Author: Zhao Ying

Source: Wall Street News

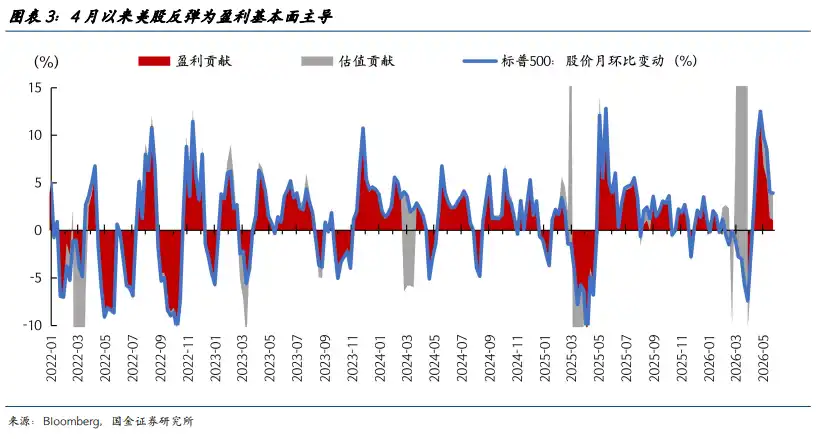

Oil prices are hovering above $100 per barrel, the Strait of Hormuz has not yet returned to normal operations, inflationary and interest rate pressures are re-emerging, and expectations for Federal Reserve rate cuts have become more fragile. According to traditional macroeconomic frameworks, this is not the most comfortable environment for high-valuation tech stocks. Yet, U.S. stocks have reached new highs, and the AI supply chain continues to attract capital.

In a research report dated May 25, Song Xuetao, a macro analyst at Guojin Securities, pointed out: "The current AI market is in a phase of rational fervor, with bubbles present but not out of control." The key to this statement lies not in "bubbles," but in "rational" fervor: Agentic AI evolving from an assistive tool to an autonomous execution tool allows the market to see more clearly for the first time the commercial loop from AI "burning cash" to "making money."

The rational side is that the proliferation of Agent applications has led to rapid growth in Token consumption, inference computing demand, and ARR of leading companies; the fervent side is that valuations have already priced in growth expectations for 2027-2028. As of May 20, the forward price-to-earnings ratio of the "Magnificent Seven" in the U.S. stock market is about 35 times, while the remaining 493 companies in the S&P 500 are about 25 times. This premium implies not ordinary growth stock logic, but the expectation that AI penetration must reach 5 to 8 times the speed of past technological revolutions.

However, what truly determines whether the AI bull market can continue is not a single quarter's performance or a single killer application, but three variables: in the short term, watch for liquidity shocks, especially from oil prices, inflation, interest rates, and unwinding of yen carry trades; in the medium term, watch for industry realization - whether AI penetration speed can match current valuations; in the long term, watch for harder constraints like energy, power grids, employment, social resistance, and hardware technology disruptions.

Agents Shift from "Co-pilot" to "Pilot," Market Begins to Reward Capex

In the past round of AI trading, the market's greatest concern was the speed at which giants spent money: massive investments in data centers, GPUs, and cloud infrastructure, with unclear paths to revenue recovery. The change with Agentic AI is that it is no longer just a Copilot-style assistive tool but is evolving towards an Autopilot-style autonomous execution tool.

This brings two results.

First, Token consumption is reaccelerating. The initial wave of demand after GPT's emergence came from improved model capabilities. The second wave after Agent deployment comes from the explosion in inference computing. Autonomous task execution means longer context, more complex steps, and more frequent model calls. Inference is no longer a byproduct after training but becomes the main battleground for sustained computing power consumption.

Second, revenue expectations are being revised upward. Following the proliferation of representative Agent applications like Openclaw and Claude Cowork, Annual Recurring Revenue for model vendors has grown rapidly. Mid-year estimates cited in the material show Anthropic's full-year ARR expectation has been raised from $90 billion at the start of the year to $440 billion, doubling on average every six weeks. If this trend continues, ARR could exceed $3 trillion next year.

This explains why the market no longer simply punishes Capex. As long as revenue growth is fast enough, capital expenditure shifts from a burden to a moat. Therefore, companies like Nvidia, Broadcom, as well as hardware chains like optical modules and storage, regain support.

Why Can AI Assets Still Rise with Oil Above $100?

The rise of AI assets despite rising oil prices is not because macroeconomic risks have disappeared, but because several forces have temporarily outweighed the risks.

First is the diffusion of industrial chain demand. The inference stage requires not only GPUs but also pulls CPUs, optical modules, and storage into the high-growth logic. 800G/1.6T optical modules are tight, and demand for high-end storage is rising. Light Counting predicts that 800G transceiver shipments will more than double by 2026, 1.6T port shipments will grow from a small base in 2025 to tens of millions, and 1.6T chipset sales will exceed $2 billion in 2026, maintaining high growth for the next three years.

Second is the exceptionally strong earnings of tech giants. The first-quarter S&P 500 EPS growth was about 27.1%, the highest since Q4 2021, with Meta, Alphabet, and Amazon contributing 70% of the index's profit increment. As long as these heavyweights continue to earn, the suppressing effect of oil price shocks on the index will be delayed.

Third, U.S. growth has become more reliant on AI infrastructure investment. In the past few quarters, AI infrastructure investment has contributed over half of U.S. GDP growth. Aggregate data like non-farm payrolls and retail sales remain acceptable. Although employment structure has diverged, as long as aggregate data doesn't weaken significantly, the market struggles to immediately shift to stagflation trades.

There's also a more direct factor: large tech companies are less sensitive to oil prices than industries like airlines, delivery, railroads, chemicals, automobiles, and tourism. They fear electricity prices more than oil prices. When traditional real economy sectors are squeezed by oil prices, capital is more likely to flock to AI assets, blending "safe-haven" trades with growth trades.

Valuations Have Already Eaten the Good Days of 2027-2028

The danger of the AI market lies not in the lack of industrial support, but in how quickly the market is pricing it.

The Magnificent Seven's 35x forward P/E vs. the remaining 493 S&P 500 companies' 25x. Behind this valuation gap lies a very smooth future: AI infrastructure continues to expand over the next 3 to 5 years, maintaining high demand for computing power, cloud, data centers, and semiconductors; AI continues to penetrate scenarios like advertising, search, cloud services, office software, code generation, financial risk control, customer service, investment research, and content; both revenue contribution and efficiency improvements materialize simultaneously.

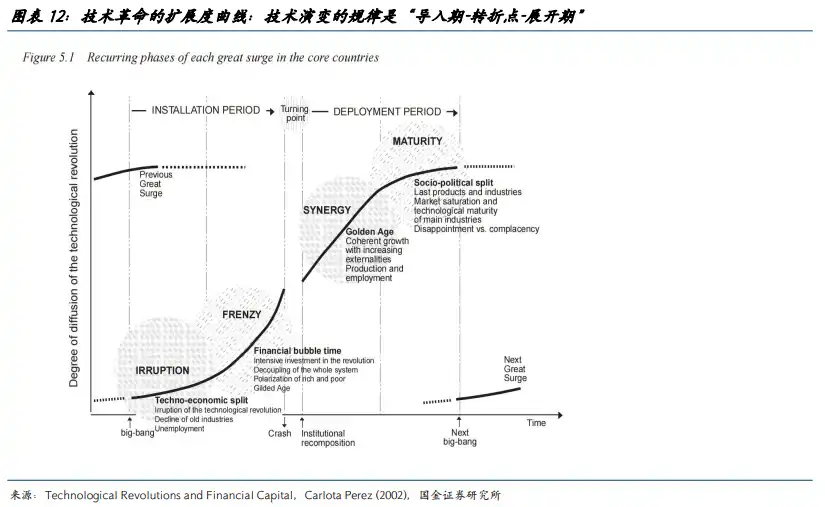

But technological revolutions are rarely this smooth. Electricity took about 40 years from invention to large-scale application in assembly lines, computers about 25 years. The diffusion speed at which AI is currently priced by the market requires it to be 5 to 8 times faster than these general-purpose technologies.

This isn't impossible, but the margin for error is thin. As long as AI application commercialization lags behind capital expenditure, inference demand fails to meet training demand, or depreciation and electricity costs begin to erode profit margins, valuations will react first. The industrial direction being correct does not mean stock prices can be brought forward indefinitely.

The Biggest Short-term Risk: Interest Rates Rising Faster than ARR

The real short-term pressure comes from liquidity.

If the Strait of Hormuz remains closed long-term, keeping oil prices above $100 or even pushing them higher, inflation will spread from energy prices to services, transportation, and raw materials. U.S. PPI in April rose 9.8% year-on-year, the highest since October 2022. Once inflation solidifies, the Federal Reserve's policy path will be forced to be rewritten.

Swap markets are pricing in about 0.8 Fed rate hikes this year, while the ECB and Bank of England are pricing in over 2 hikes. Simultaneously, challenges to Fed independence due to leadership changes and increased internal FOMC divisions are also weakening market confidence in future easing.

Japan is also a gray rhino. Japan has long been the global funding pool for leveraged trades, but yen depreciation and inflationary pressures are forcing the Bank of Japan to signal tightening, with 30-year JGB yields rising above 4%. If Japan's funding costs continue to rise, triggering global carry trade unwinding, high-valuation AI assets will find it hard to remain unscathed.

A preview occurred on May 15: 10-year U.S. Treasury yields broke 4.5%, 30-year yields broke 5%, high-crowding momentum trades cooled, the Philadelphia Semiconductor Index fell about 4% in a single day, and the Nasdaq fell about 1.5%. This isn't evidence of a trend reversal but indicates crowded trades are extremely sensitive to rates.

The most crucial short-term comparison is simple: Can the speed of ARR (Annual Recurring Revenue) upward revisions outpace the speed of interest rate hikes? If not, capital may first retreat to hardware segments with higher certainty; if liquidity worsens further and AI revenue expectations cannot be revised higher, valuation pressures will significantly amplify.

The Tougher Mid-to-Long-Term Issues: Organization, Power, Employment, and Hardware Roadmaps

The mid-term test is industry realization. General-purpose technology revolutions are typically not linear but follow a pattern of "accelerate, decelerate, re-accelerate." First comes the capital wave, then organizational磨合, and finally productivity release. The early internet also experienced investment booms, capital expenditure expansion, and asset bubbles, with true productivity improvements emerging gradually years later.

The current difficulty in pricing AI is that it almost demands rapid adaptation of corporate organizational structures, quick retraining of workers, rapid validation of business models, and no strong social resistance. This speed is not common in human history.

Long-term constraints are even harder.

First is energy and infrastructure. AI data centers require massive electricity and cooling water. Grid expansion, transformers, and energy storage are not variables in a PPT but real bottlenecks. If AI infrastructure continues to push up overall societal electricity costs, regulatory and social pushback will intensify.

Second is employment and consumption. AI can boost corporate efficiency in the short term, reducing demand for jobs like engineers and customer service. But if technological unemployment outpaces new job creation, household consumption power will be weakened. B-side efficiency gains ultimately rely on C-side purchasing power for realization. If non-AI sectors fall into recession, AI cannot flourish alone long-term.

Third is social acceptance. China saw a frenzy of everyone installing Openclaw earlier this year, but in the U.S., public resentment towards data centers pushing up electricity prices and technological unemployment is rising. This will affect AI penetration speed.

Fourth is hardware technology disruption. If an engineering breakthrough similar to a "DeepSeek moment" occurs, dramatically improving computing power, storage, and transmission efficiency, then the hardware segments in shortest supply today could suddenly become oversupplied. The high-growth logic of the hardware chain is not unassailable.

The long-term outlook for the AI industry remains optimistic. If one disregards social矛盾 arising from technological unemployment and production relations restructuring, AI does have the potential to enhance total factor productivity and help the economy escape stagflation pressures. Even if financial markets experience deleveraging mid-journey, the data centers, low-cost technologies, and validated application scenarios left behind could form the foundation for the next round of industrial expansion.

But stock pricing is not the industrial vision itself. What this AI bull market most needs to verify is whether the ARR, ROI, and technology penetration speed currently bet on by the market can continue to be realized in an environment where oil prices, inflation, interest rates, and social constraints are all tightening. The correct direction only explains why there is a bull market; the realization speed determines whether the bubble goes out of control.