Source: Bankless

Author: David Christopher

Original Title: Did Prediction Markets Win the Super Bowl?

Compiled and Edited by: BitpushNews

This year's Super Bowl—Seattle Seahawks vs. New England Patriots—though lacking the star power of last year's Chiefs vs. Eagles matchup with Taylor Swift's presence, marked a turning point: prediction markets were explicitly recognized as genuine competitors to traditional sports betting for the first time.

Two major prediction market platforms, Kalshi and Polymarket, both set up markets around the game, the halftime show, advertisements, and more. Preliminary data paints an interesting and complex picture.

A quick note before we begin: Sportsbooks have not yet aggregated and reported their total betting volume—this will take a few days. Therefore, this analysis is based on predicted data from the sports betting side versus the trading volume on prediction markets.

Sports Betting Predictions: Another Record High, But Growth Slows

The American Gaming Association estimates that U.S. sportsbooks will handle approximately $1.76 billion in bets on Super Bowl LX, setting a new record and representing a year-over-year increase of about 27%. Although specific figures vary slightly depending on the source, most predictions point in the same direction: another record high, continuing the eight-year growth trend since the Supreme Court allowed states to legalize sports betting in 2018.

But the growth rate is clearly slowing. Sports betting is now legal in 39 states and Washington D.C., with only Missouri joining this cycle as a new market—meaning the explosive growth driven by market expansion in previous years is giving way to incremental growth. Against this backdrop, prediction markets have become another factor curbing growth. Ed Birkin of H2 Gambling Capital told Fortune that he estimates prediction markets will account for 80% of the year-on-year increase in betting activity, predicting that trading volume on prediction markets during the entire event will reach $630 million.

Based on currently available data, the performance of prediction markets seems far below that figure.

Kalshi

Kalshi's markets specifically created for the Super Bowl (i.e., contracts directly tied to the game, halftime show, and broadcast) generated significant, but not predicted, trading volume:

-

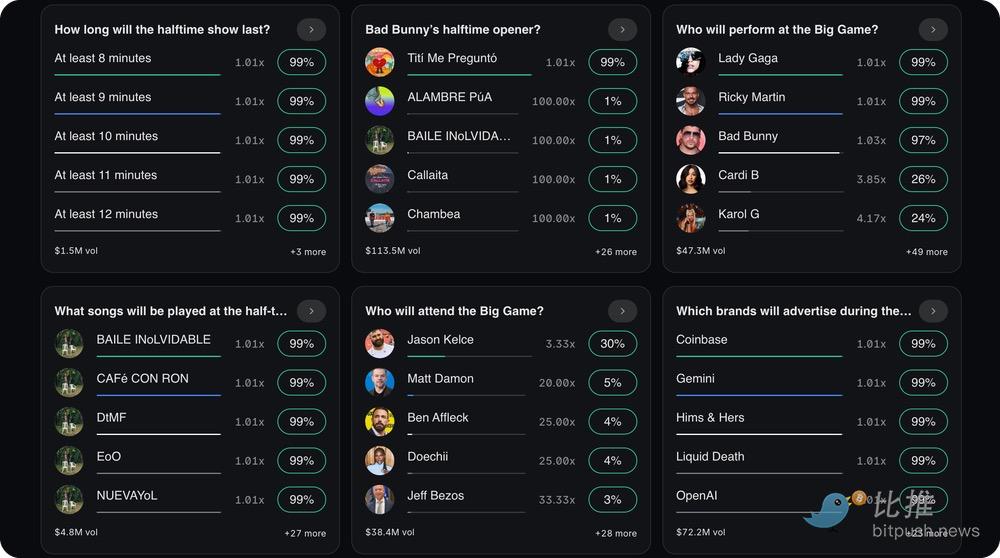

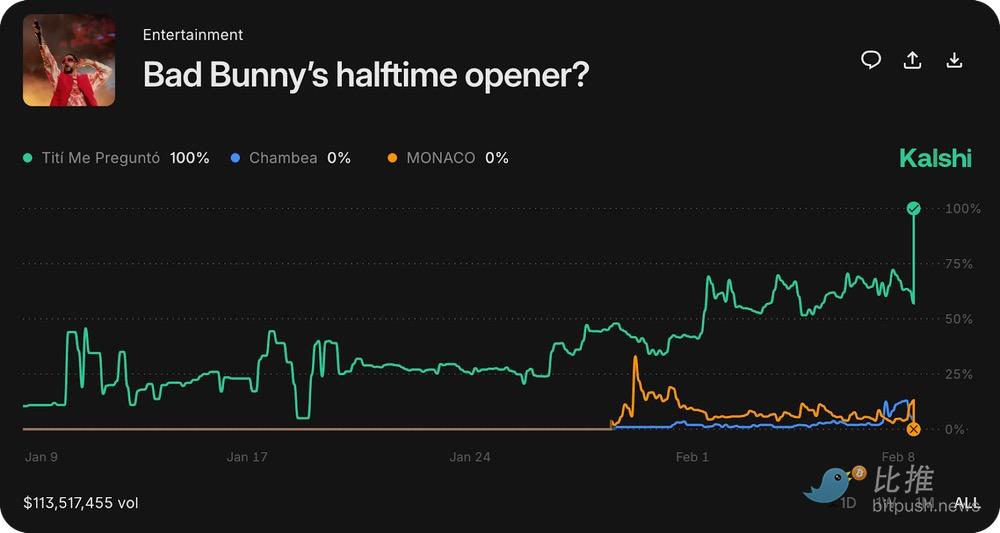

Bad Bunny Halftime Show Opening Song: $113.5 million

-

Which Company Will Air the First Commercial: $72.2 million

-

Who Will Perform at the Game: $47.3 million

Just these top few markets saw a combined trading volume of approximately $233 million, far below the $630 million prediction analysts had for the entire prediction market.

Furthermore, Kalshi's flagship NFL market—a "Who Will Win the Super Bowl" contract open for months throughout the season—saw total trading volume exceed $500 million. But this figure reflects the cumulative trading volume over the entire NFL season, not just Super Bowl weekend. Even so, this is less than a third of the amount sportsbooks are predicted to handle for the Super Bowl alone.

For months, sports betting has constituted the vast majority (over 90%) of Kalshi's total trading volume, thanks to its promotional channels which are on par with, if not better than, those of sportsbooks.

First, Kalshi's federal regulation through the CFTC means U.S. users can access it directly via its mobile app, just like a sports betting app. Coupled with a strong venture capital-backed advertising budget and a partnership with Robinhood, Kalshi stands out. This foundation is paying off: In January alone, Kalshi saw 1.9 million downloads, while DraftKings and FanDuel's new prediction market apps, launched in December, saw combined downloads of less than 100,000 (these apps were launched in states where their traditional sports betting apps are not permitted, but response has been tepid so far). Additionally, DraftKings partnered with Crypto.com last Friday to expand its event contract offerings, indicating that established giants are taking this threat seriously.

Polymarket

Polymarket's similar season-long NFL market saw trading volume of about $700 million—higher than Kalshi's—but the situation is different for its Super Bowl-specific markets. Polymarket's top three Super Bowl markets saw a combined trading volume of approximately $76 million:

-

Main Game Market: $55.26 million

-

Super Bowl MVP: $12 million

-

Who Will Perform the Halftime Show: $9 million

Polymarket lacks Kalshi's regulatory approval in the U.S., meaning American users cannot access it directly through a mobile app. Technically, Polymarket now has a U.S. app after acquiring a CFTC-registered exchange last year, but it is currently rolling out gradually through a waitlist, and its Super Bowl offerings were limited. As of the week before the game, the app didn't even list any sports markets; the full suite of Super Bowl features was only available on its global website.

Therefore, most U.S. users still need to access it via the website, using VPNs, etc. For casual sports bettors, this is not on the same playing field as downloading Kalshi from the App Store.

However, where Polymarket truly shines is its primary use case—information discovery. In its halftime show performer market, Lady Gaga's probability remained stable at around 80% in the days leading up to the game—well before her surprise appearance at the halftime show, which Billboard magazine had not reported on and genuinely surprised everyone I watched with.

Regulatory Progress

All of this is happening against the backdrop of unresolved regulatory conflicts.

Kalshi operates as a federally regulated exchange under the CFTC, which allows its sports contracts to proceed—especially after new CFTC Chairman Michael Selig stated he would not block or cede regulatory authority to the states. State gaming regulators, who oversee sportsbooks, continue to pursue legal challenges against Kalshi and its peers, and many analysts expect these cases to eventually reach the Supreme Court.

For now, prediction markets operate in a gray area, allowing them to cover the nation without needing state-by-state approval—a structural advantage that sportsbooks cannot easily replicate.

Summary

So, did prediction markets live up to the hype for Super Bowl LX? Relative to the $630 million prediction, not quite.

The combined trading volume on the visible top Super Bowl-specific markets across the two leading platforms was approximately $310 million—about half the predicted value. The season-long NFL markets on both platforms achieved huge trading volumes, but that was cumulative over months of football games, not a single-week explosion during Super Bowl weekend.

Context is also important. The 1.9 million downloads Kalshi garnered in January dwarf the combined total of DraftKings and FanDuel's prediction market apps. This pressure is already visibly reflected in stock prices—as observed by Fortune, shares of FanDuel parent Flutter Entertainment have fallen for eight consecutive weeks, their longest losing streak in twenty-three years; DraftKings' stock price is hovering near its lows since 2023, down more than 60% from its all-time high. Bloomberg data shows that over the past three months, market expectations for Flutter's Q4 earnings have been sharply cut by nearly 49%, and DraftKings' expectations have also fallen by 29%. Imagine if someone had bet on Polymarket that "DraftKings will underperform," they might have quietly profited by now.

Prediction markets may not have conquered the Super Bowl overnight, but they have certainly arrived—and for traditional sports betting platforms, the trajectory of this trend is alarming enough.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush