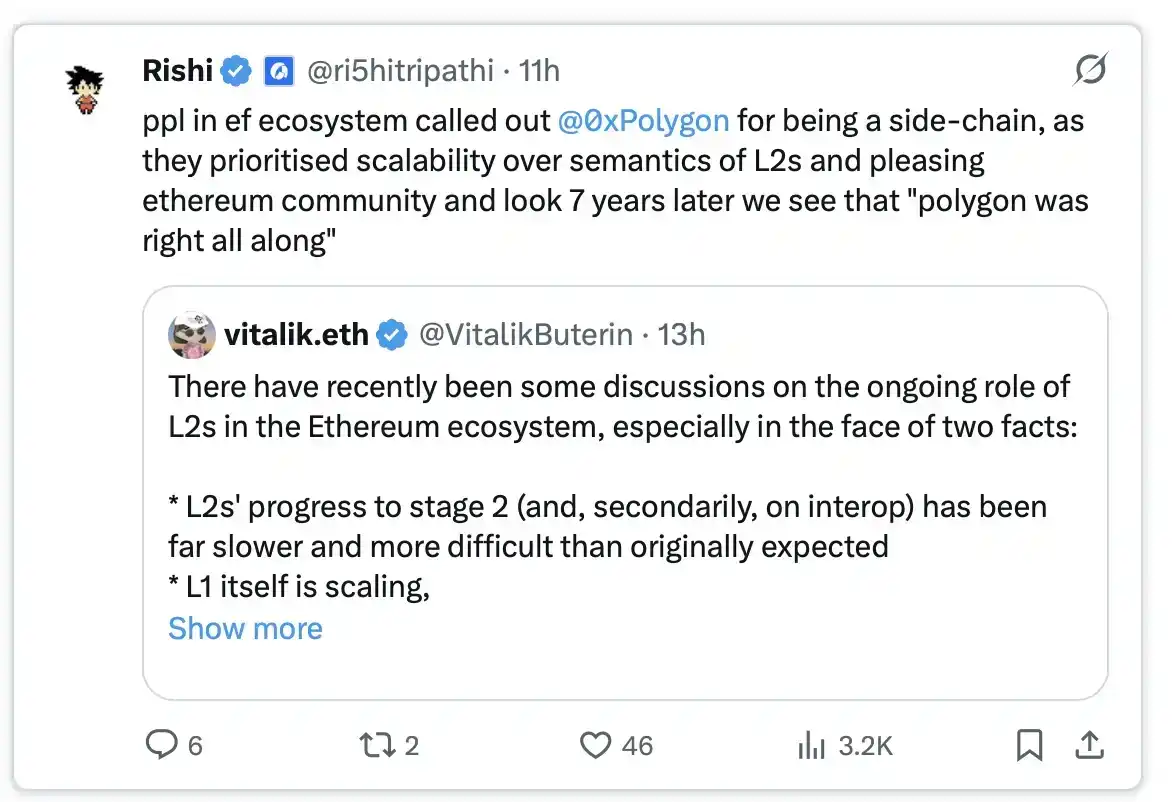

Rishi reviewed the long-standing controversy within the Ethereum ecosystem regarding Polygon: in the early days, Polygon was criticized by parts of the Ethereum community as not being a 'proper' L2 because it was seen as a 'sidechain', but Polygon chose to prioritize solving scalability issues over迎合 L2 semantics or community ideology. Looking back seven years later, Rishi believes the facts prove 'Polygon was right from the start': the pragmatic scaling-first approach has stood the test of time.

Rishi reviewed the long-standing controversy within the Ethereum ecosystem regarding Polygon: in the early days, Polygon was criticized by parts of the Ethereum community as not being a 'proper' L2 because it was seen as a 'sidechain', but Polygon chose to prioritize solving scalability issues over迎合 L2 semantics or community ideology.

Looking back seven years later, Rishi believes the facts prove 'Polygon was right from the start': the pragmatic scaling-first approach has stood the test of time.

First, the 'ultrasound money' narrative: after EIP-1559 and The Merge, ETH's economic model was shaped into a deflationary asset, touted to become a better store of value than Bitcoin. But by 2024, ETH's annual inflation rate turned positive again.

So, the 'ultrasound money' vision only lasted three years? It cannot become a store of value this way. This narrative is dead—and more importantly, it was never valid to begin with. Because ETH was never designed for 'store of value'; that's Bitcoin's mission, and you can't compete with it on that dimension.

Next, Ethereum couldn't decide what its token actually is:

Is it a commodity? Doesn't hold—because the supply is dynamic, and there's staking;

Is it more like a tech stock? Also doesn't hold—because Ethereum doesn't have enough revenue to be valued like a tech company.

Some people even think ETH isn't 'money' at all. So what's happening now? We have to pick a side.

Ethereum cannot simultaneously be something that resembles everything—either you have a globally clear, unified direction, or you fall behind.

Financial Incentives... Again

I still can't understand how a lead engineer like Péter Szilágyi only earns about $100,000 per year. He has been involved since the earliest days of the project, helping Ethereum grow from almost zero to a $450 billion market cap, yet received a return equivalent to only 0.0001% of the market cap.

The most influential and successful protocol in crypto history after Bitcoin,居然 offers neither incentives nor equity. It's easy to defend this with the ideals of 'decentralization, open source, permissionlessness': 'We're not here to make money; we're here to push progress.'

But the problem is, even the most loyal soldiers must be given incentives, otherwise they either leave or take on other projects privately. Péter left, Danny Ryan left, Dankrad Feist went directly to Tempo.

In 2024, Justin Drake and Dankrad accepted advisory roles at EigenLayer and received token allocations, and the community immediately started attacking them.

These people in the Ethereum Foundation earning 'pitiful salaries' (compared to FAANG companies and AI research labs), just because they wanted to earn some money while helping an independent protocol that 'isn't Ethereum itself but hopes to make Ethereum better', were met with collective hatred.

Isn't this absurd? Sometimes I really feel: if you are an honest, hardworking person in Ethereum, you seem to be forbidden from making money, destined to be a laborer for life just for 'recognition' from the Ethereum community.

The Ethereum Foundation has been selling ETH to fund various operations, projects, and research. But maybe, pay the researchers' salaries first?

Zero Tolerance for Adaptation

'Day 1. Ethereum will definitely win. It is the most decentralized blockchain with the highest uptime.'

We hear this rhetoric every day, just like we hear Ethereum defending itself every day.

Yes, Ethereum is expensive and slow. But we have Rollups, just use Rollups, Rollups are Ethereum!

Yes, ETH's price is underperforming everything. But Ethereum has the largest developer ecosystem, a strong foundation, demand will catch up eventually.

Ethereum is the most decentralized blockchain! Solana sucks, it has no client diversity.

Ethereum has 100% uptime! Solana sucks, it has gone down several times.

Ethereum's network activity is lower than Solana's? That's because Solana is full of junk transactions and meme gambling degens, we are the 'moral chain'!

Over the years, it's always the same excuses, the same answers, the same self-comfort. Everything except Ethereum and Rollups is garbage; if Ethereum underperforms on any metric, we say 'it's still Day 1', we know what we're doing, there's no place better than Ethereum in the world.

Everyone is already tired of these excuses repeated over and over by the community.

Ethereum is increasingly like an old, wealthy grandmother, barely able to walk, refusing any innovation, just constantly giving money to her children and grandchildren, letting them parasitize her.

Reform

Just hours before I finished this article, Vitalik tweeted承认: the Rollup-centric roadmap has failed, and a new path needs to be found,转而 scaling L1.

You know what? I'm actually happy when people can recognize their mistakes. It takes courage to admit mistakes publicly. But I'm afraid it might be a bit late. Ethereum has once again found a direction it must take long-term, but overall progress is still slow.

The Ethereum Foundation has indeed seen some changes recently: new leadership, treasury transparency, R&D structure adjustments, etc. At the same time, the Foundation has also started bringing in some young new faces from developer relations and marketing directions, such as Abbas Khan, Binji, Lou3e, and others.

But change must be fast enough. Ethereum must sprint at full speed to prove everyone wrong.

Let's wait and see: after these reforms and changes, can Ethereum once again become an exciting entity,而不是 just an existence of blind faith and disappointment.

Original Link